|

市場調查報告書

商品編碼

1934895

泰國施工機械市場佔有率分析、產業趨勢及統計、成長預測(2026-2031)Thailand Construction Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

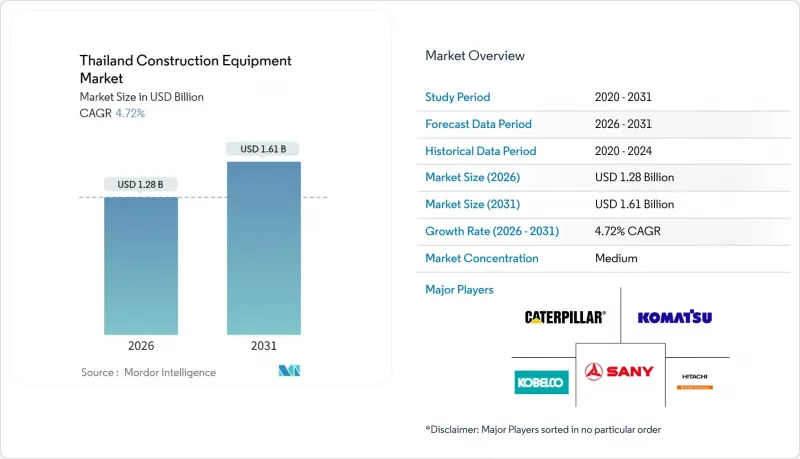

2025年泰國施工機械市場價值12.2億美元,預計到2031年將達到16.1億美元,高於2026年的12.8億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 4.72%。

這一成長軌跡反映了泰國作為東南亞當地基礎設施樞紐的地位、東部經濟走廊(EEC)大型企劃計畫以及政府對多式聯運網路的持續投入。泰國迅速崛起為電動車製造地也促進了需求,維持了工廠建設的勢頭。施工機械供應商正抓住旅遊業主導旅館業復甦、可再生能源設施擴張以及「設備即服務」模式轉變帶來的機遇,該模式旨在解決承包商利潤率低的問題。競爭日趨激烈,全球原始設備製造商(OEM)試圖抵禦來自中國成本優勢製造商的市場佔有率挑戰,而本地租賃業者則在拓展附加價值服務以應對熟練操作人員短缺的問題。

泰國施工機械市場趨勢與洞察

東部經濟走廊(EEC)大型企劃的激增

東歐經濟走廊二期工程包含77個計劃,港口、鐵路和高速公路的同步建設將推動2025年至2027年間對設備的需求。走廊內的資料中心建設需要具備嚴格耐熱和抗震性能的精密基礎設備,而先進製造區對大容量起重機和物料輸送解決方案的訂單也在不斷成長。一體化物流模式正在縮短計劃工期,並將尖峰運轉率推至歷史新高。競標中的環保條款正在加速低排放車型的更新換代,鼓勵承包商用符合Tier-4和Stage V排放標準的新型設備替換老舊的內燃機設備。

可再生能源的擴張將推動對起重機和土木機械的需求。

泰國東北部的大型太陽能發電廠和電池儲能計劃需要低接地壓力推土機、用於追蹤器基礎的打樁機以及用於貨櫃式電池儲能系統模組的重型起重機。與獎勵相關的工期壓縮,導致現有設備壓力增大,並在高峰期推高了每日租金。併網工程也增加了對用於架設高壓線路的專用張緊設備和牽引機的需求。

熟練操作人員短缺導致租賃需求超過購買需求。

影響跨境勞動力的政策變化減少了外國建築工人的數量。這推高了人事費用,也使得尋找經驗豐富的重型設備操作員變得更加困難。租賃公司採取的應對措施包括:將認證操作員與設備捆綁銷售、提供培訓項目,以及引入半自動挖土機以縮短學習曲線。承包商轉向租賃設備,以避免固定的人事費用,並確保操作員能夠根據計劃週期靈活安排。

