|

市場調查報告書

商品編碼

1693787

新加坡資料中心 -市場佔有率分析、產業趨勢與成長預測(2025-2030 年)Singapore Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

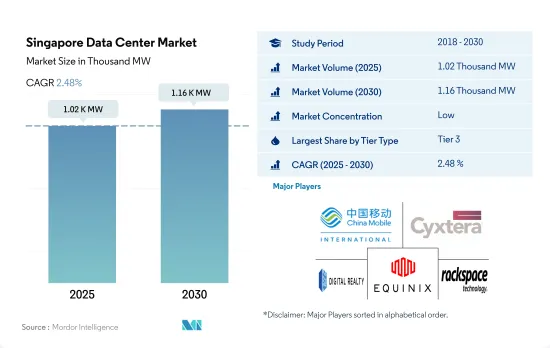

新加坡資料中心市場規模預計在 2025 年達到 1,020MW,預計 2030 年達到 1,160MW,複合年成長率為 2.48%。

預計 2025 年主機託管收益將達到 10.688 億美元,2030 年將達到 15.993 億美元,預測期內(2025-2030 年)的複合年成長率為 8.40%。

2023 年,Tier 3 將佔據市場佔有率的主導地位,而 Tier 4 將成為成長最快的資料中心

- 預計預測期內,三級和四級細分市場將佔據最高的市場佔有率。預計 2023 年 Tier 3 部分將佔據最高的市場佔有率,達到 71.5%。然而,隨著 2029 年 Tier 4 資料中心的出現,該佔有率可能會略微下降至 61.4%。

- 預計 Tier 3 部門在預測期內的複合年成長率為 0.43%,主要原因是吉寶資料中心和 STT GDC 私人有限公司計劃推出三個設施,累計 IT 負載容量為 90 兆瓦。

- 預計一級和二級市場在預測期內的複合年成長率為 1.88%,到 2029 年將佔據 12.1% 的市場佔有率。這一成長趨勢主要歸功於 NTT 有限公司即將建成的資料中心,該公司計劃推出一個 IT 負載容量為 5MW 的設施。

- 預測期內,其複合年成長率將達到 12.69%,IT 負載容量將達到 269.65 MW。

- 在新加坡,資料中心佔總電力消耗量的 7%,到 2030 年這一比例可能會上升到 12% 以上。因此,該國正致力於透過引入最新的基礎設施和冷卻技術來更有效地利用資料中心。營運商正在考慮投資更高效的冷卻解決方案,例如區域冷卻,以及為其資料中心供電的更環保的選擇,例如購電協議(PPA)。 Tier 4 認證設施將幫助營運商達到這些標準,從而有助於推動該領域的成長。

新加坡資料中心市場趨勢

連網型設備和智慧家庭的興起將推動市場需求

- 新加坡的人口相對於其他東南亞國家較少,因此智慧型手機用戶數量相對較低。

- 預計到 2029 年,該國智慧型手機用戶數將從 2022 年的 540 萬增加到 621 萬。

- 根據 Hootsuite 的數據,該國都市化達 100%,行動電話連線數達 870 萬,覆蓋 147% 的人口。數據顯示,每個公民至少擁有一台行動裝置。連網型設備和智慧家庭的普及也推動了對數位數據和網路流量的需求的成長。由於這些因素,該國的智慧型手機用戶數量預計會增加。

新加坡電信和愛立信的 5G 網路擴展將推動資料中心需求

- 新加坡是 2020 年最早採用 5G 網路的國家之一,而其 2G 網路早在 2016 年就已逐步淘汰。截至 2022 年,4G 以 49.7Mbps 的速度佔據市場主導地位,預計到 2029 年速度將達到 54.75Mbps。

- 該國的 5G 網路正在蓬勃發展,預計到 2029 年將達到 946.04 Mbps。隨著服務供應商尋找新的方式來在已經飽和的市場中吸引客戶,5G 網路和服務預計將成為未來幾年通訊產業成長的支柱。

- 新加坡電信與愛立信合作,透過擴展其網路和開發新的 5G 用例,加強其在新加坡的 5G 獨立 (SA) 部署。這家瑞典供應商在新聞稿中表示,計劃利用其 5G 無線接入產品和雲端原生雙模 5G 核心網路解決方案為新加坡電信的 5G SA 網路提供支援。 2021年9月,新加坡電信確認其5G網路覆蓋新加坡三分之二以上的地區。在蔡厝港、榜鵝、三巴旺和淡濱尼等人口密集的地區增加了新的5G站點。

新加坡資料中心產業概況

新加坡資料中心市場較為分散,前五大廠商的市佔率為28.33%。該市場的主要企業包括中國移動國際有限公司、Cyxtera Technologies、Digital Realty Trust Inc.、Equinix Inc. 和 Rackspace Technology Inc.。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 市場展望

