|

市場調查報告書

商品編碼

1692577

歐洲 EVA 黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Europe EVA Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

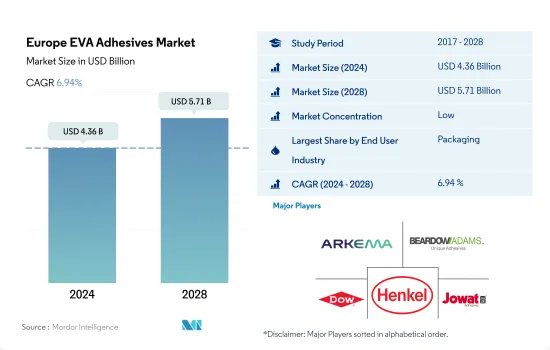

預計 2024 年歐洲 EVA 黏合劑市場規模將達到 43.6 億美元,預計到 2028 年將達到 57.1 億美元,預測期內(2024-2028 年)的複合年成長率為 6.94%。

包裝是成長最快的終端用戶,並將保持其在市場上的領先地位。

- EVA 黏合劑應用於各種終端用戶行業,包括包裝、汽車、木工和細木工以及建築和施工。這些黏合劑能夠黏合紙張、木材、塑膠、橡膠、金屬和皮革等基材。 EVA 黏合劑的常見應用包括紙/紙板盒、包裝標籤、紙箱密封、組裝、汽車內裝和紙張加工。

- 2017 年至 2019 年,EVA 黏合劑的需求大幅成長。在該地區所有國家的所有終端使用者產業中,西班牙建設產業的需求成長率最高(2017-2019 年複合年成長率為 11.07%)。住宅領域不斷成長的需求推動了西班牙的成長。

- 2020 年,由於營運和貿易限制、供應鏈限制以及 COVID-19 疫情造成的勞動力短缺等各種因素,所有終端用戶行業對 EVA 黏合劑的需求均下降。汽車產業需求受創最嚴重,較去年同期下降19.16%。旅行活動減少、原料短缺以及其他各種因素也導致了價格下降。隨著新冠疫情限制措施的放鬆,2021年全球對EVA黏合劑的需求已恢復至疫情前的水準。

- 預計這一成長趨勢將在 2022-2028 年預測期內持續下去。從數量上看,預測期內所有終端用戶行業對 EVA 黏合劑的需求預計將以 3.61% 的複合年成長率成長。包裝行業佔據了最高的需求佔有率,因為他們更喜歡 EVA 黏合劑,因為它具有快速固化的特性。預計在 2022-2028 年預測期內,它仍將是最大的最終用戶。

2022年歐洲新建占地面積將年增與前一年同期比較%,推動EVA膠合劑需求成長

- EVA樹脂基黏合劑由醋酸乙烯酯及其衍生物等聚合物製成。這些聚合物具有良好的耐熱性,因此主要用作基於熱熔技術的黏合劑。這些黏合劑用於六個以上的地理產業,包括建築、汽車和電子。這些黏合劑主要用於建築業,因為它們的非揮發性使其可安全用於建築業。由於建設產業的成長,市場也不斷成長,預計到 2022 年歐洲新建築占地面積將達到 76 億平方公尺,高於 2021 年的 73 億平方公尺。

- 其他歐洲國家地區佔據歐洲 EVA 樹脂基黏合劑市場的大部分佔有率。其他歐洲國家國家包括瑞典、挪威、波蘭和荷蘭等國家,這些國家的 EVA 樹脂黏合劑主要用於建築應用。預計2021年波蘭的住宅將比2020年增加30%,這也將推動對EVA樹脂基黏合劑的需求。

