|

市場調查報告書

商品編碼

2064541

德國圍籬市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Germany Fencing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

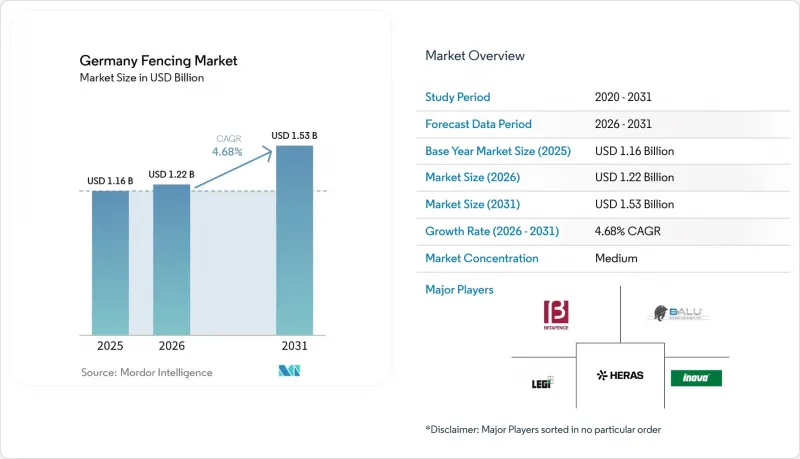

根據 Mordor Intelligence 預測,德國圍欄市場規模預計將在 2025 年達到 11.6 億美元,2026 年達到 12.2 億美元,到 2031 年達到 15.3 億美元,2026 年至 2031 年的複合年成長率為 4.68%。

本報告按材料(金屬、木材、塑膠/複合材料、其他)、最終用戶(住宅、農業、軍事/國防、其他)、安裝方式(固定/永久性圍欄、臨時/可移動圍欄)、安裝管道(專業承包商、其他)和地區(柏林、法蘭克福、其他)進行細分。市場預測以美元計價。

德國圍籬市場的趨勢與洞察

建築和基礎設施發展的成長

德國圍欄市場與建築週期密切相關,因為所有在建項目在施工期間都需要臨時圍欄,並在竣工交付時需要永久邊界系統。 2025年,德國建築訂單實際成長6.8%,這是自2021年以來的首次成長。名目訂單達1,130億歐元(1,290億美元),擴大了需要規範圍籬解決方案的在建工程規模。德國經濟研究所(DIW Berlin)預測,2026年建築總量將進一步成長,其中土木工程預計將呈現最強勁的成長勢頭,因為基礎設施投資正轉向鐵路、公路和橋樑。此外,2025年1月至11月期間,農業建築許可數量增加,這使得圍欄需求除了都市區和商業活動外,還擴展到農業設施和鄉村邊界計畫。在土木工程和商業項目進度超過住宅竣工速度的地區,德國圍籬市場受益最大。這是因為這些專案規模較大,涉及邊界保護需求,且對規範要求更為嚴格。

對安防和周界防護的需求日益成長

在德國圍籬市場,買家對圍籬的需求日益成長,他們現在不僅將邊界防護視為一項基本要求,更將其視為業務永續營運不可或缺的一部分。即使在聯邦政府於2024年9月擴大了德國陸地邊境的邊境管制之後,德國的安全態勢依然十分嚴格。根據聯邦警察(Bundespolizei)統計,2024年共發生83,572起非法入境事件。這意味著,實體安全仍然是公共採購和設施規劃的首要考量。這種影響如今已擴展到公共設施之外,資料中心和物流業者等商業用戶也開始採購具備防入侵和車輛碰撞緩解等功能的圍籬系統,而非普通的標準邊界產品。這種轉變提高了技術類別的價格彈性,有利於擁有廣泛認證的供應商,而基礎網狀產品和低規格產品則仍然面臨激烈的價格競爭。因此,在德國圍欄市場,對安全性的需求正在拉大性能導向供應商和銷售導向供應商之間的差距。

原物料價格波動

德國圍欄市場仍然受到原料成本波動的影響,因為鋼絲產品在許多永久性安防和工業圍欄系統中仍然佔據主導地位。自2021年以來,歐盟鋼鐵供應緊張,超過一半的歐洲初級鋼鐵運作能停產,這持續推高價格,並降低了製造商應對成本敏感型競標的柔軟性。隨著原料成本的上升,中等價位的供應商往往無法將增加的成本完全轉嫁給客戶,除非他們將訂單拱手讓給小規模的本地競爭對手。這使得在維持利潤率和確保產品品質之間難以權衡,尤其是在買家僅根據初始價格而非生命週期性能來比較提案時。在德國圍籬市場,這種限制因素在焊接網、基礎農業系統和標準金屬製品中最為明顯,不斷上漲的原料成本會迅速擠壓本已微薄的利潤空間。

細分市場分析

預計到2025年,木材將佔德國圍欄市場40%的佔有率,並繼續保持其在該國主要材料類別中的地位。這一地位得益於住宅和農業領域消費者對木材的高接受度。在這些領域,買家重視圍欄的熟悉外觀、豐富的款式選擇和便捷的安裝。德國擁有豐富的國內木材資源,這不僅保證了供應的透明度,也推動了包括花園圍欄、牧場圍欄和農場邊界圍欄在內的各種應用領域對木材的需求。

在德國圍籬市場,本地供應優勢使得高級產品應有盡有,而非侷限於狹窄的低成本細分市場。這也解釋了為何儘管其他材料因其安全性高、維護成本低而市場佔有率不斷成長,木材仍然是主流材料。樹種的多樣性提升了木材的永續性,使買家能夠根據預算和使用壽命需求,在經過處理的軟木和天然耐用的硬木之間進行選擇。像 ROBINIO 這樣的供應商,將其刺槐木產品定位為無需化學處理即可長期埋入地下,滿足了偏愛自然外觀的德國買家的需求。此外,FSC 認證的採購和永續性訊息在花園和牧場圍欄領域日益普及,這有助於木材在兼顧美觀和環保標準的應用中保持其吸引力。因此,在德國圍籬產業,木材並非一種日漸式微、過時的選擇,而是一種實用且具有文化底蘊的材料。雖然該細分市場的成長率不如金屬市場那麼高,但其良好的業績記錄和廣泛的應用範圍繼續支撐著德國整體圍欄市場的需求。

金屬是成長最快的材料類別,預計2026年至2031年德國圍籬市場金屬材料的市場規模將以5.6%的複合年成長率成長。對金屬材料的需求在需要防攀爬、更長使用壽命或與門禁和檢測系統相容的應用領域最為旺盛,這使得金屬成為能源設施、交通基礎設施、關鍵基礎設施和資料中心專案的核心材料。為了順應以效能為導向的採購趨勢,Praesidiad和Betafence已在其產品線中增加了經過認證的高安全性周界系統。在德國圍籬市場,鋼材仍然是主導金屬,焊接網、柵欄和軋延鋼絲系統涵蓋了廣泛的工業和公共應用。儘管鋁材的初始成本較高,但由於其輕質和耐腐蝕的特性,其生命週期價值得以提升,因此在住宅和小規模商業應用領域也獲得了越來越多的市場佔有率。塑膠和複合材料雖然與木材和金屬相比市場佔有率較小,但在隱私圍欄和模組化住宅系統中正穩步發展。複合材料填充物及相關系統正日益受到買家的青睞,他們希望降低維護成本,並在花園和邊界應用中實現更協調的外觀。雖然混凝土仍然是隔音屏障和某些基礎設施的特定選擇,但裝飾材料在特定的花園項目中發揮有限但穩定的作用。因此,德國圍欄行業並非轉向單一的替代材料,而是朝著更清晰的材料層級結構發展,由美觀、維護和安全需求決定。儘管木材仍保持領先地位,但這種層級結構最明顯地表明,在預測期內,金屬將在德國圍欄市場中超越其他材料。

到2025年,住宅領域將佔德國圍籬市場38%的佔有率,成為最大的終端用戶群。德國龐大的住宅存量、對花園和戶外生活空間隱私的高度重視以及圍欄產品廣泛的零售管道,都支撐了這一市場地位。 2025年,部分地區的住宅相關活動也有所改善,從而推動了對新型邊界圍欄、替換面板和模組化隱私系統的持續需求。住宅需求在德國圍籬市場尤其重要,因為其需求並非集中在少數合約買家手中,而是分散在各種材料類型、價格範圍和安裝管道中。這使得該細分市場對單一專案週期的依賴性降低,與更廣泛的家庭支出和小規模承包商的活動聯繫更為緊密。

此外,該領域受益於家居裝飾商店和建材供應管道強大的分銷網路,使一般家庭更容易比較產品和規劃項目。像Hornbach這樣的零售商不斷擴大其天然木材和模組化圍欄的產品範圍,這不僅滿足了更換需求,也促使人們逐漸從純粹的功能性邊界工程轉向有計劃的戶外維修。住宅買家既包括承包商主導的項目,也包括私人管理的項目,從而確保了德國圍欄市場透過多種管道實現穩定的銷售量。儘管全國範圍內的住宅完工率不均衡,但現有住宅存量的更換和維修需求依然強勁。因此,即使其他終端用戶的成長速度加快,住宅仍然是德國圍欄市場的結構性基礎。

農業用戶是第二大需求群體,因為圍欄不僅僅是視覺上的邊界,它還與牲畜管理、農場安全和土地分類密切相關。獸醫和農場保護方面的要求不斷提高,使得圍欄的安裝方式更加多樣化,佈局也比傳統的單圍欄農場更為複雜。這增加了每個項目的安裝距離,使圍欄成為營運必需品,而非可有可無的設備。德國圍欄市場正受益於此趨勢,因為農場訂單通常會將立柱、網子、門和電圍欄等組件捆綁在一個採購包中。這也帶動了大規模農村建設項目對承包商的需求,因為機械化安裝可以提高速度和統一性。能源和電力產業是成長最快的終端用戶群體,到2031年複合年成長率將達到6.3%,反映出德國圍欄市場對可再生能源和公共產業設施邊界保護的需求日益成長。這些設施需要保護設備、電纜線路、變電站區域和出入控制點,這提升了金屬和高安全性邊界系統的價值。在公共部門、軍事和政府設施領域,隨著關鍵基礎設施韌性建設的日益重要,以規範主導的項目正穩步湧現。採礦、石油化學和其他工業領域的買家對基礎更新的需求也推動了這一趨勢,但成長最顯著的領域顯然是能源相關項目。這種市場結構意味著,德國圍籬市場不再僅僅由家庭和農場的需求驅動,策略性基礎設施買家在市場成長中扮演越來越重要的角色。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 建築和基礎設施發展的成長

- 對安防和周界防護的需求日益成長

- 嚴格的安全標準和監管標準

- 智慧、低維護成本的圍欄解決方案正在被廣泛採用。

- 農業領域對防護的需求日益成長,推動了對農場和牲畜圍欄的需求。

- 對採用永續和可回收材料製成的圍欄的需求日益成長

- 市場限制因素

- 原物料價格波動

- 與非正規本地製造商的競爭會影響價格和產品品質。

- 農村和小規模買家對價格的敏感度阻礙了高檔圍欄的普及。

- 圍籬安裝技術純熟勞工短缺

- 價值鍊和供應鏈分析

- 監理情勢

- 科技與創新趨勢

- 波特五力分析

- 價格分析

- 永續發展和環保材料的發展趨勢

- 邊防安全框架與部署趨勢

第5章 市場規模與成長預測

- 材料

- 金屬

- 鋼

- 鋁

- 木頭

- 塑膠和複合材料

- 具體的

- 其他材料

- 金屬

- 最終用戶

- 住宅

- 農業

- 軍事/國防

- 政府

- 礦業

- 石油/化工

- 能源與電力

- 其他最終用戶

- 透過安裝方法

- 固定/永久圍欄

- 臨時/可移動圍欄

- 透過安裝通道

- 專家

- 其他(製造商、DIY/模組化套件)

- 按地區

- 柏林

- 法蘭克福

- 漢堡

- 慕尼黑

- 德國其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Betafence

- Heras

- LEGI Group

- Berlemann Torbau

- BALU Tore GmbH

- WISNIOWSKI

- Zaun Ltd

- Blaser Zaunsysteme GmbH

- A1 ZAUNDISCOUNT

- Heras Mobilzaun

- MY-Zaunsysteme

- GAVER Sichtschutz

- Praesidiad Group

- SchweiBgitter GmbH

- Bekaert

- DIRICKX Group

- CLD Physical Security Systems

- Jacksons Fencing

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany fencing market size is projected to be USD 1.16 billion in 2025, USD 1.22 billion in 2026, and reach USD 1.53 billion by 2031, growing at a CAGR of 4.68% from 2026 to 2031.

This report is Segmented by Material (Metal, Wood, Plastic & Composite, and More), End-User (Residential, Agricultural, Military & Defense, and More), Installation Type (Fixed / Permanent Fencing and Temporary / Mobile Fencing), Installation Channel (Professional Contractor and Others), and Geography (Berlin, Frankfurt, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Fencing Market Trends and Insights

Growth in Construction and Infrastructure Development

The Germany fencing market is closely tied to the construction cycle because every active project creates a need for temporary barriers during execution and permanent boundary systems at handover. German construction order intake grew 6.8% in real terms in 2025, which marked the first increase since 2021, and nominal orders reached EUR 113 billion (USD 129 billion), creating a broader base of live projects that require compliant fencing solutions. The German Institute for Economic Research (DIW Berlin) also expects overall construction volume to expand in 2026, with civil engineering showing the strongest momentum as infrastructure investment shifts to rail, road, and bridge work. Agricultural building permits also increased in the January to November 2025 period, which extends fencing demand into farm structures and rural perimeter projects alongside urban and commercial activity. The Germany fencing market benefits most where civil engineering and commercial work are improving faster than residential completions, because those project types carry larger and more specification-heavy perimeter needs.

Rising Demand for Security and Perimeter Protection

The Germany fencing market is seeing stronger demand from buyers that now treat perimeter protection as part of operational continuity rather than a simple boundary requirement. Germany's security posture remained elevated after federal authorities extended border controls across all German land borders from September 2024, and the Bundespolizei recorded 83,572 unauthorized entries in 2024, which kept physical security a visible priority in public procurement and facility planning. This effect now extends beyond public facilities, as commercial users such as data centers and logistics operators are buying fencing systems with forced-entry resistance and vehicle-mitigation features rather than standard perimeter products. That shift improves pricing resilience in technical categories and supports vendors with certification depth, while basic mesh and low-spec products remain exposed to price competition. In the Germany fencing market, security demand is therefore widening the gap between performance-led suppliers and volume-led suppliers.

Volatility in Raw Material Prices

The Germany fencing market remains exposed to input cost instability because steel wire products still sit at the center of many permanent security and industrial fencing systems. European Union (EU) steel supply conditions remained tight, with more than half of Europe's primary steel production capacity idled since 2021, which kept upward pressure on prices and reduced manufacturers' flexibility in responding to cost-sensitive tenders. When input costs move higher, suppliers in mid-range categories are often unable to pass through the full increase without losing orders to smaller local competitors. That creates a difficult trade-off between margin protection and product quality, especially where buyers compare offers on upfront price rather than lifecycle performance. In the German fencing market, this restraint is most visible in welded mesh, basic agricultural systems, and standard metal products, where input inflation can quickly narrow already modest margins.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Safety and Regulatory Standards

- Increasing Adoption of Smart and Low-Maintenance Fencing Solutions

- Competition from Unorganized Local Manufacturers is Affecting Pricing and Product Quality

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wood accounted for 40% of the Germany fencing market size in 2025, which kept it as the leading material category in the country. Its position rests on strong consumer acceptance in residential and agricultural settings, where buyers value familiar appearance, broad design choice, and ease of handling during installation. Germany also benefits from a large domestic timber base, which supports supply visibility and keeps wood relevant across garden fencing, paddock solutions, and farm boundaries.

In the Germany fencing market, that local supply advantage supports a wide mix of standard and premium products rather than a narrow low-cost niche. It also helps explain why wood remains established even as other materials gain share in higher-security or lower-maintenance uses. Species choice adds another layer to wood's staying power, allowing buyers to choose between treated softwood and naturally durable hardwood options, depending on budget and service-life needs. Suppliers such as ROBINIO position Robinia-based products as offering long-term in-ground durability without chemical treatment, which aligns with a segment of German buyers who prefer a more natural specification. FSC-linked sourcing and sustainability messaging have also become more visible in garden and paddock procurement, which helps wood retain appeal where aesthetics and environmental criteria both matter. In the Germany fencing industry, wood therefore continues to serve as a practical and culturally familiar material rather than a declining legacy choice. The segment's growth is slower than metal, but its installed base and broad use cases continue to anchor demand across the Germany fencing market.

Metal is the fastest-growing material segment, with the Germany fencing market size for metal projected to expand at a 5.6% CAGR between 2026 and 2031. Demand is strongest where sites require anti-climb performance, longer service life, or compatibility with access control and detection systems, making metal central to energy sites, transport facilities, critical infrastructure, and data center projects. Praesidiad and Betafence have expanded their portfolios to include certified high-security perimeter systems, reflecting this move toward performance-led procurement. Within the Germany fencing market, steel remains the main metal type because welded mesh, palisade formats, and rolled wire systems cover a wide range of industrial and public applications. Aluminum is also gaining ground in residential and light commercial applications, where lower weight and corrosion resistance support lifecycle value, even if the upfront cost is higher. Plastic and composite materials remain smaller than wood and metal, but they are building a firmer base in privacy fencing and modular residential systems. Composite infills and related systems appeal to buyers who want lower upkeep and a more uniform appearance across garden and boundary applications. Concrete remains a niche option for noise barriers and in selected infrastructure locations, while decorative materials play a limited but stable role in certain garden projects. The Germany fencing industry is therefore not shifting toward one replacement material, but toward a clearer material hierarchy shaped by aesthetics, upkeep, and security needs. That hierarchy keeps wood in the lead, but it gives metal the clearest path to outperformance through the forecast period in the Germany fencing market.

Residential held a 38% share of the Germany fencing market share in 2025, making it the largest end-user category. Germany's large housing stock, strong preference for privacy in gardens and outdoor living areas, and broad retail access to fencing products all support this position. Housing-related activity also improved in parts of the pipeline in 2025, helping maintain demand for new boundary fencing, replacement panels, and modular privacy systems. In the Germany fencing market, residential demand is especially important because it spreads orders across material types, price points, and installation channels rather than concentrating demand in a few contract buyers. That makes the segment less dependent on a single project cycle and more tied to a broad base of household spending and small-contractor activity.

The segment also benefits from strong distribution coverage across home improvement and building supply channels, making product comparison and project planning easier for households. Hornbach and other retailers continue to expand natural wood and modular fencing options, which support replacement demand and the gradual move toward planned outdoor upgrades rather than purely functional boundary work. Residential buyers span both contractor-led and self-managed projects, which keeps volume flowing through multiple sales routes in the Germany fencing market. Even with uneven residential completions at the national level, the installed housing base keeps replacement and modernization demand active. This is why residential remains the structural anchor for the Germany fencing market even while faster growth is coming from other end-users.

Agricultural users form the next important demand layer because fencing is tied to livestock management, farm security, and land separation rather than purely visual boundaries. Veterinary and farm protection requirements continue to support multi-line installations and more complex layouts than earlier single-fence farm formats. That raises per-project meterage and makes fencing an operating need rather than a discretionary one. The Germany fencing market gains from this because farm orders often combine posts, mesh, gates, and electrified elements in a single purchase set. It also supports contractor demand in larger rural jobs where mechanized installation improves speed and consistency. The energy & power is the fastest-growing end-user segment at a 6.3% CAGR through 2031, which reflects the rising perimeter needs of renewable energy and utility sites in the Germany fencing market. These sites need protection for equipment, cable routes, transformer areas, and controlled access points, which increases the value of metal and high-security perimeter systems. Public-sector, military, and government facilities also provide a steady stream of specification-led projects as critical infrastructure resilience moves further into implementation. Mining, petroleum and chemicals, and other industrial buyers add baseline replacement demand, but the strongest acceleration is clearly within energy-linked projects. This mix means the Germany fencing market is no longer driven only by household and farm demand, because strategic infrastructure buyers are taking a larger role in the growth profile.

List of Companies Covered in this Report:

- Betafence

- Heras

- LEGI Group

- Berlemann Torbau

- BALU Tore GmbH

- WISNIOWSKI

- Zaun Ltd

- Blaser Zaunsysteme GmbH

- A1 ZAUNDISCOUNT

- Heras Mobilzaun

- MY-Zaunsysteme

- GAVER Sichtschutz

- Praesidiad Group

- SchweiBgitter GmbH

- Bekaert

- DIRICKX Group

- CLD Physical Security Systems

- Jacksons Fencing

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Construction and Infrastructure Development

- 4.2.2 Rising Demand for Security and Perimeter Protection

- 4.2.3 Stringent Safety and Regulatory Standards

- 4.2.4 Increasing Adoption of Smart and Low-Maintenance Fencing Solutions

- 4.2.5 Increasing Agricultural Protection Needs Drive Demand for Farm and Livestock Fencing

- 4.2.6 Growing Preference for Sustainable and Recycled-Material Fencing

- 4.3 Market Restraints

- 4.3.1 Volatility in Raw Material Prices

- 4.3.2 Competition from Unorganized Local Manufacturers Affecting Pricing and Product Quality

- 4.3.3 Price Sensitivity among Rural and Small-Scale Buyers Limiting Premium Fencing Adoption

- 4.3.4 Shortage of Skilled Fencing Installation Labor

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology & Innovation Trends

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Sustainability & Eco-Friendly Material Trends

- 4.10 Border Security Framework & Deployment Trends

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Material

- 5.1.1 Metal

- 5.1.1.1 Steel

- 5.1.1.2 Aluminium

- 5.1.2 Wood

- 5.1.3 Plastic & Composite

- 5.1.4 Concrete

- 5.1.5 Other Materials

- 5.1.1 Metal

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Agricultural

- 5.2.3 Military & Defense

- 5.2.4 Government

- 5.2.5 Mining

- 5.2.6 Petroleum & Chemicals

- 5.2.7 Energy & Power

- 5.2.8 Other End-Users

- 5.3 By Installation Type

- 5.3.1 Fixed / Permanent Fencing

- 5.3.2 Temporary / Mobile Fencing

- 5.4 By Installation Channel

- 5.4.1 Professional Contractor

- 5.4.2 Others (Fabricators, DIY / Modular Kits)

- 5.5 By Geography

- 5.5.1 Berlin

- 5.5.2 Frankfurt

- 5.5.3 Hamburg

- 5.5.4 Munich

- 5.5.5 Rest of Germany

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Betafence

- 6.4.2 Heras

- 6.4.3 LEGI Group

- 6.4.4 Berlemann Torbau

- 6.4.5 BALU Tore GmbH

- 6.4.6 WISNIOWSKI

- 6.4.7 Zaun Ltd

- 6.4.8 Blaser Zaunsysteme GmbH

- 6.4.9 A1 ZAUNDISCOUNT

- 6.4.10 Heras Mobilzaun

- 6.4.11 MY-Zaunsysteme

- 6.4.12 GAVER Sichtschutz

- 6.4.13 Praesidiad Group

- 6.4.14 SchweiBgitter GmbH

- 6.4.15 Bekaert

- 6.4.16 DIRICKX Group

- 6.4.17 CLD Physical Security Systems

- 6.4.18 Jacksons Fencing

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2026-2034年全球水產養殖網箱市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球水產養殖網箱市場規模、佔有率、趨勢和成長分析報告 印尼圍籬市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)印度圍籬市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

印尼圍籬市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)印度圍籬市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 木質圍籬市場規模、佔有率和成長分析:按樹種、圍籬樣式、應用、銷售管道和地區分類-2026-2033年產業預測

木質圍籬市場規模、佔有率和成長分析:按樹種、圍籬樣式、應用、銷售管道和地區分類-2026-2033年產業預測 美國圍欄市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測(2026-2033 年)

美國圍欄市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測(2026-2033 年) 圍籬市場:2026-2032年全球市場預測(依產品類型、材質、功能、高度、安裝方式、銷售管道及應用分類)

圍籬市場:2026-2032年全球市場預測(依產品類型、材質、功能、高度、安裝方式、銷售管道及應用分類) 圍欄市場:按類型、應用和地區分類

圍欄市場:按類型、應用和地區分類 2026年全球圍籬市場報告2026年全球鋁製金屬圍籬市場報告動物籠具市場:2026-2032年全球市場預測(依動物種類、材料、籠具類型、最終用戶及通路分類)

2026年全球圍籬市場報告2026年全球鋁製金屬圍籬市場報告動物籠具市場:2026-2032年全球市場預測(依動物種類、材料、籠具類型、最終用戶及通路分類)