|

市場調查報告書

商品編碼

1940836

特種肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Specialty Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

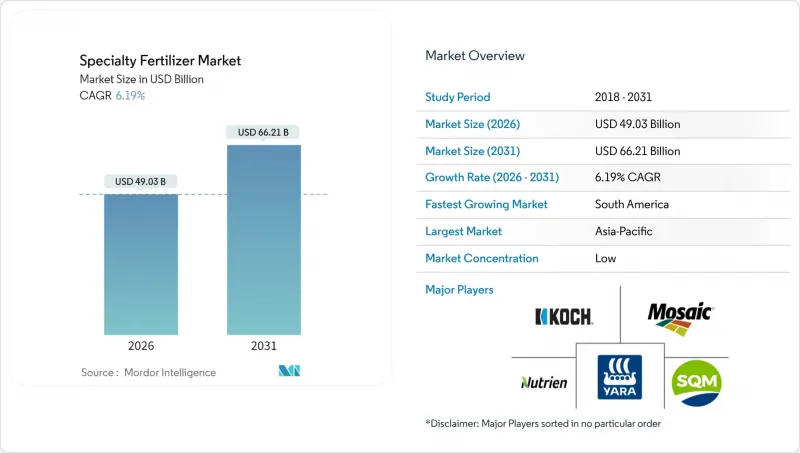

2025年特種肥料市場價值為461.7億美元,預計到2031年將達到662.1億美元,高於2026年的490.3億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 6.19%。

精密農業工具的普及應用正在推動市場成長,這主要得益於高效配方產品的快速發展以及將養分管理與環境指標掛鉤的政策支持。液態產品佔據主導地位,因為其完全溶解性符合灌溉施肥的需求,而緩釋包衣技術的進步則確保養分輸送與作物需求同步。數位化農業平台提供即時田間數據,從而提高養分利用效率,促進合規性,並實現排碳權貨幣化。推廣保護性耕作方式、提高滴灌技術的普及率以及為提高氮肥利用效率提供獎勵,將增強各類作物的需求韌性。日益激烈的市場競爭依賴於整合分析、硬體和客製化養分解決方案的綜合服務模式,從而提高特種肥料市場的農場盈利。

全球特種肥料市場趨勢與洞察

精密農業簡介

衛星影像、土壤感測器和GPS導航施肥機正在提高養分施用的精準度。 2024年,大多數玉米和大豆種植者採用了變數施肥技術,與2023年相比,每英畝特種肥料用量增加,同時減少了大面積施肥。即時氮肥額度允許在作物生長階段按需混合施肥,從而減少損失並提高產量。設備製造商目前正與養分供應商合作設計多倉施肥機,讓農民無需停機即可更換肥料配方。支援性的保護項目正在承擔部分硬體成本,加速了高效能精密農業產品的推廣應用。

水資源短缺與灌溉效率

與漫灌系統相比,滴灌和施肥相結合可顯著減少用水量,這在農業淡水資源佔有率日益減少的今天尤其重要。到2024年,全球滴灌管網的面積不斷擴大,透過這些管網施用特殊肥料的量是傳統田間施肥方式的兩倍。以色列和約旦強制規定10公頃以上的新農場必須採用壓力灌溉,從而鎖定了對完全水溶性營養混合物的需求。因此,必須使用不易堵塞、低鹽指數的線上pH值和電導率探頭。與用水目標掛鉤的補貼計畫鼓勵施肥灌溉,從而促進了特種肥料市場的成長。

原物料和能源價格波動

2024年,地緣政治緊張局勢導致天然氣、鉀肥和磷礦石價格波動,對生產商的利潤率帶來壓力。聚合物塗層佔複合樹脂(CRF)成本的25%之多,其價格與原油價格掛鉤,因此原油價格上漲會直接導致產品價格上漲。俄羅斯和白俄羅斯鉀肥供應中斷導致現貨價格暫時上漲50%,促使企業尋找替代貨源。依賴單一供應商供應特殊添加劑會加劇風險,而外匯波動則進一步增加了依賴進口製造商的不確定性。採購週期短,幾乎沒有避險的空間,因此難以維持價格穩定。

