|

市場調查報告書

商品編碼

2072911

德國化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Germany Chemical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

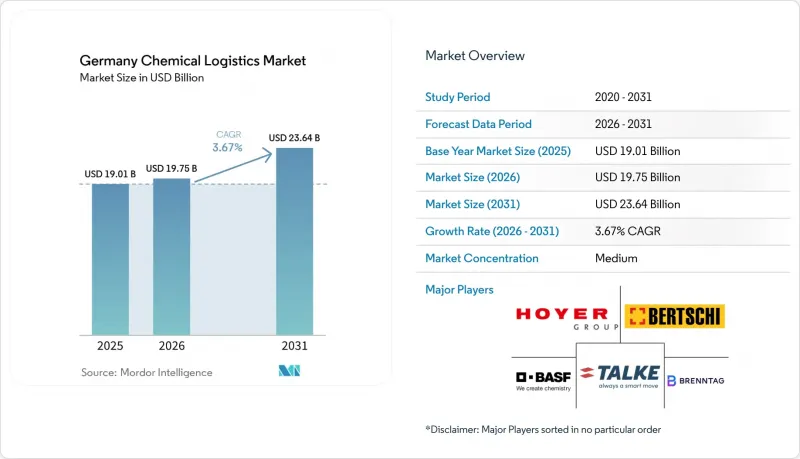

根據 Mordor Intelligence 預測,德國化學品物流市場規模將從 2025 年的 190.1 億美元成長到 2026 年的 197.5 億美元,到 2031 年將達到 236.4 億美元,2026 年至 2031 年的複合年成長率為 3.67%。

本報告按服務類型(運輸、倉儲配送、附加價值服務)、危險品分類(危險品、非危險品)、溫度控制(溫控、非溫控)、最終用戶業(製藥、化妝品、特種化學品等)以及地區(北萊茵-威斯特法倫州、巴伐利亞州及其他州)進行細分。市場預測以美元計價。

德國化工物流市場的趨勢與洞察

國內化工生產正在加速復甦:脆弱的復甦趨勢正在形成選擇性的物流需求。

德國化工和製藥業進入2026年時,其業務前景與2025年相比已顯疲軟。這主要是由於產業產量下降3.3%,銷售額下降3%,以及平均產能運轉率僅72.5%。在此背景下,德國化工物流市場的復甦並非全面,而是具有選擇性。這是因為即使產量略有回升,也只會提高油罐車利用率、倉庫周轉率和包裝作業量,而散裝貨物的裝卸量卻無法完全恢復。這為提供多元化服務的營運商提供了一定的迴旋餘地,因為與製藥相關的物流流動可以支撐網路運轉率,而散裝貨物生產商的運轉率仍然較低。這也意味著,如果德國化工物流市場的庫存補充速度在生產全面復甦之前放緩,那麼那些早期增加運輸能力的營運商可能會面臨利潤率下降的風險。因此,資產配置正在轉向能夠同時處理核心化工產品和規模較小但監管嚴格的貨物的混合型網路。

歐盟替代性爭議解決機制的合規性正在推動對專家的需求:專業知識仍然是一個明顯的差異化因素。

由於危險品運輸需要訓練有素的員工、經認證的流程以及專為受管制物質設計的儲存設施,因此合規性仍然是德國化學品物流市場需求的主要促進因素。當托運人希望減少貿易夥伴數量時,能夠整合道路運輸、罐體處理、重新包裝、檢驗和文件支援的供應商更具優勢。 Leschaco位於不來梅的物流中心於2025年10月投入運作,該中心擴展了其危險品專用基礎設施和基於分類的儲存容量,這表明供應商正在投資以滿足合規性需求。BASF在路德維希港實施的dTEX系統也體現了類似的趨勢,該系統幾乎完全實現了卡車調度的自動化,並增強了諸如場地訪問、運輸管理和工作流程執行等數位化功能。事實上,在德國化學品物流市場,那些將合規性視為營運能力而非後勤部門負擔的供應商更受青睞。隨著客戶越來越重視審計準備和管理服務支持,這種差距可能會進一步擴大。

駕駛人短缺和道路交通費上漲:短期內道路運輸能力仍是主要的阻礙因素。

在德國化工物流市場,陸路運輸仍佔據化學產品運輸的很大比例,因此合格駕駛員的短缺會迅速加劇現有運輸能力的緊張。危險品運輸面臨的壓力更大,因為化學托運人需要能夠滿足比普通貨物運輸更嚴格的操作和安全要求的駕駛員。這凸顯了路線規劃、堆場自動化和網路密度的重要性,儘管這些工具只能緩解而非消除限制。這也增加了多式聯運的吸引力,特別是對於那些能夠將公路路段與鐵路以及碼頭集散中心連接起來的業者而言。在德國化工物流市場,擁有罐式運輸能力、鐵路運輸通道和嚴格調度能力的營運商即使在公路貨運堵塞的情況下也能更好地保持盈利。因此,托運人在物流競標中越來越重視運輸的韌性和柔軟性。

細分市場分析

預計到2025年,運輸業將佔據德國化工物流市場59.2%的佔有率,證實了運輸活動仍是其核心收入來源,涵蓋油罐車、鐵路貨車、駁船和合約運輸。德國的化學生產基地分散在北萊茵-威斯特法倫州、巴登-符騰堡州和巴伐利亞州的多個叢集,這些地區都依賴密集的國內貨運網路,因此道路運輸仍然是最大的運輸方式。鐵路在德國化工物流市場中的作用持續增強,專用化工運輸專線正逐漸成為主要生產商的主要運輸方式。 2025年5月,BASF和Lineas公司慶祝了路德維希港至安特衛普貨運專線的第1000次往返,凸顯了定期鐵路運輸在跨境化工運輸路線中發揮的核心作用。

預計到2031年,附加價值服務將以6.50%的複合年成長率成長,成為德國化工物流市場成長最快的物流職能。隨著化學生產商將工廠設備維護和支援服務外包,市場需求正轉向倉庫內的混合、重新貼標、桶裝填充、檢驗和文件支援等服務。德迅計畫於2026年在拉施塔特運作一座新的危險品倉庫,這一時間節點反映了隨著化學生產逐步復甦,市場對進一步成長的需求的預期。萊斯查科位於不來梅的工廠也傳遞出類似的訊息,該工廠將專用危險物品儲存與廣泛的合約物流職能相結合,以處理受管制化學品的流動。因此,在德國化工物流市場,能夠應對營運複雜性(而不僅僅是儲存產品)的倉庫職能的價值正變得越來越重要。

到2025年,危險化學品將佔德國化學品物流市場的63%,預計2031年將以5.67%的複合年成長率成長。這凸顯了符合ADR標準的運輸、經認證的倉儲設施和專用儲罐資產的核心作用。由於許多受管制物質仍需要專門的運輸和處理,即使在基礎化學品生產放緩的情況下,該領域在德國化學品物流市場中仍然佔據著重要的結構性地位。 2025年第二季度,Brentnach收購了德國危險物質倉儲設施GSZ Kaiserslautern,從而鞏固了其在中歐的業務基礎,並擴大了其在受管制物質領域的業務。此舉表明,即使在經濟低迷時期,營運商也看到了經認證的危險物質基礎設施的長期價值。

該領域的商業性邏輯正在發生變化,因為利潤率的品質不再僅僅取決於銷量,而是取決於認證、審核合規性和處理精度。在德國化工物流行業,獲得認證的運營商可以競爭長期基地和網路契約,而專業性較低的承運商則只能承接波動較大的零星運輸業務。在非危險品領域,由於技術壁壘降低以及可以透過更廣泛的貨運網路運輸大量貨物,價格壓力日益增大。另一方面,危險品物流則受惠於鋰離子電池處理等相關領域的成長,這些領域非常適合利用現有的危險物品儲存和配送能力。因此,在德國化工物流市場,能夠將設施、培訓、倉庫管理和合規支援整合到單一營運模式中的供應商繼續保持主導地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況及物流在化學工業中的作用

- 化工產業的支出趨勢

- 市場促進因素

- 加速國內化工產品生產的復甦

- 歐盟替代性爭議解決機制(EU-ADR)的合規性正在推動對專家的需求。

- 出口導向供應鏈的複雜性

- 基於化學園區的綜合物流拓展

- 物聯網坦克數位雙胞胎的引入

- 綠色氫能走廊的開發

- 市場限制因素

- 促進要素短缺和陸上貨運價格上漲

- 碳定價導致成本增加

- 溫控鐵路罐車短缺

- 萊茵河航道堵塞,船閘運作。

- 法律規範

- 價值鍊與通路結構分析

- 技術創新前景

- 波特五力模型

- 化學物質物流需求的變化

- 地緣政治事件對供應鏈轉型的影響

第5章 市場規模及成長預測(價值,2026-2031 年)

- 透過物流功能

- 運輸

- 道路運輸

- 航空

- 海路和內河水道

- 鐵路

- 倉儲、物流和庫存管理

- 附加價值服務及其他

- 運輸

- 依危險分類

- 危險化學品

- 無害化學品

- 按類型進行溫度控制

- 溫控(冷氣/暖氣)

- 非溫控型

- 產業最終用途

- 製藥

- 化妝品

- 石油和天然氣

- 特種化學品

- 其他最終用戶

- 按地區

- 北萊茵-威斯特法倫州

- 巴伐利亞

- 巴登-符騰堡州

- 其他州

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- HOYER Group

- Bertschi AG

- TALKE Group

- BASF SE

- Brenntag SE

- Imperial Chemical Logistics GmbH

- Rhenus Group

- Kuehne+Nagel

- DSV(incl. DB Schenker)

- DHL Supply Chain

- CEVA Logistics(CMA CGM)

- GEODIS

- Noerpel Group

- Paneuropa Transport

- Den Hartogh Logistics

- VTG Tanktainer

- Suttons Group

- Leschaco Group

- Stolt-Nielsen

- Univar Solutions

- Lanfer Logistik

- DACHSER SE

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany chemical logistics market size is expected to increase from USD 19.01 billion in 2025 to USD 19.75 billion in 2026 and reach USD 23.64 billion by 2031, growing at a CAGR of 3.67% over 2026-2031.

This report is Segmented by Service Type (Transportation, Warehousing & Distribution, Value-Added Services), by Hazard Class (Hazardous, Non-Hazardous), by Temperature Control (Temp-Controlled, Non-Temp-Controlled), by End Use Industry (Pharmaceutical, Cosmetics, Specialty Chemicals, and More), and by Region (NRW, Bavaria, Rest of States). The Market Forecasts are Provided in Terms of Value (USD).

Germany Chemical Logistics Market Trends and Insights

Accelerated Domestic Chemical Output Recovery: Fragile Uptick Creates Selective Logistics Demand

Germany's chemical and pharmaceutical base entered 2026 from a weak 2025 operating position, because industry production fell 3.3%, sales declined 3%, and capacity utilization averaged 72.5%. That backdrop keeps recovery in the Germany chemical logistics market selective rather than broad-based, because even a modest pickup in output lifts tanker use, warehouse turns, and packaging activity without fully restoring bulk volumes. This gives multi-service operators a buffer, since pharma-linked flows can support network utilization while bulk producers continue to run at lower rates. It also means providers that add capacity too early in the Germany chemical logistics market may face weaker margins if restocking fades before a broader production recovery takes hold. Asset allocation is therefore moving toward mixed networks that can serve both core chemical volumes and smaller, more regulated shipments.

EU-ADR Compliance Driving Specialist Demand: Specialist Capability Remains a Clear Divider

Compliance remains a direct driver of demand in the Germany chemical logistics market, as hazardous-goods transport requires trained staff, certified processes, and storage assets designed for regulated materials. Operators that can combine road transport, tank handling, repacking, inspection, and documentation support are in a stronger position when shippers want fewer counterparties. Leschaco's Bremen logistics center, commissioned in October 2025, added dedicated hazardous-goods infrastructure and classification-based storage capabilities, demonstrating how providers are investing in compliance-intensive demand. BASF's dTEX deployment at Ludwigshafen also points in the same direction, because it nearly fully automated truck dispatch and strengthened the digital side of site access, movement control, and workflow execution. In practice, the Germany chemical logistics market is rewarding providers that treat compliance as an operating capability rather than a back-office burden. That gap is likely to widen as customers put more value on audit readiness and managed service support.

Driver Shortage and Rising Road Freight Rates: Road Capacity Remains the Main Short-Term Constraint

Road transport still accounts for a large share of chemical movement in the Germany chemical logistics market, so any shortage of qualified drivers quickly tightens available capacity. The pressure is greater in hazardous-goods transport because chemical shippers need drivers who can meet stricter handling and safety requirements than those in standard freight operations. This raises the value of route planning, yard automation, and network density, yet those tools only soften the constraint rather than remove it. It also increases the appeal of intermodal configurations, especially for operators that can connect road legs with rail or terminal-based consolidation. In the Germany chemical logistics market, providers with tank capacity, rail access, and disciplined scheduling are better placed to defend margins when road freight tightens. Shippers are therefore placing more emphasis on resilience and mode flexibility in logistics tenders.

Other drivers and restraints analyzed in the detailed report include:

- Growing Chemiepark-Based Integrated Logistics: Site Logistics Continues to Deepen Switching Costs

- Adoption of IoT Tanks and Digital Twins: Digital Control Is Moving Into Daily Operations

- Rhine Waterway Congestion and Lock Downtime: Corridor Dependence Adds Network Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 59.2% of the Germany chemical logistics market share in 2025, confirming that core movement activity still anchors revenue across tankers, rail wagons, barges, and contract haulage. Road transport remained the largest part of this function because Germany's chemical production base is spread across clusters in North Rhine-Westphalia, Baden-Wurttemberg, and Bavaria, all of which depend on dense domestic freight links. Rail continued to strengthen its role in the Germany chemical logistics market as dedicated chemical shuttles moved closer to backbone status for large producers. BASF and Lineas marked the 1,000th round trip of their freight shuttle between Ludwigshafen and Antwerp in May 2025, underscoring that scheduled rail links are now central to selected cross-border chemical lanes.

Value-added services are projected to grow at a 6.50% CAGR through 2031, making this the fastest-expanding logistics function in the Germany chemical logistics market. Demand is shifting toward in-warehouse blending, relabeling, re-drumming, inspection, and documentation support, as chemical producers seek to protect plant capital and outsource support work. DACHSER is commissioning a new hazardous materials warehouse in Rastatt in 2026, and the timing reflects expectations of stronger demand as chemical output gradually improves. Leschaco's Bremen site adds the same message, because the facility combines dedicated hazardous storage with broader contract logistics capability for regulated chemical flows. As a result, the Germany chemical logistics market is placing greater value on warehouse capabilities that can absorb operational complexity rather than just storing product.

Hazardous chemicals accounted for 63% of the Germany chemical logistics market size in 2025 and are expanding at a CAGR of 5.67% through 2031, underscoring the central role of ADR-ready transport, certified storage, and specialized tank assets. This part of the Germany chemical logistics market remains structurally important even when basic chemical output is soft, because many regulated substances still require dedicated transport and handling. Brenntag strengthened its central European footprint in Q2 2025 through the acquisition of GSZ Kaiserslautern, a hazardous substance storage facility in Germany, expanding its operational base for regulated materials. That move indicates that operators still see long-term value in certified hazardous infrastructure even during a weaker cycle.

The commercial logic inside this segment is shifting, because margin quality now depends less on pure volume and more on certification, audit readiness, and handling precision. In the Germany chemical logistics industry, certified operators can compete for long-term site and network contracts, while less specialized carriers are pushed toward more volatile spot work. The non-hazardous side faces more pricing pressure, since larger bulk flows can be routed through broader freight networks with fewer technical barriers. Hazardous logistics also gains support from adjacent categories such as lithium-ion battery handling, which fit well with existing dangerous-goods storage and distribution capability. This keeps the Germany chemical logistics market tilted toward providers that can combine equipment, training, warehousing, and compliance support in one operating model.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing, Distribution and Inventory Management

- Value-added Services and Others

- Transportation

- By Hazard Class

- Hazardous Chemicals

- Non-hazardous Chemicals

- By Temperature Control

- Temperature-Controlled (Refrigerated/Heated)

- Non-Temperature-Controlled

- By End Use Industry

- Pharmaceutical

- Cosmetic

- Oil and Gas

- Specialty Chemicals

- Other End-Users

- By Region

- North Rhine-Westphalia

- Bavaria (Bayern)

- Baden-Wurttemberg

- Rest of States

List of Companies Covered in this Report:

- HOYER Group

- Bertschi AG

- TALKE Group

- BASF SE

- Brenntag SE

- Imperial Chemical Logistics GmbH

- Rhenus Group

- Kuehne+Nagel

- DSV (incl. DB Schenker)

- DHL Supply Chain

- CEVA Logistics (CMA CGM)

- GEODIS

- Noerpel Group

- Paneuropa Transport

- Den Hartogh Logistics

- VTG Tanktainer

- Suttons Group

- Leschaco Group

- Stolt-Nielsen

- Univar Solutions

- Lanfer Logistik

- DACHSER SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview & Role of Logistics in Chemical

- 4.2 Chemical Industry Spending Trends

- 4.3 Market Drivers

- 4.3.1 Accelerated Domestic Chemical Output Recovery

- 4.3.2 EU-ADR Compliance Driving Specialist Demand

- 4.3.3 Export-Oriented Supply-Chain Complexity

- 4.3.4 Growing Chemiepark-Based Integrated Logistics

- 4.3.5 Adoption of IoT Tanks and Digital Twins

- 4.3.6 Green-Hydrogen Corridor Build-Out

- 4.4 Market Restraints

- 4.4.1 Driver Shortage and Rising Road Freight Rates

- 4.4.2 Carbon-Pricing Linked Cost Escalation

- 4.4.3 Scarcity Of Temperature-Controlled Rail Tanks

- 4.4.4 Rhine Waterway Congestion and Lock Downtime

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Chemical Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing, Distribution and Inventory Management

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Hazard Class

- 5.2.1 Hazardous Chemicals

- 5.2.2 Non-hazardous Chemicals

- 5.3 By Temperature Control

- 5.3.1 Temperature-Controlled (Refrigerated/Heated)

- 5.3.2 Non-Temperature-Controlled

- 5.4 By End Use Industry

- 5.4.1 Pharmaceutical

- 5.4.2 Cosmetic

- 5.4.3 Oil and Gas

- 5.4.4 Specialty Chemicals

- 5.4.5 Other End-Users

- 5.5 By Region

- 5.5.1 North Rhine-Westphalia

- 5.5.2 Bavaria (Bayern)

- 5.5.3 Baden-Wurttemberg

- 5.5.4 Rest of States

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 HOYER Group

- 6.4.2 Bertschi AG

- 6.4.3 TALKE Group

- 6.4.4 BASF SE

- 6.4.5 Brenntag SE

- 6.4.6 Imperial Chemical Logistics GmbH

- 6.4.7 Rhenus Group

- 6.4.8 Kuehne+Nagel

- 6.4.9 DSV (incl. DB Schenker)

- 6.4.10 DHL Supply Chain

- 6.4.11 CEVA Logistics (CMA CGM)

- 6.4.12 GEODIS

- 6.4.13 Noerpel Group

- 6.4.14 Paneuropa Transport

- 6.4.15 Den Hartogh Logistics

- 6.4.16 VTG Tanktainer

- 6.4.17 Suttons Group

- 6.4.18 Leschaco Group

- 6.4.19 Stolt-Nielsen

- 6.4.20 Univar Solutions

- 6.4.21 Lanfer Logistik

- 6.4.22 DACHSER SE

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

中國化工物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

中國化工物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 全球化學品物流市場零售油氣物流:市佔率分析、產業趨勢及統計、成長預測(2026-2031)

全球化學品物流市場零售油氣物流:市佔率分析、產業趨勢及統計、成長預測(2026-2031) 化學品物流市場規模、佔有率、趨勢和預測:按類型、服務和地區分類,2026-2034年

化學品物流市場規模、佔有率、趨勢和預測:按類型、服務和地區分類,2026-2034年 零售油氣物流市場:依運輸方式、燃料類型、物流供應商類型及基礎設施類型分類-2026-2032年全球市場預測

零售油氣物流市場:依運輸方式、燃料類型、物流供應商類型及基礎設施類型分類-2026-2032年全球市場預測 化學品物流市場:依服務、運輸方式、最終用戶產業及地區分類。

化學品物流市場:依服務、運輸方式、最終用戶產業及地區分類。 2026年全球化學品物流市場報告化學品物流市場:依服務類型、化學品類型、運輸方式、包裝類型、溫度控制及最終用途產業分類-2026-2032年全球預測新加坡化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

2026年全球化學品物流市場報告化學品物流市場:依服務類型、化學品類型、運輸方式、包裝類型、溫度控制及最終用途產業分類-2026-2032年全球預測新加坡化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)