|

市場調查報告書

商品編碼

2035045

日本太陽能市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Japan Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

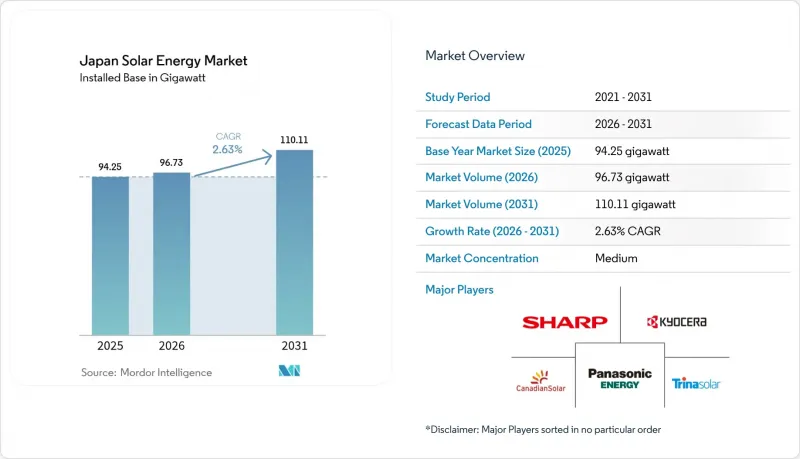

據估計,日本太陽能發電市場在 2025 年將達到 94.25 吉瓦,預計到 2031 年將達到 110.11 吉瓦,而 2026 年為 96.73 吉瓦,預測期內(2026-2031 年)複合年成長率為 2.63%。

自從上網電價補貼(FIT)制度過渡到高價購電制度以來,市場持續成長。高價購電制度鼓勵開發商順應批發價格趨勢,整合儲能系統,降低消費者成本。屋頂太陽能板核准流程的簡化、東京強制自用電政策以及組件和電池價格的下降,都擴大了分散式系統的潛在市場。儘管來自海外製造商的競爭正在降低硬體成本,但日本國內企業正在加速開發鈣鈦礦材料、整合儲能系統和能源管理軟體,以維持產品價值。資料中心電力需求的成長以及企業脫碳目標的推進,正透過長期購電協議擴大企劃案融資融資管道。

日本太陽能發電市場的趨勢與洞察

2050年實現淨零排放藍圖及上網電價補貼→上網電價獎勵

日本太陽能市場從固定價格購電模式轉向高於批發價格的溢價購電模式,使其結構與標準電力市場的經濟原則相符。截至2024年2月,固定價格購電計畫(FIP)已認證了1036個項目,其中包括518兆瓦的太陽能發電項目。政府鼓勵開發商將組件和電池結合起來,以抓住尖峰時段時段的價格差。 2025會計年度發布的政府公告確認了對早期太陽能投資的新預算撥款,顯示了政策的持續承諾。隨著開發商投資於可調節發電容量以對沖價格風險,專案結構現在整合了預測軟體、虛擬電廠(VPP)功能和輔助服務收入。這些調整鞏固了日本太陽能市場的長期競爭力,同時也減輕了公共補貼的負擔。

屋頂太陽能發電的強制性建築規範要求(東京、神奈川縣)

東京市一項新規則將於2025年4月生效,該規定強制要求所有建築占地面積超過2000平方公尺的新建建築安裝太陽能電池板,徹底改變了城市建設標準。這項新規的執行義務由建築公司而非最終業主承擔,簡化了流程,並確保了年度最低安裝量。此外,東京市政府也提供每千瓦最高8萬日圓的補貼,鼓勵採用高效能節能系統,進一步提升盈利。初步實地調查數據顯示,建築公司已將太陽能發電系統納入設計流程,東京都會區的現場發電模式正逐漸普及。其他幾個都道府縣也正在頒布類似的法令,這預示著一系列法規將在全國範圍內產生連鎖反應,從而支撐日本太陽能市場的持續需求。

九州及北海道電網擁塞及限電

2023會計年度,日本發電量削減量飆升至1.76太瓦時,九州地區削減率達6.7%。這主要是由於各地區間聯網線路有限,柔軟性的基本負載核子反應爐難以吸收白天的太陽能尖峰發電量。電力公司正在試運行人工智慧驅動的電壓調節器,該技術已成功將穩定裝置的啟動次數減少了高達70%,證明了其技術可行性。政策制定者也在努力製定負電價機制和經濟調度方案,但具體時間表尚未確定。在基礎設施完善之前,日本太陽能發電市場的開發商要麼需要安裝儲能電池,要麼需要遷移電廠,要麼需要在電力供應過剩時期承受利潤下滑的局面。

細分市場分析

日本太陽能市場規模預計到2025年將達到94.25吉瓦,到2031年將維持2.63%的複合年成長率,並由於缺乏商業性可行的集中式光伏發電(CSP)系統,將保持100%的市場佔有率。單晶PERC組件的平均效率為21.5%,並持續在公用事業和商業項目中取代多晶矽組件。異質結電池和背接觸電池雖然成本更高,但由於其效率優勢足以彌補較高的成本,因此在屋頂空間有限的住宅維修項目中越來越受歡迎。

鈣鈦礦疊層電池處於創新前沿,一個聯盟的目標是到2040年將國內生產線產能提升至20吉瓦,以重振製造業競爭力。初步試驗表明,其效率可達15.6%,重量減輕60%,從而拓展了其可安裝的表面範圍,例如建築外牆和車身。商業性化應用將取決於其耐濕性。加速劣化測試表明,在沿海環境中,鈣鈦礦疊層電池的劣化比矽電池快15%,因此封裝技術的研究和開發仍在進行中。國內製造商將這項技術視為彌補因海外晶體矽(c-Si)外流而造成的價值損失的途徑,2024年晶體矽組件進口量佔國內總進口量的68%。

《日本太陽能市場報告》按技術(光伏和聚光型太陽熱能發電)、併網類型(併網和離網)以及最終用戶(公用事業規模、商業和工業以及住宅)進行細分。市場規模和預測以裝置容量(GW)表示。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 2050年實現淨零排放藍圖及上網電價補貼→上網電價獎勵

- 根據《建築標準法》,強制要求屋頂安裝太陽能發電設施(東京、神奈川縣)

- 組件和電池價格的下降將提高專案的內部收益率(IRR)。

- 資料中心電力需求的激增正在推動企業購電協議(PPA)的簽訂。

- 輕質鈣鈦礦太陽能電池為建築外牆和汽車外殼開闢了新的應用領域。

- 「零成本太陽能發電」的訂閱模式正在加速其在普通家庭中的普及。

- 市場限制因素

- 九州及北海道電網擁塞及限電

- 土地短缺/地上工程分區規定嚴格

- 負責管理太陽能發電廢棄物和不斷上漲的回收成本

- 高壓太陽能發電和儲能系統安裝領域熟練勞動力短缺。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- PESTEL 分析

第5章 市場規模與成長預測

- 透過技術

- 太陽能發電(PV)

- 聚光型太陽熱能發電(CSP)

- 按電網連接類型

- 並網型

- 離網

- 最終用戶

- 公用事業規模

- 商業和工業(C&I)

- 住宅

- 基於成分的(定性分析)

- 光學模組/面板

- 逆變器(組串式、集中式、微型)

- 安裝和追蹤系統

- 系統平衡和電氣設備

- 儲能和混合整合

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、合作、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Sharp Corporation

- Kyocera Corporation

- Panasonic Energy Co.

- Canadian Solar Inc.

- Trina Solar Co. Ltd.

- JinkoSolar Holding Co. Ltd.

- JA Solar Technology Co. Ltd.

- LONGi Green Energy Technology Co. Ltd.

- Hanwha Q CELLS

- First Solar Inc.

- Mitsubishi Electric Corporation

- Toshiba Energy Systems & Solutions

- Omron Corporation

- Nihon Techno Co. Ltd.

- SoftBank Energy(SB Power)

- Eurus Energy Holdings

- RENOVA Inc.

- Shizen Energy Inc.

- West Holdings Corporation

- Sekisui Chemical(Perovskite R&D)

第7章 市場機會與未來展望

The Japan Solar Energy Market size was valued at 94.25 gigawatt in 2025 and estimated to grow from 96.73 gigawatt in 2026 to reach 110.11 gigawatt by 2031, at a CAGR of 2.63% during the forecast period (2026-2031).

Growth continues even after the shift from the Feed-in Tariff to the Feed-in Premium scheme, which encourages developers to follow wholesale price signals, integrated battery storage, and lower consumer levies. Faster permitting for rooftop arrays, mandatory on-site generation rules in Tokyo, and falling module plus battery prices have enlarged the addressable base for distributed systems. Competitive pressure from overseas manufacturers decreases hardware costs, while domestic firms accelerate perovskite research, co-located storage, and energy-management software to retain value. Rising power demand from data centers and corporate decarbonization targets deepens the project finance pool through long-term power-purchase agreements.

Japan Solar Energy Market Trends and Insights

Net-zero 2050 roadmap & FIT -> FIP incentives

The move from a guaranteed tariff to a premium above the wholesale price has realigned the Japanese solar energy market with standard power-market economics. By February 2024, the FIP program had accredited 1,036 projects, including 518 MW of solar, driving developers to pair modules with batteries to capture peak-price spreads. Government notices released for fiscal 2025 confirm fresh budget lines for early-stage solar investments, signaling ongoing policy commitment. As developers invest in dispatchable capacity to hedge price risk, project structures now integrate forecasting software, virtual power-plant functions, and ancillary service revenues. These adaptations anchor the long-term competitiveness of the Japanese solar energy market while easing public-subsidy exposure.

Mandatory rooftop-PV building codes (Tokyo, Kanagawa)

Tokyo's regulation that all new buildings above 2,000 m2 must include solar panels from April 2025 has changed the baseline for urban construction. Compliance obligations rest with the builder, not the end-owner, simplifying logistics and placing a floor under annual installation volumes. The city's parallel subsidy of up to JPY 80,000 per kW supports high-efficiency systems, further lifting return profiles. Early site inspection data indicate that builders now embed solar procurement into design workflows, normalizing on-site generation in the capital. Several prefectures are drafting similar ordinances, pointing toward a potential nationwide regulatory cascade that would underpin sustained demand in the Japanese solar energy market.

Grid congestion & curtailment in Kyushu/Hokkaido

Curtailment jumped to 1.76 TWh in fiscal 2023, with Kyushu hitting a 6.7% rate because limited inter-regional links and inflexible baseload reactors leave little room for midday solar peaks. Utilities are piloting AI-based voltage control that has cut stabilizer activations by up to 70%, showing a technical path forward. Policymakers also draft negative-pricing rules and economic dispatch, but timelines remain unsettled. Until infrastructure aligns, Japanese solar energy market developers must add batteries, reposition plants, or accept revenue cannibalization during oversupply events.

Other drivers and restraints analyzed in the detailed report include:

- Falling module and battery prices improve project IRRs

- Data-center electricity surge spurring corporate PPAs

- Skilled-labour gap for HV solar-plus-storage installs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Japan's solar energy market size for photovoltaic technology stood at 94.25 GW in 2025, locking in a 2.63% CAGR toward 2031 and retaining a 100.00% segment share as concentrated solar power (CSP) remains commercially absent. Mono-crystalline PERC modules averaged 21.5% efficiency and continued to displace poly-silicon panels across utility and commercial projects. Heterojunction and back-contact cells, though premium-priced, gained mindshare in residential retrofits where roof space is scarce, and efficiency premiums justify higher costs.

Perovskite tandem cells sit on the innovation frontier, with a consortium targeting 20 GW of domestic line capacity by 2040 to reclaim manufacturing competitiveness. Pilot efficiencies of 15.6% and a 60% weight reduction expand viable mounting surfaces to facades and vehicular skins. Commercial uptake hinges on humidity resilience; accelerated aging tests show 15% faster degradation than silicon under coastal conditions, prompting encapsulation R&D. Domestic manufacturers view the technology as a path to recoup value lost to overseas c-Si imports, which captured 68% of the 2024 module inflow.

The Japan Solar Energy Market Report is Segmented by Technology (Solar Photovoltaic and Concentrated Solar Power), Grid Type (On-Grid and Off-Grid), and End-User (Utility-Scale, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

List of Companies Covered in this Report:

- Sharp Corporation

- Kyocera Corporation

- Panasonic Energy Co.

- Canadian Solar Inc.

- Trina Solar Co. Ltd.

- JinkoSolar Holding Co. Ltd.

- JA Solar Technology Co. Ltd.

- LONGi Green Energy Technology Co. Ltd.

- Hanwha Q CELLS

- First Solar Inc.

- Mitsubishi Electric Corporation

- Toshiba Energy Systems & Solutions

- Omron Corporation

- Nihon Techno Co. Ltd.

- SoftBank Energy (SB Power)

- Eurus Energy Holdings

- RENOVA Inc.

- Shizen Energy Inc.

- West Holdings Corporation

- Sekisui Chemical (Perovskite R&D)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Net-zero 2050 roadmap & FIT -> FIP incentives

- 4.2.2 Mandatory rooftop-PV building codes (Tokyo, Kanagawa)

- 4.2.3 Falling module + battery prices improve project IRRs

- 4.2.4 Data-center electricity surge spurring corporate PPAs

- 4.2.5 Lightweight perovskite PV opens facade & vehicle skins

- 4.2.6 "Zero-Yen Solar" subscription model unlocks households

- 4.3 Market Restraints

- 4.3.1 Grid congestion & curtailment in Kyushu/Hokkaido

- 4.3.2 Scarce land / strict zoning for ground-mount projects

- 4.3.3 PV waste-management liability & recycling cost spike

- 4.3.4 Skilled-labour gap for HV solar-plus-storage installs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.2 Concentrated Solar Power (CSP)

- 5.2 By Grid Type

- 5.2.1 On-Grid

- 5.2.2 Off-Grid

- 5.3 By End-User

- 5.3.1 Utility-Scale

- 5.3.2 Commercial and Industrial (C&I)

- 5.3.3 Residential

- 5.4 By Component (Qualitative Analysis)

- 5.4.1 Solar Modules/Panels

- 5.4.2 Inverters (String, Central, Micro)

- 5.4.3 Mounting and Tracking Systems

- 5.4.4 Balance-of-System and Electricals

- 5.4.5 Energy Storage and Hybrid Integration

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Sharp Corporation

- 6.4.2 Kyocera Corporation

- 6.4.3 Panasonic Energy Co.

- 6.4.4 Canadian Solar Inc.

- 6.4.5 Trina Solar Co. Ltd.

- 6.4.6 JinkoSolar Holding Co. Ltd.

- 6.4.7 JA Solar Technology Co. Ltd.

- 6.4.8 LONGi Green Energy Technology Co. Ltd.

- 6.4.9 Hanwha Q CELLS

- 6.4.10 First Solar Inc.

- 6.4.11 Mitsubishi Electric Corporation

- 6.4.12 Toshiba Energy Systems & Solutions

- 6.4.13 Omron Corporation

- 6.4.14 Nihon Techno Co. Ltd.

- 6.4.15 SoftBank Energy (SB Power)

- 6.4.16 Eurus Energy Holdings

- 6.4.17 RENOVA Inc.

- 6.4.18 Shizen Energy Inc.

- 6.4.19 West Holdings Corporation

- 6.4.20 Sekisui Chemical (Perovskite R&D)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

太陽能市場規模、佔有率和成長分析:按產品/組件、技術、安裝類型、併網類型、最終用途、電源和地區分類-2026-2033年產業預測

太陽能市場規模、佔有率和成長分析:按產品/組件、技術、安裝類型、併網類型、最終用途、電源和地區分類-2026-2033年產業預測 太陽能發電系統市場:2026-2032年全球市場預測(依產品、系統規模、安裝類型及應用分類)

太陽能發電系統市場:2026-2032年全球市場預測(依產品、系統規模、安裝類型及應用分類) 2026年全球太陽能市場報告

2026年全球太陽能市場報告 太陽能發電系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、安裝類型、最終用戶、功能及設備分類

太陽能發電系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、安裝類型、最終用戶、功能及設備分類 東南亞太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙太陽能:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)越南太陽能市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

東南亞太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙太陽能:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)越南太陽能市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 太陽能解決方案市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭格局分類,2021-2031年)印尼太陽能市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

太陽能解決方案市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭格局分類,2021-2031年)印尼太陽能市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)