|

市場調查報告書

商品編碼

2073305

招募行銷平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Recruitment Marketing Platform Market - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

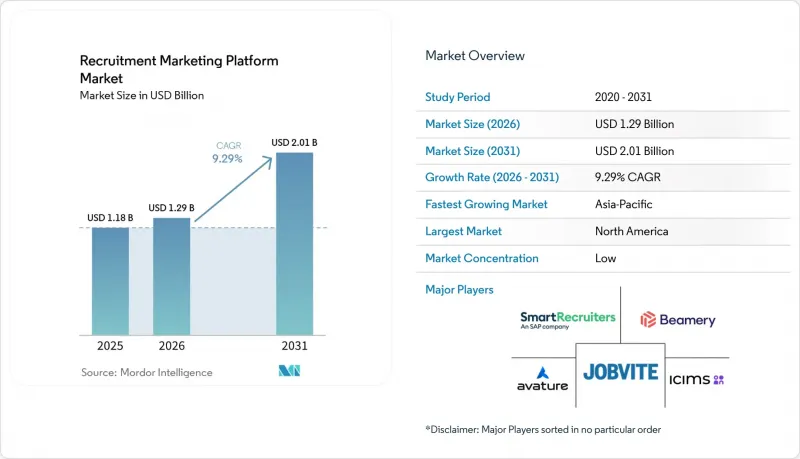

根據 Mordor Intelligence 預測,招募和行銷平台市場規模將從 2025 年的 11.8 億美元和 2026 年的 12.9 億美元成長到 2031 年的 20.1 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 9.29%。

本報告按元件(軟體/平台、服務)、部署類型(雲端、本地部署)、組織規模(大型企業、中小企業)、最終用戶產業(IT與電信、銀行、金融服務和保險、製造業等)、功能(候選人關係管理等)和地區進行細分。市場預測以美元計價。

全球招募行銷平台市場趨勢及洞察

擴大程序化招募廣告的應用範圍

在招募行銷平台市場,程序化招募廣告正從專業化的工作流程轉向更標準化的購買模式。雇主們正利用這個模式即時調整跨通路的支出,而非依賴對固定招聘網站的投放。這種轉變意義重大,因為隨著宣傳活動歷史的積累,以及競標和轉換數據在反覆招募週期中效用的提升,系統的價值也在不斷成長。這種回饋循環使得演算法媒體購買超越了人工發布方式,尤其是在雇主持續招募多種職位類型的情況下。這項變化的快速程度體現在程序化招募廣告已成為招募行銷平台市場中成長最快的功能性細分領域,預計到2031年,其複合年成長率將達到12.48%。

擴大人工智慧驅動的候選人關係管理的應用

人工智慧主導的候選人關係管理 (CRM) 在招募行銷平台市場中扮演著越來越重要的角色,尤其是在招募週期之外的招募活動中。雇主越來越需要能夠維護優質人才庫、個人化招募策略並引導負責人找到高潛力候選人的平台。這使得 CRM 從被動的聯絡人資料庫轉變為人才發現、重新互動和宣傳活動時機把控的主動營運層。隨著買家期望在人工智慧驅動的招募工作流程中實現人工監督、文件記錄和可審計性,管治的重要性也日益凸顯。因此,招募行銷平台市場更青睞那些將自動化與管理功能結合的供應商,而不是那些僅僅添加人工智慧工具而缺乏清晰合規框架的供應商。

與傳統 ATS 和 HRIS 系統整合的複雜性。

與傳統人力資源系統的整合仍然是招聘行銷平台市場擴張面臨的最明顯限制之一。 Remote發布的2025年報告顯示,51%的人力資源主管正在尋找新的人力資源資訊系統(HRIS),36%的主管正在考慮徹底更換系統。這凸顯了企業對碎片化系統環境的普遍不滿。該報告還指出,一次因整合失敗導致的違規就可能造成高達4.2萬美元的損失,顯示技術缺陷對買家而言構成直接的財務風險。因此,那些將與主流招募管理系統(ATS)和人力資本管理(HCM)系統的連接器作為標準配置的供應商,在企業評估中佔據了更有利的地位。在招募行銷平台市場,廣泛原生整合的支援不僅是一項功能優勢,而且正逐漸成為一項必備的購買條件。

