|

市場調查報告書

商品編碼

2072963

英國圍籬市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031)United Kingdom Fencing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

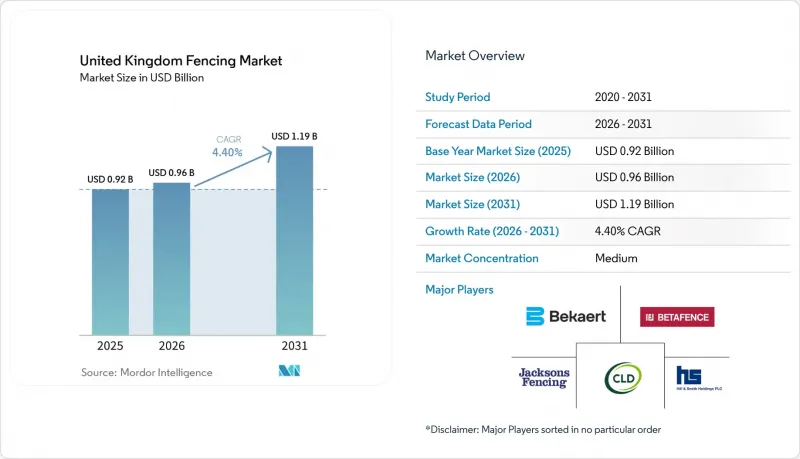

根據 Mordor Intelligence 預測,英國圍籬市場預計將從 2025 年的 9.2 億美元成長到 2026 年的 9.6 億美元,到 2031 年達到 11.9 億美元,2026 年至 2031 年的複合年成長率預計為 4.40%。

本報告按材料(金屬、木材、塑膠/複合材料、混凝土及其他材料)、最終用戶(住宅、農業及其他)、安裝類型(固定/永久性圍欄、臨時/可移動圍欄)、安裝管道(專業承包商及其他)和地區(英格蘭、蘇格蘭、威爾斯和北愛爾蘭)進行細分。市場預測以美元計價。

英國圍籬市場的趨勢與洞察

政府資助的加強周邊安全措施正在推動對關鍵基礎設施周圍圍欄的需求。

「2025年支出審查」承諾,到2028-2029會計年度,每年至少透過綜合安全基金撥款1億英鎊(1.27億美元),將國防資本預算從2025-2026會計年度度的232億英鎊(295億美元)增加到2029-2030會計年度的332億英鎊(422億美元),並專門撥款70億英鎊(89億美元)用於軍用住宅的維修。這項支出基礎對英國圍籬市場意義重大,因為周界安全系統已納入國防、監獄、交通和關鍵基礎設施的預算,而不再僅依賴單一的圍籬更換週期。該審查還撥款70億英鎊(89億美元),用於2031年將拘留設施的容納能力提高1.4萬人,以滿足未來多年對高規格周界圍欄和拘留設施周邊門禁系統的需求。 2025年6月發布的《國家安全戰略》正式將保護關鍵國家基礎設施列為優先事項,採購趨勢也從低成本的外圍安防產品轉向符合標準的認證系統。 Hill & Smith在2025年全年收益報告中指出,資料中心的需求是外圍安防收入的主要驅動力,這表明數位基礎設施正在成為高價值圍欄系統的主要買家。這提高了英國圍欄市場的規格標準,使價值向那些能夠提供經過測試的產品和認證安裝能力,並滿足高階安防標準的供應商傾斜。

疫情後住宅維修活動的活性化,也帶動了住宅圍籬安裝量的上升。

2025年全年,私人住宅的維護和維修活動十分活躍,這將持續支撐2026年的需求,推動英國圍籬市場住宅領域邊界產品的更換和升級需求。英國龐大且老舊的住宅存量意味著住宅需求依然旺盛,即使新房住宅速度放緩,仍需要定期更換圍欄。這種需求的成長不僅源自於安裝活動的增加,也源自於住宅越來越傾向於選擇品質更高、保固期較長的產品,而非基本的入門級圍籬解決方案。供應商的策略也反映了這一趨勢,製造商在2024年和2025年推出了更耐用的木質和混合複合複合材料產品系列,以滿足持續的升級需求。因此,即使英國圍欄市場的整體安裝量成長保持溫和,每個項目的收入也可能增加。此外,儘管公共場所的安全和基礎設施相關的圍欄項目日益受到關注,但住宅領域的重要性依然不減,這凸顯了其在決定競爭地位方面的重要作用。

鋼材和木材價格的波動給圍籬建造公司的利潤率帶來了壓力。

儘管許多項目採用固定價格契約,但材料成本在整個施工期間可能會波動,這使得投入成本的波動成為2026年英國圍欄市場的主要阻礙因素。 2025年,英國木材發展協會(TDUK)報告木材價格有顯著波動。該協會的木材價格指數從2025年初的107上升到2025年中的130,然後在2025年第三季度穩定在125,並由於供應狀況改善,在2025年第四季進一步下降了5%。儘管木材價格在2025年底趨於穩定,但全年的價格波動仍將繼續影響2026年的採購和競標決策。這項挑戰在英國圍籬市場尤為突出,未來材料成本的不確定性可能會阻礙中小型承包商參與公開競標。這可能導致競標競爭減少和合約簽署延遲。此外,成本波動有利於那些能夠管理供應鏈、維持庫存或分散木質、鋼質和複合材料圍欄產品風險的一體化製造商。從長遠來看,即使預計2026年整體需求依然強勁,這些趨勢也可能提升主要廠商的市場佔有率。

細分市場分析

2025年,金屬圍籬佔英國圍籬市場銷售額的46%,成為最大的材料類別。其主導地位得益於在安防、邊界防護、交通運輸、公共產業以及其他將合規網狀圍欄、鋼製圍欄和耐用邊界系統作為標準配置的應用領域的強勁表現。儘管鋼材在金屬市場佔據了較大佔有率,但鋁材憑藉其耐腐蝕性和低維護成本等優點,在住宅和商業領域擴大了市場佔有率。在那些優先考慮安全性能和結構耐久性而非美觀性的項目中,金屬圍欄也保持著明顯的優勢。從這個意義上講,即使其他材料越來越受歡迎,金屬圍欄仍然是英國圍欄市場的核心組成部分。

預計到2031年,塑膠和複合材料的複合年成長率將達到5.5%,成為成長最快的材料類別。這一領域受益於日益成長的永續性要求以及對減少住宅和商業項目後續維護需求的商品的需求。供應商提供的2025年數據顯示,複合材料系統(包括提供15至25年保固的再生材料)將會出現,這進一步凸顯了其與經過處理的木材在整個產品生命週期內的成本差異。雖然木材在住宅和農業圍欄領域仍然佔據重要地位,但其地位正受到高維護要求和消費者對更耐用替代品日益成長的需求的威脅。混凝土在邊界和隔音應用中也發揮著至關重要的作用,尤其是在正在進行維修的道路和鐵路沿線。 「森林研究木材建築路線圖」繼續建議在更廣泛的建築應用中為木材提供政策和採購支持,這可能有助於在當地規範仍然有利於木材的地區增加木柵欄的銷售量。然而,在英國的圍欄市場,材料方面出現了一種日益成長的趨勢,即採用維護需求更少、在永續性方面具有優勢的產品。

到2025年,住宅領域將佔英國圍籬銷售額的38%,成為英國圍籬市場最大的終端用戶群。這一規模反映了英國龐大的住宅基礎以及現有住宅對圍欄更換、維修和花園維修的持續需求。由於需求遍布英國四個組成國,因此該領域並不依賴任何特定的資本支出叢集或單一的機構預算週期。農業領域的需求仍然是英國圍欄市場的主要驅動力,因為農村土地管理和牲畜圈舍需要定期維護邊界。此外,受公共支出計畫的推動,軍事、國防和政府部門的需求也顯著成長,這些計畫促使監獄、軍事設施和其他公共機構進行邊界維修。

預計到2031年,能源電力產業將以6.2%的複合年成長率成長,成為英國圍籬市場成長最快的終端用戶領域。其主要推動要素是可再生能源,尤其是公用事業規模的太陽能發電,而非新建傳統發電廠。克利夫山太陽能發電場的案例(作為用戶回饋)表明,一個大型項目可能需要數公里長的周界圍欄,而此類設施對圍欄的規格要求高於標準農業應用。採礦、石油和化學工業的需求相對穩定,因為這些產業更依賴現有資產的維護,而非新建設施的建設熱潮。即使銷售量成長較為溫和,但由於營運商需要在危險環境和高安全等級要求的場所使用具備整合門禁控制功能的認證周界圍籬解決方案,因此市場價值依然存在。這意味著,在那些技術合規性優先於單純銷售量的領域,英國圍欄產業的價值成長最為強勁。這也表明,英國圍欄產業正受到那些既需要產品知識又需要安裝人員具備更嚴格專案執行標準的應用領域的推動。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 疫情後住宅維修活動的活性化,也帶動了住宅圍籬安裝量的上升。

- 政府資助的周邊安全升級計畫正在推動對關鍵基礎設施周圍圍欄的需求。

- 基礎設施維修項目推動了對老舊圍欄系統更換的需求。

- 住宅和商業領域對環保複合材料圍籬的需求都在不斷成長。

- 隨著太陽能發電廠的擴張,公用事業規模的圍欄安裝量也增加。

- 整合智慧感測器的圍欄正被廣泛應用於高階安全監控領域。

- 市場限制因素

- 鋼材和木材價格的波動給圍籬建造公司的利潤率帶來了壓力。

- 由於文化遺產和自然保護區的建築許可審查程序嚴格,圍欄安裝工程被延誤了。

- 英國整個建設產業人手不足,限制了圍欄的安裝能力。

- 智慧圍欄較高的初始成本阻礙了中小企業採用這項技術。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 價格分析

- 永續性和環保材料的發展趨勢

- 邊防安全框架與部署趨勢

第5章 市場規模與成長預測

- 材料

- 金屬

- 鋼

- 鋁

- 樹

- 塑膠和複合材料

- 具體的

- 其他材料

- 金屬

- 最終用戶

- 住宅

- 農業

- 軍事/國防

- 政府

- 礦業

- 石油/化工

- 能源與電力

- 其他最終用戶

- 按安裝類型

- 固定/永久圍欄

- 臨時/攜帶式圍欄

- 透過安裝通道

- 專家

- 其他 - 製造商、DIY/模組化套件

- 按地區

- 英格蘭

- 蘇格蘭

- 威爾斯

- 北愛爾蘭

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Bekaert

- Betafence

- Jacksons Fencing

- CLD Fencing Systems

- Hill & Smith Holdings

- IAE Fencing

- Zaun Limited

- Heras UK

- Fence Group

- Barkers Fencing

- Steelway Fensecure

- Alpha Rail

- Borderland Fencing

- Hadley Group

- Quickfencer

- KDM Timber

- Timber Focus

- Dura Composites

- Fencewise

- Gripple Ltd

第7章 市場機會與未來展望

According to Mordor Intelligence, the united kingdom fencing market size is expected to increase from USD 0.92 billion in 2025 to USD 0.96 billion in 2026 and reach USD 1.19 billion by 2031, growing at a CAGR of 4.40% over 2026-2031.

This report is Segmented by Material (Metal, Wood, Plastic & Composite, Concrete, and Other Materials), End-User (Residential, Agricultural, and More), Installation Type (Fixed / Permanent Fencing, Temporary / Mobile Fencing), Installation Channel (Professional Contractor and Others), and Geography (England, Scotland, Wales, and Northern Ireland). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Fencing Market Trends and Insights

Government-Funded Perimeter Security Upgrades Boost Fencing Demand at Critical Infrastructure Sites

The Spending Review 2025 committed at least GBP 100 million (USD 127 million) per year by 2028-2029 through the Integrated Security Fund and raised defense capital budgets from GBP 23.2 billion (USD 29.5 billion) in 2025-2026 to GBP 33.2 billion (USD 42.2 billion) by 2029-2030, while military accommodation renewal alone received GBP 7 billion (USD 8.9 billion). That spending base matters for the United Kingdom's fencing market because perimeter systems sit within defense, prison, transport, and critical infrastructure budgets rather than relying solely on stand-alone fence replacement cycles. The same review also allocated GBP 7 billion (USD 8.9 billion) for 14,000 new prison places by 2031, which supports multi-year demand for high-specification perimeter fencing and access control around custodial sites. The June 2025 National Security Strategy made protection of critical national infrastructure a formal priority, and that is pushing procurement toward rated systems rather than lower-end perimeter products. Hill & Smith stated in its 2025 full-year results that data center demand was an important driver of perimeter security revenue, which shows that digital infrastructure is becoming a major buyer of higher-value fencing systems. This is raising specification levels across the United Kingdom fencing market and shifting value toward suppliers that can meet premium security standards with tested products and approved installation capabilities.

Post-Pandemic Home Improvement Activity Increases Residential Fencing Installations

Private housing repair and maintenance activity strengthened during 2025 and continues to support demand in 2026, sustaining replacement and upgrade requirements for boundary products within the residential segment of the United Kingdom fencing market. Residential demand remains significant due to the country's large and aging housing stock, which drives recurring fence replacement needs even during periods of slower new housing construction. Demand growth is influenced not only by installation activity but also by homeowners increasingly favoring higher-quality, longer-warranty products over basic entry-level fencing solutions. This trend is reflected in supplier strategies, as manufacturers introduced extended-life timber and hybrid-composite product ranges during 2024 and 2025 to capture ongoing upgrade spending. As a result, revenue generated per project in the United Kingdom fencing market can increase even when overall installation volumes grow at a more moderate pace. The continued importance of the residential segment also underscores its role in shaping competitive positioning, despite the growing attention to institutional security and infrastructure-related fencing projects.

Volatile Steel and Timber Prices Pressure Fencing Contractor Profit Margins

Input-cost volatility remains a key restraint for the United Kingdom fencing market in 2026, as many projects are awarded under fixed-price contracts while material costs can fluctuate throughout the delivery period. During 2025, Timber Development UK (TDUK) reported significant timber price movements, with its timber price index rising from 107 at the beginning of 2025 to 130 by mid-2025, before easing to 125 in the third quarter of 2025 and recording a further 5% correction during the fourth quarter of 2025 as supply conditions improved. Although timber prices moderated toward the end of 2025, the volatility experienced throughout the year continues to influence purchasing and bidding decisions in 2026. This challenge is particularly relevant in the United Kingdom fencing market, where smaller contractors may be reluctant to participate in public tenders when future material costs are uncertain, reducing bidding depth and potentially delaying contract awards. Cost fluctuations also favor integrated manufacturers that can manage supply chains, maintain inventory, or diversify exposure across timber, steel, and composite fencing products. Over time, this dynamic may support market-share gains for larger operators, even as overall demand conditions remain healthy in 2026.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Refurbishment Projects Drive Replacement Demand for Aging Fencing Systems

- Expansion of Solar Farms Increases Utility-Scale Fencing Installations

- Labor Shortages Across the United Kingdom Construction Sector Constrain Fencing Installation Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal accounted for 46% of revenue in 2025, making it the largest material category in the United Kingdom fencing market. That leadership rested on its strong position in security, perimeter protection, transport, utilities, and other applications where rated mesh, steel palisade, and durable boundary systems are standard requirements. Steel held the larger share of the metal market, while aluminum gained ground in residential and commercial settings because it combines corrosion resistance with lower lifetime maintenance costs. Metal also retained a clear edge in projects where tested security performance and structural durability mattered more than visual style. In that sense, metal continued to anchor the core of the United Kingdom fencing market, even as other materials gained in appeal.

Plastics & composites are forecast to grow at a 5.5% CAGR through 2031, making it the fastest-growing material group. The segment is benefiting from stronger sustainability requirements and from demand for products that reduce ongoing maintenance in residential and commercial projects. Supplier documentation in 2025 showed recycled-content composite systems with 15- to 25-year warranties, sharpening the cost comparison with treated timber over the product life. Wood still holds an important place in residential and agricultural fencing, but it is under pressure from higher maintenance requirements and customer interest in longer-lasting alternatives. Concrete also plays a role in boundary walls and noise-barrier applications, especially near road and rail corridors undergoing refurbishment. The Forest Research Timber in Construction Roadmap still points to policy and procurement support for wood in broader building applications, which could help wood fencing volumes where local specifications remain favorable. Even so, the United Kingdom fencing market is seeing a material growth shift toward products that offer lower upkeep and stronger sustainability positioning.

Residential accounted for 38% of revenue in 2025, making it the largest end-user segment in the United Kingdom fencing market. That scale reflects the country's broad housing base and the continued need for fence replacement, repair, and garden upgrades across existing homes. Demand is spread across all 4 nations, so the segment is not tied to one capital spending cluster or a single institutional budget cycle. Agricultural demand remained another major driver of the United Kingdom fencing market, as rural land management and livestock containment continue to require regular boundary maintenance. Military, defense, and government demand also accelerated as public spending programs lifted perimeter upgrades at prisons, military sites, and other institutional locations.

Energy & power is projected to grow at a 6.2% CAGR through 2031, which makes it the fastest-growing end-user segment in the United Kingdom fencing market. The main driver is renewable energy, especially utility-scale solar, rather than new conventional power build-out. The Cleve Hill Solar Farm example in the user input showed that a single large project can require several kilometers of perimeter fencing, and that such a site requires a higher specification than standard agricultural use. Mining, petroleum, and chemicals demand remains steadier because it depends more on existing asset maintenance than on a wave of new sites. Even when volume growth is modest, hazardous and high-security environments still support value because operators need rated perimeter solutions with integrated access control. This means the United Kingdom fencing industry is seeing some of its strongest value expansion where technical compliance matters more than simple volume. It also means the United Kingdom fencing industry is being pulled toward applications where installers need both product knowledge and tighter project execution standards.

Complete Report Scope:

- By Material

- Metal

- Steel

- Aluminium

- Wood

- Plastic & Composite

- Concrete

- Other Materials

- Metal

- By End-User

- Residential

- Agricultural

- Military & Defense

- Government

- Mining

- Petroleum & Chemicals

- Energy & Power

- Other End-Users

- By Installation Type

- Fixed / Permanent Fencing

- Temporary / Mobile Fencing

- By Installation Channel

- Professional Contractor

- Others - Fabricators, DIY / Modular Kits

- By Geography

- England

- Scotland

- Wales

- Northern Ireland

List of Companies Covered in this Report:

- Bekaert

- Betafence

- Jacksons Fencing

- CLD Fencing Systems

- Hill & Smith Holdings

- IAE Fencing

- Zaun Limited

- Heras UK

- Fence Group

- Barkers Fencing

- Steelway Fensecure

- Alpha Rail

- Borderland Fencing

- Hadley Group

- Quickfencer

- KDM Timber

- Timber Focus

- Dura Composites

- Fencewise

- Gripple Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-Pandemic Home Improvement Activity Increases Residential Fencing Installations

- 4.2.2 Government-Funded Perimeter Security Upgrades Boost Fencing Demand at Critical Infrastructure Sites

- 4.2.3 Infrastructure Refurbishment Projects Drive Replacement Demand for Aging Fencing Systems

- 4.2.4 Demand for Eco-Friendly Composite Fencing Rises Across Residential and Commercial Sectors

- 4.2.5 Expansion of Solar Farms Increases Utility-Scale Fencing Installations

- 4.2.6 Smart Sensor-Integrated Fencing Adoption Grows for Advanced Security Monitoring Applications

- 4.3 Market Restraints

- 4.3.1 Volatile Steel and Timber Prices Pressure Fencing Contractor Profit Margins

- 4.3.2 Strict Planning Permissions in Heritage and Conservation Zones Delay Fencing Projects

- 4.3.3 Labor Shortages Across the United Kingdom Construction Sector Constrain Fencing Installation Capacity

- 4.3.4 High Upfront Costs of Smart Fencing Limit Adoption Among SMEs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Sustainability & Eco-Friendly Material Trends

- 4.10 Border Security Framework & Deployment Trends

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Metal

- 5.1.1.1 Steel

- 5.1.1.2 Aluminium

- 5.1.2 Wood

- 5.1.3 Plastic & Composite

- 5.1.4 Concrete

- 5.1.5 Other Materials

- 5.1.1 Metal

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Agricultural

- 5.2.3 Military & Defense

- 5.2.4 Government

- 5.2.5 Mining

- 5.2.6 Petroleum & Chemicals

- 5.2.7 Energy & Power

- 5.2.8 Other End-Users

- 5.3 By Installation Type

- 5.3.1 Fixed / Permanent Fencing

- 5.3.2 Temporary / Mobile Fencing

- 5.4 By Installation Channel

- 5.4.1 Professional Contractor

- 5.4.2 Others - Fabricators, DIY / Modular Kits

- 5.5 By Geography

- 5.5.1 England

- 5.5.2 Scotland

- 5.5.3 Wales

- 5.5.4 Northern Ireland

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Bekaert

- 6.4.2 Betafence

- 6.4.3 Jacksons Fencing

- 6.4.4 CLD Fencing Systems

- 6.4.5 Hill & Smith Holdings

- 6.4.6 IAE Fencing

- 6.4.7 Zaun Limited

- 6.4.8 Heras UK

- 6.4.9 Fence Group

- 6.4.10 Barkers Fencing

- 6.4.11 Steelway Fensecure

- 6.4.12 Alpha Rail

- 6.4.13 Borderland Fencing

- 6.4.14 Hadley Group

- 6.4.15 Quickfencer

- 6.4.16 KDM Timber

- 6.4.17 Timber Focus

- 6.4.18 Dura Composites

- 6.4.19 Fencewise

- 6.4.20 Gripple Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2026-2034年全球水產養殖網箱市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球水產養殖網箱市場規模、佔有率、趨勢和成長分析報告 美國圍欄:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)德國圍籬市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼圍籬市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)印度圍籬市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

美國圍欄:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)德國圍籬市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼圍籬市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)印度圍籬市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 木質圍籬市場規模、佔有率和成長分析:按樹種、圍籬樣式、應用、銷售管道和地區分類-2026-2033年產業預測

木質圍籬市場規模、佔有率和成長分析:按樹種、圍籬樣式、應用、銷售管道和地區分類-2026-2033年產業預測 美國圍欄市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測(2026-2033 年)

美國圍欄市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測(2026-2033 年) 圍籬市場:2026-2032年全球市場預測(依產品類型、材質、功能、高度、安裝方式、銷售管道及應用分類)

圍籬市場:2026-2032年全球市場預測(依產品類型、材質、功能、高度、安裝方式、銷售管道及應用分類) 圍欄市場:按類型、應用和地區分類

圍欄市場:按類型、應用和地區分類 2026年全球圍籬市場報告

2026年全球圍籬市場報告