|

市場調查報告書

商品編碼

1939652

東協施工機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)ASEAN Construction Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

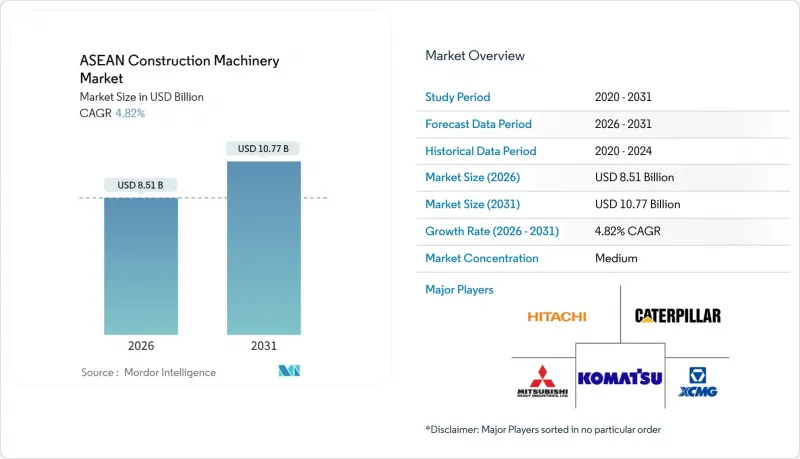

預計東協施工機械市場規模將從 2025 年的 81.2 億美元成長到 2026 年的 85.1 億美元,到 2031 年將達到 107.7 億美元,2026 年至 2031 年的複合年成長率為 4.82%。

這一市場動能反映了基礎設施超級週期,從印尼東加里曼丹的新首都到泰越高鐵走廊,無不反映這一點。工業園區持續的外商直接投資、鎳礦開採資本投資的復甦以及現場數位化的加速,持續推動關鍵設備類別的更新換代。同時,在承包商在地化需求的推動下,中國製造商正在快速擴張,重塑競爭格局和價格定位。電氣化設備和氫燃料電池原型機的出現預示著新的機遇,這得益於政府日益嚴格的排放法規和建設公司永續性的推動。儘管中美貿易緊張局勢導致的供應鏈中斷以及持續的操作員短缺仍然是阻礙成長的主要因素,但積極的技能培訓計劃和採購多元化戰略正在逐步抵消這些風險。

東協施工機械市場趨勢與洞察

印尼IKN資本建設推動基礎建設超級週期

努桑塔拉計畫的基礎建設分階段實施,採購週期將持續到2040年代中期。五家私人投資者承諾投入超過2.4兆印尼幣,用於支持住宅區、綜合用途區和關鍵基礎設施建設,以期在2025年之前實現里程碑目標。公共部門預算撥款超過100兆印尼幣,其中包括利用數位雙胞胎技術進行路段設計。這些計劃的規模保證了挖掘機、裝載機、混凝土泵和專用起重設備的訂單量,同時也鼓勵原始設備製造商(OEM)實現零件本地化供應。然而,水泥運輸延誤和持續的預算調整帶來了執行風險,並可能抑制近期設備訂購。計畫中的公私合營(PPP)模式預計在未來十年透過擴大貸款機構基礎來緩解資金籌措壓力。

鎳礦開採熱潮推動了對超大型挖土機的需求

印尼作為全球最大的鎳生產國,帶動了超大型設備的訂單訂單。 120噸級液壓挖土機EX1200於2024年11月開始量產,目前主要針對新礦開發及現有礦場的擴建。預計到2029年,電池材料需求的成長將顯著增加礦山設備的規模。原始設備製造商(OEM)正在展示專為紅土礦開採條件客製化的100噸和150噸級原型機,而當地承包商則力爭實現兩位數的市場佔有率成長。鎳價回升鼓勵礦場進行前期投資,但更嚴格的環境審核可能需要額外的技術投資。