細分市場分析

到2025年,軟體/平台授權收入將佔總收入的78.46%,成為招募行銷平台市場最大的收入來源。這一比例反映了SaaS訂閱模式在大中型企業負責人的技術格局中滲透的深度。軟體層仍然是大多數採購決策的基礎,因為雇主需要在單一作業系統內實現宣傳活動管理、工作流程控制和候選人互動。然而,服務業的成長速度更快,預計到2031年將以10.84%的複合年成長率成長。這表明,招聘行銷平台市場正邁向一個僅靠許可證已無法保證成功應用的階段。

服務業的加速成長源於企業在初始軟體購買後對實施支援、系統整合、報告設計和管理分析支援的需求日益成長。這一趨勢表明,隨著招募行銷平台與不同地區和業務部門的ATS、HRIS、分析和媒體系統整合,該行業的營運複雜性正在增加。這也表明,平台價值的評估不僅取決於功能的廣度,還取決於可衡量的使用和性能。同時,基本的交付和互動功能越來越容易整合到更廣泛的HCM套件中,這縮小了中型純軟體供應商的市場範圍。根據SHRM預測,到2025年,人力資源技術支出將同比成長9.1%,但這些支出越來越依賴能夠證明「從尋源到招聘」全程投資回報率的工具,這為招聘行銷平台市場服務行業的良好前景提供了支撐。

到2025年,基於雲端的招募行銷平台市佔率將達到71.18%,成為所有買家群體的主導交付模式。此外,預計到2031年,其複合年成長率將達到10.21%,主要得益於新增用戶仍將採用雲端平台。雲端平台的優勢在於其實用性:雲端架構能夠加速產品更新、簡化合規流程,並擴大跨客戶的整合維護範圍。這些優勢在需要頻繁調整人工智慧模型、通路連接器和宣傳活動工具的情況下尤其重要。因此,招募行銷平台市場持續整合,主要以多租戶SaaS模式為中心。

在政府、國防和某些金融服務等高度監管的產業中,對本地部署解決方案的需求仍然強勁。在這些產業中,基礎設施管理和資料儲存位置持續影響採購決策。另一個顯著的變化是,大型機構擴大使用私有雲端和混合模式,以尋求更大的控制權,同時避免完全本地部署解決方案的成本和維護負擔。這種柔軟性至關重要,因為一些大型企業正在重新評估系統結構,不僅包括部署類型,還包括整合品質、管治和資料流。 Remote 的一項調查發現,到 2025 年,影響人力資源資訊系統 (HRIS) 更換決策的主要促進因素將是系統整合。這印證了雲選擇如今與生態系相容性密切相關的觀點。在招募行銷平台市場,能夠提供與傳統和現代人力資源系統可靠整合並支援雲端主導部署的供應商,在抓住系統更換機會方面佔據優勢。

區域分析

2025年,北美持續保持領先地位,佔據招聘行銷平台市場佔有率的38.64%。這項領先優勢歸功於成熟的人力資源技術、強大的企業採購能力以及完善的招募軟體生態系統。根據美國人力資源管理協會(SHRM)的數據顯示,2025年人力資源預算年增9.1%,人力資源支出佔營運支出的中位數為2.4%。這表明,儘管普遍採取了成本削減措施,但企業在招募技術方面的支出仍然強勁。美國仍然是核心市場,加拿大也呈現類似的採購模式,而墨西哥仍處於技術應用的早期階段。在整個招聘行銷平台市場中,北美地區也因其積極大規模的行業重組而脫穎而出,例如SAP收購SmartRecruiters以及Workday收購Paradox,這些事件改變了許多獨立供應商的競爭格局。

