|

市場調查報告書

商品編碼

1690097

印度資料中心 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)India Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

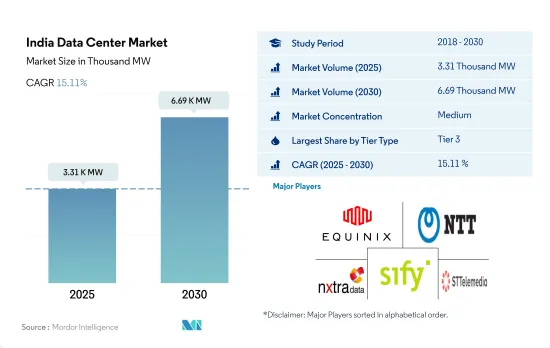

印度資料中心市場規模預計在 2025 年達到 3,310 千瓦,預計到 2030 年將達到 6,690 千瓦,複合年成長率為 15.11%。

預計 2025 年主機託管收益將達到 23.379 億美元,到 2030 年將達到 49.318 億美元,預測期內(2025-2030 年)的複合年成長率為 16.10%。

到 2023 年, 層級 3資料中心將佔據容量的大部分佔有率,並且預計在整個預測期內仍將佔據主導地位。

- 隨著城市人口不斷成長,越來越人開始採用智慧技術,加上各州政府提供誘人的獎勵,資料中心營運商正在全國各地建立大型資料處理設施。

- 隨著印度業務的發展,大型企業正在轉向層級 3 和層級 4資料中心,因為它們具有停機時間短、災難復原和現場援助能力強等特點。這導致該地區層級和層級資料中心的興起。

- 預計層級 3資料中心將從 2022 年的 888.5MW 成長到 2029 年的 3,365.0MW,複合年成長率為 16.20%。同樣,4層級資料中心於 2021 年運作使用,容量為 211.9MW。預計該容量將從 2022 年的 211.9MW 成長到 2029 年的 1,380.2MW,複合年成長率為 29.54%。

- 由於需求低迷,預計層級和二級資料中心在預測期內將停滯不前。

印度資料中心市場趨勢

Jio 等通訊業者已開始提供廉價的智慧型手機和網路服務,從而推動了資料中心市場的發展。

- 預計印度智慧型手機用戶將從 2022 年的 7.944 億成長到 2029 年的 12 億,複合年成長率為 5.52%。 「印度製造」運動等政府舉措為智慧型手機產業提供了獎勵,使得印度能夠生產價格合理、規格齊全且能夠無縫運行應用程式的智慧型手機。

- Jio 等通訊業者的成長以其實惠的套餐徹底改變了網路產業。此外,隨著政府鼓勵線上數位付款和服務,資料需求持續增加。

- 隨著印度 5G 網路的推出,資料消費量預計將快速成長,因為印度用戶傾向於線上 OTT 內容、遊戲、購物、智慧家庭自動化應用、線上保全攝影機等,預計將進一步推動對資料中心的需求。

家庭寬頻存取的增加和網際網路互動的擴大正在推動市場成長。

- 銅線網路連線提供的速度高達 300Mbps,而光纖網路速度則高達 10Gbps。此前,印度的寬頻網路嚴重依賴銅纜連接。雲端技術等新創新推動了光纖電纜的採用,光纖電纜可以以更快的速度移動儲存在雲端中的資料。用戶正在轉向使用光纖電纜連接雲端伺服器和資料中心。因此,就連接性而言,對銅纜的需求正在下降。

- 寬頻連線預計將從 2014 年 3 月的 6.1 兆增加 1,238% 至 2022 年 9 月的 816.2 兆。旗艦計劃BharatNet 正在分階段實施,旨在為該國所有 26,000 個 Gramme Panchayats(GP)提供寬頻存取。第一階段於 2017 年 12 月完成,涵蓋超過 1,000 位全科醫生。截至 2022 年 10 月,該計劃已鋪設 6,00,898 公里光纖電纜,1,90,364 個 GP 已與光纖電纜 (OFC) 連接,1,77,665 個 GP 已透過 OFC 投入服務。此外,還有 4,466 名全科醫生透過衛星媒體進行了連接。 1,82,131 名全科醫生已準備好提供服務。此統計數據顯示寬頻資料使用量增加。

- 隨著城市人口的成長,智慧電視、智慧型手機和智慧照明系統等設備的使用也隨之增加,產生了對只有光纖電纜才能提供的更快頻寬的需求。

印度資料中心產業概況

印度資料中心市場正在緩慢整合,前五大參與者佔55.86%的市場。該市場的主要企業有:Equinix Inc.、NTT Ltd、Nxtra Data Ltd、Sify Technologies Ltd 和 STT GDC Pte Ltd(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 市場展望

