|

市場調查報告書

商品編碼

2063901

印度圍籬市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)India Fencing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

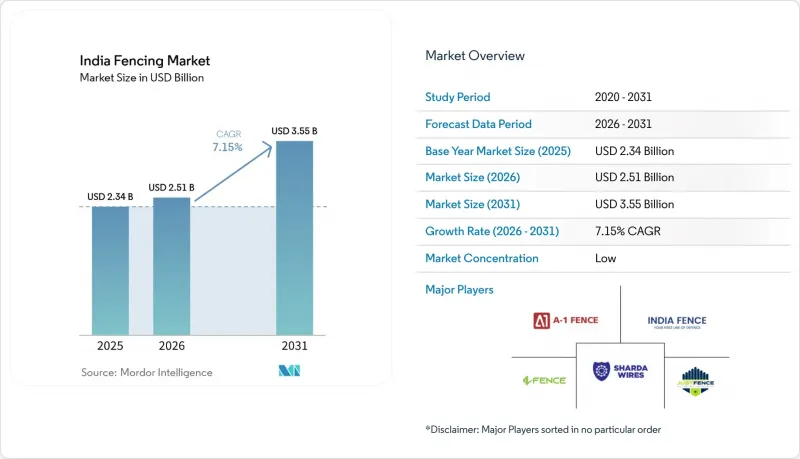

根據 Mordor Intelligence 預測,印度圍欄市場規模預計將在 2025 年達到 23.4 億美元,2026 年達到 25.1 億美元,到 2031 年達到 35.5 億美元,2026 年至 2031 年的複合年成長率為 7.15%。

本報告按材料(金屬、木材、塑膠複合材料、混凝土及其他)、最終用戶(住宅、農業、國防、政府、採礦及其他)、安裝類型(固定/永久性、臨時/移動式)、安裝管道(專業承包商、製造商/DIY)和城市(孟買、新德里、浦那及其他)進行細分。市場預測以美元計價。

印度圍籬市場的趨勢和洞察

政府邊防安全:國家需求促進多年採購

在印度的圍籬市場,邊境建設正從零星採購轉向長期基礎設施規劃週期。印度已在其與巴基斯坦接壤的93.25%的邊境線和與孟加拉國接壤的79.08%的邊境線安裝了圍欄。同時,隨著一項耗資37億美元的計畫於2024年獲得批准,與緬甸接壤的1,643公里長的邊境線也進入了新的實施階段。 2025年5月,印度內政部批准了一項2億美元的預算,將巴基斯坦邊境沿線超過500公里的老舊圍欄更換為模組化多層屏障。 「綜合邊境管理系統(CIBMS)」是一種智慧圍欄模式,它透過將感測器、熱成像和監控工具整合到屏障中,不斷擴展其產品線。這使得印度的圍欄市場不易受到傳統建設週期的影響,並為正規供應商提供了明確的專案儲備。

工業園區和物流中心:即插即用的基礎設施創造了對結構化圍籬的需求。

印度圍籬市場也受惠於規劃完善的工業園區和倉儲園區的激增,這些園區和園區根據正式規範採購邊界系統。 2024年,印度倉儲產業吸引了19.6億美元的機構投資,A級倉儲庫存在過去五年中以21%的複合年成長率成長。 2026年3月,聯邦內閣批准了價值40億美元的BHAVYA項目,該項目將開發100個配備即插即用基礎設施的工業園區,使邊界圍欄成為項目基本範圍的一部分,而不是事後附加的。工業和內部貿易部宣布,總理綠色發展計畫(PM GatiShakti)已製定了600多個項目,包括工業走廊和物流園區,以支持土地的長期開發。這將使印度圍欄市場獲得來自工業和物流用戶的更強勁的重複性專案需求。

原料成本波動:鋼材價格走軟和聚合物價格飆升,對不平衡的利潤率造成了壓力。

由於鋼材、鋁材和PVC價格不匹配,印度圍籬市場正面臨嚴峻的成本結構挑戰。截至2025年10月,線材價格已降至每噸451-455美元,而同期PVC成本上漲高達30%,鋁材價格上漲8-10%。這對大量使用鋼材的基礎產品有利,但對複合材料和PVC塗層圍欄構成壓力,儘管這些產品的需求已呈現復甦跡象。因此,擁有多元化產品系列的製造商面臨不同產品線利潤率的波動。儘管在這種情況下印度圍欄市場仍有成長空間,但成本波動可能會減緩新材料類別的全面應用。

細分市場分析

2025年,金屬圍籬佔印度圍籬市場總收入的65.1%,持續維持在印度圍籬市場最大材料類別的地位。鍍鋅低碳鋼絲網、刺鐵絲網和鏈條圍欄繼續引領銷量,因為經過認證和驗證的產品在政府競標和邊境相關項目中更受青睞。鋁製圍欄則佔據小規模的高階細分市場,主要應用於沿海地區和化工廠等對耐腐蝕性要求高於成本的場所。混凝土圍籬在高速公路護欄和公共設施場所繼續發揮重要作用,而木製圍欄則主要應用於住宅裝飾領域。

塑膠和複合材料圍籬是成長最快的細分市場,預計2026年至2031年將以7.9%的複合年成長率成長。在印度圍籬市場,這個細分市場正隨著封閉式住宅和景觀園區的擴張而不斷擴大。木塑複合材料和高密度聚苯乙烯板材因其美觀、維護成本低和防白蟻等優點,逐漸被市場接受,彌補了其較高的初始成本。卡納塔克邦的「2025-2030年產業政策」支持對電子、航太和電動車產業叢集的投資,這與在更清潔的工業環境中對模組化邊界圍欄的需求相契合。在印度圍籬產業,這種市場結構為複合材料提供了清晰的成長路徑,同時又維持了金屬產品的主導地位。

到2025年,政府終端用戶將佔印度圍籬市場30.5%的佔有率,成為最大的需求群體。這項需求主要來自國防設施、鐵路邊界、國道、邊境相關項目以及公共產業設施。 「BHAVYA」計畫和「PM GatiShakti」計畫將進一步鞏固這一地位,因為公園、道路和物流項目在建設初期就需要邊界系統。此外,由於國防相關訂單對產品規格要求更高,因此其價格也高於普通圍欄。

農業圍籬是成長最快的終端用戶領域,預計2026年至2031年將以8.1%的複合年成長率成長。在作物損失、牲畜流動和野生動物碰撞等問題直接導致需要預防性圍欄的地區,最為顯著成長。雖然採礦、石油化工以及能源電力行業目前市場佔有率仍然較小,但由於它們採購高規格系統且對常規住宅建設週期的依賴性較低,因此也構成了一個重要的市場。在印度的圍欄行業,住宅需求目前小規模,但隨著線上採購和預製組件的普及,都市區住宅的購買管道正在逐步擴大。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場趨勢與分析

- 市場概覽

- 市場促進因素

- 政府在邊防安全和基礎設施項目(例如沿著國際邊界建造圍欄)方面所做的努力。

- 政府基礎設施建設帶動了對道路、鐵路和公共設施圍欄的需求。

- 工業園區、倉庫和物流中心的成長為邊界安全圍欄提供了支撐

- 農業領域日益成長的防護需求推動了對農場和牲畜圍欄的需求。

- 日益成長的安全隱患正在推動金屬圍欄、金屬網格和電圍欄系統的普及。

- 野生動物保護和緩解人獸衝突的需求日益成長,推動了野生動物圍欄解決方案的普及。

- 市場限制因素

- 鋼材、鋁材和PVC價格的波動推高了圍籬產品的成本。

- 農村地區和小規模買家對價格的敏感度阻礙了高階圍欄的普及。

- 來自非正規本地製造商的競爭正在影響價格和產品品質。

- 價值供應鏈分析

- 監理情勢

- 科技與創新趨勢

- 波特五力模型

- 價格分析

- 永續性和環保材料的發展趨勢

- 邊防安全框架與實施趨勢

第5章 市場規模與成長預測

- 材料

- 金屬

- 鋼

- 鋁

- 木頭

- 塑膠複合材料

- 具體的

- 其他

- 金屬

- 最終用戶

- 住宅

- 農業

- 軍事/國防

- 政府

- 礦業

- 石油/化工

- 能源和發電

- 其他

- 按安裝類型

- 固定/永久型

- 臨時/可移動類型

- 透過安裝通道

- 專家

- 其他 - 製造商、DIY/模組化套件

- 按城市

- 孟買

- 新德里(NCR)

- 浦那

- 班加羅爾

- 海得拉巴

- 清奈

- 加爾各答

- 印度以及其他中東和非洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- A-1 Fence Products

- India Fence

- Maa Vishla Industries(MV FENCE)

- JustFence

- Sharda Wires

- VBS Industries(VBS Group)

- Perfect Fencings

- Smart Fence Integrated Security Pvt. Ltd.

- Safe and Save Equipments(iFENCE)

- Fence Tech Innovations

- Godrej & Boyce Mfg. Co. Ltd.

- Static Systems

第7章 市場機會與未來展望

According to Mordor Intelligence, the india fencing market size is projected to be USD 2.34 billion in 2025, USD 2.51 billion in 2026, and reach USD 3.55 billion by 2031, growing at a CAGR of 7.15% from 2026 to 2031.

This report is Segmented by Material (Metal, Wood, Plastic & Composite, Concrete, Other), by End-User (Residential, Agricultural, Defense, Government, Mining, and More), by Installation Type (Fixed/Permanent, Temporary/Mobile), by Installation Channel (Professional Contractor, Fabricators/DIY), and by City (Mumbai, Delhi NCR, Pune, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Fencing Market Trends and Insights

Government Border Security: Sovereign Mandates Unlock Multi-Year Procurement

The India fencing market is seeing border work move from periodic buying to a long-cycle infrastructure program. India had already fenced 93.25% of its border with Pakistan and 79.08% of its border with Bangladesh. At the same time, the 1,643 km Myanmar frontier moved into a new execution phase after the USD 3.7 billion project was approved in 2024. In May 2025, the Ministry of Home Affairs also cleared USD 0.2 billion to replace more than 500 km of aging fencing on the Pakistan border with modular, multi-layered barriers. The Comprehensive Integrated Border Management System, a smart-fencing model, is expanding the product mix by linking barriers with sensors, thermal imaging, and surveillance tools. This keeps the India fencing market less exposed to normal construction cycles and gives organized suppliers a visible project pipeline.

Industrial Parks and Logistics Hubs: Plug-And-Play Infrastructure Creates Structured Fencing Demand

The India fencing market is also gaining from the spread of planned industrial parks and warehouse campuses that buy perimeter systems through formal specifications. India's warehousing sector drew USD 1.96 billion in institutional investment in 2024, while Grade A stock had expanded at a 21% CAGR over the prior five years. In March 2026, the Union Cabinet approved the BHAVYA scheme at USD 4.0 billion to develop 100 industrial parks with plug-and-play infrastructure, which makes perimeter fencing part of the base project scope rather than a later add-on. The Department for Promotion of Industry and Internal Trade stated that PM GatiShakti had mapped more than 600 projects, including industrial corridors and logistics parks, which support long-horizon site development. This gives the India fencing market a stronger mix of repeatable project demand from industrial and logistics users.

Input Cost Volatility: Steel Softness and Polymer Spikes Create Asymmetric Margin Pressure

The India fencing market faces a difficult cost mix because steel, aluminum, and PVC are not moving in the same direction. Wire rod prices dropped to USD 451-455 per tonne in October 2025, while PVC costs rose by up to 30% and aluminum prices increased by 8-10% over the same broad period. This helps basic steel-heavy products but puts pressure on composite and PVC-coated fencing, which are seeing improving demand. Producers with mixed portfolios, therefore, face uneven margin performance across product lines. The India fencing market can still grow under these conditions, but cost swings are likely to slow full adoption in newer material categories.

Other drivers and restraints analyzed in the detailed report include:

- Agricultural Fencing: Crop Losses and Wildlife Pressure Drive Rural Electrification Of Perimeters

- Rising Security Concerns: Industrial And Institutional Buyers Upgrade Perimeter Systems

- Unorganized Competition: Fragmented Supply Base Restrains Quality Standardization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal fencing accounted for 65.1% of market revenues in 2025, maintaining its position as the largest material category in the India fencing market. Galvanized mild steel wire mesh, barbed wire, and chain-link panels still lead volume because government tenders and border projects favor certified and proven products. Aluminum fencing serves a smaller premium niche in coastal and chemical settings where corrosion resistance matters more than cost. Concrete fencing continues to hold a role in highway barriers and utility compounds, while wood remains limited to decorative residential use.

Plastic and composite fencing is the fastest-growing segment, with a 7.9% CAGR for 2026-2031, and this part of the India fencing market is expanding in gated housing and landscaped campuses. Wood-plastic composite and high-density polyethylene panels are gaining acceptance where appearance, low maintenance, and termite resistance offset the higher initial cost. Karnataka's Industrial Policy 2025-2030 supports investment in electronics, aerospace, and electric vehicle clusters, which aligns with demand for modular perimeter formats in cleaner industrial settings. Within the India fencing industry, this mix keeps metal dominant while giving composites a clearer growth lane.

Government end-users accounted for 30.5% of the India fencing market in 2025, making them the single largest demand group. Demand came from defense compounds, railway boundaries, national highways, border programs, and public utility sites. The BHAVYA scheme and the PM GatiShakti pipeline strengthen this position, as park, road, and logistics projects require perimeter systems early in the build cycle. Defense-linked orders also carry higher product specifications, which support better selling prices than basic enclosure work.

Agricultural fencing is the fastest-growing end-user segment, with a 8.1% CAGR for 2026-2031. Growth is strongest where crop losses, livestock movement, and wildlife conflict create a direct need for preventive fencing. Mining, petroleum and chemicals, and energy and power remain smaller in share, but they are important because they buy high-specification systems and are less tied to normal housing cycles. In the India fencing industry, residential demand is smaller today, but online sourcing and prefabricated kits are starting to expand access for urban homeowners.

List of Companies Covered in this Report:

- A-1 Fence Products

- India Fence

- Maa Vishla Industries (MV FENCE)

- JustFence

- Sharda Wires

- VBS Industries (VBS Group)

- Perfect Fencings

- Smart Fence Integrated Security Pvt. Ltd.

- Safe and Save Equipments (iFENCE)

- Fence Tech Innovations

- Godrej & Boyce Mfg. Co. Ltd.

- Static Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government initiatives for border security and infrastructure projects such as fencing along international borders

- 4.2.2 Government infrastructure development is driving fencing demand across roads, railways, and public facilities

- 4.2.3 Growth in industrial parks, warehouses, and logistics hubs supporting perimeter security fencing

- 4.2.4 Increasing agricultural protection needs driving demand for farm and livestock fencing

- 4.2.5 Rising security concerns boosting adoption of metal, wire mesh, and electric fencing systems

- 4.2.6 Growing need for wildlife protection and human-animal conflict mitigation driving adoption of wildlife fencing solutions

- 4.3 Market Restraints

- 4.3.1 Fluctuating steel, aluminum, and PVC prices increasing fencing product costs

- 4.3.2 Price sensitivity among rural and small-scale buyers limiting premium fencing adoption

- 4.3.3 Competition from unorganized local manufacturers affecting pricing and product quality

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology & Innovation Trends

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Sustainability & Eco-Friendly Material Trends

- 4.10 Border Security Framework & Deployment Trends

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Metal

- 5.1.1.1 Steel

- 5.1.1.2 Aluminium

- 5.1.2 Wood

- 5.1.3 Plastic & Composite

- 5.1.4 Concrete

- 5.1.5 Other Materials

- 5.1.1 Metal

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Agricultural

- 5.2.3 Military & Defense

- 5.2.4 Government

- 5.2.5 Mining

- 5.2.6 Petroleum & Chemicals

- 5.2.7 Energy & Power

- 5.2.8 Other End-Users

- 5.3 By Installation Type

- 5.3.1 Fixed / Permanent Fencing

- 5.3.2 Temporary / Mobile Fencing

- 5.4 By Installation Channel

- 5.4.1 Professional Contractor

- 5.4.2 Others - Fabricators, DIY / Modular Kits

- 5.5 By City

- 5.5.1 Mumbai Metropolitan Region

- 5.5.2 Delhi NCR

- 5.5.3 Pune

- 5.5.4 Bengaluru

- 5.5.5 Hyderabad

- 5.5.6 Chennai

- 5.5.7 Kolkata

- 5.5.8 Rest of India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 A-1 Fence Products

- 6.4.2 India Fence

- 6.4.3 Maa Vishla Industries (MV FENCE)

- 6.4.4 JustFence

- 6.4.5 Sharda Wires

- 6.4.6 VBS Industries (VBS Group)

- 6.4.7 Perfect Fencings

- 6.4.8 Smart Fence Integrated Security Pvt. Ltd.

- 6.4.9 Safe and Save Equipments (iFENCE)

- 6.4.10 Fence Tech Innovations

- 6.4.11 Godrej & Boyce Mfg. Co. Ltd.

- 6.4.12 Static Systems

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2026-2034年全球水產養殖網箱市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球水產養殖網箱市場規模、佔有率、趨勢和成長分析報告 德國圍籬市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼圍籬市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

德國圍籬市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼圍籬市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 木質圍籬市場規模、佔有率和成長分析:按樹種、圍籬樣式、應用、銷售管道和地區分類-2026-2033年產業預測

木質圍籬市場規模、佔有率和成長分析:按樹種、圍籬樣式、應用、銷售管道和地區分類-2026-2033年產業預測 美國圍欄市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測(2026-2033 年)

美國圍欄市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測(2026-2033 年) 圍籬市場:2026-2032年全球市場預測(依產品類型、材質、功能、高度、安裝方式、銷售管道及應用分類)

圍籬市場:2026-2032年全球市場預測(依產品類型、材質、功能、高度、安裝方式、銷售管道及應用分類) 圍欄市場:按類型、應用和地區分類

圍欄市場:按類型、應用和地區分類 2026年全球圍籬市場報告2026年全球鋁製金屬圍籬市場報告動物籠具市場:2026-2032年全球市場預測(依動物種類、材料、籠具類型、最終用戶及通路分類)

2026年全球圍籬市場報告2026年全球鋁製金屬圍籬市場報告動物籠具市場:2026-2032年全球市場預測(依動物種類、材料、籠具類型、最終用戶及通路分類)