歐洲仍然是招募行銷平台市場的第二大區域市場,這主要得益於德國、英國和法國的企業需求。尤其值得一提的是德國,其嚴格的隱私和用戶同意要求通常被視為歐盟平台部署實質合規性的標竿。德國和北歐國家的企業負責人越來越傾向於將資訊安全認證視為一項基本採購要求,而非差異化因素。隨著雇主審查其現有系統在透明度、文件記錄和人工監督方面的要求,歐盟人工智慧法案可能會加速中期平台更新週期。

預計到2031年,亞太地區將以11.93%的複合年成長率成長,成為招募行銷平台市場成長最快的區域板塊。該地區受益於數位化招聘的快速普及、龐大的候選人庫以及印度和東南亞地區活躍的行動裝置使用。根據eRoad在2025年9月發布的報告,中國84.13%的受訪企業在招募活動中採用了人工智慧,顯示人工智慧驅動的招募工具已成為市場主流。中東地區也透過沙烏地阿拉伯和阿拉伯聯合大公國的在地化招聘計畫取得了進展,而非洲仍處於起步階段,南非和奈及利亞是採用率最高的國家。南美地區持續擴張,主要由巴西和阿根廷推動,在這些國家,本地語言支援和勞動力報告相容性是招募行銷平台市場的關鍵選擇標準。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 程序化招募廣告的普及應用日益廣泛

- 擴大人工智慧驅動的候選人關係管理的應用

- 擴大企業預算,用於打造雇主品牌

- 「行動優先」搜尋行為激增。

- 對數據驅動型招募指標的需求日益成長

- 加快遠距和混合辦公模式

- 市場限制因素

- 與傳統 ATS 和 HRIS 系統整合的複雜性。

- 資料隱私和合規性限制(GDPR、CCPA)

- 景氣衰退期間,中小企業面臨預算壓力

- 新興市場分析技術成熟度較低

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按組件

- 軟體/平台

- 服務

- 依部署類型

- 基於雲端的

- 現場

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 工業製造

- 醫療保健和生命科學

- 零售與電子商務

- 政府/公共部門

- 其他終端用戶產業

- 功能性別

- 候選人關係管理

- 職位分配和職位發布

- 招聘分析和報告撰寫

- 雇主品牌

- 程序化徵才廣告

- 其他函數類型

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Jobvite Inc.

- Avature Holding Corp.

- iCIMS Inc.

- Beamery Ltd.

- SmartRecruiters Inc.

- Phenom People Inc.

- Workable Technology Limited

- Zoho Corporation Pvt. Ltd.

- Symphony Talent LLC

- Sense Talent Labs Inc.

- Recruitee BV

- Hireology Inc.

- PageUp Pty Ltd

- Talenteria Inc.

- Jobilla Oy

- GR8 People Inc.

- Yello Inc.

- TalentLyft(Zero Molecule doo)

- Radancy

- SmartDreamers SRL

- Clinch Technology Ltd.

- Eightfold AI Inc.

- Breezy HR Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the recruitment marketing platform market size is projected to expand from USD 1.18 billion in 2025 and USD 1.29 billion in 2026 to USD 2.01 billion by 2031, registering a CAGR of 9.29% between 2026 and 2031.

This report is Segmented by Component (Software/Platform, and Services), Deployment Type (Cloud-Based, and On-Premises), Organization Size (Large Enterprise, and SMEs), End-User Industry (IT and Telecommunications, BFSI, Industrial Manufacturing, and More), Functionality (Candidate Relationship Management, and More ), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Recruitment Marketing Platform Market Trends and Insights

Growth In Programmatic Job Advertising Adoption

Programmatic job advertising is moving from a specialist workflow into a more standard buying layer within the recruitment marketing platform market. Employers are using it to shift spending across channels in real time instead of relying on fixed job board allocations. This change matters because the value of the system improves as campaign history builds and as bid and conversion data become more useful over repeated hiring cycles. That feedback loop is helping algorithmic media buying pull ahead of manual placement methods, especially where employers recruit continuously across many roles. The pace of that shift is reflected in programmatic job advertising being the fastest-growing functionality segment in the recruitment marketing platform market, with a projected 12.48% CAGR through 2031.

Increasing Use Of AI-Powered Candidate Relationship Management

AI-led candidate relationship management is becoming more central to how the recruitment marketing platform market supports hiring between active requisition cycles. Employers increasingly want platforms that can help them maintain warm talent pools, personalize outreach, and guide recruiters toward higher-probability candidates. This is changing CRM from a passive contact database into an active operating layer for sourcing, re-engagement, and campaign timing. It also raises the importance of governance, because buyers now expect human oversight, documentation, and auditability in AI-supported recruiting workflows. As a result, the recruitment marketing platform market is favoring vendors that combine automation with control features rather than vendors that add AI tools without a clear compliance structure.

Integration Complexity With Legacy ATS And HRIS

Integration with older HR systems remains one of the clearest limits on expansion in the recruitment marketing platform market. Remote reported in 2025 that 51% of HR leaders were searching for a new HRIS, and 36% were considering a full system switch, which points to broad dissatisfaction with fragmented system environments. The same report noted that a single compliance incident linked to integration failure could cost USD 42,000, which turns technical gaps into a direct financial risk for buyers. This is why vendors with pre-built connectors to major ATS and HCM systems enter enterprise evaluations from a stronger position. In the recruitment marketing platform market, broad native integration support is becoming a buying requirement rather than a feature advantage.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Employer-Branding Budgets Among Enterprises

- Surge In Mobile-First Job Search Behavior

- Data-Privacy And Compliance Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software/platform licenses accounted for 78.46% of revenue in 2025, giving them the largest revenue base in the recruitment marketing platform market. That weighting reflects how deeply SaaS subscriptions are embedded in hiring technology environments across large enterprise and mid-market buyers. The software layer still anchors most buying decisions because employers need campaign management, workflow control, and candidate engagement within a single operating system. Even so, the faster movement is occurring in services, which are forecast to expand at a 10.84% CAGR through 2031. This shows that the recruitment marketing platform market is moving into a phase where successful adoption depends on more than license access.

Services are growing faster because buyers increasingly need implementation help, integration work, reporting design, and managed analytics support after the initial software purchase. This pattern suggests that the recruitment marketing platform industry is becoming more operationally complex as platforms connect with ATS, HRIS, analytics, and media systems across different regions and business units. It also indicates that platform value is being judged on measurable usage and performance, not just on feature breadth. At the same time, basic distribution and engagement features are becoming easier for broader HCM suites to bundle, which narrows room for mid-tier software-only vendors. SHRM reported that HR technology spending rose 9.1% year over year in 2025, but that spending was increasingly tied to tools that could show return from source to hire, which supports the stronger services outlook in the recruitment marketing platform market.

Cloud-based deployment accounted for 71.18% of the recruitment marketing platform market size in 2025, making it the dominant delivery model across buyer groups. It is also forecast to grow at a 10.21% CAGR through 2031, which confirms that most new adoption is staying on the cloud path. The appeal is practical because cloud architectures support faster product updates, easier compliance changes, and broader integration maintenance across clients. These advantages are especially important where AI models, channel connectors, and campaign tools need frequent adjustment. For that reason, the recruitment marketing platform market is continuing to consolidate around multi-tenant SaaS models.

On-premises demand remains prevalent in regulated settings such as government, defense, and selected financial services environments, where infrastructure control and data residency continue to influence procurement decisions. A meaningful secondary shift is the rise of private cloud and hybrid models for large institutions that want more control without full on-premises cost and maintenance. That flexibility matters because some large employers are reevaluating system architecture through the lens of integration quality, governance, and data flow rather than deployment style alone. Remote found that unified system integration was the main driver of HRIS replacement decisions in 2025, which supports the view that cloud selection is now tied closely to ecosystem fit. In the recruitment marketing platform market, vendors that can support cloud-led deployment with reliable integration into legacy and modern HR systems are in a better position to capture replacement cycles.

Complete Report Scope:

- By Component

- Software/Platform

- Services

- By Deployment Type

- Cloud-based

- On-premises

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End-User Industry

- IT and Telecommunications

- BFSI

- Industrial Manufacturing

- Healthcare and Lifesciences

- Retail and E-commerce

- Government and Public Sector

- Other End-User Industries

- By Functionality

- Candidate Relationship Management

- Job Distribution and Posting

- Recruitment Analytics and Reporting

- Employer Branding

- Programmatic Job Advertising

- Other Functionality Types

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America held 38.64% of the recruitment marketing platform market share in 2025, which kept the region in the top position. That lead came from mature HR technology adoption, strong enterprise buying capacity, and a well-developed recruiting software ecosystem. SHRM reported that HR budgets rose 9.1% year over year in 2025 and that the median HR-expense-to-operating-expense ratio was 2.4%, which suggests that hiring technology spending remained protected despite broader cost discipline. The United States remained the core market, while Canada followed a similar enterprise-buying pattern, and Mexico remained earlier in its adoption curve. Across the recruitment marketing platform market, the region also stood out for major consolidation activity, including SAP's acquisition of SmartRecruiters and Workday's acquisition of Paradox, which changed the competitive landscape for many independent vendors.

Europe remained the second-largest regional market in the recruitment marketing platform market, supported by enterprise demand in Germany, the United Kingdom, and France. Germany carried particular weight because strict privacy and consent requirements there often functioned as a practical compliance benchmark for wider EU platform adoption. Enterprise buyers across Germany and the Nordics increasingly treated information security certification as a basic procurement requirement rather than as a differentiator. The EU AI Act is likely to drive a medium-term platform refresh cycle as employers review current systems for transparency, documentation, and human oversight needs.

Asia-Pacific is projected to grow at an 11.93% CAGR through 2031, making it the fastest-growing regional segment in the recruitment marketing platform market size. The region is gaining from rapid digital hiring adoption, large candidate pools, and strong mobile engagement behavior across India and Southeast Asia. In September 2025, eRoad reported that AI adoption in Chinese recruitment reached 84.13% of surveyed companies, pointing to a market where AI-enabled hiring tools are already mainstream. The Middle East is also advancing through localization-driven hiring programs in Saudi Arabia and the UAE, while Africa remains earlier stage with South Africa and Nigeria as the clearest adoption hubs. South America continues to build from Brazil and Argentina, where local language capability and labor reporting fit remain important selection criteria in the recruitment marketing platform market.

- Jobvite Inc.

- Avature Holding Corp.

- iCIMS Inc.

- Beamery Ltd.

- SmartRecruiters Inc.

- Phenom People Inc.

- Workable Technology Limited

- Zoho Corporation Pvt. Ltd.

- Symphony Talent LLC

- Sense Talent Labs Inc.

- Recruitee B.V.

- Hireology Inc.

- PageUp Pty Ltd

- Talenteria Inc.

- Jobilla Oy

- GR8 People Inc.

- Yello Inc.

- TalentLyft (Zero Molecule d.o.o.)

- Radancy

- SmartDreamers S.R.L.

- Clinch Technology Ltd.

- Eightfold AI Inc.

- Breezy HR Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Programmatic Job Advertising Adoption

- 4.2.2 Increasing Use of AI-Powered Candidate Relationship Management

- 4.2.3 Expansion of Employer-Branding Budgets Among Enterprises

- 4.2.4 Surge in Mobile-First Job Search Behaviour

- 4.2.5 Rising Demand for Data-Driven Recruiting Metrics

- 4.2.6 Acceleration of Remote and Hybrid Work Hiring Models

- 4.3 Market Restraints

- 4.3.1 Integration Complexity with Legacy ATS and HRIS

- 4.3.2 Data-Privacy and Compliance Constraints (GDPR, CCPA)

- 4.3.3 Budget Pressures in SME Segments During Economic Downturns

- 4.3.4 Limited Analytics Maturity in Emerging Markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software/Platform