- 負載能力

- 占地面積

- 主機代管收入

- 安裝機架數量

- 機架空間利用率

- 海底電纜

第5章 產業主要趨勢

- 智慧型手機用戶數量

- 每部智慧型手機的資料流量

- 行動資料速度

- 寬頻資料速度

- 光纖連接網路

- 法律規範

- 印度

- 價值鍊和通路分析

第6章市場區隔

- 熱點

- 班加羅爾

- 清奈

- 海得拉巴

- 孟買

- NCR

- 普納

- 其他地區

- 資料中心規模

- 大規模

- 超大規模

- 中等規模

- 百萬

- 小規模

- 層級類型

- 1層級和2級

- 層級

- 層級

- 吸收量

- 未使用

- 使用

- 按主機託管類型

- 超大規模

- 零售

- 批發的

- 按最終用戶

- BFSI

- 雲

- 電子商務

- 政府

- 製造業

- 媒體與娛樂

- 電信

- 其他最終用戶

第7章競爭格局

- 市場佔有率分析

- 商業狀況

- 公司簡介.

- CtrlS Datacenters Ltd

- Equinix Inc.

- ESDS Software Solution Ltd

- Go4hosting

- NTT Ltd

- Nxtra Data Ltd

- Pi Datacenters Pvt Ltd

- Reliance

- Sify Technologies Ltd

- STT GDC Pte Ltd

- WebWerks

- Yotta Infrastructure Solutions

- LIST OF COMPANIES STUDIED

第8章:CEO面臨的關鍵策略問題

第9章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 全球市場規模和DRO

- 資訊來源及延伸閱讀

- 圖表清單

- 關鍵見解

- 資料包

- 詞彙表

The India Data Center Market size is estimated at 3.31 thousand MW in 2025, and is expected to reach 6.69 thousand MW by 2030, growing at a CAGR of 15.11%. Further, the market is expected to generate colocation revenue of USD 2,337.9 Million in 2025 and is projected to reach USD 4,931.8 Million by 2030, growing at a CAGR of 16.10% during the forecast period (2025-2030).

Tier 3 data center accounted for majority share in terms of volume in 2023, and is expected to dominate through out the forecasted period

- The growing urban population's adoption of smart technologies and attractive incentives offered by state governments has led data center operators setting up huge data processing facilities in the country.

- As businesses evolve in India, large businesses increasingly focus on tier 3 and tier 4 data centers due to their lower downtime, disaster recovery, and onsite assistance facility. This has led to the growth of tier 3 and tier 4 data centers in the region.

- Tier 3 data centers are expected to grow from 888.5 MW in 2022 to 3365.0 MW by 2029 at a CAGR of 16.20%. Similarly, tier 4 data centers operated at a capacity of 211.9 MW in 2021. This capacity is expected to increase from 211.9 MW in 2022 to 1380.2 MW by 2029 at a CAGR of 29.54%.

- As a result of low demand, tier 1 & 2 data center is expected to stagnate during the forecast period.

India Data Center Market Trends

Growth of telecom operators such as Jio, and others providing smartphones and internet services at resonable rates, it has boosted the data centers market

- Indian smartphone users are expected to grow from 794.4 million in 2022 to 1.2 billion in 2029 at a CAGR of 5.52%. Government initiatives such as the "Make in India" movement have offered incentives to the smartphone industry, which has resulted in India producing smartphones with specifications that run applications seamlessly and at an affordable cost.

- The growth of telecom operators, such as Jio, has revolutionized the internet industry with their packages at a reasonable cost. In addition to that, the data demand increased continuously, with the government encouraging digital payments and services online.

- With the launch of the 5G network in India, data consumption is expected to rapidly increase, as Indian users have a heavy inclination toward online OTT content, gaming, shopping, smart home automation applications, online security cams, etc., which is expected to further propel the demand for data centers.

Increasing household access to broadband and growing Internet exchanges are driving the market growth.

- A copper-based internet connection provides speeds of up to 300 Mbps whereas a fiber optic internet speeds are upto 10 Gbps. Earlier, the broadband network in India was more inclined toward copper cable connections. New innovations such as cloud technology have led to the adoption of fiber optic cables that offer higher speeds to move data stored in the cloud. Users are switching to fiber optic cables, which connect cloud servers with data centers. Hence, in terms of connectivity, the demand for copper cables is on the decline.

- Broadband connections rose from 6.1 crore in March 2014 to 81.62 crores in September 2022 growing by 1238%. The flagship BharatNet project is being implemented in phases to give broadband access to all 2.6 lakh Gramme Panchayats (GPs) in the country. Phase-I was finished in December 2017 and covered over 1 lakh GPs. As of October 2022, 6,00,898 km of Optical Fibre Cable had been laid under the project, 1,90,364 GPs had been connected by Optical Fibre Cable (OFC), and 1,77,665 GPs were Service Ready on OFC. Furthermore, 4466 GPs have been linked by satellite media. 1,82,131 GPs are ready to serve. This statistic shows an increase in broadband data usage.

- The growing urban population increasingly uses devices such as smart TVs, smartphones, and smart lighting systems, which has led to increased demand for higher bandwidth speeds that can only be achieved through the use of these fiber optic cables.

