|

市場調查報告書

商品編碼

2066673

中東和非洲汽車黏合劑和密封劑市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle-East And Africa Automotive Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

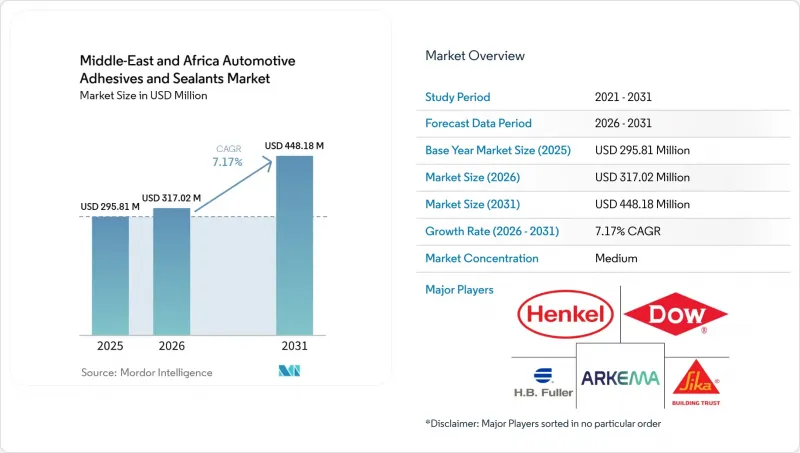

根據 Mordor Intelligence 預測,中東和非洲的汽車黏合劑和密封劑市場規模將從 2025 年的 2.9581 億美元成長到 2026 年的 3.1702 億美元,然後在 2031 年達到 4.4818 億美元,2026 年至 2031 年的複合年成長率為 7.17%。

本報告按樹脂類型(環氧樹脂、丙烯酸樹脂、氰基丙烯酸酯樹脂、聚氨酯樹脂、矽樹脂等)、技術(水性、熱熔、反應型、密封劑、溶劑型、紫外光固化)和地區(沙烏地阿拉伯、南非、阿拉伯聯合大公國、埃及、奈及利亞等中東和非洲國家)進行細分。市場預測以美元計價。

中東和非洲汽車黏合劑和密封劑市場的趨勢和見解。

提倡減重以達到地區咖啡館同等標準。

隨著汽車製造商(OEM)對企業平均燃油經濟性(CAFE)目標的提高,重點正轉向減輕車輛重量,因此結構環氧樹脂和聚氨酯取代了焊接過程。這些材料可在保持碰撞能量吸收能力的同時,將重量減輕高達15%。例如,曾有一個案例是將62%鋁製車身本體與180米環氧樹脂粘合,從而減輕了100公斤的重量,這凸顯了黏合劑在異種材料結構中的重要性。在Ceer和MG新工廠附近聯合建立混煉生產線的區域供應商可以確保長期供應,但他們需要進行更大的資本投資以滿足在地採購要求。

高溫氣候下電動車電池組的黏接要求

在環境溫度超過 50 度C 的條件下運作的鋰離子電池組需要使用導熱係數不超過 3.4 W/mK、阻燃等級達到 UL 94 V-0 的黏合劑。雙組分聚氨酯間隙填充劑符合這些要求,但它們也面臨一些挑戰,例如在無空調倉庫中適用期縮短。為了解決這個問題,化合物製造商正在使用潛熱固化催化劑來延長其工作時間。光是摩洛哥 20 GWh 的磷酸鐵鋰電池生產線預計每年就將消耗約 2,000 噸此類材料,促使該超級工廠在其廠區內安裝現場混合站。

MDI和環氧樹脂原料的價格波動

受區域性不可抗力因素影響,2026年第一季二苯基甲烷二異氰酸酯(MDI)現貨價格較上季上漲5.86%,供應量減少15%。環氧樹脂價格上漲至每公斤3.18美元,較去年同期上漲38.9%。這些成本上漲對簽訂固定價格OEM合約的複合材料生產商的利潤率帶來壓力,加速了向更具成本效益的丙烯酸類和VAE/EVA化學品的轉型。

細分市場分析

預計到2025年,環氧樹脂將在中東和非洲的汽車黏合劑和密封劑市場佔據17.46%的佔有率。這主要歸功於其25 MPa的搭接剪切強度和180 度C的工作溫度,這對於新型電動車平台中鋁和鋼的連接至關重要。同時,聚氨酯和矽樹脂繼續用於一些特定應用,例如玻璃安裝和引擎室蓋密封墊,這些應用需要彈性恢復和持續暴露於150 度C的高溫環境。

VAE/EVA樹脂固化時間不到3秒,VOC排放為零,非常適合用於熱熔頂篷和地毯背襯應用,預計到2031年將以7.31%的最高複合年成長率成長。先進的VAE等級樹脂具有更高的耐水解性,使其能夠在潮濕的沿海地區使用,並符合汽車氣味標準,從而在門板層壓和立柱裝飾等應用領域創造了商機。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 努力減輕重量,以達到地區咖啡館的同等標準。

- 高溫環境下電動車電池組的黏接要求

- OEM本地化政策正在促進一級製造商採購黏合劑。

- 海灣合作理事會國家的汽車後碰撞維修市場蓬勃發展

- 鋁製和複合材料車身的激增

- MEA電動車超級工廠的成長

- 市場限制因素

- 高揮發性MDI和環氧樹脂原料成本

- 對溶劑型化學產品實施嚴格的VOC法規

- 雙液體系低溫運輸物流的限制因素

- 自動化配藥系統熟練勞動力短缺

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 環氧樹脂

- 丙烯酸纖維

- 氰基丙烯酸酯

- 聚氨酯

- 矽酮

- VAE/EVA

- 其他樹脂

- 透過技術

- 水溶液

- 熱熔膠

- 反應性

- 密封劑

- 溶劑型

- 紫外線固化型

- 按地區

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 埃及

- 奈及利亞

- 其他中東和非洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- ACC Gulf

- Arkema

- Avery Dennison Corporation

- BASF

- DELO Industrial Adhesives

- Dow

- Dymax

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- PARKER HANNIFIN CORP

- Permabond LLC

- Pidilite Industries Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle-East and africa automotive adhesives and sealants market size is expected to grow from USD 295.81 million in 2025 to USD 317.02 million in 2026 and is forecast to reach USD 448.18 million by 2031 at 7.17% CAGR over 2026-2031.

This report is Segmented by Resin (Epoxy, Acrylic, Cyanoacrylate, Polyurethane, Silicone, and More), Technology (Water-Borne, Hot-Melt, Reactive, Sealants, Solvent-Borne, and UV-Cured), and Geography (Saudi Arabia, South Africa, United Arab Emirates, Egypt, Nigeria, and Rest of Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Middle-East And Africa Automotive Adhesives And Sealants Market Trends and Insights

Lightweighting Drive to Meet Regional CAFE-Equivalent Standards

Increasing Corporate Average Fuel Economy targets are pushing OEMs to reduce vehicle weight, leading to the substitution of welds with structural epoxies and polyurethanes. These materials provide up to 15% weight savings while maintaining crash energy absorption. For example, a 62% aluminum body-in-white bonded with 180 meters of epoxy reduced curb weight by 100 kg, highlighting the adhesive requirements for mixed-material constructions. Regional suppliers co-locating formulation lines near Ceer's and MG's new plants secure long-term volumes but must manage higher capital investments to meet local-content thresholds.

EV Battery-Pack Bonding Requirements in Hot Climates

Lithium-ion battery packs operating in ambient temperatures above 50 °C require adhesives with thermal conductivity up to 3.4 W/mK and UL 94 V-0 flame ratings. Two-part polyurethane gap fillers meet these requirements but face challenges such as reduced pot life in non-air-conditioned warehouses. To address this, formulators are extending working times using latent-cure catalysts. Morocco's 20 GWh LFP cell line alone is expected to consume approximately 2,000 tons of such materials annually, encouraging the setup of on-site mixing stations within the gigafactory premises.

Volatile MDI and Epoxy Raw-Material Costs

Spot prices for methylene diphenyl di-isocyanate (MDI) rose by 5.86% week-on-week in Q1 2026 after a regional force majeure reduced supply by 15%. Epoxy resin prices increased to USD 3.18 per kg, marking a 38.9% year-on-year rise. These cost increases are squeezing formulator margins on fixed-price OEM contracts and accelerating the transition to more cost-effective acrylic and VAE/EVA chemistries.

