|

市場調查報告書

商品編碼

1693413

中國黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)China Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

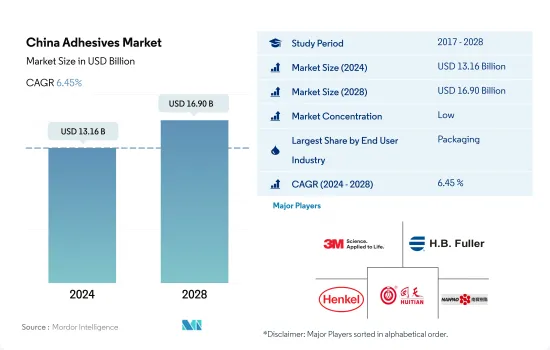

預計 2024 年中國黏合劑市場規模將達到 131.6 億美元,預計到 2028 年將達到 169 億美元,預測期內(2024-2028 年)的複合年成長率為 6.45%。

建築市場的崛起和軟包裝趨勢的演變預計將推動中國黏合劑的消費

- 中國膠合劑依用途可分為:建築和包裝是我國膠黏劑最主要的消費產業和發展最快的產業,約佔膠合劑總用戶的54%。受新冠疫情影響,2020年中國膠合劑消費量下降。從數量來看,同年的需求量與2019年相比下降了約8%。中國膠合劑產量和消費量的下降,主要是由於持續約半年的全國封鎖導致生產設施停工和勞動力短缺。

- 新中國成立前,包裝產業發展落後,但隨著新中國的成立,情況立即發生了全面的改變。中國包裝工業由小到大、由弱到強,建成了完整的現代化包裝體系,成為世界包裝強國。 2021年,中國包裝產業規模以上企業數量約達8,831家,較2020年增加648家。

- 中國是全球最大的建築市場,預計2022年至2030年期間年均成長率為8.6%。但槓桿率較高,政府正努力擺脫對土地出售的依賴。同時,該行業正受到人口老化和整體經濟衰退的影響。中國最近的設計和建築趨勢強調與當地社區、青年和文化相關的計劃。所有這些因素都傾向於增加該國對黏合劑的需求。

中國膠黏劑市場趨勢

食品飲料產業的快速成長以及對輕量化、軟包裝的需求不斷成長將推動中國包裝需求

- 包裝是設計和工程方面成長最快的行業之一,旨在保護和提高產品的安全性和壽命。食品和飲料行業佔中國包裝行業的大部分佔有率。 2019年食品飲料產業銷售額約5,950億美元,與前一年同期比較成長7.8%。憑藉強大的生產能力,中國已成為世界領先的食品和飲料出口國。

- 由於新冠疫情,全國範圍內的封鎖和製造工廠的暫時關閉導致了供應鏈中斷和進出口貿易等若干問題。因此,2020年該國包裝產量與前一年同期比較減8%,對市場造成了重大影響。該國的包裝生產主要由塑膠包裝驅動,約佔2021年包裝產量的79%。由於各種應用對輕質和軟性包裝的需求不斷增加,預計塑膠生產部門在預測期內將實現最快成長,複合年成長率約為6.58%。

- 中國包裝產業的成長主要得益於多年來中階人口的成長、供應鏈系統的完善以及電子商務活動的興起。此外,全國疫情爆發後,人們對食品安全和品質的關注度不斷提高,這可能會推動食品加工產業的發展,並在未來幾年進一步推動包裝需求。

政府政策可能會增加中國對電動車的需求,進而促進汽車生產。

- 中國是全球最大的乘用車市場,2021年保有量達2,141萬輛,與日本、美國、德國等全球主要汽車市場相比,保有量均位居第一。中國電動車製造商比亞迪佔全球電動車產量的8.84%。

- 中國是新冠肺炎疫情的中心,由於全國範圍內的停工、供應鏈中斷和人才短缺,2020 年中國汽車行業遭受了巨大損失。這就是2020年中國與前一年同期比較年增率為負的原因。

- 中國政府對電動車車主的限時購買補貼、交通豁免、充電回饋等政策促進了中國電動車的銷售和需求。預計2027年電動車銷量將達752.6萬輛。中國電動車產量預計將從2019年的100萬輛增加到2021年的350萬輛,預測期間(2022-2028年)的複合年成長率為15.07%。

- 上海工業Group Limited是中國產量最大的汽車製造商。上汽集團生產的乘用車和商用車數量大幅成長,從2019年的約200萬輛增加到2021年的700萬輛。這一成長趨勢表明,預計中國汽車市場在預測期內將穩定成長。

中國膠黏劑產業概況

中國膠合劑市場較為分散,前五大企業市佔率合計為11.81%。該市場的主要企業有:3M、HB Fuller Company、Henkel AG & Co. KGaA、湖北迴天新材料和南保樹脂化學集團(按字母順序排列)

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築與施工

- 鞋類和皮革

- 包裝

- 木製品和配件

- 法律規範

- 中國

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 航太

- 車

- 建築與施工

- 鞋類和皮革

- 衛生保健

- 包裝

- 木製品和配件

- 其他最終用戶產業

- 科技

- 熱熔膠

- 反應性

- 溶劑型

- 紫外線固化膠合劑

- 水

- 樹脂

- 丙烯酸纖維

- 氰基丙烯酸酯

- 環氧樹脂

- 聚氨酯

- 矽膠

- VAE,EVA

- 其他樹脂

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- 3M

- Arkema Group

- Beijing Comens New Materials Co., Ltd.

- HB Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co. Ltd

- Huntsman International LLC

- Kangda New Materials(Group)Co., Ltd.

- NANPAO RESINS CHEMICAL GROUP

- Sika AG

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 全球黏合劑和密封劑產業概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 促進因素、限制因素和機會

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 92472

The China Adhesives Market size is estimated at 13.16 billion USD in 2024, and is expected to reach 16.90 billion USD by 2028, growing at a CAGR of 6.45% during the forecast period (2024-2028).

Emerging construction market and evolving trend of flexible packaging expected to boost the consumption of adhesives in China

- Adhesives in China are categorized according to their application. Construction and packaging are the most important consumers in the country, accounting for roughly 54% of total adhesive users, owing to China's fastest-developing industries. China's adhesives consumption declined in 2020 due to the impact of COVID-19. In terms of volume, demand declined by approximately 8% in the same year as in 2019. The country's lockdown for around half a year, which prompted production facilities to shut down, and personnel unavailability are two of the primary reasons for the reduction in adhesives production and consumption in China.

- Before the establishment of New China, the packaging industry failed to keep pace, but the situation immediately and fully altered with the establishment of New China. China's packaging industry has advanced from tiny to huge and weak to strong, creating a fully modern packaging system and becoming the world's packaging power. The number of companies over the required size in China's packaging sector reached about 8,831 in 2021, an increase of 648 from 2020.

- China is the world's largest construction market, with an annual average growth rate of 8.6% projected between 2022 and 2030. However, it is heavily leveraged, and the government is enacting efforts to wean the economy off its reliance on land sales. At the same time, the sector is being impacted by an aging population and a general economic slump. Recent design and building trends in China emphasize local communities, younger people, and culturally relevant projects. All such factors tend to increase the demand for adhesives in the country.

China Adhesives Market Trends

Rapid growth of the food and beverage industry and rising demand for lightweight and flexible packaging to boost the China packaging demand

- Packaging is one of the fast-growing industries in terms of design and technology for protecting and enhancing products' safety and longevity. The food and beverage sector contributes a major share of the packaging industry in China. The food and beverage sector registered nearly USD 595 billion in 2019, more than 7.8% higher than the previous year. Owing to its high production capacity, China has positioned itself as a major exporter of food and drinks worldwide.

- Due to the COVID-19 pandemic, the country-wide lockdowns and temporary shutdown of manufacturing facilities caused several issues, including supply chain disruptions and imports and exports trade. As a result, the country's packaging production declined by 8% in 2020 compared to the previous year, significantly affecting the market. Packaging production is majorly driven by plastic packaging in the country, which nearly accounted for around 79% of the packaging produced in 2021. With the growing demand for lightweight and flexible packaging for a variety of applications, the plastic production segment is likely to register the fastest growth of around 6.58% CAGR during the projected period.

- The growth of the packaging industry in China is mainly attributed to the rising middle-class population, improvement of the supply-chain system, and emerging e-commerce activities over the years. Furthermore, the growing attention to food safety and quality in post-pandemic times across the nation is likely to drive the food processing industry, which will further contribute to the packaging demand in the coming years.