- 由於建築、醫療保健和汽車行業的不斷發展,德國是 EVA 黏合劑的主要消費國。 EVA 樹脂基黏合劑因其強大的結構性能而廣受歡迎,可用於許多應用,包括屋頂修復和汽車組裝。預計 2020 年將完成約 205,000 個計劃,汽車產量預計將從 2021 年的 330 萬輛成長到 2022 年的 2.94%。因此,預計歐洲 EVA 膠合劑市場在 2022 年和 2023 年的銷售成長率分別為 6.90% 和 5.60%。

歐洲EVA膠黏劑市場趨勢

歐洲食品飲料產業蓬勃發展,帶動包裝產業擴張

- 包裝是歐洲地區的關鍵產業之一。該地區是繼亞太地區之後全球第二大包裝產品生產地區,約佔全球包裝產量的24%。德國、俄羅斯、西班牙和英國是歐洲主要的包裝產品生產國。受新冠疫情影響,預計2020年包裝產量較2019年下降7.14%。今年,多個國家實施了全國封鎖,導致該地區的生產設施關閉了三到四個月。

- 俄羅斯是包裝產品主要生產國,2021年產量為2.138億噸,位居歐洲第一。近年來,俄羅斯包裝產業的發展很大程度上受到食品和飲料產業快速成長的推動。俄羅斯是全球主要食品出口國,進一步影響包裝銷售,以滿足一系列終端產業對複雜包裝的需求。

- 德國是歐洲領先的塑膠包裝生產國。 2021年塑膠包裝將佔包裝產量的約79%。塑膠包裝行業主要受到國內食品和飲料行業快速成長的推動。由於生活方式更加忙碌、消費能力增強及相關因素,該地區對快速和便攜包裝產品的需求正在增加。未來幾年,這一趨勢在歐洲包裝產品中將會成長。

政府對電動車的支持將擴大該產業

- 歐洲人均GDP為34,230美元,2022與前一年同期比較成長1.6%。汽車工業部門約佔GDP總量的2%。 2021年,歐洲汽車產量將佔乘用車81%,商用車17%,其他2%。

- 2020年,德國、義大利、西班牙、俄羅斯、英國等多個歐洲國家都受到新冠疫情影響。疫情擾亂了供應鏈,導致各國工廠關閉,並造成晶片短缺,影響了歐洲的汽車生產。汽車產量與2019年相比大幅下降22%。

- 美國25.3%的汽車進口來自歐洲,其中德國和英國是主要進口國,2021年分別佔10.3%和4.7%。 2022年初,俄羅斯入侵烏克蘭導致新車銷售下降20.5%,也反映在汽車產量上。 2022年第一季歐洲汽車市場與去年同期相比下降了10.6%。

- 由於許多歐洲國家正在對電動車進行新的投資,因此在 2022-2027 年期間,汽車產量的複合年成長率可能達到 2.25%。例如,西班牙計劃投資51億美元用於電動車生產。

歐洲EVA膠黏劑產業概況

歐洲EVA膠黏劑市場較為分散,前五大公司佔10.12%的市場佔有率。該市場的主要企業有:阿科瑪集團、Beardow Adams、陶氏、漢高股份公司和Jowat SE(按字母順序排列)

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築與施工

- 鞋類和皮革

- 包裝

- 木製品和配件

- 法律規範

- EU

- 俄羅斯

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 航太

- 車

- 建築與施工

- 鞋類和皮革

- 衛生保健

- 包裝

- 木製品和配件

- 其他最終用戶產業

- 科技

- 熱熔膠

- 溶劑型

- 水性

- 國家

- 法國

- 德國

- 義大利

- 俄羅斯

- 西班牙

- 英國

- 其他歐洲國家

第6章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- Arkema Group

- Beardow Adams

- Dow

- Follmann Chemie GmbH

- HB Fuller Company

- Henkel AG & Co. KGaA

- Jowat SE

- KLEBCHEMIE MG Becker GmbH & Co. KG

- Paramelt BV

- Soudal Holding NV

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 全球黏合劑和密封劑產業概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 促進因素、限制因素和機會

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 92414

The Europe EVA Adhesives Market size is estimated at 4.36 billion USD in 2024, and is expected to reach 5.71 billion USD by 2028, growing at a CAGR of 6.94% during the forecast period (2024-2028).

