|

市場調查報告書

商品編碼

2072914

中國化工物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)China Chemical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

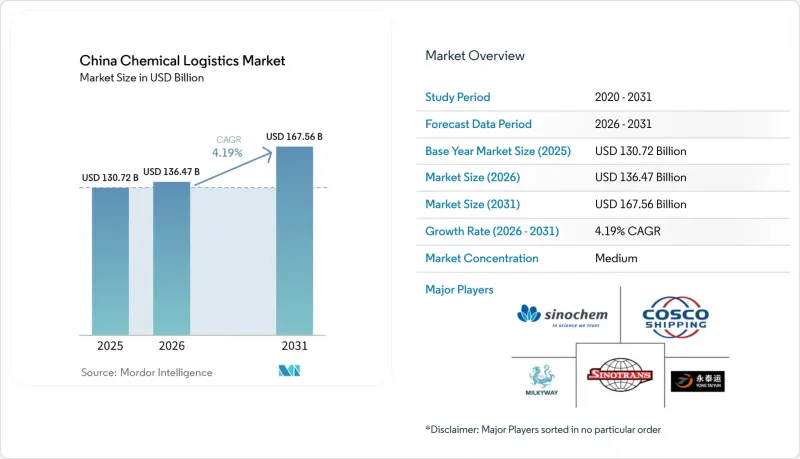

根據 Mordor Intelligence 預測,中國化工物流市場規模預計到 2025 年將達到 1307.2 億美元,到 2026 年將達到 1364.7 億美元,到 2031 年將達到 1675.6 億美元,2026 年至 2031 年的複合年成長率為 4.9%。

本報告按服務(運輸、倉儲和配送、附加價值服務)、危險品分類(危險品和非危險品)、溫度控制(溫控和非溫控)、最終用戶業(製藥、化妝品、特種化學品等)以及地區(北部、東北部、東部等)進行細分。市場預測以美元計價。

中國化工物流市場趨勢與洞察

石化產品產能從西部向東部轉移,正在推動國內運輸量成長。

中國化工物流市場正經歷重組,石化產能正從沿海叢集轉移到內陸和西部省份。新疆、寧夏、陝西和四川等地對煤化工的投資,推動了甲醇、乙二醇、芳烴和乙酸等產品的長途國內運輸。現有的以進出口為主的華東物流體系,在這些內陸運輸路線上的效率較低。武漢港江陵石化碼頭的建設正是為了因應這項變化,它在長江中上游地區新增了大規模公共石化樞紐,進一步連接了內陸生產基地和東部需求中心。河北省提出的到2025年優先發展60個化工項目、總投資2010億元人民幣(約合278億美元)的政策表明,內陸物流網路的擴張不僅限於西部地區,更北化的戰略正在構建,以滿足新的貨物運輸需求。隨著生產格局的這些變化,中國化工物流市場越來越重視能夠將河流、鐵路和公路運輸整合到單一服務平台上的營運商,而不是僅僅依賴沿海港口貨運網路。

國際海事組織2026年的脫碳目標迫使一批化學品油輪更換。

中國化學品物流市場的發展也受到與國際海事組織(IMO)脫碳和船舶能源效率標準相關的船隊現代化週期的推動。廣州船舶國際有限公司於2025年提前交付了四艘474,500載重噸的LR1型化學品和成品油輪中的首艘。這些船舶符合EEDI第三階段的要求,並預留了改裝為雙燃料船舶的空間。南京油輪公司也於2025年訂購了三艘6,600載重噸的甲醇相容型不鏽鋼化學品運輸船,預計2028年上半年交付。這表明,儘管運費疲軟,船東仍在持續投資。根據SSY的預測,全球化學品油輪訂單累積訂單的46%預計將在2026年交付,這意味著在老舊船舶退役之前,短期內可能會出現供應壓力。此外,中遠海運能源運輸有限公司還訂購了一艘9,200載重噸的不銹鋼化學品船,預計將於2025年5月交付,這表明國內營運商仍在擴大其沿海特種運輸能力。因此,中國的化學品物流市場正朝著一種新的結構轉型:透過單一的數位化操作系統來處理脫碳合規和危險品貨物的監控,而不是透過各自獨立的監管流程。

2025年「郭梁號」事故後加強隧道管理

2025年國梁事故後,中國化工物流市場中多條危險物品運輸路線的隧道管理規定更加嚴格,導致運輸時間延長。這對河南、山西、陝西、四川和貴州等省份尤其重要,因為這些省份嚴重依賴公路基礎設施,而公路基礎設施中包含大量隧道,是跨省運輸的關鍵所在。路線受限和營運時間縮短使得受影響的運輸路線無法維持下游化工產品使用者所需的「準時制」交付節奏。交通運輸運輸部於2026年2月修訂的《危險物品道路運輸管理條例》透過衛星監控加強了路線合規性。這導致對路線偏離的處罰加大,給缺乏車輛管理系統的中小型運輸企業帶來了更大的成本負擔。由於許多中小型道路運輸企業無法像大型運輸公司那樣快速地承擔採用新技術和合規性的成本,這種成本壓力可能會加速產業結構調整。因此,在中國的化學物流市場,托運人的需求正在轉向那些能夠證明其致力於安全繞行路線的公司,或者那些在道路可靠性下降時能夠轉而採用其他運輸方式的公司。

細分市場分析

到2025年,運輸業將佔中國化工物流市場總收入的64.77%,成為該市場最大的組成部分。這一格局反映了中國化工物流市場的資產密集特徵,其化學產品運輸仍依賴於油輪、鐵路貨車、沿海油輪和內河航運的協調運作,而非純粹的數位化中介模式。道路運輸仍是區域內運輸的主要方式,為產業叢集間短途危險品運輸提供了路線柔軟性。海運和內河航運承擔了大部分跨省大宗貨物的運輸,其中年吞吐能力達355萬噸的武漢石化碼頭作為公共樞紐,在該體系中發揮著至關重要的作用。

預計到2031年,附加價值服務將以7.31%的複合年成長率成長,成為物流領域成長最快的部分。 HOYER於2025年11月在上海的科思創一體化基地進行擴建,將自動化灌裝、溫控倉儲和全天候監控整合到一個符合監管要求的單一服務模式中,便是一個例證。在中國化工物流市場,這一成長趨勢表明,企業不僅在運輸方面,而且在以外包配製支援、廠內營運和單證處理為核心的服務方面,都將增加支出。

截至2025年,危險化學品將佔中國化學品物流市場的66.5%,預計2031年將以6.19%的最高成長率成長。這兩個領域對市場成長的驅動作用表明,中國化學品物流市場仍將以易燃液體、腐蝕性物質、反應性產品和電池相關材料等需要特殊處理的物料為主導。新興的合規環境進一步加速了這一趨勢,因為危險物品的運輸必須由持有許可證的承運商進行,並需要路線管理和更有系統的可追溯性。將於2026年5月生效的《危險化學品安全法》通過提高危險化學品全生命週期的操作標準,正在推動這項變革。

因此,市場佔有率正加速轉移到那些已擁有數位化管理系統和合規資產的業者。針對腐蝕性物質的RFID連結管理,為物流中心和倉儲環境增添了一層新的監管機制,而這些場所的檢驗要求也日益提高。非危險化學品在中國化工物流市場仍佔較大佔有率,主要包括基礎聚合物、化學肥料和食品化學原料,這些產品適用更廣泛的貨物運輸標準。然而,隨著越來越多的托運人意識到危險貨物的營運優勢,並在其廣泛的業務組合中擴展可追溯性工具,危險品和非危險品之間的服務品質差距正在縮小。換言之,危險品法規不僅塑造了該細分市場本身,也提高了整個中國化工物流市場的服務期望。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況及物流在化學工業中的作用

- 化工產業的支出趨勢

- 市場促進因素

- 中歐關於危險物品運輸的協議有利於跨境合規。

- 石化產品產能從西部向東部轉移,正在推動國內航運路線的貨物運輸量成長。

- 電子商務對特殊包裝化學品(油墨、塗料、黏合劑)的需求

- 國際海事組織2026年的脫碳目標正在迫使化學品運輸船船隊現代化。

- 透過在北京、天津和河北三地推行危險化學品統一許可證試點項目,降低了行政成本。

- 中國西南地區鋰離子電池回收叢集的發展

- 市場限制因素

- 2025年郭亮事故後加強隧道管理

- 由於鋼鐵產能下降,鐵路罐車短缺

- 對 8 類腐蝕性材料強制實施 RFID 追蹤,導致合規成本上升。

- 提高國際海事組織 II 類貨物沿海港口擁塞附加費。

- 法律規範

- 價值鍊與通路結構分析

- 技術創新的前景

- 波特五力模型

- 化學物質物流需求的變化

- 地緣政治事件對供應鏈轉型的影響

第5章 市場規模及成長預測(價值,2026-2031 年)

- 透過物流功能

- 運輸

- 道路運輸

- 航空

- 海路和內河航道

- 鐵路

- 倉儲、物流和庫存管理

- 附加價值服務及其他

- 運輸

- 依危險分類

- 危險化學品

- 無害化學品

- 按類型控制溫度

- 溫控(冷氣/暖氣)

- 非溫控型

- 產業最終用途

- 製藥

- 化妝品

- 石油和天然氣

- 特種化學品

- 其他最終用戶

- 按地區

- 北

- 東北

- 東方

- 中部

- 南

- 西南

- 西北

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- Sinotrans Limited

- Sinochem Logistics

- Milkyway Chemical Supply Chain Service Co., Ltd.

- Yongtaiyun Chemical Logistics

- China COSCO Shipping Logistics

- China Railway Special Cargo Logistics

- Xiamen Xiangyu Group

- Shanghai Huayi Group Logistics

- Oriental Logistics Group

- Stolt Tank Containers

- HOYER Group

- Bertschi Group

- Leschaco China

- Sinopec Chemical Commercial Holding

- China National Chemical Engineering Logistics

- CIMC ENRIC Logistics

- SF Supply Chain

- CEVA Logistics China

- DHL Supply Chain China

- Shanghai Chemical Industrial Logistics(SCIL)

- Kerry Logistics Network Ltd.

- Den Hartogh Logistics

第7章 市場機會與未來展望

According to Mordor Intelligence, the china chemical logistics market size is projected to be USD 130.72 billion in 2025, USD 136.47 billion in 2026, and reach USD 167.56 billion by 2031, growing at a CAGR of 4.19% from 2026 to 2031.

This report is Segmented by Service (Transportation, Warehousing and Distribution, and Value-Added Services), by Hazard Class (Hazardous and Non-Hazardous), by Temperature Control (Controlled and Non-Controlled), by End Use Industry (Pharmaceutical, Cosmetic, Specialty Chemicals, and More), and by Region (North, Northeast, East, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Chemical Logistics Market Trends and Insights

Petrochemical Capacity West-To-East Shift Boosting Domestic Lane Volumes

The China chemical logistics market is being reshaped by the shift of petrochemical capacity from coastal clusters toward inland and western provinces. Coal-to-chemicals investments in Xinjiang, Ningxia, Shaanxi, and Sichuan are boosting long-haul domestic shipments of methanol, ethylene glycol, aromatics, and acetic acid. Existing East China logistics systems were built more around import and export flows, so they are less efficient for these inland-origin domestic lanes. The Jiangling Petrochemical Terminal at Wuhan Port is a direct response to that change because it adds a large public petrochemical node on the upper-middle Yangtze and connects more inland output with eastern demand centers. Hebei's 2025 push to prioritize 60 chemical projects worth CNY 201 billion (USD 27.8 billion) shows that inland chain extension is not limited to western China and is also building a northern vector for new freight demand. As that production map changes, the China chemical logistics market is placing a premium on operators that can combine river, rail, and road movements on a single service platform rather than rely solely on coastal port-based freight networks.

IMO 2026 Decarbonization Targets Forcing Fleet Renewal of Chemical Tankers

The China chemical logistics market is also being driven by a fleet renewal cycle tied to IMO decarbonization and vessel-efficiency standards. Guangzhou Shipyard International delivered the first of 4,74,500-dwt LR1 chemical and product tankers ahead of schedule in 2025, and the vessels met EEDI Phase 3 requirements while also reserving dual-fuel conversion capability. Nanjing Tanker Corporation also ordered 3 methanol-ready 6,600-dwt stainless steel chemical tankers in 2025, with delivery planned for the first half of 2028, indicating that owners are still committing capital despite a softer rate backdrop. SSY expected 46% of the global chemical tanker orderbook to deliver in 2026, suggesting near-term supply pressure may emerge before older tonnage leaves the fleet. COSCO SHIPPING Energy Transportation also ordered a 9,200-dwt stainless-steel chemical tanker in May 2025, reinforcing that domestic operators are still expanding specialized coastal capacity. The China chemical logistics market is therefore moving toward a structure in which decarbonization compliance and hazardous-cargo monitoring are increasingly handled through a single digital operating system rather than through separate regulatory workflows.

Tightened Tunnel Restrictions after the 2025 Guoliang Accident

The China chemical logistics market is facing longer route times on several hazardous road corridors after tighter tunnel controls followed the 2025 Guoliang incident. This matters because provinces such as Henan, Shanxi, Shaanxi, Sichuan, and Guizhou depend heavily on tunnel-rich road infrastructure for inter-provincial movement. When routes are restricted or time windows are narrowed, affected lanes can no longer support the same just-in-time delivery rhythm demanded by downstream chemical users. The Ministry of Transport's revised dangerous-goods road transport regulations, introduced in February 2026, strengthened satellite-monitored route compliance. It raised penalties for deviations, which increases the cost burden on smaller carriers without integrated fleet systems. That cost pressure is likely to accelerate consolidation, as many smaller road operators cannot absorb new technology and compliance costs at the same pace as larger fleets. The China chemical logistics market is therefore seeing shipper demand shift toward providers that can either prove safe rerouting discipline or switch volumes to other modes when roads become less reliable.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Demand for Specialty Packaging Chemicals (Inks, Coatings, Adhesives)

- Growth of Lithium-Ion Battery Recycling Clusters in Southwest China

- Rail-Tank-Wagon Shortage Because of Steel Capacity Curbs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation accounted for 64.77% of revenue in 2025, making it the largest component of the China chemical logistics market size. That position reflects the asset-heavy nature of the China chemical logistics market, where chemical movement still depends on tank trucks, rail wagons, coastal tankers, and inland waterway links rather than on pure digital brokerage models. Road transport remains the key intra-regional mode because it offers routing flexibility for short-haul dangerous goods movements across industrial clusters. Sea and inland waterways handle much of the higher-volume inter-provincial flow, and the Wuhan petrochemical terminal adds a meaningful public node to that system with 3.55 million tons of annual capacity.

Value-added services are forecast to grow at a 7.31% CAGR through 2031, which is the fastest pace among logistics functions. HOYER's November 2025 expansion at the Covestro Integrated Site in Shanghai shows why, because the site combines automated filling, temperature-controlled warehousing, and round-the-clock monitoring into one compliance-heavy service model. In the China chemical logistics market, that growth path points to higher spending on outsourced blending support, in-plant operations, and documentation-intensive services rather than on transport alone.

Hazardous chemicals accounted for 66.5% of the China chemical logistics market in 2025 and posted the fastest projected CAGR of 6.19% through 2031. This dual lead shows that the China chemical logistics market remains centered on flammable liquids, corrosives, reactive products, and battery-related materials that require specialized handling. The new compliance environment strengthens that position because hazardous cargo cannot move without licensed carriers, route controls, and more structured traceability. China's Hazardous Chemicals Safety Law, effective from May 2026, is reinforcing that shift by raising operating standards across the hazardous chemical lifecycle.

The result is faster share migration toward operators that already have digital control systems and compliant assets. RFID-linked management for corrosives is adding another layer of discipline in parks and storage environments where inspection requirements are rising. Non-hazardous chemicals still account for a substantial share of the China chemical logistics market, mainly through base polymers, fertilizers, and food-grade chemical ingredients, which are handled under broader freight standards. Even so, the distinction between hazardous and non-hazardous service quality is narrowing, as many shippers are extending traceability tools across their broader portfolios after seeing the operational benefits of hazardous cargo. That means hazardous regulation is not only shaping its own segment, but also lifting service expectations across the wider China chemical logistics market.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing, Distribution and Inventory Management

- Value-added Services and Others

- Transportation

- By Hazard Class

- Hazardous Chemicals

- Non-hazardous Chemicals

- By Temperature Control

- Temperature-Controlled (Refrigerated/Heated)

- Non-Temperature-Controlled

- By End Use Industry

- Pharmaceutical

- Cosmetic

- Oil and Gas

- Specialty Chemicals

- Other End-Users

- By Region

- North

- Northeast

- East

- Central

- South

- Southwest

- Northwest

List of Companies Covered in this Report:

- Sinotrans Limited

- Sinochem Logistics

- Milkyway Chemical Supply Chain Service Co., Ltd.

- Yongtaiyun Chemical Logistics

- China COSCO Shipping Logistics

- China Railway Special Cargo Logistics

- Xiamen Xiangyu Group

- Shanghai Huayi Group Logistics

- Oriental Logistics Group

- Stolt Tank Containers

- HOYER Group

- Bertschi Group

- Leschaco China

- Sinopec Chemical Commercial Holding

- China National Chemical Engineering Logistics

- CIMC ENRIC Logistics

- SF Supply Chain

- CEVA Logistics China

- DHL Supply Chain China

- Shanghai Chemical Industrial Logistics (SCIL)

- Kerry Logistics Network Ltd.

- Den Hartogh Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview & Role of Logistics in Chemical

- 4.2 Chemical Industry Spending Trends

- 4.3 Market Drivers

- 4.3.1 Sino-EU Dangerous-Goods Transport Accords Easing Cross-Border Compliance

- 4.3.2 Petrochemical Capacity West-To-East Shift Boosting Domestic Lane Volumes

- 4.3.3 E-Commerce Demand for Specialty Packaging Chemicals (Inks, Coatings, Adhesives)

- 4.3.4 IMO 2026 Decarbonization Targets Forcing Fleet Renewal of Chemical Tankers

- 4.3.5 Beijing-Tianjin-Hebei "Haz-Chem One-Permit" Pilot Reducing Administrative Costs

- 4.3.6 Growth of Lithium-Ion Battery Recycling Clusters in Southwest China

- 4.4 Market Restraints

- 4.4.1 Tightened Tunnel Restrictions after 2025 Guoliang Accident

- 4.4.2 Rail-Tank-Wagon Shortage Because of Steel Capacity Curbs

- 4.4.3 Mandatory RFID Tracking for Class-8 Corrosives Raising Compliance Cost

- 4.4.4 Rising Coastal Port Congestion Surcharges for IMO Type II Cargoes

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Chemical Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing, Distribution and Inventory Management

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Hazard Class

- 5.2.1 Hazardous Chemicals

- 5.2.2 Non-hazardous Chemicals

- 5.3 By Temperature Control

- 5.3.1 Temperature-Controlled (Refrigerated/Heated)

- 5.3.2 Non-Temperature-Controlled

- 5.4 By End Use Industry

- 5.4.1 Pharmaceutical

- 5.4.2 Cosmetic

- 5.4.3 Oil and Gas

- 5.4.4 Specialty Chemicals

- 5.4.5 Other End-Users

- 5.5 By Region

- 5.5.1 North

- 5.5.2 Northeast

- 5.5.3 East

- 5.5.4 Central

- 5.5.5 South

- 5.5.6 Southwest

- 5.5.7 Northwest

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Sinotrans Limited

- 6.4.2 Sinochem Logistics

- 6.4.3 Milkyway Chemical Supply Chain Service Co., Ltd.

- 6.4.4 Yongtaiyun Chemical Logistics

- 6.4.5 China COSCO Shipping Logistics

- 6.4.6 China Railway Special Cargo Logistics

- 6.4.7 Xiamen Xiangyu Group

- 6.4.8 Shanghai Huayi Group Logistics

- 6.4.9 Oriental Logistics Group

- 6.4.10 Stolt Tank Containers

- 6.4.11 HOYER Group

- 6.4.12 Bertschi Group

- 6.4.13 Leschaco China

- 6.4.14 Sinopec Chemical Commercial Holding

- 6.4.15 China National Chemical Engineering Logistics

- 6.4.16 CIMC ENRIC Logistics

- 6.4.17 SF Supply Chain

- 6.4.18 CEVA Logistics China

- 6.4.19 DHL Supply Chain China

- 6.4.20 Shanghai Chemical Industrial Logistics (SCIL)

- 6.4.21 Kerry Logistics Network Ltd.

- 6.4.22 Den Hartogh Logistics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

印度化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

印度化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 全球化學品物流市場零售油氣物流:市佔率分析、產業趨勢及統計、成長預測(2026-2031)

全球化學品物流市場零售油氣物流:市佔率分析、產業趨勢及統計、成長預測(2026-2031) 化學品物流市場規模、佔有率、趨勢和預測:按類型、服務和地區分類,2026-2034年

化學品物流市場規模、佔有率、趨勢和預測:按類型、服務和地區分類,2026-2034年 零售油氣物流市場:依運輸方式、燃料類型、物流供應商類型及基礎設施類型分類-2026-2032年全球市場預測

零售油氣物流市場:依運輸方式、燃料類型、物流供應商類型及基礎設施類型分類-2026-2032年全球市場預測 化學品物流市場:依服務、運輸方式、最終用戶產業及地區分類。

化學品物流市場:依服務、運輸方式、最終用戶產業及地區分類。 2026年全球化學品物流市場報告化學品物流市場:依服務類型、化學品類型、運輸方式、包裝類型、溫度控制及最終用途產業分類-2026-2032年全球預測新加坡化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

2026年全球化學品物流市場報告化學品物流市場:依服務類型、化學品類型、運輸方式、包裝類型、溫度控制及最終用途產業分類-2026-2032年全球預測新加坡化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)