|

市場調查報告書

商品編碼

2073601

越南特種肥料市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Vietnam Specialty Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

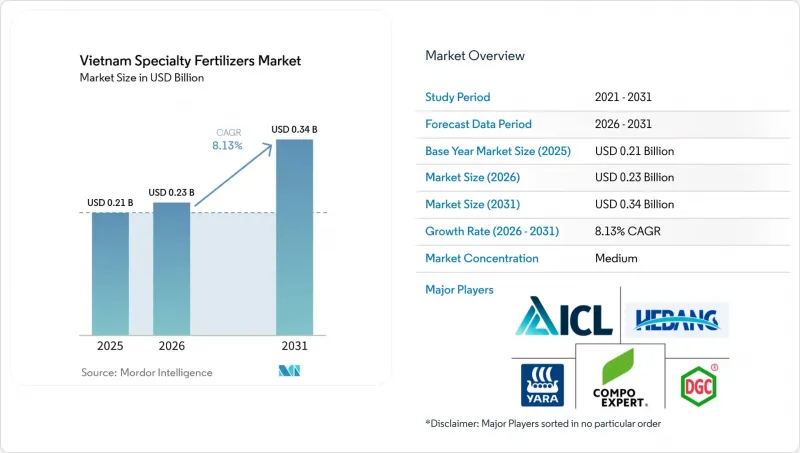

據 Mordor Intelligence 稱,越南特種肥料市場在 2025 年的價值為 2.1 億美元,預計到 2031 年將達到 3.4 億美元,而 2026 年為 2.3 億美元,預測期(2026-2031 年)的複合年成長率為 8.13%。

本報告依特殊肥料類型(控釋肥、液體肥料、緩釋肥、水溶性肥料)、施用方法(灌溉施肥、葉面噴布、土壤施用)和作物類型(田間作物、園藝作物、草坪和觀賞作物)進行分類。市場預測以價值(美元)和數量(公噸)兩種單位呈現。

越南特種肥料市場趨勢及洞察

精密農業的引進正在推動對更高效投入材料的需求。

2024年,無人機施肥技術應用於5萬公頃稻田,透過利用數位土壤圖進行可變施肥,將養分成本降低了高達25%。這種特殊的液體肥料能夠均勻溶解,避免料斗堵塞,從而克服了無人機先前只能使用低粉塵肥料的限制。雅苒國際與百事可樂合作,在2024年於一個1200公頃的合約馬鈴薯農場實現了增產15%,氮肥流失減少30%。政府計劃在2030年將100萬公頃稻田改造為“乾濕交替灌溉”,該系統需要使用與灌溉計劃相匹配的緩釋氮肥。土壤測繪計畫已涵蓋250萬公頃土地,為農業相關企業提供養分缺乏數據,以支持高品質複合肥料的有效性評估。由於大多數農場的面積不足一公頃,而且資本密集技術的引進依賴於合作模式,因此預計其採用將逐步擴大。

政府降低增值稅(VAT)提高了國內生產商的利潤率。

自2025年7月起,原先10%的增值稅將降至5%,進口在接收成本方面的優勢將縮小約5個百分點,從而使當地企業能夠將投資重點放在專業領域。儘管國內化肥產能約為800萬噸,但需求量超過1,100萬噸,因此預計進口仍將持續,但國內生產商現在擁有更大的定價空間。越南石油集團金甌公司已將2025年資本投資的15%分配給聚合物包膜複合肥,利用其80萬噸尿素生產基地向上游價值鏈發展。經營團隊預計到2027年,特種產品產量將成長10-15%。短期計劃反映了稅收負擔的即時減輕,但新生產線的設計和試運行將需要長達兩年的時間。

