|

市場調查報告書

商品編碼

1689869

聯網汽車-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Connected Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

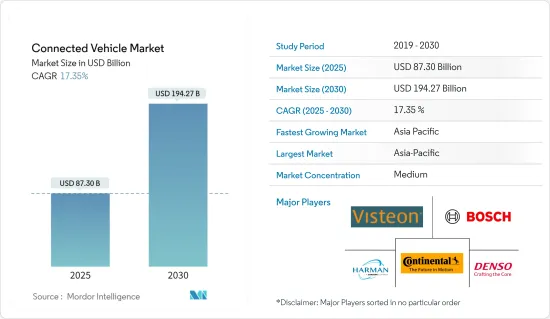

預計2025年聯網汽車市場規模為873億美元,到2030年預計將達到1942.7億美元,預測期內(2025-2030年)的複合年成長率為17.35%。

新冠疫情對所研究的市場產生了重大影響,因為封鎖和貿易限制擾亂了供應鏈並導致全球汽車生產停滯。然而,隨著法規的放寬,公司已開始專注於減輕此類風險和發展,以在預測期內為市場創造動力。

隨著 ADAS(高級駕駛輔助系統)和車輛資訊娛樂等先進的安全和舒適功能擴大融入車輛,市場正在經歷顯著成長。人們對乘客舒適度和安全性的認知不斷提高,以及政府對安全功能的強制性規定,正在推動整合 ADAS 功能的車輛的生產,預計這將推動市場需求。此外,自動駕駛汽車的日益普及也有助於推動市場成長。

世界各國政府正致力於設計多項立法政策和法規來監控用戶,並提案了強制和鼓勵消費者在車輛上安裝 ADAS 組件的政策,以減輕一些國家日益增多的道路交通事故。例如,印度政府非常重視提高汽車安全性,並已強制要求二輪車配備 ABS。印度目前正致力於在 2022-2023 年強制要求汽車安裝 ESC(電子穩定控制)和 AEB(自動緊急煞車)。

聯網汽車市場趨勢

汽車對 ADAS 功能的需求不斷增加

自動駕駛和聯網汽車已經引起了消費者的興趣,預計在預測期內將獲得廣泛認可。 ADAS(先進駕駛輔助系統)有望縮小傳統車輛和未來車輛之間的採用差距。此外,隨著汽車行業技術的不斷進步,最終用戶願意在最新技術上投入更多資金,以增強駕駛體驗並提高駕駛員和乘客的安全性。碰撞警告、車道輔助和盲點偵測等 ADAS 功能預計將對消費者行為產生重大影響,透過向車主發出車輛故障警報來減少車輛停機時間並提高車輛性能。

儘管 ADAS 已經取得了長足的進步,但連網汽車技術仍有很長的路要走。 V2V通訊具有進一步升級的潛力,因為車輛將能夠直接相互通訊,共用有關其相對速度、位置、航向甚至控制輸入(例如突然煞車、加速或改變方向)的資訊。利用這些資料以及車輛的感測器輸入,還可以創建更詳細的周圍環境圖像,並提供更準確的警告和糾正措施以避免碰撞。

然而,ADAS 組件的數量可能會繼續成長,因為以前在高階車型中發現的這些系統現在也被應用於入門級車型。這些系統為您的日常駕駛帶來了額外的安全保障。許多此類系統允許車輛根據情況調整駕駛方式。車輛可以根據情況進行轉向、煞車、加速等。例如,

根據 Canalys 的調查,2021 年上半年,歐洲銷售的新車中,56% 安裝了車道維持輔助系統,日本為 52%,中國當地為 30%,美國為 63%。車道維持系統輔助系統可在啟動時提供轉向輔助,幫助車輛維持在車道內。

市場上許多科技公司正在聯手解決 ADAS(高階駕駛輔助系統)開發的複雜性。例如

- 2022年6月,博泰車聯網與美國高通公司(Qualcomm)進一步拓展合作,共同開發支援車輛智慧化、智慧汽車聯網、服務導向架構(SOA)、基於集中控制設備的智慧駕駛座以及多領域融合的解決方案。

- 2021年7月,麥格納國際公司宣布計畫收購安全技術領導者維寧爾公司。麥格納國際公司已與維寧爾達成最終合併協議,以收購這家汽車安全技術領導者。透過此次收購,麥格納旨在加強其ADAS產品組合併擴大其行業地位。

亞太地區可望引領聯網汽車市場

由於最新汽車車型的連接功能不斷增強,亞太地區很可能在預測期內引領連網汽車市場。尤其是中國和印度等新興經濟體對汽車數位化功能的需求不斷成長,預計將推動該地區連網汽車市場的發展。

中國是全球最大的汽車市場之一,2021年國內乘用車銷量超過2,148萬輛,較2020年成長6%。儘管受到疫情影響,中國仍然是全球最大的汽車銷售國之一,這為預測技術在中國汽車市場發揮作用創造了絕佳機會。

中國政府正專注於電動車以及 ADAS 功能等多項先進汽車技術。因此,中國主要汽車製造商正在透過推出新的 2 級和 3 級 ADAS 功能來更新其產品組合。例如

- 2021年5月,長城汽車哈佛品牌全新緊湊級SUV赤兔上市,搭載1.5L渦輪增壓引擎(最大輸出功率135kW,最大扭力275Nm),組配7速濕式雙離合器變速箱。此外,它還配備了 2 級 ADAS 系統,其功能因版本而異。

隨著印度逐漸涉足汽車產業,專注於自動駕駛和人工智慧,並推出一系列新產品,聯網汽車市場擁有巨大的潛力和機會。例如

- 2021 年,Morris Garage 推出了新款 SUV Gloster,配備了基於預測技術的最新 ADAS 功能,包括自動緊急煞車、自動停車輔助、盲點偵測、前方碰撞警報和車道偏離警告。同樣在 2021 年,MG 推出了 Astor,這是一款經濟實惠的緊湊型 SUV,配備 2 級 ADAS 功能,例如主動式車距維持定速系統、自動緊急煞車、盲點偵測、車道維持輔助和車道偏離警告。

亞太地區、北美和歐洲在收益方面佔據最大的市場佔有率,預計在預測期內將會成長。預測技術領域的努力,例如在汽車中實施 ADAS 功能,可能會促進市場發展。

聯網汽車產業概況

聯網汽車市場主要由大陸集團、羅伯特博世有限公司、哈曼國際工業公司、電裝公司、Airbiquity 公司和偉世通公司主導。由於OEM已開始在其新車型中提供聯網汽車聯網汽車功能預計將成為中國和印度等新興市場的普遍現象。例如

- 2022 年 5 月,LEVC(倫敦電動車公司)宣布與物聯網和互聯交通領域的全球領導者 Geotab 建立新的合作夥伴關係,為其一流的電動計程車、TX 和 VN5 貨車提供尖端的車隊管理系統。

- 2021 年 8 月,羅伯特博世有限公司與 Mahindra & Mahindra 合作開發連網汽車平台。此次夥伴關係將促進汽車互聯平台的發展和進步。

- 2021年2月,福特汽車與Google達成策略夥伴關係關係,共同應用開發聯網汽車服務應用。此次合作將有助於加強福特汽車的連網汽車業務。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場促進因素

- 市場限制

- 波特五力分析

- 新進入者的威脅

- 購買者和消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 依技術類型

- 4G/LTE

- 3G

- 2G

- 按應用

- 駕駛員輔助

- 遠端資訊處理

- 資訊娛樂

- 其他

- 按連接性

- 融合的

- 嵌入式

- 網路分享

- 車輛連接性別

- 車對車(V2V)

- 車輛到基礎設施 (V2I)

- 車輛對行人 (V2P)

- 乘車

- 搭乘用車

- 商用車

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 韓國

- 其他亞太地區

- 世界其他地區

- 南美洲

- 中東和非洲

- 北美洲

第6章競爭格局

- 供應商市場佔有率

- 公司簡介

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Visteon Corporation

- Harman International

- AT&T Inc.

- TomTom NV

- Airbiquity Inc.

- Qualcomm Technologies Inc.

- Sierra Wireless

- Infineon Technologies

- Magna International

- ZF Friedrichshafen AG

第7章 市場機會與未來趨勢

The Connected Vehicle Market size is estimated at USD 87.30 billion in 2025, and is expected to reach USD 194.27 billion by 2030, at a CAGR of 17.35% during the forecast period (2025-2030).

The COVID-19 pandemic had a massive impact on the market studied as lockdowns and trade restrictions have led to supply chain disruptions and a halt of vehicle production across the globe. However, as restrictions eased, players started focusing on mitigating such risks and developments to create momentum in the market during the forecast period.

The rising integration of advanced safety and comfort features in the vehicle, such as advanced driver assistance systems, vehicle infotainment, and many others witnessing major growth in the market. Growing production of vehicles with integrated ADAS features in the wake of rising awareness toward comfort and safety of passengers and government regulations mandating safety features are expected to drive demand in the market. Moreover, the rising acceptance of self-driving or automated vehicles further contributes to the enhanced growth of the market.

Governments across the globe are focusing on designing several legislative policies and regulations to monitor the users and are proposing policies mandating and encouraging consumers to install ADAS components in vehicles to mitigate rising road accidents across several countries. For instance, the Indian government has already mandated a requirement for ABS on motorcycles with a focus on improving vehicle safety. Currently, India is working to make Electronic Stability Control (ESC) and Autonomous Emergency Braking (AEB) mandatory in cars by 2022-2023.

Connected Vehicle Market Trends

Growing demand for ADAS features in vehicle

Autonomous cars and connected vehicles are gaining consumers' interest and are anticipated to gain wider acceptance over the forecast period. The advanced driver assistance systems (ADAS) featured are expected to diminish the penetration gap between traditional cars and tomorrow's cars. Moreover, With the rising technological advancements in the automotive industry, end users are ready to spend more on the latest technologies, which enhance the driving experience and increase the safety of drivers and riders. ADAS features, such as collision warning, lane assistance, blind spot detection, etc., have a significant impact on consumer behavior and are expected to enhance vehicles' performance by reducing vehicle downtime by alerting the owner of any faults in the vehicle.

ADAS has advanced considerably, but there is still a long way to go with connected vehicle technology. V2V communication has the potential to upgrade it further, as vehicles may communicate with each other directly and share information on relative speeds, positions, directions of travel, and even control inputs, such as sudden braking, accelerations, or changes in direction. By using this data with the vehicle's sensor inputs, it is possible to create a more detailed picture of the surrounding area and provide more accurate warnings or even corrective actions to avoid collisions.

However, the number of ADAS components may keep growing, as these previously available systems in high-end models are now being used in entry-level vehicles. These systems bring added safety and security to daily driving. Many of these systems allow the vehicle to make driving adjustments according to the condition. Functions, such as steering, braking, and accelerating, can be performed by the vehicle in certain situations. For instance,

Research conducted by Canalys shows that the lane-keep assist feature, which when activated provides steering assistance to keep a vehicle in its lane, was installed in 56% of new cars sold in Europe in the first half of 2021, 52% in Japan, 30% in Mainland China, and 63% in the United States.

Many technology companies in the market are teaming up to solve the complexities of developing advanced driver-assistance systems (ADAS). For instance,

- In June 2022, PATEO Corporation and Qualcomm Technologies, Inc. (Qualcomm) expanded their relationship to develop solutions to support vehicle intelligence, smart car connectivity, Service-Oriented Architecture (SOA), and intelligent cockpits and multi-domain fusion based on central controllers.

- In July 2021, Magna International Inc. announced its plans to acquire safety tech major Veoneer Inc. Magna International Inc. entered a definitive merger agreement with Veoneer Inc., under which the company plans to acquire Veoneer Inc., a leading player in automotive safety technology. With this acquisition, Magna's aimed to strengthen and broaden its ADAS portfolio and industry position.

Asia-Pacific is Likely to Lead the Connected Vehicle Market

Asia-Pacific is likely to lead the connected vehicle market over the forecast owing to the increase in the connectivity features in the latest car models. The rise in demand for digital features in vehicles, especially in developing countries like China and India, is anticipated to drive the connected vehicle market in the region.

China is one of the largest automotive markets in the world, and more than 21.48 million passenger cars were sold in the country in 2021 and recorded a 6% surge in sales compared to 2020. Despite the pandemic, China is still one of the largest sellers of automobiles, which is a great opportunity for predictive technology to make its place in the Chinese automobile market.

The Chinese government is focusing on several advanced vehicles technology, like ADAS features, along with electric mobility. With that, major automakers in the country are updating their portfolio with the introduction of the new level 2 and level 3 ADAS features. For instance,

- In May 2021, the HAVAL brand of Great Wall Motor Co. Ltd launched the new Chitu compact SUV, and it is equipped with a 1.5L turbocharged engine (maximum power output of 135kW, peak torque of 275Nm) in combination with a 7-speed wet dual-clutch transmission. In addition, the vehicle includes a Level 2 ADAS system, with varying functions depending on the version.

India has a potential and opportunity for a connected vehicle market as India is stepping gradually into the autonomous and artificial intelligence-oriented automotive industry along with many new product launches. For instance,

- In 2021, Morris Garage launched its new SUV Gloster, which is equipped with the latest ADAS features based on predictive technology such as automatic emergency brake, automatic parking assist, blind spot detection, forward collision warning, and lane departure warning. MG, in 2021, has launched another SUV, the Astor, an affordable compact SUV with level-2 ADAS features such as Adaptive Cruise Control, Automatic Emergency Braking, Blind Spot Detection, Lane-keeping Assist, and Lane Departure Warning.

Followed by Asia-Pacific, North America, and Europe, also witnessing significant market share in terms of revenue and are projected to grow during the forecast period. Initiatives toward the predictive technology sector, such as implementing ADAS features in cars, are going to boost the market.

Connected Vehicle Industry Overview

The connected vehicle market is dominated by Continental AG, Robert Bosch GmbH, Harman International Industries, Inc., DENSO Corporation, Airbiquity Inc, and Visteon Corporation. Connected vehicles' features are poised to become a common phenomenon in developing nations such as China, India, etc., market over the forecast period, as OEMs have started offering connected car features in their new respective models. For instance,

- In May 2022, LEVC (London Electric Vehicle Company) announced a new partnership with the global leader in IoT and connected transportation, Geotab, providing state-of-the-art fleet management systems on its class-leading electric TX taxi and VN5 van.

- In August 2021, Robert Bosch GmbH joined with Mahindra & Mahindra for the development of a connected vehicle platform. This partnership helps to grow and boost the connected platform in vehicles.

- In February 2021, Ford Motors and Google signed a strategic partnership for the development of connected car service applications. This partnership helps to enhance the ford motors connected vehicle business.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Technology Type

- 5.1.1 4G/LTE

- 5.1.2 3G

- 5.1.3 2G

- 5.2 By Application

- 5.2.1 Driver Assistance

- 5.2.2 Telematics

- 5.2.3 Infotainment

- 5.2.4 Others

- 5.3 By Connectivity

- 5.3.1 Integrated

- 5.3.2 Embedded

- 5.3.3 Tethered

- 5.4 By Vehicle Connectivity

- 5.4.1 Vehicle to Vehicle (V2V)

- 5.4.2 Vehicle to Infrastructure (V2I)

- 5.4.3 Vehicle to Pedestrian (V2P)

- 5.5 By Vehicle

- 5.5.1 Passenger cars

- 5.5.2 Commercial Vehicle

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 India

- 5.6.3.2 China

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Rest of the World

- 5.6.4.1 South America

- 5.6.4.2 Middle-East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Robert Bosch GmbH

- 6.2.2 Continental AG

- 6.2.3 Denso Corporation

- 6.2.4 Visteon Corporation

- 6.2.5 Harman International

- 6.2.6 AT&T Inc.

- 6.2.7 TomTom N.V.

- 6.2.8 Airbiquity Inc.

- 6.2.9 Qualcomm Technologies Inc.

- 6.2.10 Sierra Wireless

- 6.2.11 Infineon Technologies

- 6.2.12 Magna International

- 6.2.13 ZF Friedrichshafen AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

聯網汽車生態系統市場規模、佔有率和成長分析:按連接類型、技術、應用、車輛類型、銷售管道和地區分類-2026-2033年產業預測

聯網汽車生態系統市場規模、佔有率和成長分析:按連接類型、技術、應用、車輛類型、銷售管道和地區分類-2026-2033年產業預測 聯網汽車市場規模、佔有率和成長分析:按連接技術、服務類型、通訊方式、車輛類型、最終用戶和地區分類-2026-2033年產業預測

聯網汽車市場規模、佔有率和成長分析:按連接技術、服務類型、通訊方式、車輛類型、最終用戶和地區分類-2026-2033年產業預測 2026-2030年全球聯網汽車市場

2026-2030年全球聯網汽車市場 聯網汽車市場:2026-2032年全球市場預測(按組件類型、連接技術、通訊方式、網路類型、應用、車輛類型和最終用戶分類)聯網汽車市場:按連接類型、通訊技術、車輛類型、提供的服務和應用分類-2026-2032年全球市場預測

聯網汽車市場:2026-2032年全球市場預測(按組件類型、連接技術、通訊方式、網路類型、應用、車輛類型和最終用戶分類)聯網汽車市場:按連接類型、通訊技術、車輛類型、提供的服務和應用分類-2026-2032年全球市場預測 聯網汽車市場:按車輛類型、最終用戶行業、通訊類型、連接性別和地區分類

聯網汽車市場:按車輛類型、最終用戶行業、通訊類型、連接性別和地區分類 2026年全球汽車互聯控制單元市場報告2026年全球聯網汽車市場報告

2026年全球汽車互聯控制單元市場報告2026年全球聯網汽車市場報告 全球聯網汽車市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球聯網汽車市場規模、佔有率、趨勢和成長分析報告(2026-2034) 聯網汽車技術市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測

聯網汽車技術市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測