細分市場分析

預計到2025年,液體肥料將佔據特種肥料市場53.38%的佔有率。這一地位主要得益於其與肥料灌溉(混施)無與倫比的兼容性以及均勻的養分分佈。液體肥料溶解迅速、易於混合,使其適用於需要精確均質性的變數施肥系統。亞太和南美洲大規模灌溉農田的普及將使液體肥料的消費量保持在高位,而室內種植因其鹽分積累風險低而備受青睞。不斷完善的分銷基礎設施,使得散裝運輸和農場現場混施成為可能,也促進了這一領域的成長。

預計緩釋特種肥料市場將以7.81%的複合年成長率成長,成為所有特種肥料類型中成長最快的。包膜技術的進步使得養分釋放曲線能夠與植物吸收相匹配,從而減少徑流和人工需求。聚合物硫基產品在缺硫地區越來越受歡迎,而可生物分解薄膜則有助於應對即將訂定的微塑膠法規。精密農業工具能提升價值,並支持單次施肥即可滿足作物多個生長階段的需求,進而提高投資報酬率。

特種肥料市場按特種肥料類型(控釋肥、液體肥料、緩釋肥、水溶性肥料)、施用方法(滴灌施肥、葉面噴布、土壤施用)、作物類型(田間作物、園藝作物、草坪和觀賞植物)以及地區(亞太地區、歐洲、中東和非洲、北美、南美)進行細分。市場預測以價值(美元)和銷售量(公噸)為單位。

區域分析

到2025年,亞太地區將佔全球收入的65.20%,這主要得益於中國的土壤檢測補貼和印度針對小規模農戶的專項養分激勵措施。日本和韓國的集約化土地利用推高了每公頃的投入,而澳洲的乾旱管理法規則則鼓勵使用液態混合肥料的灌溉系統。東南亞的棕櫚油和米生產商正在採用高效投入品以滿足永續性認證的要求,這進一步推動了產量成長。

南美洲將成為成長最快的地區,到2031年複合年成長率將達到8.55%。巴西已開始投資精密農業技術以提高養分利用效率,大型農場將控制釋放肥料(CRF)的使用與犁地技術結合,以保護土壤健康。阿根廷也朝著類似的方向發展,利用控釋肥料種植大豆和玉米,以在日益嚴格的環境監管下保持出口競爭力。

南美洲特種肥料市場的特徵是規模化農業生產和現代農業技術的擴張。該地區以巴西和阿根廷為首,擁有廣闊的農地和豐富的作物種類,因此蘊藏著巨大的市場潛力。巴西憑藉其龐大的農業規模和對農業創新的高度重視,已成為該地區最大的市場。阿根廷則憑藉精密農業技術的推廣和對出口導向農業的重視,成為成長最快的市場。該地區市場的特點是人們對永續農業實踐的認知不斷提高,對農業技術的投資也不斷增加。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章 報告

第3章執行摘要和主要發現

第4章 主要產業趨勢

- 主要農作物種植面積

- 田間作物

- 園藝作物

- 平均施肥量

- 微量營養素

- 田間作物

- 園藝作物

- 宏量營養素

- 田間作物

- 園藝作物

- 次要必需營養素

- 田間作物

- 園藝作物

- 微量營養素

- 具有灌溉設施的農田

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 精密農業簡介

- 水資源短缺與灌溉效率

- 溫室和垂直農業的擴張

- NUE投入的排碳權獎勵

- 利用 CRISPR 技術培育營養作物

- 透過數位化可追溯性實現高階化

- 市場限制

- 原物料和能源價格波動

- 化學肥料灌溉設備的高額資本投資成本

- 禁止微塑膠塗層的趨勢

- 碳計量數據標準存在差距

第5章 市場規模及成長預測(數量與價值)

- 專業類型

- 控釋肥料(CRF)

- 聚合物塗層

- 聚合物和硫塗層

- 其他

- 液體肥料

- 緩效性肥料(SRF)

- 水溶性

- 控釋肥料(CRF)

- 應用模式

- 施肥灌溉

- 葉面噴布

- 土壤

- 作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

- 地區

- 亞太地區

- 澳洲

- 孟加拉

- 中國

- 印度

- 印尼

- 日本

- 巴基斯坦

- 菲律賓

- 泰國

- 越南

- 亞太其他地區

- 歐洲

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 烏克蘭

- 英國

- 其他歐洲地區

- 中東和非洲

- 奈及利亞

- 沙烏地阿拉伯

- 南非

- 土耳其

- 其他中東和非洲地區

- 北美洲

- 加拿大

- 墨西哥

- 美國

- 北美其他地區

- 南美洲

- 阿根廷

- 巴西

- 南美洲其他地區

- 亞太地區

第6章 競爭情勢

- 關鍵策略舉措

- 市佔率分析

- 公司簡介

- 公司簡介

- Coromandel International Limited

- EuroChem Group AG

- COMPO EXPERT GmbH

- Haifa Group

- Kingenta Ecological Engineering Group Co., Ltd.

- Koch Fertilizer LLC

- Nutrien Ltd.

- Sociedad Quimica y Minera de Chile SA

- The Mosaic Company

- Yara International ASA

- ICL Group Ltd.

- K+S Aktiengesellschaft

- Indian Farmers Fertiliser Cooperative Ltd.

- Omex Agriculture Ltd.

- Agro-Culture Liquid Fertilizers LLC

第7章:CEO們需要思考的關鍵策略問題

The specialty fertilizers market was valued at USD 46.17 billion in 2025 and estimated to grow from USD 49.03 billion in 2026 to reach USD 66.21 billion by 2031, at a CAGR of 6.19% during the forecast period (2026-2031).

The adoption of precision farming tools propels market growth, driven by the rapid shift toward enhanced-efficiency formulations and policy support that links nutrient management with environmental metrics. Liquid products dominate because their full solubility matches fertigation needs, while technology improvements in controlled-release coatings keep nutrient availability synchronized with crop demand. Digital agriculture platforms provide real-time field data that enhances nutrient use efficiency, promotes regulatory compliance, and facilitates carbon-credit monetization. Expanding protected cultivation, increasing drip irrigation coverage, and offering incentives for nitrogen use efficiency enhance demand resiliency across crop categories. Competitive intensity hinges on integrated service models that bundle analytics, hardware, and tailored nutrient solutions to raise farm profitability in the specialty fertilizers market.

Global Specialty Fertilizer Market Trends and Insights

Precision-Agriculture Adoption

Satellite imagery, soil sensors, and GPS-guided spreaders are enhancing the accuracy of nutrient placement. In 2024, the majority of corn and soybean growers adopted variable-rate application, compared to 2023, and specialty fertilizer use per acre increased as the broadcast practice declined. Real-time nitrogen crediting triggers on-demand blended inputs that match crop stages, cutting losses and bolstering yields. Equipment firms now co-design multi-bin applicators with nutrient suppliers, letting farmers switch formulations without downtime. Supportive conservation programs cover part of the hardware cost, thereby accelerating the penetration of precision-ready, enhanced-efficiency products.

Water Scarcity and Irrigation Efficiency

Drip irrigation, paired with fertigation, reduces water use compared to flood systems, a critical benefit as agriculture's share of freshwater resources contracts. Global acreage under drip lines reached a higher level in 2024, and specialty fertilizer volumes through these networks doubled those of conventional field methods. Israel and Jordan mandate pressurized irrigation for new farms larger than 10 ha, creating locked-in demand for fully soluble nutrient blends. Online pH and conductivity probes require low-salt index products that remain clog-free. Subsidies linked to water use targets favor fertigation and support the growth of the specialty fertilizers market.

Raw-Material and Energy Price Volatility

Natural gas, potash, and phosphate rock prices fluctuated in 2024 amid geopolitical tensions, compressing producer margins. Polymer coatings, which account for up to 25% of CRF costs, track crude oil, so oil spikes translate quickly into higher finished product prices. Potash supply disruptions from Russia and Belarus led to spot costs increasing by 50% at times, prompting alternative sourcing. Single-supplier dependence for specialty additives magnifies risk, and currency shifts add further uncertainty for import-reliant manufacturers. Short procurement cycles leave little room for hedging, making price stability elusive.

