|

市場調查報告書

商品編碼

1940818

東協跨境公路貨運:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)ASEAN Cross Border Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

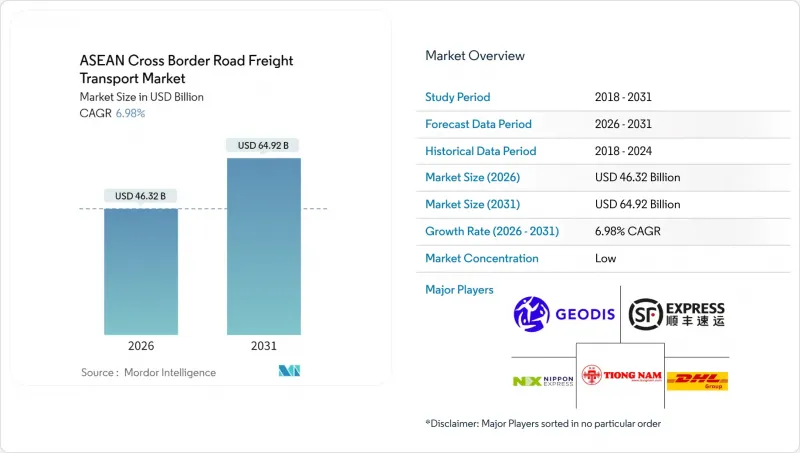

預計到 2026 年,東協區域內跨境公路貨運市場規模將達到 463.2 億美元,高於 2025 年的 433 億美元。

預計到 2031 年將達到 649.2 億美元,2026 年至 2031 年的複合年成長率為 6.98%。

預計到2030年,東協內部貿易額將達到8,000億美元,因此,可預測的卡車運輸能力日益受到關注。同時,東協單一窗口的推出已將平均邊境通關時間縮短了4天,降低了貨物落地成本,並提高了服務可靠性。借助東協海關過境系統(ACTS)的API基礎設施,數位化貨運平台正在減少空駛,並吸引尋求即時貨物可視性的跨國托運人的注意。此外,製造業外商直接投資(FDI)向柬埔寨、寮國、緬甸和越南(CLMV)的重新配置,建立了新的零件運輸走廊;印尼下游鎳加工產業的快速成長也帶來了穩定的危險品運輸量,使認證承運商受益。然而,持續的司機短缺、新的燃油定價機制以及昆明萬象鐵路的競爭仍然是主要的挑戰。

東協跨境公路貨運市場趨勢及洞察

東協電子商務的蓬勃發展推動了對時效性強的跨境卡車運輸的需求。

小包裹運輸的快速成長正推動市場朝向更小、更頻繁的運輸模式轉變,這對傳統的整車運輸模式構成了挑戰。同時,跨境運輸可享有更高的定價。 2025年第二季度,J&T Express在東南亞處理了16.9億件小包裹,年增65.9%。目前,每天有5400輛長途貨車跨境運輸。市場對隔日送達保證和支援API介面的貨物狀態更新的需求日益成長,推動了承運商採用遠端資訊處理和動態路線規劃工具。這種數位化整合促進了跨境快遞服務的成長,縮短了運輸時間,增強了採用平台經濟標準的承運商的競爭優勢。

《貿易便利化與貿易協定》(ACTS)及相關貿易便利化架構可減少邊境延誤。

東協海關清關系統(ACTS)是對合規流程的結構性改革,它透過單一電子擔保簡化了多邊清關流程,並顯著減少了紙本文件。新加坡、馬來西亞和泰國之間的領先走廊已將貨物停留時間從24小時縮短至少於6小時,從而提高了拖車周轉率和資產回報率。新加坡計劃於2025年對其車輛許可證流程進行升級,使道路運輸單據與ACTS資料欄位保持一致,以支援無縫通行。經認證的經營者(AEO)快速通道進一步明確了有利於合規承運人的分級框架,提高了非正式駕駛人的准入門檻,並鼓勵托運人過渡到使用經過審核的車輛。

長期存在的司機短缺和卡車車隊老化問題正在推高營運成本。

區域工資差距和人口結構變化導致合格駕駛員供應緊張。在日本,透過特定技能簽證計畫接納越南和印尼的駕駛員,一方面填補了國內駕駛員短缺,另一方面也進一步消耗了本地駕駛員資源。車輛老化導致停機時間增加,而馬來西亞將於2024年取消柴油補貼,燃油價格波動加劇,駕駛不願再投資。危險品和溫控運輸的認證要求也加劇了駕駛員短缺,並推高了這些特殊領域駕駛員的溢價。包括泰國對歐6排放標準卡車的稅收減免在內的車隊更新計劃,在一定程度上緩解了駕駛員短缺的影響,但無法完全抵消即將到來的勞動力錯配問題。

細分市場分析

到2025年,製造業將佔東協跨境公路貨運市場的33.78%,反映出電子、汽車和服裝零件即時供應鏈的建立。中越、越泰等零件運輸密集走廊的日常環線運輸,支撐了較高的拖車運轉率,並滿足了大型第三方物流公司(3PL)的大量採購需求。 「中國+1」投資的湧入鞏固了越南和柬埔寨作為組裝中心的地位,提振了對跨境運輸服務的需求。儘管批發零售業基數較小,但預計其增速將超過其他行業,在2026年至2031年間以8.08%的複合年成長率成長,這主要得益於B2C小包裹運輸的快速成長,此類運輸需要嚴格的組裝時間表和頻繁的出貨。這兩個趨勢正在形成複雜的貨物組合,迫使承運商對其車隊進行多元化經營,從乾貨車到溫控車,以確保在多個細分市場中獲得利潤。

印尼鎳加工產業的蓬勃發展為石油天然氣、採礦和採石叢集帶來了結構性成長,也催生了對專門用於處理危險物品的卡車車隊的需求。泰國和越南水產品低溫運輸的擴張增加了冷藏運輸路線,而建築材料則受益於與中國「一帶一路」計劃相關的大規模公路和鐵路計劃。產業結構的轉變表明,運輸模式正從以大宗商品為主轉向以高價值、時效性強的貨物為主,從而獲得更高的回報。這種轉變推動了東協跨境公路貨運市場的擴張,並凸顯了車隊更新和駕駛員技能提升的戰略必要性。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 按經濟活動分類的GDP分配

- 按經濟活動分類的GDP成長

- 經濟表現及概覽

- 電子商務產業的趨勢

- 製造業趨勢

- 運輸和倉儲業的GDP

- 物流績效

- 道路長度

- 出口趨勢

- 進口趨勢

- 燃油價格趨勢

- 卡車運輸營運成本

- 卡車運輸車隊規模(按類型)

- 主要卡車供應商

- 公路貨運量趨勢

- 公路貨運費率趨勢

- 按交通方式分享

- 通貨膨脹

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 東協電子商務的快速成長正在推動對時效性強的跨境卡車運輸的需求。

- 透過《東協貿易便利化協定》(ACTS)和其他東協貿易便利化框架減少邊境延誤時間

- 快速的製造業外商直接投資轉向柬埔寨、寮國、越南、緬甸(CLMV),並促進東協內部的零件分銷。

- 印尼電池鎳出口走危險物品路線

- 水產品和農產品低溫運輸的發展開啟了新的溫控運輸路線

- 使用 ACTS API 的數位貨運平台顯著降低了空服率

- 市場限制

- 長期存在的司機短缺和卡車車隊老化問題正在推高營運成本。

- 軸荷規定執行不力擾亂長途運輸時刻表

- 昆明-萬像走廊和泛婆羅洲走廊改用鐵路運輸將減少長途道路運輸的貨運量。

- 甲醇價格上漲威脅印尼B40生質柴油的成本優勢。

- 市場創新

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 終端用戶產業

- 農業、漁業、林業

- 建設業

- 製造業

- 石油天然氣、採礦和採石

- 批發和零售

- 其他

- 按國家/地區

- 印尼

- 馬來西亞

- 泰國

- 越南

- 其他東南亞國協

第6章 競爭情勢

- 市場集中度

- 關鍵策略舉措公司

- 市佔率分析

- 公司簡介

- "K"Line Logistics, Ltd.

- Bintang Baru Forwarding Sdn. Bhd.

- DHL Group

- Dimerco

- EWT Logistics

- Gemadept

- GEODIS

- J&T Express

- Kart Asia

- Konoike Group(including Konoike Transport Co., Ltd.)

- LOGISTEED, Ltd

- Mitsui OSK Lines

- Nippon Express Holdings

- Overland Total Logistic Services(M)Sdn Bhd

- Profreight Group

- SF Express(KEX-SF)

- SUMISHO GLOBAL LOGISTICS(THAILAND)CO., LTD.

- Team Global Logistics Co., Ltd.

- Tiong Nam Logistics Holdings Bhd

- Yatfai

第7章 市場機會與未來展望

ASEAN cross border road freight transport market size in 2026 is estimated at USD 46.32 billion, growing from 2025 value of USD 43.3 billion with 2031 projections showing USD 64.92 billion, growing at 6.98% CAGR over 2026-2031.

Rising intra-ASEAN trade, valued at USD 800 billion by 2030, is sharpening the focus on predictable trucking capacity, while the ASEAN Single Window continues to trim average border clearance by four days, lowering landed costs and elevating service reliability. Digital freight platforms tapping the ASEAN Customs Transit System (ACTS) API infrastructure reduce empty-mile rates and attract multinational shippers that require real-time shipment visibility. At the same time, manufacturing FDI reallocations toward Cambodia, Laos, Myanmar, and Vietnam (CLMV) anchor fresh component corridors, while Indonesia's downstream nickel-processing boom creates steady hazardous-goods volumes that reward certified carriers. Persistent driver shortages, new fuel-pricing regimes, and rail competition from the Kunming-Vientiane route remain the principal headwinds.

ASEAN Cross Border Road Freight Transport Market Trends and Insights

ASEAN E-Commerce Boom Fuels Time-Sensitive Cross-Border Truckload Demand

Soaring parcel volumes have moved the market toward smaller, higher-frequency shipments that challenge legacy full-truckload models yet unlock premium pricing for expedited cross-border lanes. J&T Express handled 1.69 billion parcels in Southeast Asia during Q2 2025, a 65.9% year-on-year rise, relying on 5,400 long-haul vehicles that now traverse multiple borders daily. Marketplaces increasingly insist on guaranteed next-day delivery windows and API-enabled status updates, prompting fleets to install telematics and dynamic routing tools. This digital integration supports growth in cross-border express services and compresses transit windows, heightening the competitive advantage of carriers that embrace platform economy standards.

ACTS and Allied Trade-Facilitation Frameworks Cut Border Dwell Time

The ASEAN Customs Transit System represents a structural change in compliance processing, providing a single electronic guarantee regime that simplifies multi-country clearances and slashes paperwork. Early-adopter corridors linking Singapore, Malaysia, and Thailand report dwell-time reductions from 24 hours to under six, producing higher trailer turns and improved asset yields. Singapore's 2025 upgrade of vehicle-permit procedures aligns road-haul documentation with ACTS data fields, underpinning seamless transfers. Authorized Economic Operator (AEO) fast-track lanes further demarcate a tiered framework that rewards compliant carriers, raising barriers for informal truckers and nudging shippers toward vetted fleets.

Chronic Driver Shortages and Ageing Truck Fleets Push Operating Costs Up

Regional wage gaps and demographic shifts squeeze the pool of qualified drivers, with Japan recruiting Vietnamese and Indonesian operators under its specified-skills visa to plug its own shortages, further draining local supply. Older vehicles require more downtime, and operators hesitate to reinvest amid fuel-price volatility following Malaysia's 2024 diesel subsidy removal. Certification requirements for hazardous and temperature-controlled haulage exacerbate scarcities, inflating driver premiums in these niches. Fleet renewal programs, including tax rebates in Thailand for Euro 6 trucks, partially soften the blow, yet cannot fully offset the immediate labor mismatch.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Manufacturing FDI Shift to CLMV Drives Intra-ASEAN Component Flows

- Digital Freight Platforms Using ACTS Apis Slash Empty-Mile Rates

- Rail Modal Shift on Kunming-Vientiane and Pan-Borneo Corridors Cannibalizes Long-Haul Road Tonnage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing contributed 33.78% to the ASEAN cross border road freight transport market share in 2025, reflecting entrenched just-in-time supply chains for electronics, automotive, and apparel components. Component-heavy corridors-such as China to Vietnam and Vietnam to Thailand-register daily loops that underpin elevated trailer utilization rates and sustain high-capacity purchases among large 3PLs. The influx of China-plus-one investment cements Vietnam and Cambodia as assembly hubs, inflating demand for cross-border shuttle runs feeding final-assembly lines. Wholesale and retail trade, although accounting for a smaller base, will outrun every other sector at an 8.08% CAGR between 2026-2031, propelled by surging B2C parcel flows that call for tight delivery windows and frequent dispatches. These twin patterns build a more complex freight mix that forces carriers to diversify equipment-from dry vans to temperature-controlled units-ensuring they capture value across multiple verticals.

The oil and gas, mining, and quarrying cluster receives a structural uplift from Indonesia's nickel-processing boom, which necessitates specialized truck fleets outfitted for hazardous materials. Cold-chain build-outs for fisheries in Thailand and Vietnam add reefer lanes, while construction materials benefit from large-scale road and rail projects entwined with China's Belt and Road initiatives. The sector mix signals a shift away from dominance by bulk commodities toward a balanced portfolio where high-value, time-critical loads command premium yields. This evolution underpins the ASEAN cross border road freight transport market size expansion trajectory, reinforcing the strategic imperative for fleet renewal and driver up-skilling.

The ASEAN Cross Border Road Freight Transport Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Manufacturing, Construction, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others) and by Country (Indonesia, Malaysia, Thailand, Vietnam, and Rest of ASEAN). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- "K"Line Logistics, Ltd.

- Bintang Baru Forwarding Sdn. Bhd.

- DHL Group

- Dimerco

- EWT Logistics

- Gemadept

- GEODIS

- J&T Express

- Kart Asia

- Konoike Group (including Konoike Transport Co., Ltd.)

- LOGISTEED, Ltd

- Mitsui O.S.K. Lines

- Nippon Express Holdings

- Overland Total Logistic Services (M) Sdn Bhd

- Profreight Group

- SF Express (KEX-SF)

- SUMISHO GLOBAL LOGISTICS (THAILAND) CO., LTD.

- Team Global Logistics Co., Ltd.

- Tiong Nam Logistics Holdings Bhd

- Yatfai

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 GDP Distribution by Economic Activity

- 4.3 GDP Growth by Economic Activity

- 4.4 Economic Performance and Profile

- 4.4.1 Trends in E-Commerce Industry

- 4.4.2 Trends in Manufacturing Industry

- 4.5 Transport and Storage Sector GDP

- 4.6 Logistics Performance

- 4.7 Length of Roads

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Pricing Trends

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Road Freight Tonnage Trends

- 4.15 Road Freight Pricing Trends

- 4.16 Modal Share

- 4.17 Inflation

- 4.18 Regulatory Framework

- 4.19 Value Chain and Distribution Channel Analysis

- 4.20 Market Drivers

- 4.20.1 ASEAN E-Commerce Boom Fuels Time-Sensitive Cross-Border Truckload Demand

- 4.20.2 ACTS and Other ASEAN Trade-Facilitation Frameworks Cut Border Dwell Time

- 4.20.3 Rapid Manufacturing FDI Shift to CLMV Drives Intra-ASEAN Component Flows

- 4.20.4 Battery-Grade Nickel Exports from Indonesia Create Hazardous-Goods Trucking Corridors

- 4.20.5 Cold-Chain Build-Out for Seafood and Produce Opens New Temperature-Controlled Lanes

- 4.20.6 Digital Freight Platforms Using ACTS APIs Slash Empty-Mile Rates

- 4.21 Market Restraints

- 4.21.1 Chronic Driver Shortages and Ageing Truck Fleets Push Operating Costs Up

- 4.21.2 Uneven Axle-Load Enforcement Disrupts Long-Haul Scheduling

- 4.21.3 Rail Modal Shift on Kunming-Vientiane and Pan-Borneo Corridors Cannibalises Long-Haul Road Tonnage

- 4.21.4 Methanol Price Spikes Jeopardise Indonesia's B40 Biodiesel Cost Advantage

- 4.22 Technology Innovations in the Market

- 4.23 Porter's Five Forces Analysis

- 4.23.1 Threat of New Entrants

- 4.23.2 Bargaining Power of Buyers

- 4.23.3 Bargaining Power of Suppliers

- 4.23.4 Threat of Substitutes

- 4.23.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Country

- 5.2.1 Indonesia

- 5.2.2 Malaysia

- 5.2.3 Thailand

- 5.2.4 Vietnam

- 5.2.5 Rest of ASEAN

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 "K"Line Logistics, Ltd.

- 6.4.2 Bintang Baru Forwarding Sdn. Bhd.

- 6.4.3 DHL Group

- 6.4.4 Dimerco

- 6.4.5 EWT Logistics

- 6.4.6 Gemadept

- 6.4.7 GEODIS

- 6.4.8 J&T Express

- 6.4.9 Kart Asia

- 6.4.10 Konoike Group (including Konoike Transport Co., Ltd.)

- 6.4.11 LOGISTEED, Ltd

- 6.4.12 Mitsui O.S.K. Lines

- 6.4.13 Nippon Express Holdings

- 6.4.14 Overland Total Logistic Services (M) Sdn Bhd

- 6.4.15 Profreight Group

- 6.4.16 SF Express (KEX-SF)

- 6.4.17 SUMISHO GLOBAL LOGISTICS (THAILAND) CO., LTD.

- 6.4.18 Team Global Logistics Co., Ltd.

- 6.4.19 Tiong Nam Logistics Holdings Bhd

- 6.4.20 Yatfai

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment