|

市場調查報告書

商品編碼

2073614

南美洲特種肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)South America Specialty Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

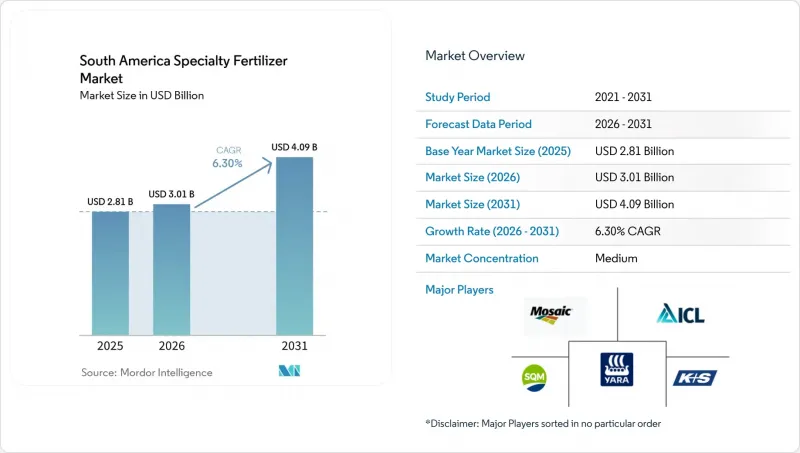

據 Mordor Intelligence 稱,2025 年南美洲特種肥料市場價值為 28.1 億美元,預計到 2031 年將從 2026 年的 30.1 億美元成長至 40.9 億美元,預測期(2026-2031 年)複合年成長率為 6.30%。

本報告依特殊肥料類型(控釋肥、液體肥料、緩釋肥、水溶性肥料)、施用方法(灌溉施肥、葉面噴布、土壤施用)、作物類型(田間作物、園藝作物、草坪和觀賞作物)以及國家(阿根廷、巴西和其他南美國家)進行分類。市場預測以價值(美元)和數量(公噸)表示。

南美洲特種肥料市場趨勢與洞察

滴灌灌溉面積迅速增加

2019年至2024年間,巴西灌溉面積增加了12%,達到820萬公頃。在這成長過程中,滴灌系統發展最為迅速。由於滴灌需要完全水溶性的肥料,因此專用肥料對於防止發送器堵塞以及根據作物需求提供養分至關重要。在阿根廷,新增的180萬公頃灌溉面積(主要位於門多薩的葡萄園和北部柑橘園)進一步提高了液態和水溶性肥料的使用率。區域農業設備製造商的年銷售額成長了15%至20%,強化了精準灌溉和肥料創新之間的良性循環。產量數據顯示,採用水溶性氮磷鉀肥和微量元素螯合物進行施肥,可使產量提高8%至10%,這表明即使在商品價格波動的情況下,這項投資也卓有成效。當地農業服務供應商現在提供與灌溉設備捆綁銷售的施肥諮詢服務,並加快了農民的學習進程。隨著滴灌技術在巴拉圭和烏拉圭的普及,跨國對水溶性混合肥料的需求不斷成長,擴大了南美洲特殊肥料的潛在基本客群。

政府對高效肥料的稅收優惠

在巴西,2024年的一項稅制改革將緩釋和長效肥料的PIS/COFINS稅率從9.25%降至3.65%,導致零售價格下降約6%。阿根廷隨後也採取了類似措施,降低了聚合物包衣尿素和生物促效劑添加劑的進口關稅,並將其與ISO 14001認證的退稅政策掛鉤。初步市場數據顯示,緩釋肥料推出僅六個月,出貨量就成長了23%。這項政策加強了環境保護與盈利之間的聯繫,加速了緩釋肥料在高價值園藝領域的市場滲透,同時也促進了大豆、玉米和棉花等大面積農田的種植。在過渡期內,當地肥料混合商利用庫存抵免迅速將產品系列轉向包覆產品。由於稅收優惠將於2026年到期,製造商預計,在產量提高和每公頃人事費用降低的支撐下,市場需求將持續成長。鄰國政府也密切關注巴西的模式,有跡象表明,一股更廣泛的獎勵浪潮將席捲整個南美特種肥料市場經濟。