天然氣原料成本波動劇烈

氨價從2022年的每噸700美元以上跌至2024年的每噸300-400美元,凸顯了尿素利潤率對全球天然氣價格波動的敏感度。越南石油集團(PetroVietnam)旗下的金甌公司(Ca Mau)依賴海上天然氣田,但自2020年以來,其產量每年下降3-5%,迫使其依賴補充進口。當原物料成本飆升時,生產商不願投資升級生產特殊產品的設備,因為如果無法將價格上漲轉嫁給注重成本的農民,這些產品可能會變得無利可圖。來自中國的進口價格徘徊在每噸314美元左右,這構成了一個價格上限,國內供應商應密切注意。短期時間線凸顯了價格衝擊帶來的迫在眉睫的壓力,但可以透過避險和調整產品組合來減輕影響。

細分市場分析

到2025年,液態肥料將佔越南高性能肥料市場49.2%的佔有率。這主要得益於溫室蔬菜種植,溫室蔬菜種植透過灌溉施肥,將養分濃度提高到150-200ppm。大叻的水耕種植者供應了大部分高級沙拉綠葉,他們表示水耕顯著節約了用水。因此,液態肥料已成為一種標準的施肥方法。由於低溫運輸基礎設施有限,液態肥料在都市區的銷售受到限制。平田公司即將推出的水溶性顆粒肥料可在室溫下儲存,將作為咖啡和胡椒種植園的替代方案。

預計2026年至2031年間,緩釋肥料的複合年成長率將達4.3%。越南石油集團金甌公司利用其剩餘尿素,開發出了可延長氮肥釋放的聚合物包膜產品,這些產品適用於咖啡和火龍果的生長週期。生物炭和聚氨酯包膜可減少養分流失,並符合日益嚴格的有機質含量標準。水溶性緩釋肥料的市佔率落後於液體肥料,但在咖啡和辣椒種植園中,由於滴灌系統能夠大幅減少人工成本,水溶性緩釋肥料正逐漸獲得市場認可。由於暴雨可能導致養分釋放不均勻,硫包膜緩釋顆粒肥料的推廣速度相對較慢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 主要農作物種植面積

- 大田作物

- 園藝作物

- 平均施肥量

- 微量營養素

- 田間作物

- 園藝作物

- 主要營養素

- 田間作物

- 園藝作物

- 次要營養元素

- 田間作物

- 園藝作物

- 微量營養素

- 配備灌溉設施的農田

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 精密農業的引進增加了對高效投入材料的需求。

- 政府將增值稅調整為 5%,提高了國內生產商的利潤率。

- 擴大高附加價值農產品出口

- 溫室蔬菜種植面積迅速擴大

- 過剩的尿素產能將使推出包膜尿素增值生產線成為可能。

- 從荷蘭進口的堆肥顆粒正在加速有機混合物的推廣。

- 市場限制因素

- 天然氣原料成本波動

- 農民對優質投入材料的價格敏感度

- 假冒仿冒品產品的氾濫

- 微生物和液體特種產品低溫運輸短缺

第5章 市場規模與成長預測

- 依產品類型

- CRF

- 聚合物塗層

- 聚合物硫塗層

- 其他

- 液體肥料

- SRF

- 水溶性

- CRF

- 透過應用方法

- 施肥和灌溉

- 葉面噴布

- 土壤

- 按作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介

- PVFCCo(PetroVietnam-越南石油天然氣集團)

- PetroVietnam Ca Mau Fertilizer-DCM

- Baconco(Hebang Biotechnology Co. Ltd.)

- Binh Dien Fertilizer

- Yara International ASA

- Duc Giang Chemicals Group

- Kingenta Ecological Engineering

- Vietnam National Chemical Group

- Song Gianh Corporation

- Grupa Azoty SA(Compo Expert)

- Haifa Group

- Nutrien Ltd.

- ICL Group Ltd.

- Hebei Sanyuanjiuqi Fertilizer Co. Ltd.