細分市場分析

預計2025年,挖土機在泰國施工機械市場總銷售量中佔比將達45.12%。其需求涵蓋大型企劃高速公路專案的土方工程、公用設施走廊的溝槽挖掘以及資料中心的基礎開挖等。挖土機適用於各種小規模的土木工程項目,確保了租賃車隊的高運轉率。裝載機和後鏟挖土機的成長速度最快,複合年成長率達5.19%,主要受可再生的推動。起重機的採購量激增,用於風力發電機安裝和高層建築玻璃幕牆工程;伸縮臂叉裝機則滿足了電子商務成長帶來的倉庫建設需求。平地平土機在區域道路建設工程中維持了穩定的需求。專用挖泥船和兩棲挖土機則為港口擴建提供了支持,這表明計劃複雜性正在推動泰國施工機械市場產品組合的多樣化。

多功能性是挖土機優勢的關鍵。諸如破碎錘、螺旋鑽和傾斜鏟斗等附件無需底盤投資底盤即可擴展作業範圍。經銷商提供快速連接器套件和預測性維護套餐,以最大限度地減少停機時間並提升價值。同時,起重機供應商也透過推出專為高起重能力和狹小空間設計的機型來區分產品。因此,各種類型的機器既包括多用途主力機型,也包括高規格的專業產品,隨著基礎設施設計的不斷發展,每種機器都在不斷擴大市場佔有率。

儘管內燃機在2025年仍佔據94.08%的市場佔有率,但預計到2031年,電池電動馬達的市場佔有率將以10.84%的複合年成長率成長,從而擠壓內燃機的市場佔有率。都市區排放法規和工地噪音管制條例正促使建築公司試用電動小型挖土機、裝載機和剪叉式升降機。混合模式將小型引擎與電力驅動系統相結合,透過消除對固定充電樁的依賴並降低油耗,填補了基礎設施的空白。雖然初始成本較高,但整體擁有成本模型在兩班制下可在三年內收回成本,這有助於證明曼谷一家大型建築公司進行車隊試用的合理性。

挑戰依然存在:農村地區電力供應匱乏,電池系統零件供應鏈尚未成熟,進口關稅推高了售價。原始設備製造商(OEM)正透過在當地組裝電池組或將充電設備租賃納入購置合約來應對這些挑戰。隨著東部經濟走廊(EEC)沿線港口和工業園區擴大電網容量,電氣化進程預計將進一步加速,並在未來十年內推動泰國施工機械市場向更清潔的動力系統轉型。

泰國施工機械市場報告按機器類型(例如,起重機、伸縮臂叉裝車)、動力方式(例如,內燃機)、功率輸出(例如,小於100馬力)、最終用戶(例如,基礎設施、住宅和商業建築)、應用領域(例如,土方工程、物料輸送)和地區進行細分。市場預測以價值(美元)和數量(台)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 東部經濟走廊(EEC)大型企劃的激增

- 透過公私合營加速基礎建設

- 旅遊業主導商業和旅館業復甦

- 可再生能源設施(太陽能發電廠、儲能系統)的擴建將提升對起重機和土木機械的需求。

- 待開發區工廠對於實現電動車供應鏈工廠的本地化至關重要。

- 快速採用機器控制和BIM整合設備以降低成本計劃超支

- 市場限制

- 建築材料價格上漲給承包商的資本投資帶來了壓力。

- 熟練操作人員短缺導致租賃需求超過購買需求。

- 高昂的電價和充電基礎設施的缺乏正在減緩電動重型機械的普及。

- 小型企業信貸環境嚴峻,導致車隊更新周期放緩。

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按機器類型

- 起重機

- 伸縮臂堆高機

- 挖土機

- 裝載機和後鏟

- 平土機機

- 其他機器類型

- 透過推進力

- 內燃機

- 電動/混合動力

- 透過輸出

- 不到100馬力

- 101-200馬力

- 超過200馬力

- 最終用戶

- 基礎設施

- 住宅及商業建築

- 採礦和工業

- 農業

- 能源與公共產業

- 透過使用

- 土木工程施工

- 物料輸送

- 道路建設

- 吊起吊裝置

- 按地區

- 曼谷大都會

- 泰國中部

- 泰國北部

- 泰國東北部

- 泰國南部

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery Co. Ltd.

- Kobelco Construction Machinery Co. Ltd.

- SANY Group

- XCMG Group

- Zoomlion Heavy Industry Science & Technology Co. Ltd.

- Hyundai Construction Equipment Co. Ltd.

- Liebherr Group

- CNH Industrial NV

- JC Bamford Excavators Ltd(JCB)

- Volvo Construction Equipment

- Doosan Bobcat

- Wirtgen Group(John Deere)

- Yanmar Holdings Co. Ltd.

- Takeuchi Mfg. Co. Ltd.

- Kubota Corporation

- Sumitomo Construction Machinery Co. Ltd.

- Terex Corporation

- Manitowoc Company Inc.

第7章 市場機會與未來展望

The Thailand construction equipment market was valued at USD 1.22 billion in 2025 and estimated to grow from USD 1.28 billion in 2026 to reach USD 1.61 billion by 2031, at a CAGR of 4.72% during the forecast period (2026-2031).

The growth trajectory reflects the nation's role as an infrastructure hub for mainland Southeast Asia, the megaproject pipeline of the Eastern Economic Corridor (EEC), and continued state commitment to multi-modal transport links. Demand also benefits from Thailand's rapid emergence as an electric-vehicle manufacturing base, which keeps factory construction momentum high. Equipment suppliers are capitalizing on the rebound in tourism-led hospitality developments, the renewable-energy build-out, and the shift toward equipment-as-a-service models that address tight contractor margins. Competitive intensity rises as global OEMs defend share against cost-aggressive Chinese entrants, while local rental operators broaden value-added services to counter skilled-operator shortages.

Thailand Construction Equipment Market Trends and Insights

Surge in Megaprojects Under Eastern Economic Corridor (EEC)

Phase-2 EEC developments span 77 projects and introduce simultaneous port, rail, and highway workstreams concentrating equipment demand over 2025-2027. Data-center builds within the corridor require precision foundation equipment capable of strict thermal and seismic tolerances, while advanced-manufacturing zones drive orders for high-capacity cranes and material-handling solutions. The integrated logistics approach compresses project timelines, lifting utilization peaks above historic norms. Environmental compliance clauses in EEC tenders accelerate fleet renewal toward low-emission models, nudging contractors to replace aging internal-combustion units with newer Tier-4 and Stage V machines.

Renewable-Energy Build-Out Lifting Demand for Cranes and Earth-Moving Gear

Large-scale solar farms and battery-energy-storage projects in Northeastern Thailand need low-ground-pressure dozers, pile drivers for tracker foundations, and heavy-lift cranes for containerized BESS modules. Compressed construction schedules tied to incentive windows strain existing fleets, pushing daily rental rates upward during peak months. Grid-connection works add demand for specialized tensioners and pullers used in high-voltage line stringing.

Skilled-Operator Shortages Pushing Renters Over Buyers

Policy shifts affecting cross-border labor reduced the available foreign construction workforce, raising labor costs and limiting experienced operators for heavy machinery. Rental companies respond by bundling certified operators with equipment, offering training programs, and adopting semi-autonomous excavators that cut the learning curve. Contractors migrate to rental to avoid fixed payroll costs and ensure operator availability aligned with project cycles.

Other drivers and restraints analyzed in the detailed report include:

- Public-Private Partnerships Accelerating Infrastructure Roll-Outs

- Rapid Adoption of Machine-Control and BIM-Integrated Equipment

- Tight Credit Conditions for SMEs Slowing Fleet Renewal Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Thailand construction equipment market size for excavators stood at 45.12% of total revenue in 2025. Demand spans earthworks for megaproject highways, trenching for utility corridors, and foundation digging for data centers. Rental fleets keep high utilization because excavators suit both small and large civil packages. Loaders and backhoe units record the quickest rise at a 5.19% CAGR, favored for renewable-energy site prep and industrial estate grading. Crane purchases surge for wind-turbine erection and high-rise glazing, while telescopic handlers satisfy warehouse builds tied to e-commerce growth. Motor graders remain stable on provincial road programs. Specialist dredgers and amphibious excavators underpin port expansions, illustrating how project complexity diversifies unit mix within the Thailand construction equipment market.

Versatility explains excavators' dominance: attachments such as rock-breakers, augers, and tilt buckets extend task scope without extra chassis investment. Dealers deepen value by offering quick-coupler kits and predictive-maintenance packages that minimize downtime. Conversely, crane suppliers differentiate through high-lift capacity and narrow-footprint models tailored to congested urban sites. The machinery-type landscape therefore reflects both multi-purpose workhorses and high-spec niche products, each carving share as infrastructure designs evolve.

Internal-combustion engines supplied 94.08% of 2025 units, but their share slips as battery-electric machines log an 10.84% CAGR to 2031. Urban emission curbs and site-noise ordinances encourage contractors to trial electric mini-excavators, loaders, and scissors lifts. Hybrid models bridge the infrastructure gap by pairing smaller engines with electrified drive trains, cutting fuel use without reliance on fixed chargers. Despite upfront premiums, total-cost-of-ownership models show breakeven within three years on two-shift operations, helping justify fleet pilots among leading contractors in Bangkok.

Challenges persist: rural sites lack power supply, spare-parts channels for battery systems are nascent, and import duties inflate sticker prices. OEMs respond by localizing battery-pack assembly and bundling charging-equipment leases within purchase deals. As EEC ports and industrial estates expand grid capacity, electric adoption is expected to accelerate further, lifting the Thailand construction equipment market toward cleaner propulsion over the decade.

The Thailand Construction Equipment Report is Segmented by Machinery Type (Cranes, Telescopic Handlers, and More), Propulsion (Internal Combustion Engine and More), Power Output (Below 100 HP and More), End-User (Infrastructure, Residential and Commercial Construction, and More), Application (Earth-Moving, Material Handling, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery Co. Ltd.

- Kobelco Construction Machinery Co. Ltd.

- SANY Group

- XCMG Group

- Zoomlion Heavy Industry Science & Technology Co. Ltd.

- Hyundai Construction Equipment Co. Ltd.

- Liebherr Group

- CNH Industrial N.V.

- JC Bamford Excavators Ltd (JCB)

- Volvo Construction Equipment

- Doosan Bobcat

- Wirtgen Group (John Deere)

- Yanmar Holdings Co. Ltd.

- Takeuchi Mfg. Co. Ltd.

- Kubota Corporation

- Sumitomo Construction Machinery Co. Ltd.

- Terex Corporation

- Manitowoc Company Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge In Megaprojects Under Eastern Economic Corridor (EEC)

- 4.2.2 Public-Private Partnerships Accelerating Infrastructure Roll-Outs

- 4.2.3 Tourism-Led Rebound in Commercial and Hospitality Construction

- 4.2.4 Renewable-Energy Build-Out (Solar Farms, BESS) Lifting Demand for Cranes and Earth-Moving Gear

- 4.2.5 Localization of EV Supply-Chain Plants Requiring Green-Field Factory Construction

- 4.2.6 Rapid Adoption of Machine-Control & BIM-Integrated Equipment to Cut Project Over-Runs

- 4.3 Market Restraints

- 4.3.1 Construction-Input Inflation Squeezing Contractor CAPEX

- 4.3.2 Skilled-Operator Shortages Pushing Renters Over Buyers

- 4.3.3 High Import Duties and Sparse Charging Infra Delaying Electric Heavy Machinery Uptake

- 4.3.4 Tight Credit Conditions for SMEs Slowing Fleet Renewal Cycles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD), Volume (Units))

- 5.1 By Machinery Type

- 5.1.1 Cranes

- 5.1.2 Telescopic Handlers

- 5.1.3 Excavators

- 5.1.4 Loaders & Backhoe

- 5.1.5 Motor Graders

- 5.1.6 Other Machinery Types

- 5.2 By Propulsion

- 5.2.1 Internal Combustion Engine

- 5.2.2 Electric & Hybrid

- 5.3 By Power Output

- 5.3.1 Below 100 HP

- 5.3.2 101 - 200 HP

- 5.3.3 Above 200 HP

- 5.4 By End-user

- 5.4.1 Infrastructure

- 5.4.2 Residential and Commercial Construction

- 5.4.3 Mining and Industrial

- 5.4.4 Agriculture

- 5.4.5 Energy and Utilities

- 5.5 By Application

- 5.5.1 Earth-moving

- 5.5.2 Material Handling

- 5.5.3 Road Construction

- 5.5.4 Lifting & Hoisting

- 5.6 By Region

- 5.6.1 Bangkok Metropolitan Area

- 5.6.2 Central Thailand

- 5.6.3 Northern Thailand

- 5.6.4 Northeastern Thailand

- 5.6.5 Southern Thailand

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 Komatsu Ltd.

- 6.4.3 Hitachi Construction Machinery Co. Ltd.

- 6.4.4 Kobelco Construction Machinery Co. Ltd.

- 6.4.5 SANY Group

- 6.4.6 XCMG Group

- 6.4.7 Zoomlion Heavy Industry Science & Technology Co. Ltd.

- 6.4.8 Hyundai Construction Equipment Co. Ltd.

- 6.4.9 Liebherr Group

- 6.4.10 CNH Industrial N.V.

- 6.4.11 JC Bamford Excavators Ltd (JCB)

- 6.4.12 Volvo Construction Equipment

- 6.4.13 Doosan Bobcat

- 6.4.14 Wirtgen Group (John Deere)

- 6.4.15 Yanmar Holdings Co. Ltd.

- 6.4.16 Takeuchi Mfg. Co. Ltd.

- 6.4.17 Kubota Corporation

- 6.4.18 Sumitomo Construction Machinery Co. Ltd.

- 6.4.19 Terex Corporation

- 6.4.20 Manitowoc Company Inc.

7 Market Opportunities & Future Outlook

施工機械市場:2026-2032年全球市場預測(依產品類型、功率輸出、燃料類型、設計類型、運作小時數、銷售管道和最終用戶分類)橡膠壓機市場:依橡膠類型、壓機類型、操作模式、產能、應用及通路分類-全球預測,2026-2032年電動施工機械市場:依設備類型、推進系統和應用分類-全球預測,2026-2032年自動液壓機市場:按壓機類型、控制類型、操作模式和終端用戶產業分類,全球預測,2026-2032年

施工機械市場:2026-2032年全球市場預測(依產品類型、功率輸出、燃料類型、設計類型、運作小時數、銷售管道和最終用戶分類)橡膠壓機市場:依橡膠類型、壓機類型、操作模式、產能、應用及通路分類-全球預測,2026-2032年電動施工機械市場:依設備類型、推進系統和應用分類-全球預測,2026-2032年自動液壓機市場:按壓機類型、控制類型、操作模式和終端用戶產業分類,全球預測,2026-2032年 2026 年至 2035 年施工機械輪胎市場的商業機會、成長要素、產業趨勢分析與預測。

2026 年至 2035 年施工機械輪胎市場的商業機會、成長要素、產業趨勢分析與預測。 中國施工機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)施工機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)東協施工機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中國施工機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)施工機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)東協施工機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球施工機械市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球施工機械市場規模、佔有率、趨勢及成長分析報告(2026-2034) 2026年全球建築及道路施工機械市場報告

2026年全球建築及道路施工機械市場報告