|

市場調查報告書

商品編碼

1934699

美國跨境公路貨運:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031 年)United States Cross Border Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

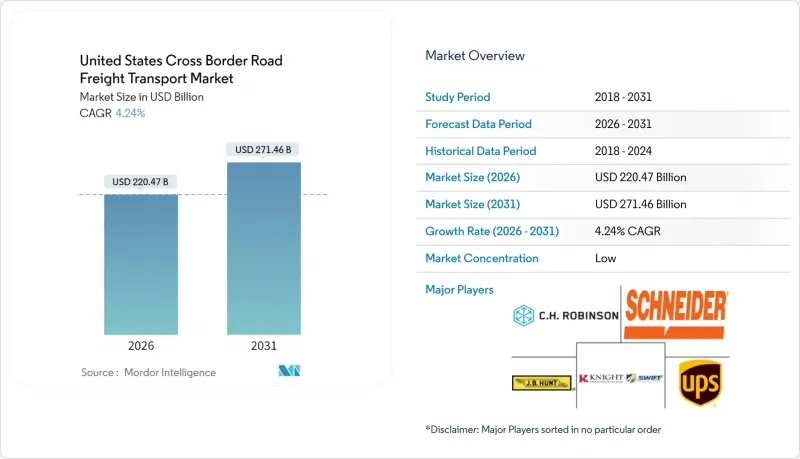

美國跨境公路貨運市場預計將從 2025 年的 2,115.1 億美元成長到 2026 年的 2,204.7 億美元,預計到 2031 年將達到 2,714.6 億美元,2026 年至 2031 年的複合年成長率為 4.24%。

美墨加協定(USMCA)貿易走廊內的近岸外包、電子商務的持續成長以及大規模的基礎設施建設正在推動需求,而更嚴格的安全通訊協定和勞動力短缺則考驗著網路的柔軟性。墨西哥已超越中國成為美國最大的貿易夥伴,擁有密集的南北向卡車運輸路線,每天的貿易額超過30億美元。同時,由於碳定價機制,加拿大繼續扮演著至關重要但成本高昂的角色。預計到2032年,加拿大的司機短缺將達到16萬人,這推高了貨運價格,同時也加速了提高運力運轉率和定價準確性的技術應用。大型卡車運輸公司之間的整合,例如DSV收購DB Schenker以及Ryder的收購攻勢,正在實現跨境專用車隊的規模經濟。與此同時,一些專注於溫控和電商主導的小包裹運輸路線的營運商正在擴大市場佔有率。在 I-45 和 I-35 走廊進行的自動駕駛卡車試驗以及人工智慧驅動的定價引擎正在減少空駛里程,並補充全天候長途運輸能力,使技術成為競爭優勢的核心。

美國跨境公路貨運市場趨勢與洞察

美墨加協定和近岸外包推動美墨貨運量激增

美墨加協定(USMCA)的條款打造了一條價值1.3兆美元的貿易走廊,將促進墨西哥對美國的製造業出口,並已促成到2027年新增460億美元的投資承諾。每月跨境卡車數量平均達到150萬輛,比疫情前增加了166.3%,這給傳統的邊境基礎設施帶來了巨大壓力,並隨著北向工業貨運接近飽和,承運商的定價權也隨之增強。自2019年以來,墨西哥一側的工業用地需求加倍,這印證了製造商優先考慮接近性而非遙遠的亞洲供應鏈。汽車原始設備製造商(OEM)已經證明了乘數效應:在墨西哥組裝廠每投資10億美元,就會產生大規模的向北區域物流需求,從而強化美國跨境公路貨運市場的成長動能。