第7章 化肥產業執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the vietnam specialty fertilizers market size was valued at USD 0.21 billion in 2025 and estimated to grow from USD 0.23 billion in 2026 to reach USD 0.34 billion by 2031, at a CAGR of 8.13% during the forecast period (2026-2031).

This report is Segmented by Specialty Type (CRF, Liquid Fertilizer, SRF, and Water-Soluble), Application Mode (Fertigation, Foliar, and Soil) and Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Vietnam Specialty Fertilizers Market Trends and Insights

Precision-Farming Adoption Boosts Demand for Efficient Inputs

Drone application covered 50,000 hectares of rice in 2024, reducing nutrient costs by up to 25% through variable-rate dosing that relies on digital soil maps. Specialty liquids dissolve evenly and avoid the hopper clogging that restricts drones to low-dust materials. Yara International partnered with PepsiCo on 1,200 hectares of contract potato farms, raising yields 15% and cutting nitrogen runoff 30% in 2024. The government plans to shift 1 million hectares of rice to alternate wetting and drying irrigation by 2030, a system that requires slow-release nitrogen to match water schedules. Soil-mapping programs already cover 2.5 million hectares, equipping agribusinesses with deficiency data that validate premium blends. Adoption will scale in phases because most farms remain below one hectare and depend on cooperative models for capital-intensive technology.

Government VAT Cut Improves Domestic Producer Margins

From July 2025, a 5% VAT replaced the prior 10% rate, shrinking the landed-cost advantage of imports by roughly five percentage points and freeing up local firms to pursue specialty investments. National fertilizer capacity stands near 8 million metric tons compared with demand above 11 million metric tons, so imports will still flow, yet domestic manufacturers now enjoy higher pricing headroom. PetroVietnam Ca Mau earmarked 15% of 2025 capital expenditure for polymer-coated NPK, leveraging its 800,000 metric tons urea base to climb the value chain. Management expects specialty output to rise 10-15% by 2027. The near-term timeline reflects immediate tax savings, while engineering and commissioning of new lines require up to two years.

Volatile Natural-Gas Feedstock Costs

Ammonia prices fell from over USD 700 per metric ton in 2022 to USD 300-400 per metric ton in 2024, underscoring the sensitivity of urea margins to global gas swings. PetroVietnam Ca Mau relies on offshore gas fields whose output has slipped 3-5% each year since 2020, forcing supplemental imports. When feedstock costs spike, producers hesitate to fund specialty upgrades that could turn uneconomic if pricing cannot be passed along to cost-conscious farmers. Imports priced near USD 314 per metric ton from China set a ceiling that domestic suppliers must watch. The short-term timeline highlights immediate pressure during price shocks, although hedging and product-mix shifts can soften the blow.

Other drivers and restraints analyzed in the detailed report include:

- High-Value Crop Export Expansion in Coffee and Pepper

- Rapid Growth of Greenhouse Vegetable Acreage

- Farmer Price Sensitivity Toward Premium Inputs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid fertilizers accounted for 49.2% of the Vietnam specialty fertilizers market share in 2025, anchored by greenhouse vegetables, where fertigation delivers nutrients at 150-200 parts per million. Hydroponic growers in Da Lat supply a large share of premium salad greens and report considerable water savings, cementing liquids as the default feed. Limited cold chain infrastructure narrows distribution outside urban zones. Binh Dien's upcoming launch of water-soluble granules offers an alternative that can be stored at ambient temperatures and targets coffee and pepper farms.

Controlled-release fertilizers are anticipated to grow at a CAGR of 4.3% from 2026 to 2031. PetroVietnam Ca Mau's surplus urea enables polymer-coated lines that extend nitrogen release, aligning with coffee and dragon-fruit cycles. Biochar-polyurethane coatings reduce leaching and meet rising organic content rules. Water-soluble products trail liquids in market share but are gaining traction across coffee and pepper farms, where drip systems significantly cut labor. Slow-release sulfur-coated granules grow more slowly because heavy rainfall can trigger uneven nutrient pulses.