Other drivers and restraints analyzed in the detailed report include:

- Greenhouse and Vertical-Farm Expansion

- Digital Traceability Premiums

- Emerging Micro-Plastic Coating Bans

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid fertilizers accounted for 53.38% of the specialty fertilizers market share in 2025, a position built on their unmatched compatibility with fertigation and uniform nutrient distribution. Their rapid dissolution and ease of blending suit variable-rate rigs that demand precise homogeneity. Adoption of large irrigated acreage across the Asia Pacific and South America keeps volumes high, while indoor farming values its low salt risk. The segment also benefits from an expanded distribution infrastructure that supports bulk shipments and on-farm blending.

The specialty fertilizers market size for controlled-release products is projected to expand at a 7.81% CAGR, the fastest among specialty types. Coating advances offer predictable nutrient release curves that align with crop uptake, thereby curbing leaching and reducing labor requirements. Polymer-sulfur variants gain traction in sulfur-deficient regions, and biodegradable films help satisfy looming microplastic laws. Precision agriculture tools amplify value, as one application now feeds a crop across multiple growth stages, improving return on investment.

The Specialty Fertilizer Market is Segmented by Specialty Type (CRF, Liquid Fertilizer, SRF, Water Soluble), by Application Mode (Fertigation, Foliar, Soil), by Crop Type (Field Crops, Horticultural Crops, Turf and Ornamental), and by Region (Asia-Pacific, Europe, Middle East and Africa, North America, and South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Geography Analysis

Asia Pacific commanded 65.20% of global revenue in 2025, supported by China's soil testing subsidies and India's specialty nutrient incentives for smallholders. Intensive land use in Japan and South Korea further propels per-hectare spending, while Australia's drought management rules promote the use of fertigation systems with liquid blends. Southeast Asian palm and rice producers adopt enhanced-efficiency inputs to comply with sustainability certifications, adding incremental volume.

South America represents the fastest-growing region with an 8.55% CAGR to 2031. Brazil has initiated investments in precision agriculture technologies that enhance nutrient efficiency, and large farms are aligning CRF usage with no-till practices to safeguard soil health. Argentina mirrors this trajectory, utilizing controlled-release solutions for soy and corn to maintain export competitiveness amid growing environmental scrutiny.

The South American specialty fertilizer market is characterized by large-scale agricultural operations and growing adoption of modern farming practices. The region, primarily represented by Brazil and Argentina, shows significant market potential driven by extensive agricultural lands and diverse crop portfolios. Brazil emerges as the largest market in the region, supported by its vast agricultural operations and strong focus on technological advancement in farming. Argentina stands as the fastest-growing market, driven by increasing adoption of precision farming techniques and a focus on export-oriented agriculture. The region's market is characterized by growing awareness about sustainable farming practices and increasing investments in agricultural technology.

- Coromandel International Limited

- EuroChem Group AG

- COMPO EXPERT GmbH

- Haifa Group

- Kingenta Ecological Engineering Group Co., Ltd.

- Koch Fertilizer LLC

- Nutrien Ltd.

- Sociedad Quimica y Minera de Chile S.A.

- The Mosaic Company

- Yara International ASA

- ICL Group Ltd.

- K+S Aktiengesellschaft

- Indian Farmers Fertiliser Cooperative Ltd.

- Omex Agriculture Ltd.

- Agro-Culture Liquid Fertilizers LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped for Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Precision-agriculture adoption

- 4.6.2 Water scarcity and irrigation efficiency

- 4.6.3 Greenhouse and vertical-farm expansion

- 4.6.4 Carbon-credit incentives for NUE inputs

- 4.6.5 CRISPR-enabled nutrient-dense crops

- 4.6.6 Digital traceability premiums

- 4.7 Market Restraints

- 4.7.1 Raw-material and energy price volatility

- 4.7.2 High capex of fertigation hardware

- 4.7.3 Emerging micro-plastic coating bans

- 4.7.4 Data-standard gaps for carbon accounting

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Specialty Type

- 5.1.1 Controlled-Release Fertilizer (CRF)

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 Slow-Release Fertilizer (SRF)