India Data Center Industry Overview

The India Data Center Market is moderately consolidated, with the top five companies occupying 55.86%. The major players in this market are Equinix Inc., NTT Ltd, Nxtra Data Ltd, Sify Technologies Ltd and STT GDC Pte Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 MARKET OUTLOOK

- 4.1 It Load Capacity

- 4.2 Raised Floor Space

- 4.3 Colocation Revenue

- 4.4 Installed Racks

- 4.5 Rack Space Utilization

- 4.6 Submarine Cable

5 Key Industry Trends

- 5.1 Smartphone Users

- 5.2 Data Traffic Per Smartphone

- 5.3 Mobile Data Speed

- 5.4 Broadband Data Speed

- 5.5 Fiber Connectivity Network

- 5.6 Regulatory Framework

- 5.6.1 India

- 5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

- 6.1 Hotspot

- 6.1.1 Bangalore

- 6.1.2 Chennai

- 6.1.3 Hyderabad

- 6.1.4 Mumbai

- 6.1.5 NCR

- 6.1.6 Pune

- 6.1.7 Rest of India

- 6.2 Data Center Size

- 6.2.1 Large

- 6.2.2 Massive

- 6.2.3 Medium

- 6.2.4 Mega

- 6.2.5 Small

- 6.3 Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 Absorption

- 6.4.1 Non-Utilized

- 6.4.2 Utilized

- 6.4.2.1 By Colocation Type

- 6.4.2.1.1 Hyperscale

- 6.4.2.1.2 Retail

- 6.4.2.1.3 Wholesale

- 6.4.2.2 By End User

- 6.4.2.2.1 BFSI

- 6.4.2.2.2 Cloud

- 6.4.2.2.3 E-Commerce

- 6.4.2.2.4 Government

- 6.4.2.2.5 Manufacturing

- 6.4.2.2.6 Media & Entertainment

- 6.4.2.2.7 Telecom

- 6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Landscape

- 7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 7.3.1 CtrlS Datacenters Ltd

- 7.3.2 Equinix Inc.

- 7.3.3 ESDS Software Solution Ltd

- 7.3.4 Go4hosting

- 7.3.5 NTT Ltd

- 7.3.6 Nxtra Data Ltd

- 7.3.7 Pi Datacenters Pvt Ltd

- 7.3.8 Reliance

- 7.3.9 Sify Technologies Ltd

- 7.3.10 STT GDC Pte Ltd

- 7.3.11 WebWerks

- 7.3.12 Yotta Infrastructure Solutions

- 7.4 LIST OF COMPANIES STUDIED

8 KEY STRATEGIC QUESTIONS FOR DATA CENTER CEOS

9 APPENDIX

- 9.1 Global Overview

- 9.1.1 Overview

- 9.1.2 Porter's Five Forces Framework

- 9.1.3 Global Value Chain Analysis

- 9.1.4 Global Market Size and DROs

- 9.2 Sources & References

- 9.3 List of Tables & Figures

- 9.4 Primary Insights

- 9.5 Data Pack

- 9.6 Glossary of Terms

全球配電中心市場:依類型、應用和地區劃分 - 市場規模、行業趨勢、機會分析和預測(2025-2033 年)

全球配電中心市場:依類型、應用和地區劃分 - 市場規模、行業趨勢、機會分析和預測(2025-2033 年) 資料中心設備及基礎設施市場:2025-2030

資料中心設備及基礎設施市場:2025-2030 高階主管簡報:2025 年第四季

高階主管簡報:2025 年第四季 資料中心遷移市場-2025-2030 年預測

資料中心遷移市場-2025-2030 年預測 AI資料中心的設備投資的明細和未來預測

AI資料中心的設備投資的明細和未來預測 全球資料中心服務市場按服務類型、設施服務、IT 服務、專業諮詢與認證、層級類型、資料中心規模與容量、資料中心類型、企業資料中心和地區分類 - 預測至 2030 年

全球資料中心服務市場按服務類型、設施服務、IT 服務、專業諮詢與認證、層級類型、資料中心規模與容量、資料中心類型、企業資料中心和地區分類 - 預測至 2030 年 資料中心資產管理市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

資料中心資產管理市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 全球企業 IT 資產處置市場規模、佔有率和行業分析報告:2025 年至 2032 年按資產類型、服務、行業和地區分類的展望和預測

全球企業 IT 資產處置市場規模、佔有率和行業分析報告:2025 年至 2032 年按資產類型、服務、行業和地區分類的展望和預測 資料中心市場:按組件、資料中心類型、層級、冷卻類型、電源、最終用戶和組織規模分類 - 全球預測,2025-2032 年

資料中心市場:按組件、資料中心類型、層級、冷卻類型、電源、最終用戶和組織規模分類 - 全球預測,2025-2032 年 2025年全球託管資料中心服務市場報告

2025年全球託管資料中心服務市場報告