|

市場調查報告書

商品編碼

1693374

馬來西亞黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Malaysia Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

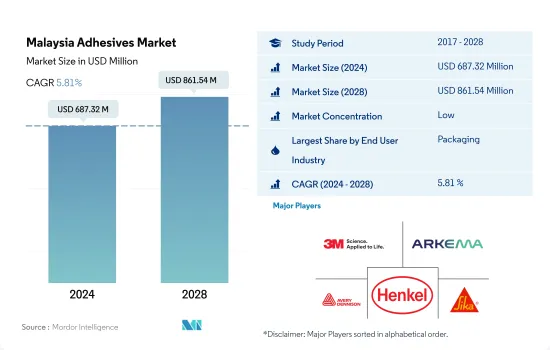

馬來西亞黏合劑市場規模預計在 2024 年為 6.8732 億美元,預計到 2028 年將達到 8.6154 億美元,預測期內(2024-2028 年)的複合年成長率為 5.81%。

包裝產業引領馬來西亞黏合劑需求

- 在馬來西亞,黏合劑主要用於包裝產業。就產量而言,預測期內馬來西亞包裝產業的複合年成長率預計將達到約 5.7%。軟包裝是許多行業和商品運輸系統的重要組成部分,包括消費品、電子產品、化妝品和醫療用品。目前,Ecoplas Sdn Bhd、Polymart、Tomypak Pvt.Ltd、Biszon 和 Taisei Lamick 是馬來西亞黏合劑市場的主要包裝公司。

- 汽車膠黏劑的消費主要依賴國內汽車生產。預計2022年汽車產量將從2021年的481,700輛成長8.5%。 2022年馬來西亞汽車膠黏劑消耗量成長率為8.43%。 2020 年,新冠疫情嚴重打擊了汽車黏合劑的消費。與 2019 年相比,2020 年的產量和價值均下降了約 10%。供應鏈中斷、原料短缺和國家封鎖導致汽車膠合劑生產停滯。

- 預計在 2022 年至 2028 年預測期內,馬來西亞建築膠合劑和密封劑市場銷量的複合年成長率約為 3.89%,價值的複合年成長率約為 6.23%。 2019 年,馬來西亞建築業產出約 1,463.7 億馬來西亞林吉特,較 2018 年略有成長。由於多個計劃因償還債務而停滯,馬來西亞建築業 2019 年成長放緩。由於多個大型建築計劃的停止以及未售出住宅庫存的增加,建設產業在 2019 年幾乎陷入停滯。

馬來西亞膠黏劑市場趨勢

電子商務行業的快速成長可能會擴大該行業的規模

- 包裝是保護和提升產品設計和技術方面成長最快的行業之一。近年來,馬來西亞包裝產業的發展很大程度上受到食品和飲料產業快速成長的推動。農業食品產業是馬來西亞最有前景的產業。在當今競爭激烈的快速消費品市場中,企業不可避免地要採用有吸引力的包裝並在包裝上進行創新,以在競爭對手中脫穎而出並在市場上保持其品牌形象。這可能會促進包裝黏合劑在市場上的使用。

- 由於新冠疫情,全國範圍內的封鎖和製造工廠的暫時關閉造成了一些問題,包括供應鏈和進出口貿易中斷。因此,2020年該國包裝產量較去年與前一年同期比較下降6%,對市場造成了重大影響。該國的包裝生產主要由塑膠驅動,佔2021年包裝產量的近86%。預計塑膠可回收性的提高將有助於塑膠產業在預測期內保持4%的複合年成長率。

- 馬來西亞包裝產業的成長很大程度上受到該國對生鮮食品需求不斷成長的推動。疫情爆發後,人們對公共衛生問題更加關注,加上全國電子商務活動的活性化,可能會促進食品加工行業的成長,從而進一步推動預測期內對包裝的需求。

電動車需求的不斷成長將影響該國的汽車產業

- 馬來西亞繼續成為跨國汽車製造商青睞的基地。本田、豐田、日產、梅賽德斯-奔馳和寶馬等全球汽車公司都已在中國設立業務,以滿足日益成長的客戶需求。汽車工業在馬來西亞工業領域佔有重要地位,貢獻了馬來西亞GDP的4%以上,是東協第三大汽車市場。馬來西亞目前擁有28家乘用車、商用車、摩托車、Scooter、汽車零件製造和組裝廠。

- 毫無疑問,該行業促進了工程、輔助和支援行業的發展。它還有助於技能發展和提高技術和工程能力。馬來西亞的汽車產業似乎未能免受全球數位化趨勢和新經營模式出現的影響。 2019年,該國汽車產量約571,632輛,但受新冠疫情影響,2020年產量暴跌至485,186輛,下降了15%。受此影響,2019年至2021年汽車產量波動約為-16%,而2020年至2021年則為-1%。