將墨西哥汽車零件運回國內將活性化向北運輸。

在貿易緊張局勢下,亞洲零件製造商正紛紛在墨西哥位置工廠,以維持進入美國市場的管道,從而重塑汽車供應鏈。上海優尼森計劃在2024年投資4億美元,便是其中的典型例子。這些新進業者打破了航運路線的平衡,北向貨運價格居高不下,而南向貨運價格停滯不前,這使得資產重新配置變得更加複雜,並推高了某些方向的承運商利潤。半導體和電池製造商也面臨類似的趨勢,進一步推高了北向貨運量。即時視覺化平台對於防止貨物被盜、協調運往美國的工廠和碼頭至關重要,有助於維持美國跨境公路貨運市場的效率。

司機短缺推高公路貨運費率

到2032年,勞動力短缺問題可能加倍,職缺將達到16萬個。公路貨運費率將會上漲,而隨著55歲以上人士退出勞動市場的速度快於新入行者,中小運輸公司的抗風險能力將下降。儘管聯邦汽車運輸安全管理局(FMCSA)提供的4,800萬美元津貼擴大了商用駕駛執照(CDL)的培訓途徑,但跨國營運需要額外的安全許可,這限制了候選人的範圍。允許實習駕駛員進行商業運營的例外情況表明,運輸公司迫切需要提高運力,而運力不足仍然是美國跨境公路貨運市場最大的結構性限制。

細分市場分析

至2025年,製造業將占美國跨境公路貨運市場佔有率的32.14%。這主要得益於複雜的汽車和工業供應鏈,這些供應鏈需要專用的整車運輸能力和嚴格的準時交付可靠性。隨著原始設備製造商(OEM)和一級供應商加大近岸外包投資,美國製造業相關路線的跨境公路貨運市場規模預計將穩定成長。然而,由於金屬和塑膠等大宗商品價格波動的影響,預計成長速度將放緩。隨著跨境電子商務滲透率的提高,批發和零售貨運量開始加速成長。隨著面向消費者的企業尋求更頻繁、更小批量的配送,預計該領域在2026年至2031年間的複合年成長率將達到4.92%。

多元化發展,涵蓋電子產品、醫療設備和生鮮產品等,推動了貨運品類的豐富化,需要更廣泛的設備類型,並強化了零擔貨運和溫控貨運細分市場。批發商和零售商正在採用基於區塊鏈的報關方式來加快清關速度,而汽車製造商則在擴展數位雙胞胎建模技術以最佳化車道。這些變化共同鞏固了製造業的基礎性作用,同時也凸顯了零售商在美國跨境公路貨運市場運輸網路設計中日益成長的影響力。

至2025年,非貨櫃貨物將占美國跨境公路貨運市場的85.05%。這主要是由於散裝貨物和大型汽車零件直接依賴卡車運輸。對時效性要求較高的製成品避免了鐵路轉換,這鞏固了卡車運輸的運輸方式優勢,即使鐵路的競爭力日益增強。

預計2026年至2031年間,貨櫃貨運業將以4.82%的複合年成長率成長,這主要得益於多式聯運服務的整合,以及基於區塊鏈的追蹤系統減少了單據錯誤並提高了透明度。使用40英尺貨櫃進口消費品的電商企業正在嘗試沿著跨境。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 人口統計數據

- 按經濟活動分類的GDP分配

- 按經濟活動分類的GDP成長

- 經濟表現及概況

- 電子商務產業的趨勢

- 製造業趨勢

- 運輸和倉儲業的GDP

- 物流績效

- 道路長度

- 出口趨勢

- 進口趨勢

- 燃油價格趨勢

- 卡車運輸營運成本

- 公路貨運量趨勢

- 公路貨運費率趨勢

- 按交通方式分享

- 通貨膨脹

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 美墨加協定和近岸外包推動美墨貨運量激增

- 將生產轉移回墨西哥以增加向北運輸汽車零件

- 電子商務的成長推動了對限時跨境包裹運輸的需求。

- 擴建CTPAT快速通道可減少邊境延誤

- 自動駕駛卡車測試正在I-45和I-35貿易路線上進行

- 人工智慧定價平台正悄悄重塑市場版圖

- 市場限制

- 促進要素短缺推高公路貨運費率

- 加拿大的碳定價體系增加了美國卡車司機的隱性成本。

- 加強邊防安全可能會導致無法預測的等待時間。

- 野火引發的道路封閉導致美國和加拿大的高速公路交通中斷

- 市場創新

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 終端用戶產業

- 農業、漁業、林業

- 建造

- 製造業

- 石油天然氣、採礦和採石

- 批發和零售

- 其他

- 卡車裝載規範

- 整車運輸 (FTL)

- 小批量貨物(零擔)

- 貨櫃運輸

- 貨櫃運輸

- 非貨櫃運輸

- 距離

- 長途

- 短程交通

- 貨物類型

- 液體貨物

- 固體貨物

- 溫度控制

- 非溫控型

- 溫度控制

第6章 競爭情勢

- 市場集中度

- 關鍵策略舉措

- 市佔率分析

- 公司簡介

- ArcBest Corporation

- ATS(Anderson Trucking Service)

- Bay and Bay Transportation

- CH Robinson Worldwide, Inc.

- CR England

- Covenant Logistics Group, Inc.

- CRST The Transportation Solution, Inc.

- DHL Group

- DSV A/S(Including DB Schenker)

- Estes Express Lines

- FedEx

- JB Hunt Transport, Inc.

- Knight-Swift Transportation Holdings, Inc.(Including Swift Transportation Company)

- Landstar System, Inc.

- Old Dominion Freight Line

- Penske Corporation, Inc.

- R+L Carriers

- Ryder System, Inc.

- Schneider National, Inc.

- United Parcel Service of America, Inc.(UPS)

- Werner Enterprises, Inc.

- XPO, Inc.

第7章 市場機會與未來展望

The United States cross border road freight transport market is expected to grow from USD 211.51 billion in 2025 to USD 220.47 billion in 2026 and is forecast to reach USD 271.46 billion by 2031 at 4.24% CAGR over 2026-2031.

Nearshoring within the USMCA trade corridor, sustained e-commerce expansion, and large-scale infrastructure upgrades are reinforcing demand even as tighter security protocols and labor shortages test network agility. Mexico has overtaken China as the United States' largest trading partner, creating dense south-north truck lanes that now channel more than USD 3 billion in daily commerce, while Canada retains a vital but costlier role due to carbon-pricing regimes. Persistent driver scarcity, widening to a projected 160,000-person deficit by 2032, is pushing rates higher and accelerating technology adoption that boosts equipment utilization and pricing precision. Consolidation among top carriers, exemplified by DSV's purchase of DB Schenker and Ryder's acquisition push, is enabling scale efficiencies in cross-border dedicated fleets even as niche operators gain share in temperature-controlled and e-commerce-led LTL lanes. Autonomous truck pilots on the Interstate 45 and Interstate 35 corridors and AI-enabled pricing engines are lowering empty miles and rounding out 24/7 long-haul capacity, placing technology at the heart of competitive advantage.

United States Cross Border Road Freight Transport Market Trends and Insights

USMCA and Near-Shoring Fueling a Mexico-U.S. Freight Surge

USMCA provisions have catalyzed a USD 1.3 trillion trade corridor that funnels manufacturing exports from Mexico to the United States and has already drawn USD 46 billion in new investment commitments through 2027. Monthly truck crossings average 1.5 million units, a 166.3% jump versus pre-pandemic flows, overwhelming legacy border infrastructure and lifting carrier pricing power as northbound industrial freight pushes capacity limits. Demand for industrial space along the Mexican side has doubled since 2019, confirming manufacturers' preference for proximity over distant Asian supply chains. Automotive OEMs illustrate the multiplier effect: every USD 1 billion poured into Mexican assembly plants triggers sizable localized logistics demand that migrates north, reinforcing the growth arc of the United States cross border road freight transport market.

Reshoring Sparking Stronger Northbound Auto-Parts Traffic from Mexico

Automotive supply chains continue to retool as Asian component makers site new Mexican factories to preserve U.S. market access amid trade frictions, exemplified by a USD 400 million investment by Shanghai Unison in 2024. These additions skew lane balance, with northbound trailers commanding premium spot rates while southbound rates stagnate, complicating asset repositioning and elevating carrier margins on preferred directions. Semiconductor and battery firms mirror this footprint, further amplifying northbound tonnage. Real-time visibility platforms are now indispensable for cargo-theft mitigation and for orchestrating inbound origin docks with U.S. destination plants, sustaining the efficiency of the United States cross border road freight transport market.

Driver Shortages Driving Up Line-Haul Rates

The labor crunch could double to 160,000 vacant seats by 2032 as the cohort aged over 55 exits in greater numbers than new entrants replace them, pushing line-haul rates higher and eroding small-carrier resilience. FMCSA grants worth USD 48 million are widening CDL training pathways, yet cross-border work demands additional security clearances that limit candidate pools. Exemptions allowing learner-permit holders to operate in revenue service signal how urgently fleets must shore up capacity, and this constraint is the largest structural drag on the United States cross border road freight transport market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Growth Boosting Demand for Time-Definite Cross-Border LTL

- Expanded CTPAT FAST Lanes Reducing Border Delays

- Canadian Carbon Pricing Adding Hidden Costs for U.S. Carriers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing generated 32.14% of the United States cross border road freight transport market share in 2025, anchored by complex automotive and industrial supply chains that require dedicated FTL capacity and stringent just-in-time reliability. The United States cross border road freight transport market size tied to manufacturing lanes is projected to expand steadily as OEMs and tier suppliers deepen near-shoring investments, although incremental gains moderate due to commodity price swings affecting metals and plastics. Wholesale and retail trade volumes have begun to rise faster as cross-border e-commerce penetration propels shipment counts; the segment is forecast to log a 4.92% CAGR (2026-2031) as consumer-facing firms press for more frequent, smaller-lot deliveries.

Diversification across electronics, healthcare equipment, and agricultural perishables enriches the shipment mix, calling for wider equipment varieties and bolstering LTL and temperature-controlled sub-markets. Wholesale and retail trade players embrace blockchain-enabled customs filing to compress clearance windows, while auto makers expand digital twin modeling for lane optimization. Together, these shifts reinforce manufacturing's anchor role yet spotlight retail's growing pull on carrier network design across the United States cross border road freight transport market.

Non-containerized freight held 85.05% of the United States cross border road freight transport market share in 2025, powered by bulk commodities and oversized auto components that depend on direct truck service. Time-sensitive manufacturing cargo sidesteps rail handoffs, cementing trucking's modal advantage despite rising rail competitiveness.

Containerized freight is poised for a 4.82% CAGR (2026-2031) as intermodal services integrate blockchain-supported tracking that slashes document errors and enhances visibility. E-tailers importing fast-moving goods in 40-ft boxes are experimenting with truck-rail transloads along the U.S.-Mexico Gulf corridor, tempering highway lane congestion. Non-containerized dominance will hold through 2030, yet incremental intermodal penetration signals carriers must broaden asset portfolios to capture rising container drayage revenue within the United States cross border road freight transport market.

The United States Cross Border Road Freight Transport Market Report is Segmented by End User Industry (Construction and More), Truckload Specification (Full-Truck-Load (FTL) and More), Containerization (Containerized and More), Distance (Long Haul and Short Haul), Goods Configuration (Fluid Goods and Solid Goods), and Temperature Control (Temperature Controlled and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ArcBest Corporation

- ATS (Anderson Trucking Service)

- Bay and Bay Transportation

- C.H. Robinson Worldwide, Inc.

- C.R. England

- Covenant Logistics Group, Inc.

- CRST The Transportation Solution, Inc.

- DHL Group

- DSV A/S (Including DB Schenker)

- Estes Express Lines

- FedEx

- J.B. Hunt Transport, Inc.