Packaging is the fastest-growing end-user and to remain as pole position in market

- EVA adhesives find applications in various end-user industries, including packaging, automotive, woodworking and joinery, and building and construction. These adhesives can bond substrates like paper, wood, plastics, rubbers, metals, and leather. Some major applications of these adhesives are paper/card stock boxes, package labeling, carton sealing, assembly, vehicle interiors, and paper conversion.

- The demand for EVA adhesives grew significantly from 2017 to 2019. The Spanish building and construction industry witnessed the highest growth (CAGR of 11.07% for 2017-2019) in demand among all end-user industries from all countries in the region. Increased demand from the residential sector fueled this growth in Spain.

- In 2020, the demand for EVA adhesives declined from all end-user industries because of various factors such as operational and trade restrictions, supply chain constraints, and labor shortages due to the COVID-19 pandemic. The demand from the automotive industry suffered the most, declining by 19.16% Y-o-Y. Reduced travel activity, shortage of raw materials, and various other factors also led to this decline. As the COVID-19 pandemic-induced restrictions eased, the global EVA adhesives demand rose back to pre-pandemic levels in 2021.

- This growth trend is expected to continue during the forecast period 2022-2028. In volume terms, the demand for EVA adhesives from all end-user industries combined is expected to record a CAGR of 3.61% during the forecast period. The packaging industry favors EVA adhesives over others because of their fast-curing properties and, thus, accounts for the highest share of the demand. It is expected to remain the largest end-user during the forecast period 2022-2028.

The rising new floor area in Europe by 4.10% y-o-y in 2022 to boost the demand for EVA adhesives in the coming years

- EVA resin-based adhesives are made of polymers such as vinyl acetate and their derivatives. These polymers show good thermal resistance, which is why they are mainly used as hot melt technology-based adhesives. These adhesives are used in more than six regional industries, including construction, automotive, and electronics. These adhesives are consumed mainly in the building and construction industry as their non-volatile nature makes them safe for use in the construction industry. The market is witnessing growth due to growth in the construction industry, with the new floor area of Europe constructions set to reach 7.6 billion square footage in 2022 from 7.3 billion in 2021.

- The Rest of Europe regional segment occupies a major share of the European EVA resin-based adhesives market. The Rest of Europe consists of countries such as Sweden, Norway, Poland, and the Netherlands, where EVA resin-based adhesives are primarily consumed for construction applications. Residential construction in Poland increased by 30% in 2021 compared to 2020, which is also expected to boost the demand for EVA resin-based adhesives.

- Germany is the prime consumer of EVA resin-based adhesives owing to the rising construction, healthcare, and automotive industries. EVA resin-based adhesives are popular due to their strong structural properties, which can be used in many applications, such as roof repairing and automotive assemblies. About 205 thousand projects were completed in 2020, and vehicle production was expected to increase by 2.94% in 2022 from 3.3 million units in 2021. Thus, the European EVA adhesives market is expected to register growth rates of 6.90% and 5.60% by volume during 2022 and 2023, respectively.

Europe EVA Adhesives Market Trends

Significant growth of food & beverage industry in Europe to escalate packaging industry

- Packaging is one of the major sectors of Europe region. The region is the second-largest producer of packaging products in the world, which holds about 24% of global packaging production after the Asia-Pacific region. Germany, Russia, Spain, and the United Kingdom are major producers of packaging products in Europe. It is seen that packaging production reduced by 7.14% in 2020 compared to 2019 due to the impact of the COVID-19 pandemic. During the year, a nationwide lockdown imposed by several countries halted the production facilities for three to four months in the region.

- Russia is a leading producer of packaging products producing 213.8 million tons in 2021, which is the highest in Europe. The Russian packaging industry has majorly been driven by the rapid growth of the food and beverages industry in recent years. Russia is a major exporter of food products worldwide, which further influences packaging sales to meet the need for sophisticated packaging across various-end use industries.

- Germany is the major producer of plastic packaging in Europe. Plastic packaging which nearly accounts for around 79% of the packaging produced in 2021. The plastic packaging industry is majorly driven by the rapid growth of the food and beverages industry in the country. With the rise in busier lifestyles, greater spending power, and related factors in the region, the demand for quick and on-the-go packaged products is increasing. This trend will rise in packaging products in the coming years in Europe.

Supportive government initiatives to promote electric vehicles will raise the industry size

- Europe has a GDP of 34,230 USD per capita with a growth rate of 1.6% y-o-y in 2022. The automotive industry sector contributes a percentage of around 2% of the total GDP. The European vehicle production comprises 81% passenger vehicles, 17% commercial vehicles, and 2% other vehicles in 2021.

- In 2020, many European countries were affected by the COVID-19 pandemic, including Germany, Italy, Spain, Russia, and the United Kingdom. The pandemic resulted in supply chain disruptions, lockdowns in the countries, and chip shortages which affected automotive production in Europe. The production of vehicles sharply declined by 22% compared to 2019.

- The United States imports 25.3% worth of cars from Europe and became one of the leading importers of the United States, where Germany accounted for 10.3% and the United Kingdom for 4.7% of total imports of vehicles in the country in 2021. At the beginning of 2022, the sale of the new vehicle dropped by 20.5% due to the invasion of Ukraine by Russia, which reflected in vehicle production as well. In the first quarter of 2022, the European automotive market was down by 10.6% compared to the same period last year.

- Vehicle production is likely to grow with a CAGR of 2.25% during the period (2022 to 2027) due to the new investments being made in electric vehicles by many European countries. For instance, Spain is going to invest USD 5.1 billion in electric vehicle production.

Europe EVA Adhesives Industry Overview

The Europe EVA Adhesives Market is fragmented, with the top five companies occupying 10.12%. The major players in this market are Arkema Group, Beardow Adams, Dow, Henkel AG & Co. KGaA and Jowat SE (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 EU

- 4.2.2 Russia

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Solvent-borne

- 5.2.3 Water-borne

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Arkema Group

- 6.4.2 Beardow Adams

- 6.4.3 Dow

- 6.4.4 Follmann Chemie GmbH

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Jowat SE

- 6.4.8 KLEBCHEMIE M. G. Becker GmbH & Co. KG

- 6.4.9 Paramelt B.V.

- 6.4.10 Soudal Holding N.V.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

丙烯酸樹脂熱熔膠市場-全球產業規模、佔有率、趨勢、機會和預測(按應用、分銷模式、地區和競爭細分,2020-2030 年)2025年全球磁磚膠黏劑市場報告

丙烯酸樹脂熱熔膠市場-全球產業規模、佔有率、趨勢、機會和預測(按應用、分銷模式、地區和競爭細分,2020-2030 年)2025年全球磁磚膠黏劑市場報告 全球可脫黏黏合劑市場 - 2025 至 2032 年

全球可脫黏黏合劑市場 - 2025 至 2032 年 EVA 黏合劑:市場佔有率分析、產業趨勢和統計數據、成長預測(2025-2030 年)中國黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)新加坡黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)英國黏合劑:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)馬來西亞黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)

EVA 黏合劑:市場佔有率分析、產業趨勢和統計數據、成長預測(2025-2030 年)中國黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)新加坡黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)英國黏合劑:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)馬來西亞黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年) 低創傷/親膚親和性市場規模、佔有率及成長分析(按類型、應用和地區)-2025-2032 年產業預測

低創傷/親膚親和性市場規模、佔有率及成長分析(按類型、應用和地區)-2025-2032 年產業預測

▼