- 負載能力

- 占地面積

- 主機代管收入

- 安裝機架數量

- 機架空間利用率

- 海底電纜

第5章 產業主要趨勢

- 智慧型手機用戶數量

- 每部智慧型手機的數據流量

- 行動數據速度

- 寬頻數據速度

- 光纖連接網路

- 法律規範

- 新加坡

- 價值鍊和通路分析

第6章市場區隔

- 熱點

- 新加坡東部

- 新加坡西部

- 其他中東和非洲地區

- 資料中心規模

- 大規模

- 超大規模

- 中等規模

- 超大規模

- 小規模

- 等級類型

- 1級和2級

- 第 3 層

- 第 4 層

- 吸收量

- 未使用

- 使用

- 按主機託管類型

- 超大規模

- 零售

- 批發的

- 按最終用戶

- BFSI

- 雲

- 電子商務

- 政府

- 製造業

- 媒體與娛樂

- 電信

- 其他

第7章競爭格局

- 市場佔有率分析

- 商業狀況

- 公司簡介

- 1-Net Singapore Pte Ltd(Mediacorp)

- Air Trunk Operating Pty Ltd

- China Mobile International Ltd

- Cyxtera Technologies

- Digital Realty Trust Inc.

- Empyrion DC

- Equinix Inc.

- Global Switch Holdings Limited

- PhoenixNAP

- Princeton Digital Group

- Rackspace Technology Inc.

- STT GDC Pte Ltd

第8章:CEO面臨的關鍵策略問題

第9章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 全球市場規模和DRO

- 資訊來源及延伸閱讀

- 圖表清單

- 關鍵見解

- 數據包

- 詞彙表

The Singapore Data Center Market size is estimated at 1.02 thousand MW in 2025, and is expected to reach 1.16 thousand MW by 2030, growing at a CAGR of 2.48%. Further, the market is expected to generate colocation revenue of USD 1,068.8 Million in 2025 and is projected to reach USD 1,599.3 Million by 2030, growing at a CAGR of 8.40% during the forecast period (2025-2030).

Tier 3 holds the majority market share in 2023, Tier 4 is the fastest growing data center

- The tier 3 and 4 segments are expected to hold the highest market share during the forecast period. The tier 3 segment is expected to hold the highest market share of 71.5% in 2023. However, its share may decrease marginally to 61.4% in 2029 due to the upcoming tier 4 data centers.

- The tier 3 segment is expected to record a CAGR of 0.43% during the forecast period, majorly due to the upcoming data centers from Keppel Data Center and STT GDC Pte Ltd, which plan to launch three facilities with a cumulative IT load capacity of 90 MW.

- The tier 1 & 2 segment is expected to record a CAGR of 1.88% during the forecast period, with a market share of 12.1% by 2029. The growth trend is majorly due to the upcoming data centers from NTT Ltd, which plans to launch one facility with an IT load capacity of 5 MW.

- Both the tier 1 & 2 and tier 3 segments may witness a dip in their market share due to the growth of the tier 4 segment, with a CAGR of 12.69% and an IT load capacity of 269.65 MW during the forecast period.

- In Singapore, 7% of total electricity consumption goes to data centers, which may grow to more than 12% by 2030. As a result, the country aims to efficiently use data centers by equipping them with modern infrastructure and cooling techniques. Operators are considering investing in more efficient cooling solutions, such as district cooling, and greener options for powering data centers, such as engaging in Power Purchase Agreements (PPAs). Tier 4-certified facilities may help operators achieve these standards, thus boosting the segment's growth.

Singapore Data Center Market Trends

Growing application of connected devices and smart homes to boost the market demand

- The country has a smaller population compared to other Southeast Asian countries, owing to which the number of smartphone users is comparatively lesser than the rest.

- The country is expected to grow significantly and reach 6.21 million users by 2029, from 5.4 million users in 2022.

- According to Hootsuite, the country has a 100% urbanized population with 8.7 million cellular mobile connections, accounting for 147% of the population. This data suggests that each citizen in the country owns more than one cellular device. The growing application of connected devices and smart homes also boosted the demand for digital data and increased network traffic. Such factors are anticipated to increase the number of smartphone users in the country.

Singtel's expanding 5G network in partnership with Ericsson boost the data center demand

- Singapore was one of the early adopters of the 5G network in 2020, while the presence of 2G was decommissioned as early as 2016. As of 2022, 4G dominated the market with 49.7 Mbps, while its speed is expected to reach 54.75 Mbps by 2029.

- The country's 5G network is booming and is expected to reach 946.04 Mbps by 2029. 5G networks and services are expected to form the backbone of growth in the telecom sector over the coming years as service providers seek new ways to engage customers in a market that is otherwise already saturated.

- Singtel is ramping up its 5G standalone (SA) deployment in Singapore by expanding the network and developing new 5G use cases in partnership with Ericsson. In a press release, the Swedish vendor stated its plans to power Singtel's 5G SA network with 5G radio access products and cloud-native dual-mode 5G Core network solutions. In September 2021, Singtel confirmed that its 5G network covers over two-thirds of Singapore. New 5G sites were added in densely populated areas like Choa Chu Kang, Punggol, Sembawang, and Tampines.

Singapore Data Center Industry Overview

The Singapore Data Center Market is fragmented, with the top five companies occupying 28.33%. The major players in this market are China Mobile International Ltd, Cyxtera Technologies, Digital Realty Trust Inc., Equinix Inc. and Rackspace Technology Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 MARKET OUTLOOK

- 4.1 It Load Capacity

- 4.2 Raised Floor Space

- 4.3 Colocation Revenue

- 4.4 Installed Racks

- 4.5 Rack Space Utilization

- 4.6 Submarine Cable

5 Key Industry Trends

- 5.1 Smartphone Users

- 5.2 Data Traffic Per Smartphone

- 5.3 Mobile Data Speed

- 5.4 Broadband Data Speed

- 5.5 Fiber Connectivity Network

- 5.6 Regulatory Framework

- 5.6.1 Singapore

- 5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

- 6.1 Hotspot

- 6.1.1 East Singapore

- 6.1.2 West Singapore

- 6.1.3 Rest of Singapore

- 6.2 Data Center Size

- 6.2.1 Large

- 6.2.2 Massive

- 6.2.3 Medium

- 6.2.4 Mega

- 6.2.5 Small

- 6.3 Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 Absorption

- 6.4.1 Non-Utilized

- 6.4.2 Utilized

- 6.4.2.1 By Colocation Type

- 6.4.2.1.1 Hyperscale

- 6.4.2.1.2 Retail

- 6.4.2.1.3 Wholesale

- 6.4.2.2 By End User

- 6.4.2.2.1 BFSI

- 6.4.2.2.2 Cloud

- 6.4.2.2.3 E-Commerce

- 6.4.2.2.4 Government

- 6.4.2.2.5 Manufacturing

- 6.4.2.2.6 Media & Entertainment

- 6.4.2.2.7 Telecom

- 6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Landscape

- 7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 7.3.1 1-Net Singapore Pte Ltd (Mediacorp)

- 7.3.2 Air Trunk Operating Pty Ltd

- 7.3.3 China Mobile International Ltd

- 7.3.4 Cyxtera Technologies

- 7.3.5 Digital Realty Trust Inc.

- 7.3.6 Empyrion DC

- 7.3.7 Equinix Inc.

- 7.3.8 Global Switch Holdings Limited

- 7.3.9 PhoenixNAP

- 7.3.10 Princeton Digital Group

- 7.3.11 Rackspace Technology Inc.

- 7.3.12 STT GDC Pte Ltd

- 7.4 LIST OF COMPANIES STUDIED

8 KEY STRATEGIC QUESTIONS FOR DATA CENTER CEOS

9 APPENDIX

- 9.1 Global Overview

- 9.1.1 Overview

- 9.1.2 Porter's Five Forces Framework

- 9.1.3 Global Value Chain Analysis

- 9.1.4 Global Market Size and DROs

- 9.2 Sources & References

- 9.3 List of Tables & Figures

- 9.4 Primary Insights

- 9.5 Data Pack

- 9.6 Glossary of Terms

2025年全球資料中心資訊技術(IT)設備市場報告2025年全球資料中心遷移市場報告2025年全球配置自動化市場報告

2025年全球資料中心資訊技術(IT)設備市場報告2025年全球資料中心遷移市場報告2025年全球配置自動化市場報告 全球配電中心市場:依類型、應用和地區劃分 - 市場規模、行業趨勢、機會分析和預測(2025-2033 年)

全球配電中心市場:依類型、應用和地區劃分 - 市場規模、行業趨勢、機會分析和預測(2025-2033 年) 資料中心設備及基礎設施市場:2025-2030

資料中心設備及基礎設施市場:2025-2030 高階主管簡報:2025 年第四季

高階主管簡報:2025 年第四季 資料中心遷移市場-2025-2030 年預測

資料中心遷移市場-2025-2030 年預測 AI資料中心的設備投資的明細和未來預測

AI資料中心的設備投資的明細和未來預測 全球資料中心服務市場按服務類型、設施服務、IT 服務、專業諮詢與認證、層級類型、資料中心規模與容量、資料中心類型、企業資料中心和地區分類 - 預測至 2030 年

全球資料中心服務市場按服務類型、設施服務、IT 服務、專業諮詢與認證、層級類型、資料中心規模與容量、資料中心類型、企業資料中心和地區分類 - 預測至 2030 年 全球企業 IT 資產處置市場規模、佔有率和行業分析報告:2025 年至 2032 年按資產類型、服務、行業和地區分類的展望和預測

全球企業 IT 資產處置市場規模、佔有率和行業分析報告:2025 年至 2032 年按資產類型、服務、行業和地區分類的展望和預測