- Knight-Swift Transportation Holdings, Inc. (Including Swift Transportation Company)

- Landstar System, Inc.

- Old Dominion Freight Line

- Penske Corporation, Inc.

- R+L Carriers

- Ryder System, Inc.

- Schneider National, Inc.

- United Parcel Service of America, Inc. (UPS)

- Werner Enterprises, Inc.

- XPO, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Economic Performance and Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport and Storage Sector GDP

- 4.7 Logistics Performance

- 4.8 Length of Roads

- 4.9 Export Trends

- 4.10 Import Trends

- 4.11 Fuel Pricing Trends

- 4.12 Trucking Operational Costs

- 4.13 Road Freight Tonnage Trends

- 4.14 Road Freight Pricing Trends

- 4.15 Modal Share

- 4.16 Inflation

- 4.17 Regulatory Framework

- 4.18 Value Chain and Distribution Channel Analysis

- 4.19 Market Drivers

- 4.19.1 USMCA and Near-Shoring Fueling a Mexico-U.S. Freight Surge

- 4.19.2 Reshoring Sparking Stronger Northbound Auto-Parts Traffic From Mexico

- 4.19.3 E-Commerce Growth Boosting Demand for Time-Definite Cross-Border LTL

- 4.19.4 Expanded CTPAT FAST Lanes Reducing Border Delays

- 4.19.5 Autonomous Truck Trials Gaining Traction on I-45 and I-35 Trade Routes

- 4.19.6 AI-Powered Pricing Platforms Quietly Reshaping the Market

- 4.20 Market Restraints

- 4.20.1 Driver Shortages Driving Up Line-Haul Rates

- 4.20.2 Canadian Carbon Pricing Adding Hidden Costs for U.S. Carriers

- 4.20.3 Heightened Border Security Creating Unpredictable Wait Times

- 4.20.4 Wildfire-Related Closures Disrupting U.S.-Canada Highway Routes

- 4.21 Technology Innovations in the Market

- 4.22 Porter's Five Forces Analysis

- 4.22.1 Threat of New Entrants

- 4.22.2 Bargaining Power of Buyers

- 4.22.3 Bargaining Power of Suppliers

- 4.22.4 Threat of Substitutes

- 4.22.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Truckload Specification

- 5.2.1 Full-Truck-Load (FTL)

- 5.2.2 Less than-Truck-Load (LTL)

- 5.3 Containerization

- 5.3.1 Containerized

- 5.3.2 Non-Containerized

- 5.4 Distance

- 5.4.1 Long Haul

- 5.4.2 Short Haul

- 5.5 Goods Configuration

- 5.5.1 Fluid Goods

- 5.5.2 Solid Goods

- 5.6 Temperature Control

- 5.6.1 Non-Temperature Controlled

- 5.6.2 Temperature Controlled

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 ArcBest Corporation

- 6.4.2 ATS (Anderson Trucking Service)

- 6.4.3 Bay and Bay Transportation

- 6.4.4 C.H. Robinson Worldwide, Inc.

- 6.4.5 C.R. England

- 6.4.6 Covenant Logistics Group, Inc.

- 6.4.7 CRST The Transportation Solution, Inc.

- 6.4.8 DHL Group

- 6.4.9 DSV A/S (Including DB Schenker)

- 6.4.10 Estes Express Lines

- 6.4.11 FedEx

- 6.4.12 J.B. Hunt Transport, Inc.

- 6.4.13 Knight-Swift Transportation Holdings, Inc. (Including Swift Transportation Company)

- 6.4.14 Landstar System, Inc.

- 6.4.15 Old Dominion Freight Line

- 6.4.16 Penske Corporation, Inc.

- 6.4.17 R+L Carriers

- 6.4.18 Ryder System, Inc.

- 6.4.19 Schneider National, Inc.

- 6.4.20 United Parcel Service of America, Inc. (UPS)

- 6.4.21 Werner Enterprises, Inc.

- 6.4.22 XPO, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment