|

市場調查報告書

商品編碼

2073169

中國至歐洲跨境電商物流:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)China To Europe Cross-Border E-commerce Logistics Analysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

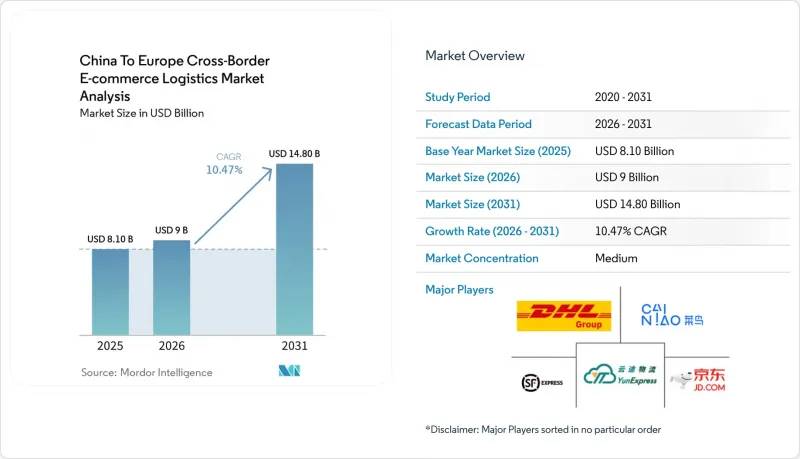

根據 Mordor Intelligence 預測,2025 年中國到歐洲的跨境電子商務物流市場規模預計將達到 81 億美元,2026 年達到 90 億美元,2031 年達到 148 億美元,2026 年至 2031 年的複合年成長率為 10.47%。

本報告按產品類型(時尚生活、個人護理及家居用品、其他)、物流功能(運輸、倉儲配送、附加價值服務)、經營模式(B2C、B2B、C2C)、配送速度(快遞、標準)和發送國(西歐、東歐、北歐)進行細分。市場預測以美元計價。

中國至歐洲跨境電商物流市場分析:洞察與趨勢

運往歐洲的小包裹數量激增,主要由中國物流平台主導。

中國電商平台徹底改變了中歐之間物流路線的小包裹處理量格局。預計到2025年,將有59億件低價值小包裹抵達歐盟,其中歐盟委員會預測近90%將來自中國。包裹量的成長進一步加劇了中歐跨境電商物流市場的海關資料處理、邊境通關系統以及最後一公里配送能力的壓力。物流供應商也被迫投資自動化申報工具和更完善的到貨前資料處理系統,以防止因海關延誤而導致小包裹處理能力中斷。到2026年,中國平台也將把更多庫存轉移到歐盟境內的倉庫,減少對大批量SKU(庫存單位)小小包裹直接運輸的依賴。這進一步拉大了僅提供小包裹運輸服務的供應商與能夠在同一營運模式下同時管理直接消費者小包裹配送和倉庫批量補貨的供應商之間的差距。

符合 ISOS 標準的結帳流程可確保稅務透明度和順暢的清關流程。

進口一站式服務 (IOSS) 的推出降低了許多向歐盟出貨的大宗經銷商的海關摩擦。 2025 年 5 月,歐盟理事會就簡化進口稅徵收措施達成一致,歐盟委員會表示,這項新措施旨在改善電子商務進口的貿易和合規性。這對從中國到歐洲的跨境電子商務物流市場具有重大意義,因為在結帳時收取增值稅(VAT) 的賣家可以降低貨物在邊境運輸的不確定性。類似的合規方法目前正擴展到 ICS2 系統,該系統透過提高資料品質來降低註冊營運商的檢查風險並提高處理速度。擁有自有海關入口網站的承運商具有優勢,因為他們可以將稅務處理、報關和海關程序整合到單一服務中。隨著歐盟向更加集中的海關資料模型邁進,對標準化資料管道的早期投資不再只是遵循成本,而正在成為一項實際的服務優勢。

歐盟對低價值商品免關稅並取消小包裹費。

歐盟取消150歐元(162美元)的關稅豁免是影響該運輸路線的最重要短期監管變化。 2025年12月,歐洲理事會同意自2026年7月1日起對小小包裹徵收關稅,對價值低於150歐元(173.59美元)的小包裹,按每個關稅類別徵收3歐元(3.20美元)的固定費用。如果賣家繼續使用直接從中國小包裹的方式,這項新規將降低低價商品組合的吸引力。平台也將被迫將熱銷商品轉移到歐洲的倉儲設施,並透過批量進口而非重複進口低價值小包裹來管理關稅風險。儘管如此,這並不會消除中國到歐洲跨境電商物流市場的需求。相反,部分收入來源將轉向海運、鐵路運輸、倉儲和歐洲國內配送。因此,能夠同時處理直接小包裹物流和本地補貨物流的供應商,即使監管模式發生變化,也更有能力保持獲利能力。

細分市場分析

預計2025年,時尚生活類別將佔據中國至歐洲跨境電商物流市場佔有率的31.47%,而個人護理及家居用品類別預計到2031年將以11.45%的複合年成長率成長。時尚品類之所以能維持領先地位,主要得益於Shein和Temu等電商平台在歐洲的服飾、鞋履及配件訂單量龐大。然而,隨著中國經銷商拓展護膚、健康及家居用品品類,品類組成正在改變。這些品類鼓勵消費者重複購買,且退貨率通常低於服裝。此外,家用電器及消費性電器產品也持續佔有重要的戰略地位,Anker、小米、大疆等品牌不斷推高對更安全運輸、更優質包裝及更嚴格倉儲條件的需求。

食品飲料和家具在中國至歐洲的跨境電商物流行業中所佔佔有率仍然相對較小,但這兩個品類都面臨嚴峻的挑戰。食品飲料在歐洲需要更嚴格的溫度控制,並且需要更嚴格的食品法規相關文件。家具重量大且運輸頻率低,這可能導致每筆訂單的物流成本居高不下,從而迅速降低客戶價值。順豐國際的數據顯示,2025年上半年中國至歐洲的跨境電商物流銷售額較去年同期加倍,其中服裝和電子產品佔了相當大的佔有率。這一銷售趨勢表明,中國至歐洲的電商物流市場不僅受益於訂單量的成長,也受益於那些能夠提高單筆訂單履約收入的品類。

預計到2025年,運輸環節將佔中國至歐洲跨境電商物流市場規模的71.20%,附加價值服務及其他相關業務預計到2031年將以15.64%的複合年成長率成長。空運、海運、鐵路和陸運將繼續滿足沿線不同的緊急程度和成本需求,使運輸環節成為最大的收入來源。同時,退貨處理、合規標籤、國際線上銷售服務(IOSS)管理、海關支援和套件組裝等領域正經歷加速成長。此外,隨著越來越多的中國經銷商在歐洲備貨以縮短交貨時間,倉儲、配送和庫存管理的重要性日益凸顯。

航空運輸業對緊急和高價值訂單仍保持結構性溢價,順豐航空已於2026年4月開通鄂州華虎至巴黎戴高樂機場的每週兩班B747-400F貨機航班,進一步增強了運力。鐵路運輸佔有重要的中間地位。 2026年第一季,中歐班列營運5,460架次,運輸54萬個標準箱,分別較去年同期成長29%及22%。鑑於海運航線的不穩定性,鐵路運輸對中價位補給貨物的吸引力日益增強,這項業績意義重大。從長遠來看,這種轉變將使部分補給貨物能夠在不大幅減少倉儲或歐洲國內物流需求的情況下,從海運轉向鐵路運輸。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況及跨境電商物流在電商市場的作用

- 電子商務產業趨勢

- 消費者行為及供需分析

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 運往歐洲的小包裹數量激增,主要由中國物流平台主導。

- 符合 ISOS 標準的結帳流程可確保稅務透明度和順暢的清關程序。

- 中國經銷商對歐盟倉庫的本地化

- 注重成本績效的歐洲消費者更喜歡來自中國的產品系列。

- 提高宅配的摩擦。

- 中價位補貨SKU的鐵路、海運及空運運輸方式轉型

- 市場限制因素

- 歐盟取消低價值商品關稅豁免及小包裹費用

- 非歐盟經銷商。

- 逆向物流的經濟優勢削弱了人們購買低價大件商品的慾望。

- 紅海和歐亞鐵路變化導致的路線風險轉移

- 技術創新的前景

- 波特五力模型

- 跨境電子商務物流需求的演變

- 地緣政治事件對供應鏈轉型的影響

第5章 市場規模及成長預測(價值與數量,2020-2031 年)

- 產品類型

- 食品/飲料

- 個人護理和居家護理

- 時尚與生活方式(配件、服裝、鞋類)

- 家具

- 家用電子電器和電器產品

- 其他產品

- 按職能分類的物流

- 運輸

- 道路運輸

- 航空

- 海路和內河航道

- 鐵路

- 倉儲、物流和庫存管理

- 附加價值服務及其他

- 運輸

- 按經營模式

- B2C

- B2B

- C2C

- 按配送速度

- 表達

- 標準

- 發送國

- 西歐

- 德國

- 法國

- 英國

- 比荷盧經濟聯盟

- 西班牙

- 義大利

- 其他西歐國家

- 東歐

- 波蘭

- 捷克共和國

- 匈牙利

- 羅馬尼亞

- 其他東歐國家

- 北歐(北歐國家和波羅的海國家)

- 西歐

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- Cainiao Group

- JD Logistics

- SF Express/SF International

- YunExpress

- 4PX Express

- Yanwen Express

- J&T Express International

- ZTO Express Global

- YTO International Express and Supply Chain Technology

- ECMS Express

- Asendia

- CEVA Logistics(CMA CGM)

- DSV(including DB schenker)

- Kuehne+Nagel

- GEODIS

- FedEx Cross Border

- UPS

- CH Robinson

- Meest China-Europe Logistics

- CIRRO E-Commerce

- RongExpress

第7章 市場機會與未來展望

According to Mordor Intelligence, the china-to-Europe cross-border e-commerce logistics market size was valued at USD 8.10 billion in 2025 and is projected to be USD 9 billion in 2026 and USD 14.80 billion by 2031, growing at a CAGR of 10.47% from 2026 to 2031.

This report is Segmented by Product Category (Fashion and Lifestyle, Personal and Household Care, and More), by Logistics Function (Transportation, Warehousing and Distribution, Value-Added Services), by Business Model (B2C, B2B, C2C), by Delivery Speed (Express, Standard), and by Destination Country (Western, Eastern, Northern Europe). The Market Forecasts are Provided in Terms of Value (USD).

Insights and Trends of China To Europe Cross-Border E-commerce Logistics Market Analysis

Chinese Platform-Led Parcel Volume Surge into Europe

Chinese fast-commerce platforms have changed the volume base on the China-Europe corridor. The EU received 5.9 billion low-value parcels in 2025, and the European Commission said close to 90% of those parcels came from China. That volume is putting more pressure on customs data processing, border release systems, and final-mile carrier capacity across the China-to-Europe cross-border e-commerce logistics market. It is also pushing logistics providers to invest in automated declaration tools and stronger pre-arrival data handling to prevent clearance delays from disrupting parcel throughput. In 2026, Chinese platforms are also moving more inventory into EU warehouses, which reduces reliance on direct small-parcel shipping for high-volume stock-keeping units. This is widening the gap between providers that only move parcels and providers that can manage direct consumer parcels and bulk warehouse replenishment within the same operating model.

IOSS-Enabled Checkout Tax Transparency and Smoother Clearance

The Import One-Stop Shop has reduced customs friction for many high-volume sellers shipping into the EU. In May 2025, the Council of the European Union agreed on its position on measures designed to simplify tax collection for imports, and the European Commission stated that the new approach was intended to improve trade and compliance for e-commerce imports. In the China-to-Europe cross-border e-commerce logistics market, this matters because sellers who collect VAT at checkout can move goods with less border uncertainty. The same compliance logic now extends into ICS2, where better data quality can reduce inspection risk and improve processing speed for registered operators. Carriers with their own customs gateways are in a stronger position because they can package tax handling, customs filing, and border release into one service. As the EU moves toward a more centralized customs data model, early investment in standardized data pipelines is becoming a practical service advantage rather than only a compliance expense.

End of EU Low-Value Duty Relief and Parcel Fees

The removal of the EU's EUR 150 (USD 162) customs duty exemption is the most important near-term regulatory change affecting this corridor. In December 2025, the Council agreed to levy customs duty on small parcels from July 1, 2026, and this reform introduced a flat EUR 3 (USD 3.2) charge per tariff heading on sub-EUR 150 (USD 173.59) parcels. The rule makes very low-ticket baskets less attractive when sellers continue to use direct parcel shipping from China. It also pushes platforms to shift popular items into European storage programs so duty exposure is managed through bulk imports rather than repeated low-value parcel entries. That does not remove logistics demand from the China-to-Europe cross-border e-commerce logistics market. Still, it does shift part of the revenue base toward ocean, rail, warehousing, and domestic European distribution. Providers that can handle both direct parcel flows and localized replenishment flows are therefore better placed to protect revenue as the regulatory model changes.

Other drivers and restraints analyzed in the detailed report include:

- EU Warehousing Localization by China-Linked Sellers

- Parcel-Locker and Out-Of-Home Density Lowers Last-Mile Friction

- GPSR and ICS2 Data-Compliance Burden on Non-EU Sellers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fashion and lifestyle accounted for 31.47% of the China-to-Europe cross-border e-commerce logistics market share in 2025, while personal and household care is forecast to grow at a 11.45% CAGR through 2031. Fashion kept the lead because Shein and Temu built very high order volumes in apparel, footwear, and accessories across Europe. Even so, the category mix is changing as Chinese sellers add more skincare, wellness, and household care lines that encourage repeat purchases and usually face lower return rates than apparel. Consumer electronics and household appliances also remain strategically important because brands such as Anker, Xiaomi, and DJI create demand for safer transport, better packaging, and more controlled storage conditions.

Foods and beverages and furniture remain smaller parts of the China-to-Europe cross-border e-commerce logistics industry, but both categories pose difficult handling requirements. Foods and beverages require stronger temperature control and tighter food compliance documentation inside Europe. Furniture creates high-weight, low-frequency shipments, where logistics costs per order can quickly erode the customer value proposition. SF International said its cross-border e-commerce logistics revenue from China to Europe doubled year on year in H1 2025, and apparel and electronics were important parts of that mix. That revenue pattern suggests the China-to-Europe e-commerce logistics market is gaining value not only from more orders, but also from categories that support higher fulfillment revenue per shipment.

Transportation accounted for 71.20% of the China to Europe cross-border e-commerce logistics market size in 2025, while value-added services and others are projected to grow at 15.64% CAGR through 2031. Air, ocean, rail, and road continue to serve different urgency and cost needs on the corridor, so transport remains the largest revenue pool. At the same time, the faster-growing opportunity is moving toward returns handling, compliance labeling, IOSS administration, customs support, and kitting. Warehousing, distribution, and inventory management are also becoming increasingly important as more chinese sellers stock goods in Europe to shorten delivery windows.

The air segment still carries a structural premium for urgent or higher-value orders, and SF Airlines launched a twice-weekly B747-400F service between Ezhou Huahu and Paris-Charles de Gaulle in April 2026 to strengthen that capability. Rail is holding a valuable middle position because the China-Europe Railway Express handled 5,460 train trips and 546,000 TEUs in Q1 2026, up 29% and 22% year on year. That performance matters because route instability in maritime corridors has made rail more attractive for mid-value replenishment cargo. Over time, that shift can move some replenishment freight from ocean to rail without materially reducing the need for warehousing and domestic European distribution.

Complete Report Scope:

- By Product Category

- Foods and Beverages

- Personal and Household Care

- Fashion and Lifestyle (Accessories, Apparel, Footwear)

- Furniture

- Consumer Electronics and Household Appliances

- Other Products

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing, Distribution and Inventory Management

- Value-added Services and Others

- Transportation

- By Business Model

- B2C

- B2B

- C2C

- By Delivery Speed

- Express

- Standard

- By Destination Country

- Western Europe

- Germany

- France

- United Kingdom

- BENELUX

- Spain

- Italy

- Rest of Western Europe

- Eastern Europe

- Poland

- Czech Republic

- Hungary

- Romania

- Rest of Eastern Europe

- Northern Europe (Nordics & Baltic Countries)

- Western Europe

List of Companies Covered in this Report:

- DHL Group

- Cainiao Group

- JD Logistics

- SF Express / SF International

- YunExpress

- 4PX Express

- Yanwen Express

- J&T Express International

- ZTO Express Global

- YTO International Express and Supply Chain Technology

- ECMS Express

- Asendia

- CEVA Logistics (CMA CGM)

- DSV (including DB schenker)

- Kuehne+Nagel

- GEODIS

- FedEx Cross Border

- UPS

- C.H. Robinson

- Meest China-Europe Logistics

- CIRRO E-Commerce

- RongExpress

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview & Role of Cross-border E-commerce Logistics in E-commerce Market

- 4.2 Trends in E-Commerce Industry

- 4.3 Consumer Behavior and Demand-Supply Analysis

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Chinese Platform-Led Parcel Volume Surge into Europe

- 4.6.2 IOSS-Enabled Checkout Tax Transparency and Smoother Clearance

- 4.6.3 EU Warehousing Localization By China-Linked Sellers

- 4.6.4 Value-Seeking European Consumers Favor China-Origin Assortments

- 4.6.5 Parcel-Locker and Out-Of-Home Density Lowers Last-Mile Friction

- 4.6.6 Rail-Sea-Air Mode Shifting for Mid-Value Replenishment SKUs

- 4.7 Market Restraints

- 4.7.1 End of EU Low-Value Duty Relief and Parcel Fees

- 4.7.2 GPSR and ICS2 Data-Compliance Burden on Non-EU Sellers

- 4.7.3 Reverse-Logistics Economics Weaken Low-Ticket Bulky Baskets

- 4.7.4 Route-Risk Migration from Red Sea and Eurasian Rail Volatility

- 4.8 Technology Innovations Outlook

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Rivalry Among Competitors

- 4.10 Evolution of Cross-border E-commerce Logistics Requirements

- 4.11 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value and Volume, 2020-2031)

- 5.1 By Product Category

- 5.1.1 Foods and Beverages

- 5.1.2 Personal and Household Care

- 5.1.3 Fashion and Lifestyle (Accessories, Apparel, Footwear)

- 5.1.4 Furniture

- 5.1.5 Consumer Electronics and Household Appliances

- 5.1.6 Other Products

- 5.2 By Logistics Function

- 5.2.1 Transportation

- 5.2.1.1 Road

- 5.2.1.2 Air

- 5.2.1.3 Sea and Inland Waterways

- 5.2.1.4 Rail

- 5.2.2 Warehousing, Distribution and Inventory Management

- 5.2.3 Value-added Services and Others

- 5.2.1 Transportation

- 5.3 By Business Model

- 5.3.1 B2C

- 5.3.2 B2B

- 5.3.3 C2C

- 5.4 By Delivery Speed

- 5.4.1 Express

- 5.4.2 Standard

- 5.5 By Destination Country

- 5.5.1 Western Europe

- 5.5.1.1 Germany

- 5.5.1.2 France

- 5.5.1.3 United Kingdom

- 5.5.1.4 BENELUX

- 5.5.1.5 Spain

- 5.5.1.6 Italy

- 5.5.1.7 Rest of Western Europe

- 5.5.2 Eastern Europe

- 5.5.2.1 Poland

- 5.5.2.2 Czech Republic

- 5.5.2.3 Hungary

- 5.5.2.4 Romania

- 5.5.2.5 Rest of Eastern Europe

- 5.5.3 Northern Europe (Nordics & Baltic Countries)

- 5.5.1 Western Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Cainiao Group

- 6.4.3 JD Logistics

- 6.4.4 SF Express / SF International

- 6.4.5 YunExpress

- 6.4.6 4PX Express

- 6.4.7 Yanwen Express

- 6.4.8 J&T Express International

- 6.4.9 ZTO Express Global

- 6.4.10 YTO International Express and Supply Chain Technology

- 6.4.11 ECMS Express

- 6.4.12 Asendia

- 6.4.13 CEVA Logistics (CMA CGM)

- 6.4.14 DSV (including DB schenker)

- 6.4.15 Kuehne+Nagel

- 6.4.16 GEODIS

- 6.4.17 FedEx Cross Border

- 6.4.18 UPS

- 6.4.19 C.H. Robinson

- 6.4.20 Meest China-Europe Logistics

- 6.4.21 CIRRO E-Commerce

- 6.4.22 RongExpress

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment