|

市場調查報告書

商品編碼

2072905

印度化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Chemical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

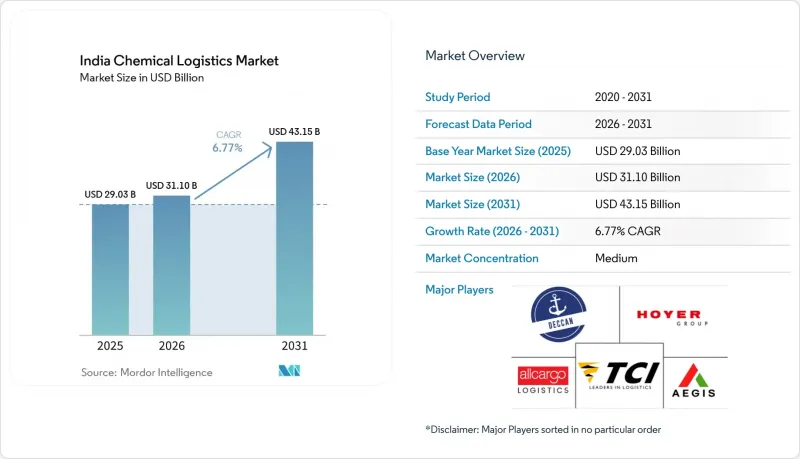

據 Mordor Intelligence 稱,印度化學品物流市場預計將從 2025 年的 290.3 億美元成長到 2026 年的 311 億美元,到 2031 年達到 431.5 億美元,2026 年至 2031 年的複合年成長率為 6.77%。

本報告按物流(運輸、倉儲和配送、附加價值服務)、危險品分類(危險品、非危險品)、溫度控制(溫控、非溫控)、最終用戶(藥品、化妝品、石油和天然氣、特種化學品、其他)以及地區(北部、中部、西部、東部、南部)進行分類。預測值以美元計價。

印度化工物流市場的趨勢與洞察

更嚴格的大宗貨物安全標準正在推動以合規為主導的物流改善。

強制認證和更嚴格的檢驗系統正推動印度化學品物流市場朝著設備可靠性提升和流程控制加強的方向發展。散貨運輸公司正在升級壓力測試設備、監控系統和文件流程,以確保在受監管的運輸路線上提供不間斷的服務。雖然這增加了所有承運商的固定成本,但擁有大規模運輸車隊的公司可以透過更高的貨運量和更長的客戶合約來分攤成本。因此,小規模承運商的盈利下降,尤其是在危險品運輸路線上,買家現在要求承運商提供經過審計的合規證明和更正式的安全措施。在整個預測期內,這種以合規主導的重組將使正規承運商在印度化學品物流市場中擁有更強的議價能力。

PM Gati Shakti 多式聯運走廊重新定義了化學品貨物的經濟性。

PM Gati Shakti計畫透過加強工廠、鐵路走廊、碼頭和港口之間的協調,正在改變印度化工物流市場的貨運經濟格局。其有效影響不僅限於提高幹線運輸速度,更在於提升散裝和容器化化工貨物的調度可靠性。隨著專用貨運基礎設施和碼頭貨運量的增加,化工托運人可以降低利潤率,制定更嚴格的運輸計畫。這正逐步將供應鏈從分散的公路環路轉變為鐵路和港口一體化的模式。未來,能夠提供走廊接入、化工倉儲和合規支援的物流供應商預計將在印度化工物流市場佔據更大的佔有率。

危險品貨運鐵路專用線的投資不足,阻礙了模式轉換。

在印度化學品物流市場中,許多托運人希望採用的運輸方式轉型因鐵路危險品專用線投資不足而受阻。這種差距在東部和中部走廊尤為明顯,這些地區的化工廠由於缺乏與鐵路連接的專用基礎設施,仍然嚴重依賴公路油輪運輸。與普通貨運設施相比,危險品專用線需要更多的資金、更多的許可證和更長的建設週期。因此,即使鐵路運輸能夠降低成本並提高安全性,道路運輸。

細分市場分析

至2025年,運輸業將佔印度化工物流市場62.93%的佔有率,成為本報告的主要成長驅動力。由於許多化工廠仍遠離道路運輸樞紐和港口,且買家需要靈活的跨工業區「最後一公里」配送服務,公路運輸仍將佔據主導地位。對於大多數運輸量有限、無法持續佔用專用鐵路或沿海貨運線路的中小型托運人而言,公路運輸也十分適用。隨著承運商拓展液體貨物運輸業務並利用容器化解決方案來適應更長的運輸路線,鐵路運輸的重要性仍然不減。

預計到2031年,附加價值服務將以9.60%的複合年成長率成長,成為印度化工物流行業成長最快的領域。化工托運人越來越傾向於由單一供應商提供集中管理服務,包括貨物追蹤、溫度記錄、海關支援、危險物品文件和異常處理。因此,倉儲、配送和庫存管理仍然至關重要,因為客戶要求在關鍵生產環節周圍提供更安全的儲存和更嚴格的庫存控制。由此,產業模式正從簡單的貨運轉向一體化服務模式,合規性和可視性與運輸本身同等重要。

到2025年,危險化學品將佔印度化學品物流市場佔有率的64.12%,並將成為成長最快的細分市場,到2031年複合年成長率將達到8.77%。這反映了石化產品、農藥和工業溶劑在印度化學品物流市場的重要角色。此細分市場規模龐大,不僅源自於其龐大的貨物吞吐量,也源自於每次運輸所帶來的更高服務負擔。危險品運輸認證的罐車、符合聯合國標準的包裝、完善的安全規程以及經過認證的司機,都為危險品運輸業務的收入成長做出了貢獻。

由於合規要求的複雜性,危險化學品運輸仍然是印度化學品物流行業中最難進入的領域。營運商要想在這個領域保持競爭力,需要符合印度環保署(PESO)標準的碼頭、維修的車輛、數位化記錄和訓練有素的員工。這使得規模較大的公司擁有強大的競爭優勢,並限制了新業務在高度監管的貨運市場中的快速擴張。小規模的業者由於缺乏大規模安全和文件管理所需的系統,往往面臨更大的利潤壓力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況及物流在化學工業中的作用

- 化工產業的支出趨勢

- 市場促進因素

- 加強散裝貨物安全標準(BIS 14687-2024,草案)

- 在總理加蒂沙克蒂計劃下擴大多模態化學品走廊

- 特種化學品出口激增(2013 會計年度比上年成長超過 10%)。

- 低溫運輸對高附加價值醫藥原料藥的需求

- CONCOR基於區塊鏈的貨車追蹤試點項目

- 印度港口軟性罐和ISO罐裝容器處理標準化

- 市場限制因素

- 鐵路危險品貨運專用線投資不足。

- 危險品油輪駕駛人技能不足

- 一線城市以外地區的冷藏倉庫儲存能力不足。

- LG Polymer事故後,維沙卡帕特南的保費飆升。

- 法律規範

- 價值鍊與通路結構分析

- 技術創新前景

- 波特五力模型

- 化學物質物流需求的變化

- 地緣政治事件對供應鏈轉型的影響

第5章 市場規模及成長預測(價值,2026-2031 年)

- 透過物流功能

- 運輸

- 道路運輸

- 航空

- 海路和內河航道

- 鐵路

- 倉儲、物流和庫存管理

- 附加價值服務及其他

- 運輸

- 依危險分類

- 危險化學品

- 無害化學品

- 按類型進行溫度控制

- 溫度控制(冷氣/暖氣)

- 非溫控型

- 產業最終用途

- 製藥

- 化妝品

- 石油和天然氣

- 特種化學品

- 其他最終用戶

- 按地區

- 北

- 中部

- 西方

- 東方

- 南

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- Aegis Logistics Limited

- Allcargo Logistics Ltd.

- Transport Corporation of India(TCI)

- Deccan Transcon Leasing Pvt. Ltd.

- HOYER Global Transport India

- Bertschi India Pvt. Ltd.

- Stolt Tank Containers India

- Balmer Lawrie & Co. Ltd.

- Kuehne+Nagel India

- DHL Supply Chain India

- Adani Logistics Ltd.

- Maersk India Pvt. Ltd.

- DSV India

- Gateway Distriparks Ltd.

- APL Logistics India

- NewPort Tank Containers India Pvt. Ltd.

- SAR Logistics

- CKB Global Logistics Pvt. Ltd.

- Crystal Group India

- Navkar Corporation Ltd.

- Shreeji Translogistics Ltd.

- RM Logistics Pvt. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the india chemical logistics market size is expected to increase from USD 29.03 billion in 2025 to USD 31.10 billion in 2026 and reach USD 43.15 billion by 2031, growing at a CAGR of 6.77% over 2026-2031.

This report is Segmented by Logistics (Transportation, Warehousing & Distribution, Value-Added Services), by Hazard Class (Hazardous, Non-Hazardous), by Temperature Control (Temperature-Controlled, Non-Temperature-Controlled), by End User (Pharmaceutical, Cosmetic, Oil & Gas, Specialty Chemicals, Others), and by Region (North, Central, West, East, South). The Forecasts are Provided in Terms of Value (USD).

India Chemical Logistics Market Trends and Insights

Tightening Bulk-Cargo Safety Norms Drive Compliance-Led Logistics Upgrades

Mandatory certification and stricter inspection discipline are pushing the India chemical logistics market toward greater equipment integrity and stronger process control. Bulk cargo operators are upgrading pressure-tested assets, monitoring systems, and documentation procedures to continue serving regulated lanes without disruption. This raises fixed costs for all participants, but larger fleets can spread that burden across higher shipment volumes and longer customer contracts. Smaller carriers, therefore, face weaker economics in hazardous lanes, especially where buyers now expect audited compliance and more formal safety safeguards. Over the forecast period, this compliance-led reset should leave organized operators with a stronger negotiating position in the India chemical logistics market.

PM Gati-Shakti Multimodal Corridors Redefine Chemical Freight Economics

PM Gati-Shakti is changing freight economics in the India chemical logistics market by improving links between plants, rail corridors, terminals, and ports. The practical effect is not only better line-haul speed, but also stronger schedule reliability for bulk and containerized chemical cargo. As more traffic moves through dedicated freight and cargo-terminal infrastructure, chemical shippers can work with leaner buffers and tighter dispatch planning. This is gradually shifting supply chains away from fragmented road-only loops and toward integrated rail and port combinations. Logistics providers that pair corridor access with chemical warehousing and compliance support are likely to capture a larger share of the India chemical logistics market over time.

Under-Investment in DG Cargo Rail Sidings Limits Rail Modal Shift

Under-investment in DG cargo rail sidings is slowing the modal shift that many shippers want in the India chemical logistics market. The gap is more visible in eastern and central corridors, where chemical plants still rely heavily on road tankers because dedicated rail-linked infrastructure is limited. Hazardous-commodity sidings also demand more capital, more approvals, and longer execution timelines than ordinary cargo facilities. That keeps road as the default choice for a large part of bulk DG traffic, even where rail could lower cost and improve safety. Until rail-linked hazardous cargo infrastructure improves, the India chemical logistics market will continue to carry avoidable trucking exposure in several inland corridors.

Other drivers and restraints analyzed in the detailed report include:

- Specialty-Chemical Export Surge Creates Dedicated Logistics Sub-Segments

- Cold-Chain Demand for Pharma APIs Redefines Temperature-Sensitive Chemical Logistics

- Driver-Skill Shortage Constrains Hazmat Tank-Truck Capacity Nationally

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 62.93% of the India chemical logistics market share in 2025, making it the report's core volume engine. Road continues to dominate because many chemical plants still sit away from railheads and ports, and buyers need flexible last-mile delivery across industrial belts. This also suits the large base of smaller shippers that move limited batches and cannot always fill dedicated rail or coastal lots. Rail is still gaining relevance in transportation, as carriers widen their liquid-cargo offerings and use containerized solutions to serve longer corridors.

Value-added services are projected to expand at a 9.60% CAGR through 2031, making it the fastest-growing function in the India chemical logistics industry. Chemical shippers increasingly want one provider to manage tracking, temperature logging, customs support, hazmat paperwork, and exception handling. Warehousing, distribution, and inventory management, therefore, remain important because customers are asking for safer storage and tighter stock control near major manufacturing belts. The result is a shift from pure freight execution toward bundled service models where compliance and visibility carry as much value as movement.

Hazardous chemicals accounted for 64.12% of the India chemical logistics market share in 2025 and are also the fastest-growing segment, with a CAGR of 8.77% through 2031, reflecting the significant role of petrochemicals, agrochemicals, and industrial solvents in the India chemical logistics market. The segment is large not only because of volume, but also because each shipment carries a heavier service burden. DG-rated tankers, UN-rated packaging, documented safety procedures, and endorsed drivers all lift the revenue value of hazardous cargo.

Hazardous chemicals remain the most defensible part of the India chemical logistics industry because compliance complexity raises the cost of entry. Operators need PESO-grade terminals, retrofitted fleets, digital records, and trained staff before they can compete credibly in this lane. That creates durable moats for organized companies and limits how quickly new carriers can scale in the regulated cargo market. It also means margin pressure tends to fall harder on smaller operators that lack the systems needed to manage safety and documentation at scale.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing, Distribution and Inventory Management

- Value-added Services and Others

- Transportation

- By Hazard Class

- Hazardous Chemicals

- Non-hazardous Chemicals

- By Temperature Control

- Temperature-Controlled (Refrigerated/Heated)

- Non-Temperature-Controlled

- By End Use Industry

- Pharmaceutical

- Cosmetic

- Oil and Gas

- Specialty Chemicals

- Other End-Users

- By Region

- North

- Central

- West

- East

- South

List of Companies Covered in this Report:

- Aegis Logistics Limited

- Allcargo Logistics Ltd.

- Transport Corporation of India (TCI)

- Deccan Transcon Leasing Pvt. Ltd.

- HOYER Global Transport India

- Bertschi India Pvt. Ltd.

- Stolt Tank Containers India

- Balmer Lawrie & Co. Ltd.

- Kuehne+Nagel India

- DHL Supply Chain India

- Adani Logistics Ltd.

- Maersk India Pvt. Ltd.

- DSV India

- Gateway Distriparks Ltd.

- APL Logistics India

- NewPort Tank Containers India Pvt. Ltd.

- SAR Logistics

- CKB Global Logistics Pvt. Ltd.

- Crystal Group India

- Navkar Corporation Ltd.

- Shreeji Translogistics Ltd.

- RM Logistics Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview & Role of Logistics in Chemical

- 4.2 Chemical Industry Spending Trends

- 4.3 Market Drivers

- 4.3.1 Tightening Bulk Cargo Safety Norms (BIS 14687-2024, Draft)

- 4.3.2 Growing Multi-Modal Chemical Corridors Under PM Gati-Shakti

- 4.3.3 Surge in Specialty-Chemical Exports (More Than 10 % YoY FY 25)

- 4.3.4 Cold-Chain Demand for High-Value Pharma APIs

- 4.3.5 Blockchain-Enabled Wagon Tracing Pilots by CONCOR

- 4.3.6 Standardization Of Flexitank & ISO-Tank Handling at Indian Ports

- 4.4 Market Restraints

- 4.4.1 Under-Investment in DG Cargo Rail Sidings

- 4.4.2 Driver-Skill Shortage for Haz-Mat Tank-Trucks

- 4.4.3 Limited Refrigerated Warehouse Capacity Outside Tier-1 Cities

- 4.4.4 High Insurance Premiums after Vizag LG Polymer Incident

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Chemical Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing, Distribution and Inventory Management

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Hazard Class

- 5.2.1 Hazardous Chemicals

- 5.2.2 Non-hazardous Chemicals

- 5.3 By Temperature Control

- 5.3.1 Temperature-Controlled (Refrigerated/Heated)

- 5.3.2 Non-Temperature-Controlled

- 5.4 By End Use Industry

- 5.4.1 Pharmaceutical

- 5.4.2 Cosmetic

- 5.4.3 Oil and Gas

- 5.4.4 Specialty Chemicals

- 5.4.5 Other End-Users

- 5.5 By Region

- 5.5.1 North

- 5.5.2 Central

- 5.5.3 West

- 5.5.4 East

- 5.5.5 South

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Aegis Logistics Limited

- 6.4.2 Allcargo Logistics Ltd.

- 6.4.3 Transport Corporation of India (TCI)

- 6.4.4 Deccan Transcon Leasing Pvt. Ltd.

- 6.4.5 HOYER Global Transport India

- 6.4.6 Bertschi India Pvt. Ltd.

- 6.4.7 Stolt Tank Containers India

- 6.4.8 Balmer Lawrie & Co. Ltd.

- 6.4.9 Kuehne+Nagel India

- 6.4.10 DHL Supply Chain India

- 6.4.11 Adani Logistics Ltd.

- 6.4.12 Maersk India Pvt. Ltd.

- 6.4.13 DSV India

- 6.4.14 Gateway Distriparks Ltd.

- 6.4.15 APL Logistics India

- 6.4.16 NewPort Tank Containers India Pvt. Ltd.

- 6.4.17 SAR Logistics

- 6.4.18 CKB Global Logistics Pvt. Ltd.

- 6.4.19 Crystal Group India

- 6.4.20 Navkar Corporation Ltd.

- 6.4.21 Shreeji Translogistics Ltd.

- 6.4.22 RM Logistics Pvt. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

中國化工物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

中國化工物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 全球化學品物流市場零售油氣物流:市佔率分析、產業趨勢及統計、成長預測(2026-2031)

全球化學品物流市場零售油氣物流:市佔率分析、產業趨勢及統計、成長預測(2026-2031) 化學品物流市場規模、佔有率、趨勢和預測:按類型、服務和地區分類,2026-2034年

化學品物流市場規模、佔有率、趨勢和預測:按類型、服務和地區分類,2026-2034年 零售油氣物流市場:依運輸方式、燃料類型、物流供應商類型及基礎設施類型分類-2026-2032年全球市場預測

零售油氣物流市場:依運輸方式、燃料類型、物流供應商類型及基礎設施類型分類-2026-2032年全球市場預測 化學品物流市場:依服務、運輸方式、最終用戶產業及地區分類。

化學品物流市場:依服務、運輸方式、最終用戶產業及地區分類。 2026年全球化學品物流市場報告化學品物流市場:依服務類型、化學品類型、運輸方式、包裝類型、溫度控制及最終用途產業分類-2026-2032年全球預測新加坡化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

2026年全球化學品物流市場報告化學品物流市場:依服務類型、化學品類型、運輸方式、包裝類型、溫度控制及最終用途產業分類-2026-2032年全球預測新加坡化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)