Other drivers and restraints analyzed in the detailed report include:

- OEM Localization Policies Boosting Tier-1 Adhesive Sourcing

- Aftermarket Collision-Repair Boom in GCC

- Stringent VOC Limits on Solvent-Borne Chemistries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy resins held 17.46% of the Middle-East and Africa automotive adhesives and sealants market share in 2025, attributed to their 25 MPa lap-shear strength and 180 °C service temperature, which are essential for aluminum-steel assemblies in new EV platforms. Meanwhile, polyurethane and silicone chemistries continue to serve specific applications such as glazing and under-hood gaskets, where elastic recovery or continuous exposure to 150 °C is required.

VAE/EVA resins are projected to grow at the fastest CAGR of 7.31% through 2031, driven by their sub-3-second set times and zero-VOC emissions, making them suitable for hot-melt headliner and carpet-backing applications. Enhanced hydrolysis resistance in advanced VAE grades supports their use in humid coastal regions while meeting interior-odor standards, creating opportunities in door-panel lamination and pillar trims.

List of Companies Covered in this Report:

- 3M

- ACC Gulf

- Arkema

- Avery Dennison Corporation

- BASF

- DELO Industrial Adhesives

- Dow

- Dymax

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- PARKER HANNIFIN CORP

- Permabond LLC

- Pidilite Industries Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lightweighting drive to meet regional CAFE-equivalent standards

- 4.2.2 EV battery-pack bonding requirements in hot climates

- 4.2.3 OEM localization policies boosting Tier-1 adhesive sourcing

- 4.2.4 Aftermarket collision-repair boom in GCC

- 4.2.5 Surge in aluminum and multi-material car bodies

- 4.2.6 Growth of MEA gigafactories for e-mobility

- 4.3 Market Restraints

- 4.3.1 Volatile MDI and epoxy raw-material costs

- 4.3.2 Stringent VOC limits on solvent-borne chemistries

- 4.3.3 Limited cold-chain logistics for two-part systems

- 4.3.4 Skilled-labor shortages for automated dispensing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Epoxy

- 5.1.2 Acrylic

- 5.1.3 Cyanoacrylate

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Hot-melt

- 5.2.3 Reactive

- 5.2.4 Sealants

- 5.2.5 Solvent-borne

- 5.2.6 UV-cured

- 5.3 By Geography

- 5.3.1 Saudi Arabia

- 5.3.2 South Africa

- 5.3.3 United Arab Emirates

- 5.3.4 Egypt

- 5.3.5 Nigeria

- 5.3.6 Rest of Middle-East and Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 ACC Gulf

- 6.4.3 Arkema

- 6.4.4 Avery Dennison Corporation

- 6.4.5 BASF

- 6.4.6 DELO Industrial Adhesives

- 6.4.7 Dow

- 6.4.8 Dymax

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Huntsman International LLC

- 6.4.12 ITW Performance Polymers

- 6.4.13 PARKER HANNIFIN CORP

- 6.4.14 Permabond LLC

- 6.4.15 Pidilite Industries Ltd.

- 6.4.16 PPG Industries, Inc.

- 6.4.17 RPM International Inc.

- 6.4.18 Sika AG

- 6.4.19 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

汽車黏合劑和密封劑市場預測至2034年-按產品類型、樹脂類型、技術、車輛類型、基材、應用、銷售管道和地區分類的全球分析

汽車黏合劑和密封劑市場預測至2034年-按產品類型、樹脂類型、技術、車輛類型、基材、應用、銷售管道和地區分類的全球分析 2026-2030年全球汽車密封劑市場

2026-2030年全球汽車密封劑市場 亞太地區汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

亞太地區汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 汽車黏合劑市場:2026-2032年全球市場預測(按產品類型、形態、車輛類型、應用、分銷管道和最終用戶分類)

汽車黏合劑市場:2026-2032年全球市場預測(按產品類型、形態、車輛類型、應用、分銷管道和最終用戶分類) 汽車黏合劑市場報告:按技術、樹脂類型、車輛類型、應用和地區分類(2026-2034 年)

汽車黏合劑市場報告:按技術、樹脂類型、車輛類型、應用和地區分類(2026-2034 年) 全球汽車黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球汽車黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球汽車黏合劑市場報告

2026年全球汽車黏合劑市場報告 汽車密封劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

汽車密封劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年