- 電動車(EV)已被國內汽車產業藍圖確定為未來汽車動力系統的關鍵技術。電動車最近才在馬來西亞產生重大影響。然而,馬來西亞缺乏電動車基礎設施和高度依賴石化燃料是主要障礙。

馬來西亞黏合劑產業概況

馬來西亞膠黏劑市場較分散,前五大公司佔18.36%。該市場的主要企業有:3M、阿科瑪集團、艾利丹尼森公司、漢高股份公司和西卡股份公司(按字母順序排列)

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築與施工

- 鞋類和皮革

- 包裝

- 木製品和配件

- 法律規範

- 馬來西亞

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 航太

- 車

- 建築與施工

- 鞋類和皮革

- 衛生保健

- 包裝

- 木製品和配件

- 其他最終用戶產業

- 科技

- 熱熔膠

- 反應性

- 溶劑型

- 紫外線固化膠合劑

- 水

- 樹脂

- 丙烯酸纖維

- 氰基丙烯酸酯

- 環氧樹脂

- 聚氨酯

- 矽膠

- VAE,EVA

- 其他樹脂

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- 3M

- Aica Kogyo Co..Ltd.

- Arkema Group

- AVERY DENNISON CORPORATION

- HB Fuller Company

- Henkel AG & Co. KGaA

- Mohm Chemical SDN. BHD.

- Sika AG

- Syarikat Chemibond Enterprise Sdn Bhd

- VITAL TECHNICAL SDN BHD

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 全球黏合劑和密封劑產業概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 促進因素、限制因素和機會

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 92429

The Malaysia Adhesives Market size is estimated at 687.32 million USD in 2024, and is expected to reach 861.54 million USD by 2028, growing at a CAGR of 5.81% during the forecast period (2024-2028).

Packaging industry leading in terms of demand for adhesives in Malaysia

- Across Malaysia, adhesives are largely being consumed across the packaging industry. The packaging industry of Malaysia is expected to record a CAGR of about 5.7% in terms of volume during the forecast period. Flexible packaging is an essential component of the transportation system for many industries and commodities, including consumer goods, electronics, cosmetics, and medical supplies. As of now, Ecoplas Sdn Bhd, Polymart, Tomypak Pvt. Ltd, Biszon, and Taisei Lamick are the leading packaging companies in the Malaysian adhesives market.

- The consumption of automotive adhesives mainly depends on automotive production in the country. Vehicle production was expected to increase by 8.5% in 2022 from 481.7 thousand units in 2021. Malaysia registered a growth rate of 8.43% in 2022 in automotive adhesives consumption. Automotive adhesives consumption was hit by the COVID-19 pandemic in 2020. Production fell by around 10% in terms of value and volume in 2020 compared to 2019. Supply chain disruptions, shortage of raw materials, and lockdowns in the countries caused a halt in the production of automotive adhesives at the time.

- The Malaysian construction adhesives and sealants market is projected to record a CAGR of about 3.89% in volume and 6.23% in value during the forecast period 2022 to 2028. In 2019, the construction output in Malaysia stood at approximately MYR 146.37 billion, exhibiting a slight growth over 2018. Malaysia's construction sector grew slower in 2019 as a few projects were stalled to cover the debt values. Owing to the halt in several mega construction projects, coupled with an increasing inventory of unsold housing stocks, the construction industry was almost stagnant in 2019.

Malaysia Adhesives Market Trends

Significant growth in the e-commerce industry is likely to proliferate the industry size

- Packaging is one of the fastest-growing industries in terms of design and technology for protecting and enhancing products. The packaging industry of Malaysia has been majorly driven by the rapid growth of the food and beverages industry in recent years. The agri-food industry is the most promising sector in Malaysia. In today's competitive market of FMCG, it has become inevitable for companies to use attractive packaging and bring innovation to their packaging to stand out from their competitors and maintain their brand image in the market. This is likely to encourage the use of packaging adhesives in the market.

- Due to the COVID-19 pandemic, the country-wide lockdowns and temporary shutdown of manufacturing facilities caused several issues, including disruptions in supply chains and imports and exports trade. As a result, the country's packaging production declined by 6% in 2020 compared to the previous year, significantly affecting the market. Packaging production is majorly driven by plastic in the country, which accounted for nearly 86% of the packaging produced in 2021. With the advancement of plastic recyclability, the plastic segment is likely to maintain its growth with a 4% CAGR during the forecast period.