與通用肥料相比,初始成本較高

特種肥料的售價比傳統複合肥料高出25%至40%,這對巴西390萬小規模農戶(佔農業企業總數的77%)造成了障礙。當農作物價格下跌時,生產者會轉而使用價格較低的散裝肥料。在阿根廷,由於許多農資以美元計價,披索疲軟進一步擴大了價格差距。經銷商正透過季節性信貸計畫和糧食以物易物項目來應對,但由於還款風險,利率仍居高不下。在勞動力充裕但產量成長潛力有限的地區,缺乏成本分攤獎勵減緩了特種肥料的普及。政府的代金券計畫仍處於試行階段,短期內只能提供有限的協助。因此,預計未來兩年,價格敏感性將使南美特種肥料市場的複合年成長率下降約1.8%。

細分市場分析

2025年,液態肥料在南美洲特種肥料市場佔據了36.6%的主導地位。這主要得益於其與柑橘、咖啡和甘蔗人工林中使用的灌溉施肥和葉面噴布系統的結合使用。快速吸收、均勻混合以及與作物保護劑的罐混相容性促進了其廣泛應用。儘管緩釋肥料的市佔率較小,但預計2026年至2031年間其複合年成長率將達7.4%。這反映出巴西的稅收減免和強制性硝酸鹽含量上限政策使得這種高效的肥料更具成本競爭力。

近年來,減緩結晶速度的技術進步也推動了液態肥料的普及,其優點包括減少施肥頻率、降低人力成本以及提高儲存穩定性。同時,聚合物包膜顆粒肥料在大型糧食種植田中表現出色,其一次性施用的便利性足以彌補較高的初始成本。硫包膜尿素在棉花和玉米種植中日益普及,而聚合物硫混合肥料則被應用於注重成本控制的大豆種植區。緩釋有機-無機混合肥料在有機認證生產商中佔據了一席之地。總體而言,產品系列多元化使供應商能夠規避天氣、價格波動和政策變化帶來的風險,從而在各個專業領域保持穩健的獲利能力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 主要農作物種植面積

- 田間作物

- 園藝作物

- 平均施肥量

- 微量營養素

- 田間作物

- 園藝作物

- 主要營養素

- 田間作物

- 園藝作物

- 次要營養元素

- 田間作物

- 園藝作物

- 微量營養素

- 配備灌溉設施的農田

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 滴灌灌溉面積迅速增加

- 政府對高效肥料的稅收優惠

- 提高大豆和玉米雙季種植密度

- 加強對硝酸鹽淋溶的水質監管。

- 生物促效劑和肥料預混合料的整合

- 利用區塊鏈技術實現可追溯性,進而增加價值。

- 市場限制因素

- 與通用肥料相比,初始成本較高

- 巴西內陸地區物流基礎設施匱乏

- 缺乏熱帶土壤中不同作物的田間試驗數據。

- 外匯波動影響進口成本

第5章 市場規模與成長預測

- 按類型分類的專用肥料

- 控制釋放肥料(CRF)

- 聚合物塗層

- 聚合物和硫塗層

- 其他

- 液體肥料

- 緩效性肥料(SRF)

- 水溶性肥料

- 控制釋放肥料(CRF)

- 透過應用方法

- 施肥和灌溉

- 葉面噴布

- 土壤

- 按作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

- 國家

- 阿根廷

- 巴西

- 其他南美國家

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介

- EuroChem Group

- SQM SA

- The Mosaic Company

- ICL Group Ltd.

- K+S Aktiengesellschaft

- Yara International ASA

- Grupa Azoty SA(Compo Expert GmbH)

- Haifa Group

- TIMAC Agro Brasil(Groupe Roullier)

- Nutrien

- Compass Minerals International Inc.

- Koch Agronomic Services LLC(Koch Industries)

- Valagro(Syngenta Group)

- AgroLiquid

- Omex Agrifluids Ltd.

第7章 化肥產業執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the south america specialty fertilizer market size was valued at USD 2.81 billion in 2025 and estimated to grow from USD 3.01 billion in 2026 to reach USD 4.09 billion by 2031, at a CAGR of 6.30% during the forecast period (2026-2031).

This report is Segmented by Speciality Type (CRF, Liquid Fertilizer, SRF, and Water Soluble), by Application Mode (Fertigation, Foliar, and Soil), by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and by Country (Argentina, Brazil, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

South America Specialty Fertilizer Market Trends and Insights

Surge in Drip-Irrigated Acreage

Brazil's irrigated land expanded 12% between 2019 and 2024, reaching 8.2 million ha, with drip systems the fastest-growing share. Drip technology requires fully soluble inputs, making specialty fertilizers essential to prevent emitter clogging and to match nutrient pulses with crop demand. Argentina added 1.8 million ha, chiefly in Mendoza vineyards and northern citrus groves, reinforcing liquid and water-soluble uptake. Regional equipment manufacturers posted 15-20% annual sales growth, reinforcing the feedback loop between precision irrigation and fertilizer innovation. Yield data show 8-10% gains when fertigation combines soluble NPK with micronutrient chelates, validating investment even under volatile commodity prices. Local agronomic service providers now bundle irrigation kits with nutrition advisories, speeding farmer learning curves. As drip lines penetrate Paraguay and Uruguay, cross-border demand for soluble blends climbs, widening the addressable base of the South America specialty fertilizer market.

Government Tax Incentives on Enhanced-Efficiency Fertilizers

Brazil's 2024 reform cut PIS/COFINS on controlled-release and slow-release fertilizers from 9.25% to 3.65%, trimming retail prices about 6%. Argentina matched with lower import duties on polymer-coated urea and biostimulant additives, aligning with ISO 14001 certification rebates. Early market data show controlled-release tonnage up 23% just six months after rollout. The policy tightens the link between environmental stewardship and profitability, accelerating market penetration beyond high-value horticulture into broadacre soybean, corn, and cotton. Local blenders rapidly shifted portfolios toward coated products, leveraging transitional inventory credits. As fiscal benefits sunset in 2026, manufacturers expect demand stickiness given demonstrable yield boosts and lower labor costs per hectare. Neighboring governments monitor the Brazilian model, foreshadowing a broader incentive wave across South America specialty fertilizer market economies.

High Upfront Cost versus Commodity Fertilizers

Specialty fertilizers sell at 25-40% premiums to conventional NPK, a hurdle for Brazil's 3.9 million smallholders who comprise 77% of farm units. When crop prices soften, growers revert to cheaper bulk nutrients. Peso depreciation in Argentina magnifies price gaps because many inputs are dollar-denominated. Distributors counter with seasonal credit plans and grain-barter programs, but repayment risk keeps interest rates high. Without cost-sharing incentives, adoption lags in zones where labor is abundant and yield ceilings are lower. Government voucher schemes remain pilot-scale, limiting near-term relief. Consequently, price sensitivity chops an estimated 1.8% from the South America specialty fertilizer market CAGR forecast over the next two years.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Soybean and Corn Double-Cropping Intensity

- Tightening Water-Quality Regulations on Nitrate Leaching

- Limited Distribution Infrastructure in Interior Brazil

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid fertilizers held a dominant 36.6% share of the South America specialty fertilizer market in 2025, boosted by integration with fertigation and foliar equipment used in citrus, coffee, and sugarcane plantations. Rapid absorption, uniform mixing, and compatibility with crop-protection tank mixes underpin adoption. Controlled-release fertilizers, though smaller, are forecast to deliver a 7.4% CAGR during 2026-2031, reflecting Brazil's tax cuts and mandatory nitrate caps that make enhanced-efficiency options cost-competitive.

Operational gains also favor liquids, such as fewer passes, reduced labor, and better shelf stability after recent innovations that slow crystallization. Conversely, polymer-coated granules thrive in broadacre grains where single-application convenience offsets higher upfront cost. Sulfur-coated urea finds traction in cotton and corn, while polymer-sulfur hybrids serve cost-sensitive soy areas. Slow-release organo-mineral blends occupy a niche among organic-certified growers. Overall, product portfolio diversification allows suppliers to hedge against weather, price swings, and policy shifts, sustaining revenue robustness across specialty categories.

Complete Report Scope:

- Specialty Type

- Controlled-Release Fertilizer (CRF)

- Polymer-Coated

- Polymer-Sulfur-Coated

- Others

- Liquid Fertilizer

- Slow-Release Fertilizer (SRF)

- Water-Soluble Fertilizer

- Controlled-Release Fertilizer (CRF)

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

- Country

- Argentina

- Brazil

- Rest of South America

List of Companies Covered in this Report:

- EuroChem Group

- SQM S.A.

- The Mosaic Company

- ICL Group Ltd.

- K+S Aktiengesellschaft

- Yara International ASA

- Grupa Azoty S.A. (Compo Expert GmbH)

- Haifa Group

- TIMAC Agro Brasil (Groupe Roullier)

- Nutrien

- Compass Minerals International Inc.

- Koch Agronomic Services LLC (Koch Industries)

- Valagro (Syngenta Group)

- AgroLiquid

- Omex Agrifluids Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped for Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Surge in drip-irrigated acreage

- 4.6.2 Government tax incentives on enhanced-efficiency fertilizers

- 4.6.3 Increasing soybean and corn double-cropping intensity

- 4.6.4 Tightening water-quality regulations on nitrate leaching

- 4.6.5 Biostimulant-fertilizer premix integration

- 4.6.6 Blockchain-based traceability premiums

- 4.7 Market Restraints

- 4.7.1 High upfront cost vs. commodity fertilizers

- 4.7.2 Limited distribution infrastructure in interior Brazil

- 4.7.3 Lack of crop-specific field trial data for tropical soils

- 4.7.4 Currency-exchange volatility impacting import costs

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Specialty Type

- 5.1.1 Controlled-Release Fertilizer (CRF)

- 5.1.1.1 Polymer-Coated

- 5.1.1.2 Polymer-Sulfur-Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 Slow-Release Fertilizer (SRF)

- 5.1.4 Water-Soluble Fertilizer

- 5.1.1 Controlled-Release Fertilizer (CRF)

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

- 5.4 Country

- 5.4.1 Argentina

- 5.4.2 Brazil

- 5.4.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 EuroChem Group

- 6.4.2 SQM S.A.

- 6.4.3 The Mosaic Company

- 6.4.4 ICL Group Ltd.

- 6.4.5 K+S Aktiengesellschaft

- 6.4.6 Yara International ASA

- 6.4.7 Grupa Azoty S.A. (Compo Expert GmbH)

- 6.4.8 Haifa Group

- 6.4.9 TIMAC Agro Brasil (Groupe Roullier)

- 6.4.10 Nutrien

- 6.4.11 Compass Minerals International Inc.

- 6.4.12 Koch Agronomic Services LLC (Koch Industries)

- 6.4.13 Valagro (Syngenta Group)

- 6.4.14 AgroLiquid

- 6.4.15 Omex Agrifluids Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOs

美國特種肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)越南特種肥料市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區特種肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

美國特種肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)越南特種肥料市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區特種肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 特種肥料市場-全球產業規模、佔有率、趨勢、機會和預測:按作物類型、形態、應用方法、技術、地區和競爭格局分類,2021-2031年

特種肥料市場-全球產業規模、佔有率、趨勢、機會和預測:按作物類型、形態、應用方法、技術、地區和競爭格局分類,2021-2031年 晶體肥料市場:2026-2032年全球市場預測(依養分類型、應用、形態、作物類型、作用機制與銷售管道)特種肥料市場:2026-2032年全球市場預測(依產品形式、作物類型、養分類型、施用方法、通路和最終用途分類)

晶體肥料市場:2026-2032年全球市場預測(依養分類型、應用、形態、作物類型、作用機制與銷售管道)特種肥料市場:2026-2032年全球市場預測(依產品形式、作物類型、養分類型、施用方法、通路和最終用途分類) 特種肥料市場規模、佔有率和趨勢分析報告:按技術、作物、類型、應用、地區和細分市場預測(2026-2033 年)特種肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

特種肥料市場規模、佔有率和趨勢分析報告:按技術、作物、類型、應用、地區和細分市場預測(2026-2033 年)特種肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球特種肥料市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球特種肥料市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球特種肥料市場報告

2026年全球特種肥料市場報告