Complete Report Scope:

- Speciality Type

- CRF

- Polymer Coated

- Polymer-Sulfur Coated

- Others

- Liquid Fertilizer

- SRF

- Water Soluble

- CRF

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

List of Companies Covered in this Report:

- PVFCCo (PetroVietnam - Vietnam Oil and Gas Group)

- PetroVietnam Ca Mau Fertilizer - DCM

- Baconco (Hebang Biotechnology Co. Ltd.)

- Binh Dien Fertilizer

- Yara International ASA

- Duc Giang Chemicals Group

- Kingenta Ecological Engineering

- Vietnam National Chemical Group

- Song Gianh Corporation

- Grupa Azoty S.A. (Compo Expert)

- Haifa Group

- Nutrien Ltd.

- ICL Group Ltd.

- Hebei Sanyuanjiuqi Fertilizer Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Precision-farming adoption boosts demand for efficient inputs

- 4.6.2 Government VAT change (5 %) improves domestic producer margins

- 4.6.3 High-value crop export expansion

- 4.6.4 Rapid growth of greenhouse vegetable acreage

- 4.6.5 Surplus urea capacity enables coated-urea value-added lines

- 4.6.6 Dutch manure-granulate imports accelerate organic blends

- 4.7 Market Restraints

- 4.7.1 Volatile natural-gas feedstock costs

- 4.7.2 Farmer price-sensitivity toward premium inputs

- 4.7.3 Proliferation of counterfeit / sub-standard products

- 4.7.4 Limited cold-chain for microbial and liquid specialties

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Speciality Type

- 5.1.1 CRF

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 SRF

- 5.1.4 Water Soluble

- 5.1.1 CRF

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 PVFCCo (PetroVietnam - Vietnam Oil and Gas Group)

- 6.4.2 PetroVietnam Ca Mau Fertilizer - DCM

- 6.4.3 Baconco (Hebang Biotechnology Co. Ltd.)

- 6.4.4 Binh Dien Fertilizer

- 6.4.5 Yara International ASA

- 6.4.6 Duc Giang Chemicals Group

- 6.4.7 Kingenta Ecological Engineering

- 6.4.8 Vietnam National Chemical Group

- 6.4.9 Song Gianh Corporation

- 6.4.10 Grupa Azoty S.A. (Compo Expert)

- 6.4.11 Haifa Group

- 6.4.12 Nutrien Ltd.

- 6.4.13 ICL Group Ltd.

- 6.4.14 Hebei Sanyuanjiuqi Fertilizer Co. Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

美國特種肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)南美洲特種肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區特種肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

美國特種肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)南美洲特種肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區特種肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 特種肥料市場-全球產業規模、佔有率、趨勢、機會和預測:按作物類型、形態、應用方法、技術、地區和競爭格局分類,2021-2031年

特種肥料市場-全球產業規模、佔有率、趨勢、機會和預測:按作物類型、形態、應用方法、技術、地區和競爭格局分類,2021-2031年 晶體肥料市場:2026-2032年全球市場預測(依養分類型、應用、形態、作物類型、作用機制與銷售管道)特種肥料市場:2026-2032年全球市場預測(依產品形式、作物類型、養分類型、施用方法、通路和最終用途分類)

晶體肥料市場:2026-2032年全球市場預測(依養分類型、應用、形態、作物類型、作用機制與銷售管道)特種肥料市場:2026-2032年全球市場預測(依產品形式、作物類型、養分類型、施用方法、通路和最終用途分類) 特種肥料市場規模、佔有率和趨勢分析報告:按技術、作物、類型、應用、地區和細分市場預測(2026-2033 年)特種肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

特種肥料市場規模、佔有率和趨勢分析報告:按技術、作物、類型、應用、地區和細分市場預測(2026-2033 年)特種肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球特種肥料市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球特種肥料市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球特種肥料市場報告

2026年全球特種肥料市場報告