- The growth of the packaging industry in Malaysia is significantly boosted by the growing demand for fresh food domestically. The increasing interest in public health issues during the post-pandemic period, along with the emerging e-commerce activities across the nation, is likely to boost the growth of the food processing industry, which will further drive the packaging demand in the forecast period.

Growing demand for electric vehicles will influence the country's automotive industry

- Malaysia remains an appealing base for multinational automakers. Honda, Toyota, Nissan, Mercedes-Benz, and BMW are among the global automobile corporations that have established operations in the country to capitalize on growing customer demand. The industry is a crucial part of the country's industrial sector, contributing above 4% of its GDP and remaining the third-largest automotive market in ASEAN. Malaysia currently has 28 manufacturing and assembly plants for passenger vehicles, commercial vehicles, motorcycles, and scooters, as well as automotive parts and components.

- The industry has undoubtedly aided the growth of engineering, auxiliary, and supporting sectors. It also helps with skill development and the advancement of technology and engineering capabilities. The automotive industry in Malaysia will not be immune to the global trend of digitalization and the advent of new business models. In 2019, the country produced about 5,71,632 units of vehicles, which drastically reduced to 4,85,186 units in 2020, with a 15% decline due to the COVID-19 pandemic. Due to this, the variation in automotive production between 2019 and 2021 was about -16%, whereas it was recorded at -1% between 2020 and 2021.

- The electric vehicle (EV) is recognized as a critical technology for the future of automotive power systems in the country's automotive industry's roadmaps. EVs have just recently emerged as a significant influence in Malaysia. However, in Malaysia, the absence of EV infrastructure and the country's heavy reliance on fossil fuels creates a considerable obstacle.

Malaysia Adhesives Industry Overview

The Malaysia Adhesives Market is fragmented, with the top five companies occupying 18.36%. The major players in this market are 3M, Arkema Group, AVERY DENNISON CORPORATION, Henkel AG & Co. KGaA and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 Malaysia

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Resin

- 5.3.1 Acrylic

- 5.3.2 Cyanoacrylate

- 5.3.3 Epoxy

- 5.3.4 Polyurethane

- 5.3.5 Silicone

- 5.3.6 VAE/EVA

- 5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Aica Kogyo Co..Ltd.

- 6.4.3 Arkema Group

- 6.4.4 AVERY DENNISON CORPORATION

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Mohm Chemical SDN. BHD.

- 6.4.8 Sika AG

- 6.4.9 Syarikat Chemibond Enterprise Sdn Bhd

- 6.4.10 VITAL TECHNICAL SDN BHD

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

彈性黏合劑市場規模、佔有率和趨勢分析報告:按樹脂、應用、地區和細分市場預測(2025-2033 年)

彈性黏合劑市場規模、佔有率和趨勢分析報告:按樹脂、應用、地區和細分市場預測(2025-2033 年) 光膠膜:全球市佔率及排名、總收入及需求預測(2025-2031年)陶瓷磚黏合劑:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

光膠膜:全球市佔率及排名、總收入及需求預測(2025-2031年)陶瓷磚黏合劑:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 永續黏合劑市場分析及至2034年的預測:類型、產品、應用、技術、材料類型、最終用戶、配方、製程、成分和應用類型黏著包裝解決方案市場分析及至2034年的預測:按類型、產品、服務、技術、材料類型、應用、流程、最終用戶、功能和解決方案

永續黏合劑市場分析及至2034年的預測:類型、產品、應用、技術、材料類型、最終用戶、配方、製程、成分和應用類型黏著包裝解決方案市場分析及至2034年的預測:按類型、產品、服務、技術、材料類型、應用、流程、最終用戶、功能和解決方案 按產品類型、黏合劑化學、黏合劑技術和最終用途產業分類的黏合劑市場-2025-2032年全球預測橡膠修補膠黏劑市場按產品類型、形態、應用、終端用戶產業、分銷管道和技術分類-2025-2032年全球預測混凝土黏合劑市場按產品類型、形式、應用和最終用途產業分類-2025-2032年全球預測

按產品類型、黏合劑化學、黏合劑技術和最終用途產業分類的黏合劑市場-2025-2032年全球預測橡膠修補膠黏劑市場按產品類型、形態、應用、終端用戶產業、分銷管道和技術分類-2025-2032年全球預測混凝土黏合劑市場按產品類型、形式、應用和最終用途產業分類-2025-2032年全球預測 導熱箔黏合劑市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年)

導熱箔黏合劑市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年) 全球永續黏合劑市場(按類型、原料、最終用途產業和地區分類)—預測至 2030 年

全球永續黏合劑市場(按類型、原料、最終用途產業和地區分類)—預測至 2030 年

▼