Owing to government policies, EVs demand in China is rising and is likely to propel the automotive production

- China's automotive market for passenger vehicles is the largest in the world, as it accounted for 21.41 million units in 2021 compared to other major global players such as Japan, the United States, and Germany. This number is expected to grow at the same pace because of the increasing production capacity of automotive companies post-pandemic in China, as BYD, which is a local electric vehicle manufacturer in China, holds 8.84% of total electric vehicle production in the world.

- China, being the epicenter of the COVID-19 pandemic, witnessed huge losses in the automotive industry in 2020 as it led to nationwide lockdowns, supply chain disruptions, lack of human resources availability, etc. This was the reason for the negative Y-o-Y growth rate in China in 2020.

- The Chinese government's policies for electric vehicle owners, such as time-limited purchase subsidies, traffic regulations waivers, and charging rebates for EV owners, have encouraged the sale and demand for EVs in China. The sales of electric vehicles are expected to reach 7,526 thousand in 2027. EV production in China increased from 1 million units in 2019 to 3.5 million units in 2021, and it is expected to record a 15.07% CAGR in the forecast period (2022-2028).

- Shanghai Automotive Industry Corporation is China's largest automotive company in terms of production. The growth in the number of both passenger and commercial vehicles manufactured by SAIC is significant, as it increased from nearly 2 million units in 2019 to 7 million units in 2021. This growth trend shows that the Chinese automotive market is expected to grow steadily during the forecast period.

China Adhesives Industry Overview

The China Adhesives Market is fragmented, with the top five companies occupying 11.81%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Hubei Huitian New Materials Co. Ltd and NANPAO RESINS CHEMICAL GROUP (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 China

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Resin

- 5.3.1 Acrylic

- 5.3.2 Cyanoacrylate

- 5.3.3 Epoxy

- 5.3.4 Polyurethane

- 5.3.5 Silicone

- 5.3.6 VAE/EVA

- 5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Beijing Comens New Materials Co., Ltd.

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Hubei Huitian New Materials Co. Ltd

- 6.4.7 Huntsman International LLC

- 6.4.8 Kangda New Materials (Group) Co., Ltd.

- 6.4.9 NANPAO RESINS CHEMICAL GROUP

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

有機熱連接件市場:依產品類型、應用、終端用戶產業及通路分類,全球預測(2026-2032年)橡皮筋黏合劑市場按類型、形式、分銷管道、應用和最終用戶分類,全球預測(2026-2032年)橡膠基材黏合劑市場按配方技術、樹脂類型、基材類型、最終用途產業和應用分類-全球預測,2026-2032年

有機熱連接件市場:依產品類型、應用、終端用戶產業及通路分類,全球預測(2026-2032年)橡皮筋黏合劑市場按類型、形式、分銷管道、應用和最終用戶分類,全球預測(2026-2032年)橡膠基材黏合劑市場按配方技術、樹脂類型、基材類型、最終用途產業和應用分類-全球預測,2026-2032年 2025-2032年全球塗料、黏合劑和密封劑添加劑(CAS)市場

2025-2032年全球塗料、黏合劑和密封劑添加劑(CAS)市場 全球黏合劑市場:機會與策略展望(至2034年)

全球黏合劑市場:機會與策略展望(至2034年) 整體包裝解決方案市場分析及預測(至2035年):依類型、產品類型、服務、技術、材料類型、應用、製程、最終用戶、功能、解決方案分類智慧黏合劑技術市場分析及預測(至2035年):依類型、產品、技術、應用、材料類型、最終用戶、功能、製程、形式及解決方案分類衛生黏合劑市場分析及預測(至2035年):類型、產品類型、應用、技術、材料類型、最終用戶、形態、組成、功能、工藝

整體包裝解決方案市場分析及預測(至2035年):依類型、產品類型、服務、技術、材料類型、應用、製程、最終用戶、功能、解決方案分類智慧黏合劑技術市場分析及預測(至2035年):依類型、產品、技術、應用、材料類型、最終用戶、功能、製程、形式及解決方案分類衛生黏合劑市場分析及預測(至2035年):類型、產品類型、應用、技術、材料類型、最終用戶、形態、組成、功能、工藝 東南亞黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

東南亞黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

▼