初始資本投資增加及企劃案融資利率收緊

隨著全球利率週期波動,利息負擔日益加重,提高了新設備採購的門檻利率。政府預算調整,尤其是在印尼削減了2025年基礎設施預算,限制了公共部門的競標。負債累累的國有承包商仍在為短期債務進行再融資,但利潤下滑限制了它們自籌資金資金籌措機械設備的能力。區域性貸款文件標準化措施旨在將保險和退休資本投入長期基礎設施投資,並緩解中期資金籌措壓力。擁有大量建築相關貸款的銀行正在推出與永續發展掛鉤的貸款工具,以激勵低排放機械的採用。

細分市場分析

到2025年,挖土機將佔東協施工機械市場總規模的35.10%,以鞏固其在該領域的領先地位。大噸位挖土機將主導印尼的採礦市場,而中型挖土機仍廣泛用於公路和鐵路計劃。在市政排水和通訊線路建設的推動下,能夠在擁擠的城市環境中同時進行挖掘和裝載的後鏟式裝載機預計將實現最高的複合年成長率,達到9.86%。履帶挖土機(20-30噸級)佔印尼訂單的四分之三以上,展現了其在複雜地形中的多功能性。由於港口擴建,裝載機的需求將保持強勁,而由於高速公路復線化項目,平地平土機和攤舖機的需求將會增加。加長型堆高機和自動卸貨卡車雖然銷量仍然較低,但在工業園區倉庫和礦物運輸路線中仍保持著一定的市場需求。

採用趨勢表明,整合控制系統正穩步發展,這推動了二手市場對新型號設備的需求。租賃公司擴大將遠端資訊處理合約納入月費,這獎勵承包商選擇連網設備,並擴大了業務收益的潛在市場。本地組裝正利用優惠關稅和擴大信用額度,降低中小型承包商的購買門檻,並維持關鍵土木機械的更換週期。

土木工程和施工機械在東協施工機械市場中佔53.72%的佔有率,是成長最快的應用領域,年複合成長率達4.83%。諸如努桑塔拉城建設項目和跨境鐵路走廊等大型企劃需要在廣闊區域內進行持續的挖掘、平整和運輸作業。越南大規模高速公路計劃的訂單推動了混凝土道路建設的發展,滑模攤舖機的日產量可達500公尺。隨著工業園區租戶進口生產線機械和預製模組,物料輸送量也不斷成長。

受鎳礦開採持續投資的推動,礦業配套產業持續保持高於區域平均的成長。同時,為響應城市改造的需要,拆除和回收活動也不斷擴大。公共產業工程,特別是涉及光纖幹線和電網升級的工程,正採用具備先進感測功能的緊湊型設備,以最大限度地減少服務中斷。數位雙胞胎技術的應用,尤其是在智慧城市和鐵路路線規劃領域,正在縮短返工週期,並推動對精密導向機械的需求。承包商報告稱,由於使用了遠端資訊處理數據,停機時間減少了10-15%,這進一步凸顯了先進技術方案的優勢。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 透過印尼資本遷移計劃(IKN)促進基礎設施超級週期

- 鎳礦開採熱潮推動了對超大型挖土機的需求

- 泰越高速鐵路走廊帶動跨境設備需求

- 強勁的外國直接投資流入東協工業園區和經濟特區

- 受「一帶一路」計劃相關建築企業在地化要求的影響,中國OEM製造商的銷售額有所成長。

- 透過現場數位化(BIM + 5G 車聯網)加速車輛更新

- 市場限制

- 高額的初始資本投入和企劃案融資利率收緊

- 由於合格操作員短缺,營運成本 (OPEX) 增加。

- 充電基礎設施和氫氣加註網路的缺乏減緩了綠色設備的普及。

- 中美貿易摩擦導致引擎和零件供應中斷

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按機器類型

- 挖土機

- 裝載機

- 起重機

- 後鏟式裝載機

- 平土機機

- 攤舖機和壓路機

- 其他(加長型堆高機堆高機、自動卸貨卡車等)

- 透過使用

- 土木工程施工機械

- 混凝土和道路施工

- 物料輸送與物流

- 採礦支持

- 拆卸和回收

- 公用設施安裝

- 其他

- 按最終用途行業分類

- 住宅

- 商業建築

- 基礎設施/公共工程

- 礦業

- 石油和天然氣

- 工業製造

- 其他

- 透過推廣

- 柴油引擎

- 混合

- 電池式電動車

- 氫燃料電池

- 其他

- 按國家/地區

- 印尼

- 泰國

- 越南

- 菲律賓

- 馬來西亞

- 新加坡

- 其他東南亞國協(緬甸、寮國、柬埔寨、汶萊)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery Co.

- XCMG Group

- Sany Heavy Industry

- Liebherr Group

- JCB

- CNH Industrial(CASE and New Holland)

- Volvo Construction Equipment

- Zoomlion Heavy Industry

- Doosan Infracore

- Hyundai Construction Equipment

- Kobelco Construction Machinery

- Yanmar Co., Ltd.

- Wirtgen Group

- Kubota Corporation

- Sandvik Mining and Rock Tech.

- Terex Corporation

- Sumitomo Construction Machinery

- Manitou Group

第7章 市場機會與未來展望

The ASEAN construction machinery market is expected to grow from USD 8.12 billion in 2025 to USD 8.51 billion in 2026 and is forecast to reach USD 10.77 billion by 2031 at 4.82% CAGR over 2026-2031.

The market's momentum reflects an infrastructure super-cycle stretching from Indonesia's new capital city in East Kalimantan to a Thailand-Vietnam high-speed rail corridor. Sustained foreign direct investment into industrial parks, a resurgence in nickel-mining capital expenditure, and accelerating job-site digitalization continue to refresh fleets across every major equipment category. At the same time, Chinese original-equipment manufacturers (OEMs) are expanding rapidly under contractor-localization mandates, reshaping competitive dynamics and price points. Equipment electrification and emerging hydrogen prototypes signal another layer of opportunity as governments tighten emissions regulations and construction firms pursue sustainability credentials. Supply-chain shocks tied to U.S.-China trade frictions and persistent operator shortages remain the principal brakes on growth, but proactive skills-training programs and diversified sourcing strategies are gradually offsetting these risks

ASEAN Construction Machinery Market Trends and Insights

Infrastructure Super-Cycle Driven by Indonesia's IKN Capital-City Build

Groundwork at the Nusantara project is proceeding in phased packages that extend procurement cycles into the mid-2040s. Five private investors have already committed more than Rp 2.4 trillion for 2025 milestones covering lifestyle centers, mixed-use precincts, and essential utilities. Public-sector allocations have surpassed Rp 100 trillion and include road sections designed within a digital-twin framework. Such project breadth sustains order pipelines for excavators, loaders, concrete pumps, and specialist lifting gear while encouraging OEMs to localize component supply. Nonetheless, delayed cement shipments and episodic budget revisions illustrate execution risks that could temper near-term equipment call-offs. Planned public-private-partnership structures are expected to relieve funding pressure by broadening the lender base over the next decade.

Nickel-Mine Boom Fuelling Demand for Ultra-Large Excavators

Indonesia's ascent as the world's leading nickel producer underpins a wave of ultra-large equipment orders. Mass production of 120-ton class EX1200 hydraulic excavators began in November 2024 and is now geared toward both green-field and brown-field mine expansions. The mining equipment fleet is positioned to climb significantly by 2029 as battery-materials demand widens. OEMs are showcasing 100-ton and 150-ton prototypes tailored for laterite ore conditions, while local contractors target double-digit market share gains. With nickel prices rebounding, mines are front-loading capital outlays although tighter environmental audits could require additional technology investments.

High Upfront Capex and Tightening Project-Finance Rates

Interest costs have climbed alongside global rate cycles, lifting hurdle rates for new equipment purchases. Government budget adjustments, most visible in Indonesia where the 2025 infrastructure allocation has narrowed, restrict public-sector tender releases. Highly leveraged state-owned contractors continue to refinance short-dated debt, but profit erosion limits their ability to self-fund machinery. A regional effort to standardize loan documentation seeks to mobilize insurance and pension capital into long-dated infrastructure vehicles, thereby easing financing constraints over the medium term. Banks with large construction portfolios are introducing sustainability-linked loan tranches that reward the uptake of low-emission machinery.

Other drivers and restraints analyzed in the detailed report include:

- Thailand-Vietnam High-Speed Rail Corridor Boosting Cross-Border Equipment Demand

- Strong FDI Inflows into ASEAN Industrial Parks and Sezs

- Shortage of Certified Operators Inflating OPEX

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The ASEAN construction equipment market size for excavators amounted to 35.10% of total value in 2025, solidifying the category's lead. High-tonnage models now dominate Indonesian mine specifications, while medium-class units remain omnipresent on road and railway projects. Backhoe loaders, which deliver combined digging and loading capability in congested urban environments, post the fastest 9.86% CAGR as municipalities upgrade drainage and telecom lines. Crawler excavators in the 20-30 tonne band captured more than three-quarters of Indonesian orders, underscoring their versatility within mixed-terrain sites. Loader demand stays resilient on account of port expansions, whereas motor graders and pavers benefit from motorway duplication programs. Telehandlers and dump trucks, although smaller in volume, enjoy niche resilience for industrial-park warehousing and mineral-haul circuits.

Adoption patterns reveal a steady pivot toward integrated control systems, a trend that moves secondary-market valuations in favor of more recent models. Rental companies increasingly bundle telematics subscriptions with monthly rates, incentivizing contractors to opt for connected equipment and thereby enlarging the addressable service revenue pool. Local assemblers, leveraging tariff preferences, extend credit lines that lower acquisition barriers for small contractors and sustain the replacement cycle for primary earth-moving machines.

Earth-moving held 53.72% of ASEAN construction equipment market share and remains the fastest-expanding application at a 4.83% CAGR. Mega-projects such as the Nusantara city build and the cross-border rail corridor require continuous excavation, grading, and hauling across vast footprints. Concrete-road construction benefits from large expressway packages in Vietnam where slip-form pavers reach productivity outputs of 500 meters per day. Material-handling volumes climb as industrial-park tenants import line machinery and prefabricated modules.

Mining support continues to outpace regional averages thanks to sustained investment in nickel extraction, while demolition and recycling activities scale up alongside inner-city redevelopment. Utility-installation works, especially fiber-optic backbones and grid upgrades, leverage compact equipment fitted with advanced detection to minimize service interruptions. Integration of digital twins, especially on smart-city and rail alignments, compresses rework cycles and elevates demand for precision-guided machines. Contractors report 10% to 15% reductions in idle time by exploiting telematics data, reinforcing the case for premium technology packages.

The ASEAN Construction Machinery Market Report is Segmented by Machinery Type (Excavators, Loaders, and More), Application (Earth-Moving, Concrete and Road Construction, and More), End-Use Industry (Residential Construction, Commercial Construction, and More), Propulsion (Diesel, Hybrid, and More), and Country (Indonesia, Thailand, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery Co.

- XCMG Group

- Sany Heavy Industry

- Liebherr Group

- JCB

- CNH Industrial (CASE and New Holland)

- Volvo Construction Equipment

- Zoomlion Heavy Industry

- Doosan Infracore

- Hyundai Construction Equipment

- Kobelco Construction Machinery

- Yanmar Co., Ltd.

- Wirtgen Group

- Kubota Corporation

- Sandvik Mining and Rock Tech.

- Terex Corporation

- Sumitomo Construction Machinery

- Manitou Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure Super-Cycle Driven by Indonesia's IKN Capital-City Build

- 4.2.2 Nickel-Mine Boom Fuelling Demand for Ultra-Large Excavators

- 4.2.3 Thailand-Vietnam High-Speed Rail Corridor Boosting Cross-Border Equipment Demand

- 4.2.4 Strong FDI Inflows into ASEAN Industrial Parks and Sezs

- 4.2.5 Belt and Road Contractor-Localization Mandates Increasing Chinese OEM Sales

- 4.2.6 Job-Site Digitalization (BIM + 5G Telematics) Accelerating Fleet Renewal

- 4.3 Market Restraints

- 4.3.1 High Upfront Capex and Tightening Project-Finance Rates

- 4.3.2 Shortage of Certified Operators Inflating OPEX

- 4.3.3 Sparse Charging / Hydrogen Refuelling Network Slowing Green-Equipment Uptake

- 4.3.4 China-US Trade Volatility Causing Engine and Parts Supply Shocks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Machinery Type

- 5.1.1 Excavators

- 5.1.2 Loaders

- 5.1.3 Cranes

- 5.1.4 Backhoe Loaders

- 5.1.5 Motor Graders

- 5.1.6 Pavers and Compactors

- 5.1.7 Others (Telehandlers, Dump Trucks, etc.)

- 5.2 By Application

- 5.2.1 Earth-Moving

- 5.2.2 Concrete and Road Construction

- 5.2.3 Material Handling and Logistics

- 5.2.4 Mining Support

- 5.2.5 Demolition and Recycling

- 5.2.6 Utilities Installation

- 5.2.7 Others

- 5.3 By End-Use Industry

- 5.3.1 Residential Construction

- 5.3.2 Commercial Construction

- 5.3.3 Infrastructure / Public Works

- 5.3.4 Mining

- 5.3.5 Oil and Gas

- 5.3.6 Industrial Manufacturing

- 5.3.7 Others

- 5.4 By Propulsion

- 5.4.1 Diesel

- 5.4.2 Hybrid

- 5.4.3 Battery-Electric

- 5.4.4 Hydrogen Fuel-Cell

- 5.4.5 Others

- 5.5 By Country

- 5.5.1 Indonesia

- 5.5.2 Thailand

- 5.5.3 Vietnam

- 5.5.4 Philippines

- 5.5.5 Malaysia

- 5.5.6 Singapore

- 5.5.7 Rest of ASEAN (Myanmar, Laos, Cambodia, Brunei)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 Komatsu Ltd.

- 6.4.3 Hitachi Construction Machinery Co.

- 6.4.4 XCMG Group

- 6.4.5 Sany Heavy Industry

- 6.4.6 Liebherr Group

- 6.4.7 JCB

- 6.4.8 CNH Industrial (CASE and New Holland)

- 6.4.9 Volvo Construction Equipment

- 6.4.10 Zoomlion Heavy Industry

- 6.4.11 Doosan Infracore

- 6.4.12 Hyundai Construction Equipment

- 6.4.13 Kobelco Construction Machinery

- 6.4.14 Yanmar Co., Ltd.

- 6.4.15 Wirtgen Group

- 6.4.16 Kubota Corporation

- 6.4.17 Sandvik Mining and Rock Tech.

- 6.4.18 Terex Corporation

- 6.4.19 Sumitomo Construction Machinery

- 6.4.20 Manitou Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

施工機械市場:2026-2032年全球市場預測(依產品類型、功率輸出、燃料類型、設計類型、運作小時數、銷售管道和最終用戶分類)橡膠壓機市場:依橡膠類型、壓機類型、操作模式、產能、應用及通路分類-全球預測,2026-2032年電動施工機械市場:依設備類型、推進系統和應用分類-全球預測,2026-2032年自動液壓機市場:按壓機類型、控制類型、操作模式和終端用戶產業分類,全球預測,2026-2032年

施工機械市場:2026-2032年全球市場預測(依產品類型、功率輸出、燃料類型、設計類型、運作小時數、銷售管道和最終用戶分類)橡膠壓機市場:依橡膠類型、壓機類型、操作模式、產能、應用及通路分類-全球預測,2026-2032年電動施工機械市場:依設備類型、推進系統和應用分類-全球預測,2026-2032年自動液壓機市場:按壓機類型、控制類型、操作模式和終端用戶產業分類,全球預測,2026-2032年 2026 年至 2035 年施工機械輪胎市場的商業機會、成長要素、產業趨勢分析與預測。

2026 年至 2035 年施工機械輪胎市場的商業機會、成長要素、產業趨勢分析與預測。 中國施工機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)施工機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國施工機械市場佔有率分析、產業趨勢及統計、成長預測(2026-2031)

中國施工機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)施工機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國施工機械市場佔有率分析、產業趨勢及統計、成長預測(2026-2031) 全球施工機械市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球施工機械市場規模、佔有率、趨勢及成長分析報告(2026-2034) 2026年全球建築及道路施工機械市場報告

2026年全球建築及道路施工機械市場報告