|

市場調查報告書

商品編碼

2072876

美國圍欄:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Fencing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

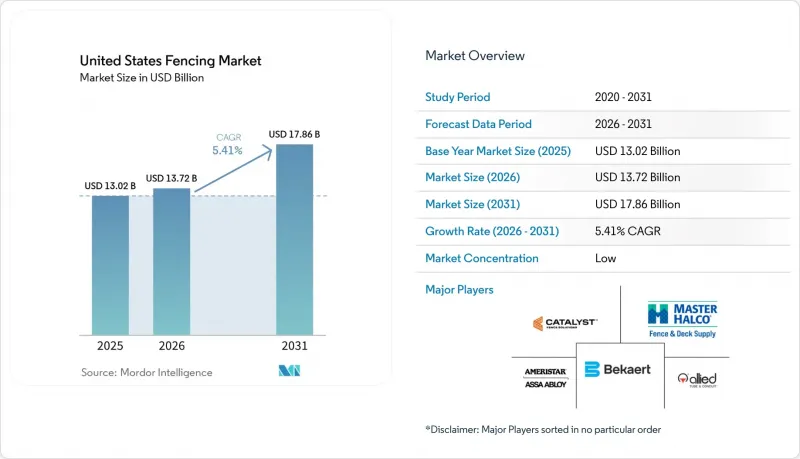

根據 Mordor Intelligence 預測,美國圍籬市場規模將從 2025 年的 130.2 億美元成長到 2026 年的 137.2 億美元,然後在 2031 年達到 178.6 億美元,2026 年至 2031 年的複合年成長率為 5.41%。

本報告按材料(金屬、木材、塑膠/複合材料、混凝土及其他)、最終用戶(住宅、農業、軍事/國防及其他)、安裝類型(固定/永久性、臨時/可移動式)、安裝管道(專業承包商、製造商/DIY)以及州(德克薩斯州、加利福尼亞州、佛羅裡達州、紐約州、伊利諾伊州及其他美國州)進行分類。預測值以美元計價。

美國圍欄市場的趨勢和洞察

郊區住宅開發案對住宅隱私和安全圍欄的需求日益成長。

美國陽光地帶各州郊區的發展為住宅圍欄創造了強勁的需求基礎。在達拉斯-沃斯堡、鳳凰城和坦帕等地區的新獨棟住宅項目中,圍欄擴大被列為標準配置,而非可選附加項目。此外,混合型工程的興起也提高了人們對後院利用的興趣,從而帶動了現有住宅的新安裝和更換需求。在許多項目中,長期維護的重要性超過了初始購買價格,這促使住宅轉向乙烯基、複合材料和粉末塗層鋁製產品。此外,快速發展社區的住宅協會的規章制度也鼓勵購屋者選擇經批准的設計和認證的供應商,這有助於提高安裝工程的價值並維持穩定的利潤率。

商業和工業建築的成長推動了周界安全圍欄的引入。

在美國圍籬市場,訂單商業和工業建築的訂單量將持續支撐周界安防需求,直至2026年。物流設施、資料中心、能源資產和製造工廠都需要比標準住宅系統更安全的圍欄。這推動了非住宅項目對防攀爬鋼板、焊接網、抗衝擊屏障和整合門禁系統的需求。太陽能發電廠、儲能設施和電動車充電站進一步增加了特定場所的周界安防需求,尤其是在業主既需要物理防護又需要門禁控制的情況下。隨著專案範圍日益複雜,圍欄供應商被迫提供整合屏障、網路基地台和監控功能的捆綁式產品。

高昂的人事費用和安裝成本推高了圍欄工程的總成本。

在美國,勞動力短缺仍然是圍欄市場面臨的一項重大營運挑戰。圍籬安裝,尤其是永久性圍籬系統,高度依賴熟練工人進行立柱安裝、校準、大門安裝和收尾工作。熟練工人的短缺迫使承包商延長工期並提高人事費用,從而競標高了住宅、商業和農業領域的專案總成本。這些成本壓力促使人們對模組化面板和預組裝大門單元的興趣日益濃厚,因為這些產品可以減少現場施工時間。這也推動了產業整合,使擁有更多可用勞動力的大型承包商能夠承接小規模本地企業難以招到人手的專案。

細分市場分析

到2025年,金屬圍欄將佔據美國圍欄市場45.1%的佔有率,並繼續保持其在所有材料類別中的領先地位。這一主導地位反映了工業邊界、軍事和政府應用領域的強勁需求,在這些領域,強度、抗攀爬性和抗衝擊性比裝飾性更為重要。雖然鋼材仍然是農業和工業應用領域的主流材料,但鋁材在住宅和小規模商業項目中越來越受歡迎,因為這些項目需要維護成本更低、外觀更精緻的材料。塑膠和複合材料圍籬是成長最快的材料類別,預計到2031年將以6.21%的複合年成長率成長,因為越來越多的買家轉向選擇生命週期維護成本較低的材料。

複合材料供應商正憑藉其產品的耐用性和高階定位,不斷擴大在美國圍欄行業的市場佔有率。在2026年國際建築商展上,Trex重點展示了其戶外生活產品系列,並重申了其複合材料產品的長壽命特性,強調了複合材料圍欄在高檔住宅項目中的吸引力。由於木材的初始成本相對較低,且許多住宅可以相對輕鬆地自行安裝,因此在低預算住宅和鄉村項目中仍然佔據一定地位。混凝土仍然是隔音屏障和高安全性邊界圍欄等應用領域的小眾選擇。相較之下,再生聚合物網和竹子等其他材料仍局限於小規模、永續性的市場。該領域的主要變化並非金屬的消失,而是市場正穩步轉向高階產品,例如塗層產品、複合材料和長壽命產品。

到2025年,住宅用戶將占美國圍籬市場38.7%的佔有率,成為最大的住宅群。這反映了單戶住宅買賣、郊區建設、為提升隱私而進行的房屋維修以及後院改造支出之間的直接關聯。許多新住宅在購屋後立即安裝圍欄,而現有住戶則繼續將老舊圍欄作為戶外維修計畫的一部分進行更換。農業圍籬是成長最快的終端使用者群體,預計到2031年將以6.34%的複合年成長率成長,這主要得益於與環境保護相關的安裝支援以及大型畜牧場中智慧電圍欄的普及。

農業領域日益成長的需求意義重大,因為它將美國圍籬市場拓展到主導需求之外。根據美國農業部報告顯示,到2024年,牛的數量將達到9,440萬頭,這意味著畜牧場將廣泛使用圍欄,並且對維修和更換的需求也將持續存在。軍方和國防用戶仍然是重要的高階買家,他們需要抗衝擊屏障、更高的防攀爬面板以及整合監控系統。政府、礦業、石油化工以及能源電力用戶也構成了另一層不可或缺的需求,因為在這些領域,圍籬直接關係到安全和資產保護,而非美觀。與依賴單一建築業的市場相比,如此廣泛的終端用戶群有助於美國圍欄行業保持更強的韌性。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場趨勢與分析

- 市場概覽

- 市場促進因素

- 郊區住宅開發案對住宅隱私和安全圍欄的需求日益成長。

- 商業和工業建築的成長推動了周邊安全圍欄的普及。

- 先進安防應用領域對自動化和智慧圍欄系統的需求日益成長。

- 來自鄰國的跨境移民增加,推動了對邊防安全圍欄基礎設施的需求。

- 畜牧管理和土地保護對農業圍籬的需求日益成長。

- 人們越來越關注野生動物保護和公路安全,這推動了野生動物圍欄的安裝。

- 市場限制因素

- 人事費用和安裝成本的上漲增加了圍欄建設的總成本。

- 鋼鐵、鋁和木材等原物料價格的波動正在影響產品成本。

- 嚴格的區域分類法和地方政府法規限制在特定區域安裝圍欄。

- 價值供應鏈分析

- 監理情勢

- 科技與創新趨勢

- 波特五力模型

- 定價分析

- 永續性和環保材料的發展趨勢

- 邊防安全框架與實施趨勢

第5章 市場規模與成長預測

- 材料

- 金屬

- 鋼

- 鋁

- 木頭

- 塑膠和複合材料

- 具體的

- 其他

- 金屬

- 最終用戶

- 住宅

- 農業

- 軍事/國防

- 政府

- 礦業

- 石油/化工

- 能源與電力

- 其他

- 按安裝類型

- 固定/永久型

- 臨時/可移動的

- 透過安裝通道

- 專家

- 其他 - 製造商、DIY/模組化套件

- 按州

- 德克薩斯州

- 加州

- 佛羅裡達

- 紐約

- 伊利諾州

- 其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Catalyst Fence Solutions

- Master Halco

- Ameristar Perimeter Security

- Bekaert Fencing

- Allied Tube & Conduit

- Fortress Building Products

- Merchants Metals

- Gregory Industries

- Eastern Wholesale Fence

- SpecRail

- Long Fence

- Stephens Pipe & Steel

- Ultra Aluminum Mfg.

- Jamieson Fence Supply

- Jerith Manufacturing LLC

- Ametco Manufacturing

- Pexco LLC(PDS Fence Products)

- Wheatland Tube

- Sharon Fence

- Ply Gem Residential Solutions

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states fencing market size is expected to grow from USD 13.02 billion in 2025 to USD 13.72 billion in 2026 and is forecast to reach USD 17.86 billion by 2031 at 5.41% CAGR over 2026-2031.

This report is Segmented by Material (Metal, Wood, Plastic & Composite, Concrete, Others), by End-User (Residential, Agricultural, Military & Defense, and More), by Installation Type (Fixed/Permanent, Temporary/Mobile), by Installation Channel (Professional Contractor, Fabricators/DIY), and by State (Texas, California, Florida, New York, Illinois, Rest of US). Forecasts are in Value (USD)

United States Fencing Market Trends and Insights

Increasing Demand for Residential Privacy and Security Fencing Across Suburban Housing Developments

Suburban growth across Sun Belt states has created a durable base of demand for residential fencing in the United States. New single-family communities in areas such as Dallas-Fort Worth, Phoenix, and Tampa often include fencing as standard with the property rather than an optional add-on. Hybrid work patterns have also kept attention on backyard use, which supports both first-time installations and replacement demand in established neighborhoods. Homeowners are moving toward vinyl, composite, and powder-coated aluminum because long-term upkeep matters more than initial purchase price in many projects. Homeowner association rules in fast-growing communities also steer buyers toward approved designs and certified suppliers, which supports higher-value installations and steadier margins.

Growth in Commercial and Industrial Construction Driving Perimeter Security Fencing Adoption

Commercial and industrial construction pipelines continued to support perimeter security demand entering 2026 in the United States fencing market. Logistics sites, data centers, energy assets, and manufacturing facilities all require fencing that can handle higher security standards than standard residential systems. This is lifting demand for anti-climb steel panels, welded mesh, crash-rated barriers, and integrated gate systems across nonresidential projects. Solar farms, battery storage locations, and electric vehicle charging sites are adding another layer of site-specific perimeter demand, especially where owners want both physical protection and controlled access. As project scopes become more complex, fencing suppliers are being pushed toward bundled products that combine barriers, access points, and monitoring features.

High Labor and Installation Costs Increasing Overall Fencing Project Expenses

Labor availability remains a major operating challenge across the United States fencing market. Fence installation still depends heavily on skilled crews for post setting, alignment, gate placement, and finish work, especially in permanent systems. When trained crews are scarce, installers can extend lead times and bid at higher labor rates, which pushes up total project costs across residential, commercial, and agricultural jobs. That cost pressure is encouraging more interest in modular panels and pre-assembled gate units that reduce on-site work time. It also supports consolidation, as larger contractors with better crew access can take on projects that smaller local firms may struggle to staff.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Automated and Smart Fencing Systems in High-Security Applications

- Increasing Cross-Border Migration from Neighboring Countries Driving Demand for Border Security Fencing Infrastructure

- Fluctuating Prices of Raw Materials Such as Steel, Aluminum, and Wood Impacting Product Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal fencing held 45.1% of the United States fencing market share in 2025, maintaining its leading position across material categories. That lead reflects strong demand from industrial perimeter, military, and government applications where strength, anti-climb performance, and crash resistance carry more weight than decorative value. Steel remains the primary material for agricultural and industrial work, while aluminum is more commonly used in residential and light commercial projects that require lower maintenance and cleaner finishes. Plastic and composite fencing is the fastest-growing material segment, with a projected 6.21% CAGR through 2031, as more buyers move away from wood toward materials with lower lifecycle maintenance costs.

Composite suppliers are using product longevity and premium positioning to widen their role in the United States fencing industry. Trex highlighted its outdoor living portfolio and reinforced the long-life positioning of composite products at the 2026 International Builders' Show, which supports the appeal of composite fencing in higher-value residential projects. Wood still holds a place in budget residential and rural installations because its upfront cost stays lower, and many homeowners can handle simpler installation work themselves. Concrete remains a niche option for applications such as noise barriers and high-security perimeters. In contrast, other materials, such as recycled polymer mesh and bamboo, remain limited to small, sustainability-focused pockets. The main change in this segment is not the disappearance of metal, but rather the steady shift in premium toward coated, composite, and longer-life products.

Residential end users accounted for 38.7% of the United States fencing market in 2025, making housing-related demand the largest end-use segment. This position reflects the direct link between single-family housing turnover, suburban construction, privacy upgrades, and backyard improvement spending. Many new homeowners install fencing soon after purchase, while established households continue to replace aging systems as part of outdoor renovation programs. Agricultural fencing is the fastest-growing end-use segment, with a 6.34% CAGR through 2031, supported by conservation-linked installation support and by wider use of smart electric fencing across large-acreage livestock operations.

The agricultural push matters because it broadens the United States fencing market beyond consumer-led demand. The U.S. Department of Agriculture reported a cattle inventory of 94.4 million head in 2024, indicating a large installed base of fencing across livestock operations and a recurring need for repair and replacement. Military and defense users remain important premium buyers because they require crash-rated barriers, taller anti-climb panels, and integrated monitoring systems. Government, mining, petroleum and chemicals, and energy and power users add another layer of non-discretionary demand because fencing in those settings is tied to safety and asset protection rather than appearance. This spread of end users helps the United States fencing industry remain more resilient than markets tied to a single construction category.

Complete Report Scope:

- By Material

- Metal

- Steel

- Aluminium

- Wood

- Plastic & Composite

- Concrete

- Other Materials

- Metal

- By End-User

- Residential

- Agricultural

- Military & Defense

- Government

- Mining

- Petroleum & Chemicals

- Energy & Power

- Other End-Users

- By Installation Type

- Fixed / Permanent Fencing

- Temporary / Mobile Fencing

- By Installation Channel

- Professional Contractor

- Others - Fabricators, DIY / Modular Kits

- By State

- Texas

- California

- Florida

- New York

- Illinois

- Rest of US

List of Companies Covered in this Report:

- Catalyst Fence Solutions

- Master Halco

- Ameristar Perimeter Security

- Bekaert Fencing

- Allied Tube & Conduit

- Fortress Building Products

- Merchants Metals

- Gregory Industries

- Eastern Wholesale Fence

- SpecRail

- Long Fence

- Stephens Pipe & Steel

- Ultra Aluminum Mfg.

- Jamieson Fence Supply

- Jerith Manufacturing LLC

- Ametco Manufacturing

- Pexco LLC (PDS Fence Products)

- Wheatland Tube

- Sharon Fence

- Ply Gem Residential Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing demand for residential privacy and security fencing across suburban housing developments

- 4.2.2 Growth in commercial and industrial construction driving perimeter security fencing adoption

- 4.2.3 Rising demand for automated and smart fencing systems in high-security applications

- 4.2.4 Increasing cross-border migration from neighboring countries driving demand for border security fencing infrastructure

- 4.2.5 Growing agricultural fencing needs for livestock management and land protection

- 4.2.6 Increasing focus on wildlife conservation and highway safety driving installation of wildlife fencing

- 4.3 Market Restraints

- 4.3.1 High labor and installation costs increasing overall fencing project expenses

- 4.3.2 Fluctuating prices of raw materials such as steel, aluminum, and wood impacting product costs

- 4.3.3 Strict zoning laws and local regulations limiting fencing installations in certain areas

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology & Innovation Trends

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Sustainability & Eco-Friendly Material Trends

- 4.10 Border Security Framework & Deployment Trends

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Metal

- 5.1.1.1 Steel

- 5.1.1.2 Aluminium

- 5.1.2 Wood

- 5.1.3 Plastic & Composite

- 5.1.4 Concrete

- 5.1.5 Other Materials

- 5.1.1 Metal

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Agricultural

- 5.2.3 Military & Defense

- 5.2.4 Government

- 5.2.5 Mining

- 5.2.6 Petroleum & Chemicals

- 5.2.7 Energy & Power

- 5.2.8 Other End-Users

- 5.3 By Installation Type

- 5.3.1 Fixed / Permanent Fencing

- 5.3.2 Temporary / Mobile Fencing

- 5.4 By Installation Channel

- 5.4.1 Professional Contractor

- 5.4.2 Others - Fabricators, DIY / Modular Kits

- 5.5 By State

- 5.5.1 Texas

- 5.5.2 California

- 5.5.3 Florida

- 5.5.4 New York

- 5.5.5 Illinois

- 5.5.6 Rest of US

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Catalyst Fence Solutions

- 6.4.2 Master Halco

- 6.4.3 Ameristar Perimeter Security

- 6.4.4 Bekaert Fencing

- 6.4.5 Allied Tube & Conduit

- 6.4.6 Fortress Building Products

- 6.4.7 Merchants Metals

- 6.4.8 Gregory Industries

- 6.4.9 Eastern Wholesale Fence

- 6.4.10 SpecRail

- 6.4.11 Long Fence

- 6.4.12 Stephens Pipe & Steel

- 6.4.13 Ultra Aluminum Mfg.

- 6.4.14 Jamieson Fence Supply

- 6.4.15 Jerith Manufacturing LLC

- 6.4.16 Ametco Manufacturing

- 6.4.17 Pexco LLC (PDS Fence Products)

- 6.4.18 Wheatland Tube

- 6.4.19 Sharon Fence

- 6.4.20 Ply Gem Residential Solutions

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2026-2034年全球水產養殖網箱市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球水產養殖網箱市場規模、佔有率、趨勢和成長分析報告 英國圍籬市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031)德國圍籬市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼圍籬市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)印度圍籬市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

英國圍籬市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031)德國圍籬市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼圍籬市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)印度圍籬市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 木質圍籬市場規模、佔有率和成長分析:按樹種、圍籬樣式、應用、銷售管道和地區分類-2026-2033年產業預測

木質圍籬市場規模、佔有率和成長分析:按樹種、圍籬樣式、應用、銷售管道和地區分類-2026-2033年產業預測 美國圍欄市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測(2026-2033 年)

美國圍欄市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測(2026-2033 年) 圍籬市場:2026-2032年全球市場預測(依產品類型、材質、功能、高度、安裝方式、銷售管道及應用分類)

圍籬市場:2026-2032年全球市場預測(依產品類型、材質、功能、高度、安裝方式、銷售管道及應用分類) 圍欄市場:按類型、應用和地區分類

圍欄市場:按類型、應用和地區分類 2026年全球圍籬市場報告

2026年全球圍籬市場報告