|

市場調查報告書

商品編碼

1937364

西班牙低溫運輸物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Spain Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

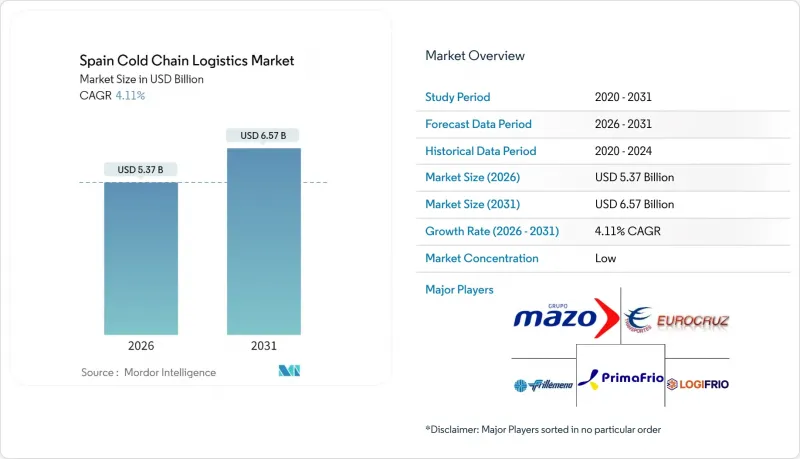

2025年西班牙低溫運輸物流市場價值為51.6億美元,預計到2031年將達到65.7億美元,高於2026年的53.7億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 4.11%。

農產品出口成長、公路和港口基礎設施改善以及電商配送加速向溫控模式轉型,支撐了倉儲、運輸和附加價值服務的穩定需求前景。國際物流集團持續收購區域營運商,以確保戰略定位和多溫區配送能力,而本地企業則投資自動化以控制人事費用和能源成本。政策支持鐵路貨運、清潔冷凍技術以及可再生能源的推廣,正在拓展西班牙低溫運輸物流市場的運輸選擇並減少排放。最具成長潛力的領域包括藥品分銷、人工智慧賦能的都市區微型倉配以及連接西班牙生產區與北歐和北非的多式聯運走廊。

西班牙低溫運輸物流市場趨勢與洞察

生鮮食品配送電子商務快速成長

隨著消費者對冷藏和冷凍產品當日送達的需求不斷成長,線上食品雜貨銷售額持續以兩位數的速度成長,這促使零售商建設微型倉配中心並投資自動化倉庫,以減少廢棄物和人工成本。例如,SimCorp為Mercadona開發的自動化配送系統,能夠實現生鮮食品從採摘到門市的當日送達,這充分展現了現代機器人技術為西班牙低溫運輸物流市場帶來的效率提升。都市區營運商正在利用基於人工智慧的需求預測來最佳化配送路線並降低能耗,從而打造高利潤的加值服務領域。亞馬遜在阿斯圖裡亞斯投資3億歐元(約3.3109億美元)的設施,正是大型零售商如何將機器人技術融入溫控履約以滿足顧客期望的典型案例。這些投資正鼓勵第三方物流供應商在人口中心周邊擴大多溫區轉運站,並在人口密集的都市區地區安裝小包裹大小的冷藏櫃。

藥品和疫苗低溫運輸需求不斷成長

西班牙生物製藥產業正在擴大國內生產和轉口業務,推動了對符合GDP認證標準的倉庫、檢驗的包裝和追蹤技術的需求。 DHL計劃在2030年投資20億歐元(22億美元)用於醫療物流,其中包括其在西班牙的設施。該設施將配備溫度控制區,溫度範圍從-80°C的超低溫到+15°C的室溫控制(CRT),以確保先進療法的安全運輸。從幹線運輸到最後一公里配送,提供即時溫度警報的物聯網感測器已成為標準配置,滿足了衛生當局日益嚴格的審核要求。光是加泰隆尼亞的公共疫苗接種計劃,其疫苗劑量處理量就比20年前增加了21倍,凸顯了該產業的結構性擴張。日益複雜的服務以及不斷加強的監管審查,使得供應商能夠提供價格更高的解決方案,從而促成了西班牙低溫運輸物流市場更強力的長期合約。

冷藏倉庫能源和房地產成本高昂

批發電力價格的波動推高了深冷凍庫和多溫區倉庫的營運成本,迫使營運商對其維修,加裝變速驅動裝置、高效能壓縮機和屋頂太陽能板。新的氟化氣體法規逐步淘汰高全球暖化潛勢(GWP)冷媒,迫使超級市場和第三方物流業者投資自然冷氣系統,增加了初始資本支出。馬德里和巴塞隆納附近優質土地的短缺推高了租金,迫使營運商建造高層、全自動化的設施,以最大限度地提高倉儲容量。西班牙的電網級電池儲能藍圖預計在未來緩解這一問題,但目前能源成本轉嫁的政策仍不明確,限制了其擴張計畫。

細分市場分析

到2025年,冷藏倉庫將佔西班牙低溫運輸物流市場41.35%的佔有率,這主要得益於出口商、食品雜貨商和製藥公司為應對供應鏈中斷而尋求緩衝能力的需求。像Carnicas Chamberí公司位於托萊多的倉庫這樣的自動化高層冷藏倉庫,可以在-18 度C的低溫環境下處理超過1800個托盤,同時降低能耗和人事費用。公共倉庫因其資產共用和靈活的部位安排而日益受到歡迎,而大型加工商則在建造配備整合式產品專用溫區的專用設施。包括重新包裝、貼標、套件組裝和越庫作業在內的附加價值服務正以3.84%的複合年成長率成長,這反映出客戶傾向於將非核心業務外包並縮短交貨時間。由於西班牙15825公里的高速公路網路,運輸服務的需求保持穩定,但利潤壓力正推動企業採用液化天然氣、電力和鐵路兼容的冷藏集裝箱,以達到排放目標。西班牙的低溫運輸物流市場正受益於《ATP條約》的實施,該條約對該國約30萬輛車隊的隔熱材料和製冷設備進行了標準化。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 生鮮食品配送電子商務快速成長

- 藥品和疫苗低溫運輸需求不斷成長

- 出口導向園藝和水產品的發展

- 根據歐盟「Fit-for-55」計劃,向以鐵路為基礎的多式聯運低溫運輸過渡

- 人工智慧驅動的微型倉配減少了最後一公里環節的損耗

- 氣候變遷導致從南向北的逆向物流

- 市場限制

- 冷藏倉庫能源和房地產成本高昂

- 農村地區基礎設施匱乏

- 合格冷凍技術人員短缺

- 氨/二氧化碳工廠水資源管理條例

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 激烈的競爭

- 排放標準對低溫運輸的影響

- 新冠疫情與地緣政治事件的影響

第5章 市場規模與成長預測

- 按服務類型

- 冷藏保管

- 公共倉庫

- 私人倉庫

- 冷藏運輸

- 道路運輸

- 鐵路

- 海

- 航空郵件

- 附加價值服務

- 冷藏保管

- 按溫度類型

- 冷藏(0-5°C)

- 冷凍(-18 至 0°C)

- 環境的

- 超低溫冷凍(低於-20°C)

- 透過使用

- 水果和蔬菜

- 肉類/家禽

- 魚貝類

- 乳製品和冷凍甜點

- 麵包糖果甜點

- 調理食品

- 製藥和生物製藥

- 疫苗和臨床試驗材料

- 化學品/特殊材料

- 其他生鮮產品

- 按地區

- 安達盧西亞

- 加泰隆尼亞

- 瓦倫西亞地區

- 馬德里及西班牙中部

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Grupo Mazo

- Eurocruz

- Primafrio

- Frillemena SA

- Logifrio

- STEF

- Lineage Logistics

- DHL

- Transportes Corredor

- Frimercat

- Ferro-Montajes Albacete SCL de Balazote

- Asgasa Servicios Frigorificos

- ID Logistics

- Frigorifics Gelada SL

- CubeCold

- Frigorificos SOLY

- Frigorificos Sanchidrian

- Antonio Marco

- Vitotrans

- Autransa SL

第7章 市場機會與未來展望

The Spain Cold Chain Logistics Market was valued at USD 5.16 billion in 2025 and estimated to grow from USD 5.37 billion in 2026 to reach USD 6.57 billion by 2031, at a CAGR of 4.11% during the forecast period (2026-2031).

Rising agrifood exports, highway and port upgrades, and the accelerating shift toward temperature-sensitive e-commerce deliveries underpin a stable demand outlook for warehousing, transport, and value-added services. International logistics groups continue acquiring regional operators to secure strategic locations and multi-temperature capacity, while local firms invest in automation to curb labor and energy costs. Policy support for rail freight, clean refrigeration technologies, and renewable energy adoption is widening modal choices and lowering emissions across the Spain cold chain logistics market. Growth opportunities remain strongest in pharmaceutical distribution, AI-enabled urban micro-fulfillment, and intermodal corridors linking Spanish production zones with Northern Europe and North Africa.

Spain Cold Chain Logistics Market Trends and Insights

E-commerce boom in fresh grocery delivery

Online food sales are growing at double-digit rates as consumers demand same-day delivery of chilled and frozen items, compelling retailers to build micro-fulfillment hubs and invest in automated storage that reduces spoilage and labor requirements. Automated distribution systems such as Cimcorp's installation for Mercadona now move fresh produce from field to store within a single day, demonstrating the efficiency gains that modern robotics bring to the Spain cold chain logistics market. Urban operators leverage AI-based demand forecasting to optimize route planning and shrink energy consumption, creating premium service niches that command higher margins. The EUR 300 million (USD 331.09 million) Amazon facility in Asturias exemplifies how large retailers are embedding robotics into temperature-controlled fulfillment to meet customer expectations . These investments stimulate third-party logistics providers to expand multi-temperature cross-docks near population centers and embed parcel-sized cool lockers inside dense city zones.

Rising pharma and vaccine cold-chain needs

Spain's biopharmaceutical sector is scaling both domestic manufacturing and re-export activity, elevating demand for GDP-certified warehousing, validated packaging, and track-and-trace technology. DHL's pledge to inject EUR 2 billion (USD 2.20 billion) into health logistics by 2030 includes Spanish hubs with controlled zones ranging from -80 °C deep-freeze to +15 °C CRT, enabling safe movement of advanced therapies. IoT sensors that deliver real-time temperature alerts are becoming standard across line-haul and last-mile operations, satisfying stricter health authority audits. The public immunization program in Catalonia alone processes vaccine volumes 21 times larger than two decades earlier, underscoring the sector's structural expansion. Higher service complexity and regulatory scrutiny allow providers to price premium solutions and reinforce long-term contracts in the Spain cold chain logistics market.

High energy and real-estate costs for cold storage

Wholesale electricity volatility has elevated operating costs for blast freezers and multi-temperature warehouses, prompting operators to retrofit variable-speed drives, high-efficiency compressors, and rooftop solar arrays. New F-Gas rules that phase down high-GWP refrigerants force supermarkets and 3PLs to invest in natural refrigerant systems, raising upfront capex. Prime land scarcity near Madrid and Barcelona pushes lease prices upward, compelling operators to build taller, fully automated facilities that maximize cubic capacity. Spain's grid-scale battery storage roadmap promises future relief, yet current policy clarity on energy cost pass-through remains limited, constraining expansion plans.

Other drivers and restraints analyzed in the detailed report include:

- Export-oriented horticulture and seafood growth

- EU Fit-for-55 rail intermodal transition

- Rural infrastructure gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerated storage generated 41.35% of the Spain cold chain logistics market size in 2025 as exporters, grocers, and pharmaceutical firms sought buffer capacity against supply chain shocks. Automated high-bay freezers such as the Toledo site of Carnicas Chamberi handle more than 1,800 pallets at -18°C while cutting power use and labor expense. Public warehouses gain appeal by offering pooled assets and flexible slotting, whereas large processors build private facilities that integrate product-specific temperature zones. Value-added services, covering repacking, labeling, kitting, and cross-docking, are growing at a 3.84% CAGR, reflecting customer willingness to outsource non-core tasks and tighten turnaround times. Transportation services retain steady demand thanks to Spain's 15,825 km motorway network, yet margin pressure encourages adoption of LNG, electric, and rail-compatible reefers to align with emission goals. The Spain cold chain logistics market benefits from ATP treaty enforcement, which standardizes vehicle insulation and refrigeration equipment across the roughly 300,000-unit national fleet.

The Spain Cold Chain Logistics Market Report is Segmented by Service Type (Refrigerated Storage, Refrigerated Transportation, Value-Added Services), Temperature Type (Chilled, Frozen, Ambient, Deep-Frozen), Application (Fruits & Vegetables, Meat & Poultry, Fish & Seafood, Dairy, and More), and Geography (Andalusia, Valencia Region, Madrid & Central Spain, Others). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Grupo Mazo

- Eurocruz

- Primafrio

- Frillemena SA

- Logifrio

- STEF

- Lineage Logistics

- DHL

- Transportes Corredor

- Frimercat

- Ferro-Montajes Albacete SCL de Balazote

- Asgasa Servicios Frigorificos

- ID Logistics

- Frigorifics Gelada SL

- CubeCold

- Frigorificos SOLY

- Frigorificos Sanchidrian

- Antonio Marco

- Vitotrans

- Autransa SL

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce boom in fresh grocery delivery

- 4.2.2 Rising pharma and vaccine cold-chain needs

- 4.2.3 Export-oriented horticulture and seafood growth

- 4.2.4 EU "Fit-for-55" shift to rail intermodal cold-chain

- 4.2.5 AI-enabled micro-fulfilment cuts last-mile spoilage

- 4.2.6 Climate-driven south-to-north reverse logistics

- 4.3 Market Restraints

- 4.3.1 High energy and real-estate costs for cold storage

- 4.3.2 Rural infrastructure gaps

- 4.3.3 Shortage of certified refrigeration technicians

- 4.3.4 Water-scarcity rules for ammonia/CO? plants

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Impact of Emission Standards on Cold-Chain

- 4.9 Impact of COVID-19 and Geo-Political Events

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Refrigerated Storage

- 5.1.1.1 Public Warehousing

- 5.1.1.2 Private Warehousing

- 5.1.2 Refrigerated Transportation

- 5.1.2.1 Road

- 5.1.2.2 Rail

- 5.1.2.3 Sea

- 5.1.2.4 Air

- 5.1.3 Value-Added Services

- 5.1.1 Refrigerated Storage

- 5.2 By Temperature Type

- 5.2.1 Chilled (0-5 °C)

- 5.2.2 Frozen (-18-0 °C)

- 5.2.3 Ambient

- 5.2.4 Deep-Frozen / Ultra-Low (less than-20 °C)

- 5.3 By Application

- 5.3.1 Fruits and Vegetables

- 5.3.2 Meat and Poultry

- 5.3.3 Fish and Seafood

- 5.3.4 Dairy and Frozen Desserts

- 5.3.5 Bakery and Confectionery

- 5.3.6 Ready-to-Eat Meals

- 5.3.7 Pharmaceuticals and Biologics

- 5.3.8 Vaccines and Clinical Trial Materials

- 5.3.9 Chemicals and Specialty Materials

- 5.3.10 Other Perishables

- 5.4 By Region

- 5.4.1 Andalusia

- 5.4.2 Catalonia

- 5.4.3 Valencia Region

- 5.4.4 Madrid and Central Spain

- 5.4.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Grupo Mazo

- 6.4.2 Eurocruz

- 6.4.3 Primafrio

- 6.4.4 Frillemena SA

- 6.4.5 Logifrio

- 6.4.6 STEF

- 6.4.7 Lineage Logistics

- 6.4.8 DHL

- 6.4.9 Transportes Corredor

- 6.4.10 Frimercat

- 6.4.11 Ferro-Montajes Albacete SCL de Balazote

- 6.4.12 Asgasa Servicios Frigorificos

- 6.4.13 ID Logistics

- 6.4.14 Frigorifics Gelada SL

- 6.4.15 CubeCold

- 6.4.16 Frigorificos SOLY

- 6.4.17 Frigorificos Sanchidrian

- 6.4.18 Antonio Marco

- 6.4.19 Vitotrans

- 6.4.20 Autransa SL

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

RAP冷藏貨櫃市場:依貨櫃類型、冷卻系統類型、隔熱材料、容量、溫度範圍、應用、最終用戶分類,全球預測,2026-2032年

RAP冷藏貨櫃市場:依貨櫃類型、冷卻系統類型、隔熱材料、容量、溫度範圍、應用、最終用戶分類,全球預測,2026-2032年 2026-2030年全球低溫運輸市場

2026-2030年全球低溫運輸市場 低溫運輸市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、解決方案、最終用戶分類

低溫運輸市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、解決方案、最終用戶分類 亞太地區低溫運輸物流:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

亞太地區低溫運輸物流:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 2026-2034年全球低溫運輸物流市場規模、佔有率、趨勢及成長分析報告

2026-2034年全球低溫運輸物流市場規模、佔有率、趨勢及成長分析報告 日本低溫運輸運輸市場:規模、佔有率、趨勢和預測:按類型、應用、設備和地區分類,2026-2034年

日本低溫運輸運輸市場:規模、佔有率、趨勢和預測:按類型、應用、設備和地區分類,2026-2034年 低溫運輸物流市場-全球產業規模、佔有率、趨勢、機會與預測:按服務類型、應用、溫度類型、技術、地區和競爭格局分類,2021-2031年血漿分餾低溫運輸產品市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年低溫運輸物流車輛市場依運輸方式、溫度範圍、冷凍技術及終端用戶產業分類-2026-2032年全球預測創新醫藥低溫運輸服務市場:按服務類型、運輸方式、溫度範圍、包裝類型和最終用戶分類,全球預測(2026-2032年)

低溫運輸物流市場-全球產業規模、佔有率、趨勢、機會與預測:按服務類型、應用、溫度類型、技術、地區和競爭格局分類,2021-2031年血漿分餾低溫運輸產品市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年低溫運輸物流車輛市場依運輸方式、溫度範圍、冷凍技術及終端用戶產業分類-2026-2032年全球預測創新醫藥低溫運輸服務市場:按服務類型、運輸方式、溫度範圍、包裝類型和最終用戶分類,全球預測(2026-2032年)