- 5.1.4 Water-Soluble

- 5.1.1 Controlled-Release Fertilizer (CRF)

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

- 5.4 Region

- 5.4.1 Asia-Pacific

- 5.4.1.1 Australia

- 5.4.1.2 Bangladesh

- 5.4.1.3 China

- 5.4.1.4 India

- 5.4.1.5 Indonesia

- 5.4.1.6 Japan

- 5.4.1.7 Pakistan

- 5.4.1.8 Philippines

- 5.4.1.9 Thailand

- 5.4.1.10 Vietnam

- 5.4.1.11 Rest of Asia-Pacific

- 5.4.2 Europe

- 5.4.2.1 France

- 5.4.2.2 Germany

- 5.4.2.3 Italy

- 5.4.2.4 Netherlands

- 5.4.2.5 Russia

- 5.4.2.6 Spain

- 5.4.2.7 Ukraine

- 5.4.2.8 United Kingdom

- 5.4.2.9 Rest of Europe

- 5.4.3 Middle East and Africa

- 5.4.3.1 Nigeria

- 5.4.3.2 Saudi Arabia

- 5.4.3.3 South Africa

- 5.4.3.4 Turkey

- 5.4.3.5 Rest of Middle East and Africa

- 5.4.4 North America

- 5.4.4.1 Canada

- 5.4.4.2 Mexico

- 5.4.4.3 United States

- 5.4.4.4 Rest of North America

- 5.4.5 South America

- 5.4.5.1 Argentina

- 5.4.5.2 Brazil

- 5.4.5.3 Rest of South America

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Coromandel International Limited

- 6.4.2 EuroChem Group AG

- 6.4.3 COMPO EXPERT GmbH

- 6.4.4 Haifa Group

- 6.4.5 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.6 Koch Fertilizer LLC

- 6.4.7 Nutrien Ltd.

- 6.4.8 Sociedad Quimica y Minera de Chile S.A.

- 6.4.9 The Mosaic Company

- 6.4.10 Yara International ASA

- 6.4.11 ICL Group Ltd.

- 6.4.12 K+S Aktiengesellschaft

- 6.4.13 Indian Farmers Fertiliser Cooperative Ltd.

- 6.4.14 Omex Agriculture Ltd.

- 6.4.15 Agro-Culture Liquid Fertilizers LLC

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

亞太地區特種肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

亞太地區特種肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 特種肥料市場-全球產業規模、佔有率、趨勢、機會和預測:按作物類型、形態、應用方法、技術、地區和競爭格局分類,2021-2031年

特種肥料市場-全球產業規模、佔有率、趨勢、機會和預測:按作物類型、形態、應用方法、技術、地區和競爭格局分類,2021-2031年 晶體肥料市場:2026-2032年全球市場預測(依養分類型、應用、形態、作物類型、作用機制與銷售管道)特種肥料市場:2026-2032年全球市場預測(依產品形式、作物類型、養分類型、施用方法、通路和最終用途分類)

晶體肥料市場:2026-2032年全球市場預測(依養分類型、應用、形態、作物類型、作用機制與銷售管道)特種肥料市場:2026-2032年全球市場預測(依產品形式、作物類型、養分類型、施用方法、通路和最終用途分類) 特種肥料市場規模、佔有率和趨勢分析報告:按技術、作物、類型、應用、地區和細分市場預測(2026-2033 年)

特種肥料市場規模、佔有率和趨勢分析報告:按技術、作物、類型、應用、地區和細分市場預測(2026-2033 年) 全球特種肥料市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球特種肥料市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球特種肥料市場報告

2026年全球特種肥料市場報告 特種肥料市場規模、佔有率和成長分析(按類型、技術、形態、作物類型、應用方法和地區分類)-2026-2033年產業預測全球特種肥料市場規模(依特種肥料類型、作物類型、施用方法、區域範圍及預測)中國特種肥料市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)

特種肥料市場規模、佔有率和成長分析(按類型、技術、形態、作物類型、應用方法和地區分類)-2026-2033年產業預測全球特種肥料市場規模(依特種肥料類型、作物類型、施用方法、區域範圍及預測)中國特種肥料市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)