|

市場調查報告書

商品編碼

2035156

日本積層陶瓷電容(MLCC)市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Japan MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

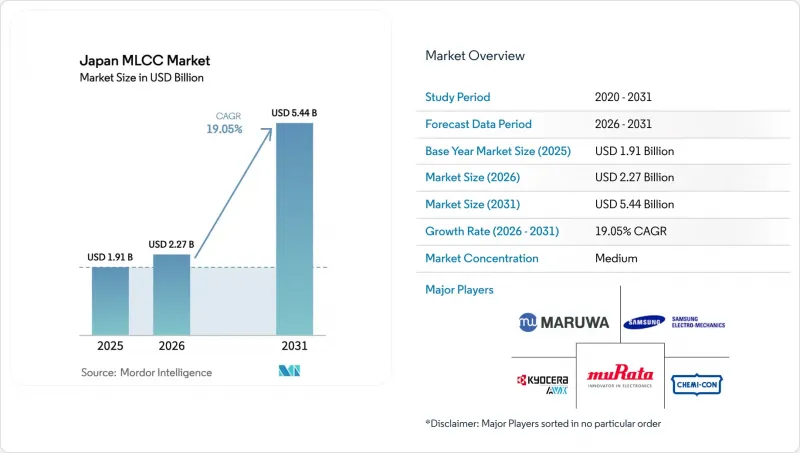

2025年日本MLCC(積層陶瓷電容)市場價值為19.1億美元,預計到2031年將達到54.4億美元,而2026年為22.7億美元,預測期(2026-2031年)複合年成長率為19.05%。

日本汽車電氣化領域的持續主導、5G在全國範圍內的廣泛應用以及對高價值半導體(支持多層陶瓷電容器創新)的投資,共同推動了日本多層陶瓷電容器市場的成長。汽車製造商的電氣化策略與政府對半導體的補貼相結合,為日本多層陶瓷電容器市場在動力傳動系統、電源管理和射頻前端電路等領域創造了清晰的需求前景。同時,由於5G小型基地台的部署和Mini-LED顯示器的普及,對高頻元件的需求不斷成長,而工業邊緣節點則需要長壽命和高可靠性的裝置。日本供應商正投資先進材料和精密製造技術,以區別於韓國和台灣的競爭對手,競爭仍然激烈。然而,與稀土元素採購和出口限制相關的供應鏈風險限制了短期利潤率。

日本MLCC市場的趨勢與洞察

電動車動力系統用多層陶瓷動力傳動系統需求激增

電動車使用的電容器數量是內燃機汽車的6到10倍,高階純電動車每輛車甚至配備超過1萬個多層陶瓷電容器(MLCC)。國內汽車製造商正積極推動電氣化進程,推動了對符合AEC-Q200認證、使用壽命長達20年且動作溫度範圍為-55度C至150度C的組件的需求。新型3225尺寸100V車用MLCC在擴大容量的同時,縮小了封裝體積。因此,隨著一級供應商與國內廠商簽訂多年採購協議,日本MLCC市場擁有良好的長期需求前景。

對Mini-LED和Micro-LED背光燈的需求

當顯示器製造商向Mini-LED背光過渡時,由於每個局部調光段都需要獨立的驅動器和電源濾波器,因此每個面板的電容器數量增加了三到五倍。 DNP的50µm擴散膜可以將面板厚度減小到6mm以下,這使得使用具有卓越ESR控制的0402封裝MLCC變得至關重要。日本供應商正利用其在陶瓷技術方面的專業知識,提供即使在MHz級開關頻率下也能保持電容值的超小型元件,從而降低每個面板的元件成本。

稀土元素和貴金屬價格波動

稀土元素價格劇烈波動,漲幅高達200%,對電介質和電極的利潤率帶來壓力,地緣政治風險每增加1%,進口價格就會上漲0.429%。雖然轉向使用基底金屬電極可以減少對鈀的依賴,但高容量設計仍需要稀土元素摻雜劑。將業務多元化,轉向澳洲和加拿大的精煉廠可以緩解未來的衝擊,但商業化仍需3到5年。

細分市場分析

預計到2025年,1類MLCC將在日本MLCC市場維持61.95%的市場佔有率,並在2031年之前以20.12%的複合年成長率成長。此類MLCC具有低損耗和高溫穩定性等特性,能夠滿足汽車動力傳動系統-55°C至150°C的工作溫度範圍。因此,隨著電動車的普及,以及1類MLCC元件在逆變器直流鏈路緩衝器和ADAS調節器等核心部件的應用,預計日本1類MLCC產品的市場規模將進一步擴大。

製造商憑藉其獨特的陶瓷化學成分和BME堆疊技術獲得了溢價,該技術可將整個溫度範圍內的電容波動控制在±15%以內。此外,隨著固態微型電池研究的深入,由於共用燒結生產線降低了規模化生產成本,1類電池的重要性日益凸顯。

預計到2025年,傳統的201封裝將佔據55.83%的市場佔有率,這反映了智慧型手機和筆記型電腦PCB安裝面積的成熟度。然而,隨著5G設備和穿戴式裝置對更薄基板的需求日益成長,402封裝正以20.05%的複合年成長率引領市場。村田製作所突破性的47µF 0402產品表明,日本MLCC市場正利用其在陶瓷工藝方面的領先優勢,實現極高的體積效率。

隨著介電層厚度減小,其機械脆性增加,因此引入了軟端子技術來分散彎曲應力。一些供應商引進了解析度小於5µm的自動光學檢測技術,即使層數增加,也能有效降低缺陷率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車動力傳動系統(MLCC)的需求正在激增。

- 對迷你LED和微型LED背光的需求

- 5G小型基地台基礎設施的部署

- 物聯網邊緣節點的激增

- 全固態電池研發的一致性。

- 在智慧製造中推廣「零缺陷品質」。

- 市場限制因素

- 稀土元素和貴金屬價格波動

- 汽車PPAP認證瓶頸

- 由於高密度基板變形導致的故障。

- 地緣政治出口管制對製造設備構成風險。

- 宏觀經濟因素的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按介電類型

- 一年級

- 二年級

- 外殼尺寸

- 201

- 402

- 603

- 1005

- 1210

- 其他尺寸

- 透過電壓

- 低電壓(100伏特或以下)

- 中壓(100-500伏特)

- 高壓(超過500伏特)

- MLCC安裝類型

- 金屬帽

- 徑向引線

- 表面黏著技術

- 透過最終用戶應用程式

- 航太/國防

- 車

- 家用電子電器

- 產業

- 醫療設備

- 電力/公共產業

- 溝通

- 其他終端用戶應用程式

第6章 競爭情勢

- 市場集中度

- 重大策略舉措

- 市佔率分析

- 公司簡介

- Kyocera AVX Components Corporation

- Maruwa Co., Ltd.

- Murata Manufacturing Co., Ltd.

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics Co., Ltd.

- Taiyo Yuden Co., Ltd.

- TDK Corporation

- Vishay Intertechnology, Inc.

- Walsin Technology Corporation

- Wurth Elektronik GmbH and Co. KG

- Yageo Corporation

- Panasonic Holdings Corporation

- ROHM Co., Ltd.

- Samwha Capacitor Group Co., Ltd.

- Holy Stone Enterprise Co., Ltd.

- Darfon Electronics Corp.

- Shenzhen Sunlord Electronics Co., Ltd.

- Guangdong Fenghua Advanced Technology Holding Co., Ltd.

- Tai-Tech Advanced Electronics Co., Ltd.

- KEMET Corporation

第7章 市場機會與未來展望

The Japan MLCC market size was valued at USD 1.91 billion in 2025 and estimated to grow from USD 2.27 billion in 2026 to reach USD 5.44 billion by 2031, at a CAGR of 19.05% during the forecast period (2026-2031).

The growth rests on sustained domestic leadership in automotive electrification, national 5G expansion, and high-value semiconductor investment that underpins the innovation of multilayer ceramic capacitors. Automotive OEM electrification strategies, combined with government semiconductor subsidies, provide the Japan MLCC market with clear demand visibility across powertrain, power management, and RF front-end circuits. At the same time, 5G small-cell rollouts and the adoption of Mini-LED displays raise high-frequency component needs, while industrial edge nodes elevate long-life reliability specifications. Competitive intensity remains elevated as Japanese vendors deploy advanced materials and precision manufacturing to defend differentiation against Korean and Taiwanese rivals, yet supply-chain risks tied to rare-earth sourcing and export-control compliance temper near-term margins.

Japan MLCC Market Trends and Insights

EV Powertrain MLCC Surge

Electric vehicles use six to ten times more capacitors than combustion cars, with luxury BEVs exceeding 10,000 MLCCs per unit. Domestic OEMs have pledged aggressive electrification timelines, driving demand for AEC-Q200-qualified parts rated from -55 °C to 150 °C and with 20-year lifetimes. New 100 V automotive MLCCs in the 3225 size extend capacitance thresholds while reducing pack volume. The outcome is long-cycle visibility for the Japan MLCC market as Tier-1 suppliers lock multi-year sourcing contracts with domestic vendors.

Mini-LED and Micro-LED Backlighting Demand

Display makers moving to Mini-LED backlights multiply the number of per-panel capacitor counts three to five times because every local-dimming segment includes its own driver and power filter. DNP's 50 µm diffuser film enables sub-6 mm panel thickness, forcing the use of 0402-size MLCCs with superior ESR control. Japanese suppliers leverage ceramic know-how to deliver ultra-compact parts that maintain capacitance at MHz switching frequencies, unlocking higher dollar-content per panel.

Rare-Earth and Precious-Metal Price Volatility

Sudden 200% swings in rare-earth costs squeeze dielectric and electrode margins, with every 1% uptick in geopolitical risk lifting unit import prices 0.429%. Base-metal-electrode migration eases palladium exposure, yet high-capacitance designs still rely on rare-earth dopants. Diversification into Australian and Canadian refiners mitigates future shocks but remains three to five years from commercial scale.

Other drivers and restraints analyzed in the detailed report include:

- 5G Small-Cell Infrastructure Roll-out

- IoT Edge-Node Proliferation

- Automotive PPAP Qualification Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Class 1 MLCCs retained a 61.95% share of the Japan MLCC market in 2025 and are expected to widen their revenue at a 20.12% CAGR through 2031. The class's low-loss, temperature-stable behavior satisfies -55 °C to 150 °C automotive powertrain envelopes. Consequently, Class 1 parts, which anchor inverter DC-link buffers and ADAS regulators, allow the Japan MLCC market size for Class 1 products to rise alongside EV penetration.

Manufacturers capture pricing premiums through proprietary ceramic chemistries and BME stacks that maintain capacitance drift within +-15% across the entire temperature spectrum. Solid-state micro-battery research further broadens Class 1 relevance as shared sintering lines cut scale-up costs.

The legacy 201 format held 55.83% share in 2025, mirroring entrenched smartphone and notebook PCB footprints. Yet the 402 format leads with 20.05% CAGR because 5G handsets and wearables adopt thinner boards. Murata's 47 µF 0402 milestone highlights how the Japanese MLCC market leverages ceramic process leadership to achieve extreme volumetric efficiency.

Thinner dielectric stacks heighten mechanical fragility, prompting soft-termination launches that disperse flex stress. Vendors deploying automated optical inspection at sub-5 µm resolution help sustain defect yields even as layer counts climb.

The Japan MLCC Market Report is Segmented by Dielectric Type (Class 1, Class 2), Case Size (201, 402, 603, 1005, 1210, Other Case Sizes), Voltage (Low Voltage, Mid Voltage, High Voltage), MLCC Mounting Type (Metal Cap, Radial Lead, Surface Mount), End-User Application (Aerospace and Defence, Consumer Electronics, Industrial, Medical Devices, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Kyocera AVX Components Corporation

- Maruwa Co., Ltd.

- Murata Manufacturing Co., Ltd.

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics Co., Ltd.

- Taiyo Yuden Co., Ltd.

- TDK Corporation

- Vishay Intertechnology, Inc.

- Walsin Technology Corporation

- Wurth Elektronik GmbH and Co. KG

- Yageo Corporation

- Panasonic Holdings Corporation

- ROHM Co., Ltd.

- Samwha Capacitor Group Co., Ltd.

- Holy Stone Enterprise Co., Ltd.

- Darfon Electronics Corp.

- Shenzhen Sunlord Electronics Co., Ltd.

- Guangdong Fenghua Advanced Technology Holding Co., Ltd.

- Tai-Tech Advanced Electronics Co., Ltd.

- KEMET Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV Powertrain MLCC Surge

- 4.2.2 Mini-LED and Micro-LED Backlighting Demand

- 4.2.3 5G Small-Cell Infrastructure Roll-out

- 4.2.4 IoT Edge-Node Proliferation

- 4.2.5 Solid-state Battery RandD Alignment.

- 4.2.6 Smart-Manufacturing Quality-Zero Defect Push.

- 4.3 Market Restraints

- 4.3.1 Rare-earth and Precious-metal Price Volatility

- 4.3.2 Automotive PPAP Qualification Bottlenecks

- 4.3.3 High-Density Board Warpage Failures.

- 4.3.4 Geopolitical Export-Control Risks on Fabrication Tools.

- 4.4 Impact of Macroeconomic Factors

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Dielectric Type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 By Case Size

- 5.2.1 201

- 5.2.2 402

- 5.2.3 603

- 5.2.4 1005

- 5.2.5 1210

- 5.2.6 Other Case Sizes

- 5.3 By Voltage

- 5.3.1 Low Voltage (less than or equal to 100 V)

- 5.3.2 Mid Voltage (100 - 500 V)

- 5.3.3 High Voltage (above 500 V)

- 5.4 By MLCC Mounting Type

- 5.4.1 Metal Cap

- 5.4.2 Radial Lead

- 5.4.3 Surface Mount

- 5.5 By End-User Application

- 5.5.1 Aerospace and Defence

- 5.5.2 Automotive

- 5.5.3 Consumer Electronics

- 5.5.4 Industrial

- 5.5.5 Medical Devices

- 5.5.6 Power and Utilities

- 5.5.7 Telecommunication

- 5.5.8 Other End-User Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Kyocera AVX Components Corporation

- 6.4.2 Maruwa Co., Ltd.

- 6.4.3 Murata Manufacturing Co., Ltd.

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics Co., Ltd.

- 6.4.6 Taiyo Yuden Co., Ltd.

- 6.4.7 TDK Corporation

- 6.4.8 Vishay Intertechnology, Inc.

- 6.4.9 Walsin Technology Corporation

- 6.4.10 Wurth Elektronik GmbH and Co. KG

- 6.4.11 Yageo Corporation

- 6.4.12 Panasonic Holdings Corporation

- 6.4.13 ROHM Co., Ltd.

- 6.4.14 Samwha Capacitor Group Co., Ltd.

- 6.4.15 Holy Stone Enterprise Co., Ltd.

- 6.4.16 Darfon Electronics Corp.

- 6.4.17 Shenzhen Sunlord Electronics Co., Ltd.

- 6.4.18 Guangdong Fenghua Advanced Technology Holding Co., Ltd.

- 6.4.19 Tai-Tech Advanced Electronics Co., Ltd.

- 6.4.20 KEMET Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

用於MLCC內電極的鎳漿-2026年至2032年全球市佔率及排名、總收入及需求預測

用於MLCC內電極的鎳漿-2026年至2032年全球市佔率及排名、總收入及需求預測 英國陶瓷電容器(MLCC):市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

英國陶瓷電容器(MLCC):市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 用於MLCC電極的鎳漿(<200nm)—全球市場佔有率和排名、總收入和需求預測(2025-2031年)MLCC鎳內電極膏:全球市佔率排名、總銷售額及需求預測,2025-2031年中國MLCC市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)中壓MLCC:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太地區MLCC:市場佔有率分析、產業趨勢與成長預測(2025-2030年)個人電腦和筆記型電腦用 MLCC——市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)北美MLCC:市場佔有率分析、產業趨勢與成長預測(2025-2030年)印度MLCC:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

用於MLCC電極的鎳漿(<200nm)—全球市場佔有率和排名、總收入和需求預測(2025-2031年)MLCC鎳內電極膏:全球市佔率排名、總銷售額及需求預測,2025-2031年中國MLCC市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)中壓MLCC:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太地區MLCC:市場佔有率分析、產業趨勢與成長預測(2025-2030年)個人電腦和筆記型電腦用 MLCC——市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)北美MLCC:市場佔有率分析、產業趨勢與成長預測(2025-2030年)印度MLCC:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)