- 5.1.2 Services

- 5.2 By Deployment Type

- 5.2.1 Cloud-based

- 5.2.2 On-premises

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Industrial Manufacturing

- 5.4.4 Healthcare and Lifesciences

- 5.4.5 Retail and E-commerce

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-User Industries

- 5.5 By Functionality

- 5.5.1 Candidate Relationship Management

- 5.5.2 Job Distribution and Posting

- 5.5.3 Recruitment Analytics and Reporting

- 5.5.4 Employer Branding

- 5.5.5 Programmatic Job Advertising

- 5.5.6 Other Functionality Types

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Egypt

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Jobvite Inc.

- 6.4.2 Avature Holding Corp.

- 6.4.3 iCIMS Inc.

- 6.4.4 Beamery Ltd.

- 6.4.5 SmartRecruiters Inc.

- 6.4.6 Phenom People Inc.

- 6.4.7 Workable Technology Limited

- 6.4.8 Zoho Corporation Pvt. Ltd.

- 6.4.9 Symphony Talent LLC

- 6.4.10 Sense Talent Labs Inc.

- 6.4.11 Recruitee B.V.

- 6.4.12 Hireology Inc.

- 6.4.13 PageUp Pty Ltd

- 6.4.14 Talenteria Inc.

- 6.4.15 Jobilla Oy

- 6.4.16 GR8 People Inc.

- 6.4.17 Yello Inc.

- 6.4.18 TalentLyft (Zero Molecule d.o.o.)

- 6.4.19 Radancy

- 6.4.20 SmartDreamers S.R.L.

- 6.4.21 Clinch Technology Ltd.

- 6.4.22 Eightfold AI Inc.

- 6.4.23 Breezy HR Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

技術技能評估平台市場:預測(至2034年)-按組件、評估類型、部署方式、技術、最終用戶和地區分類的全球分析

技術技能評估平台市場:預測(至2034年)-按組件、評估類型、部署方式、技術、最終用戶和地區分類的全球分析 2026年國際搬家服務全球市場報告

2026年國際搬家服務全球市場報告 全球臨時工市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球臨時工市場規模、佔有率、趨勢和成長分析報告(2026-2034) 臨時勞動力市場規模、佔有率和成長分析(按類型、最終用途和地區分類)-2026-2033年產業預測

臨時勞動力市場規模、佔有率和成長分析(按類型、最終用途和地區分類)-2026-2033年產業預測 人工智慧應用市場規模、佔有率和成長分析(按組件、部署模式、公司規模、應用、最終用戶和地區分類)—產業預測(2026-2033 年)全球臨時勞動力市場規模(按類型、最終用戶、區域範圍和預測)

人工智慧應用市場規模、佔有率和成長分析(按組件、部署模式、公司規模、應用、最終用戶和地區分類)—產業預測(2026-2033 年)全球臨時勞動力市場規模(按類型、最終用戶、區域範圍和預測) 2031 年亞太地區人員配備和招聘市場預測 - 區域分析 - 按人員配備類型(臨時和永久)、招聘管道(線上、混合和線下)和最終用戶分類

2031 年亞太地區人員配備和招聘市場預測 - 區域分析 - 按人員配備類型(臨時和永久)、招聘管道(線上、混合和線下)和最終用戶分類 2031 年北美人員配備和招聘市場預測 - 區域分析 - 按人員配備類型(臨時和永久)、招聘管道(線上、混合和線下)和最終用戶

2031 年北美人員配備和招聘市場預測 - 區域分析 - 按人員配備類型(臨時和永久)、招聘管道(線上、混合和線下)和最終用戶 歐洲人員配備和招聘市場預測(至 2031 年)- 區域分析 - 按人員配備類型(臨時和永久)、招聘管道(線上、混合和線下)和最終用戶

歐洲人員配備和招聘市場預測(至 2031 年)- 區域分析 - 按人員配備類型(臨時和永久)、招聘管道(線上、混合和線下)和最終用戶 招聘:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

招聘:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)