|

市場調查報告書

商品編碼

2066670

亞太地區汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Asia-Pacific Automotive Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

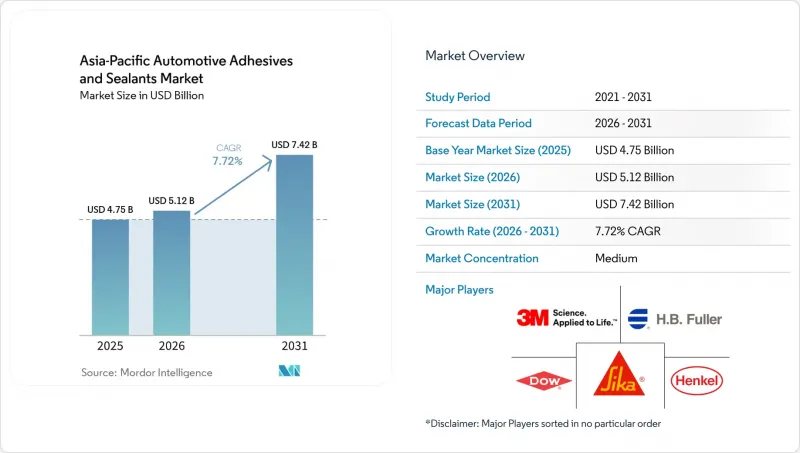

根據 Mordor Intelligence 預測,亞太地區汽車黏合劑和密封劑市場規模預計在 2025 年達到 47.5 億美元,2026 年達到 51.2 億美元,到 2031 年達到 74.2 億美元,2026 年至 2031 年的複合年成長率為 7.72%。

本報告按樹脂類型(丙烯酸樹脂、氰基丙烯酸酯樹脂、環氧樹脂、聚氨酯樹脂、矽樹脂、VAE/EVA樹脂及其他樹脂)、技術(熱熔型、反應型、密封型、溶劑型等)和地區(澳洲、中國、印度、印尼、日本、馬來西亞、新加坡、韓國、泰國及其他亞太地區)進行細分。市場預測以美元計價。

亞太地區汽車黏合劑和密封劑市場的趨勢和洞察。

OEM廠商朝向多材料白車身設計方向發展的趨勢

該地區的汽車製造商正將鋼、鋁、鎂和碳纖維增強塑膠整合到單一結構中,以減輕車輛總重8%至12%。這項改變使每輛車使用的黏合劑用量從約15公斤增加到超過25公斤。安賽樂米塔爾為其中國轎車採用的多階段整合工藝,結合了超高高抗張強度鋼和鋁製車門面板,這種組合由於存在電流腐蝕的風險,不適用於電阻點焊。 2025年,Ceres公司指定了一種環氧結構性黏著劑,該黏合劑無需表面預處理即可在鎂合金壓鑄副車架上實現超過10兆帕(MPa)的搭接剪切強度。據日本一級供應商稱,室溫固化的矽烷改質聚合物密封劑無需燒結爐,因此可以縮短生產週期。這些進步進一步鞏固了黏合劑在計畫於2027年至2030年間推出的大量生產平台上的應用。

基於中國VI和CAFE標準的輕量化要求

2026年1月,中國將實施「國六B」排放標準,屆時顆粒物排放限值將降低30%,氮氧化物(NOx)排放限值將降低50%,並透過引入實際道路排放氣體測試來加強法規執行力道。此外,汽車製造商(OEM)必須在2030年實現平均百公里油耗3.3公升的目標,這促使他們用黏合劑鋁材和複合材料取代鋼材,因此無需耗能的高能耗熱處理製程。現代和起亞也採用了類似的方法,在後行李箱蓋和引擎蓋中使用反應型熱熔膠,使每個開啟和關閉部分的重量減輕3至5公斤。隨著日本第四階段排放標準於2026年生效,減重要求將擴展到廂型車和輕型卡車,這將增加供應商對經認證的單組分聚氨酯的需求。

異氰酸酯和環氧樹脂原料價格波動

2025年全年,二苯基甲烷二異氰酸酯(MDI)供應意外中斷以及原油價格波動導致現貨市場劇烈波動,使得東協地區小規模複合材料生產商的利潤率下降了200-300個基點。 2026年初,環氧樹脂市場疲軟,迫使一些供應商延後研發和產能擴張計畫。 DIC公司位於千葉縣的新環氧樹脂工廠獲得了津貼以確保國內供應,這凸顯了為應對原料風險而進行大量資本投資的必要性。雖然矽烷改質聚合物替代品有助於減少對異氰酸酯的依賴,但由於其在120 度C以上溫度下會發生熱老化,因此應用仍然有限。

細分市場分析

聚氨酯具有400%的延伸率和濕氣固化特性,適用於黏合不同基材,預計到2025年將佔據亞太地區汽車黏合劑和密封劑市場27.25%的佔有率。漢高公司的導熱聚氨酯產品導熱係數為1.2至3.4瓦/米·開爾文(W/m·K),廣泛用於電動車(EV)模組的黏合。環氧樹脂黏合劑適用於引擎室內等需要耐高溫達180 度C的應用,而介電強度超過10千伏/毫米(kV/mm)的矽酮黏合劑則較適用於高壓電池組。

醋酸乙烯酯/乙烯/乙烯-醋酸乙烯酯 (VAE/EVA) 水性系統目前市佔率較小,但預計到 2031 年將以 6.55% 的複合年成長率成長。其成本績效效益高,且符合揮發性有機化合物 (VOC) 法規,因此適用於印度的車頂內襯和車門內裝板等應用。這些黏合劑有助於目的地設備製造商 (OEM) 滿足日本對汽車內裝甲醛濃度的最高限值(100 微克/立方米,µg/m³),而無需投資紫外線 (UV) 燈。在國內供應商區域產能提升的推動下,VAE/EVA黏合劑市場預計將顯著擴張。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 原始設備製造商 (OEM) 更傾向於採用多材料白車身設計

- 根據中國六號排放標準和CAFE標準規定的減重義務

- 電動車電池組對墊圈的需求增加

- 將生物基聚氨酯化學技術商業化的新創公司。

- 低表面能複合黏合劑的出現

- 市場限制因素

- 異氰酸酯和環氧樹脂原料價格波動

- 原始設備製造商為方便維修而努力採用機械緊固方式

- 日本和韓國對揮發性有機化合物(VOC)有嚴格的規定。

- 二級供應商在機器人點膠編程方面存在技能差距

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 氰基丙烯酸酯

- 環氧樹脂

- 聚氨酯

- 矽酮

- VAE/EVA

- 其他樹脂

- 透過技術

- 熱熔膠

- 反應性

- 密封劑

- 溶劑型

- 紫外光固化黏合劑

- 水溶液

- 按地區

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 馬來西亞

- 新加坡

- 韓國

- 泰國

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)和排名分析

- 公司簡介

- 3M

- Arkema

- Ashland

- DIC Corporation

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International

- ITW Performance Polymers

- Jowat SE

- PARKER HANNIFIN CORP

- Permabond LLC

- Pidilite Industries Ltd.

- PPG Industries, Inc.

- Shanghai Huitian New Material Co., Ltd

- SHINSUNG PETROCHEMICAL

- Sika AG

- THREEBOND INTERNATIONAL, INC

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific automotive adhesives and Sealants Market size is projected to be USD 4.75 billion in 2025, USD 5.12 billion in 2026, and reach USD 7.42 billion by 2031, growing at a CAGR of 7.72% from 2026 to 2031.

This report is Segmented by Resin (Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA, Other Resins), Technology (Hot Melt, Reactive, Sealants, Solvent-Borne, and More), and Geography (Australia, China, India, Indonesia, Japan, Malaysia, Singapore, South Korea, Thailand, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Automotive Adhesives And Sealants Market Trends and Insights

OEM Preference for Multi-Material Body-in-White Designs

Automakers in the region are integrating steel, aluminum, magnesium, and carbon-fiber-reinforced polymers within single structures to reduce curb weight by 8-12%. This change has increased adhesive usage from approximately 15 kilograms to over 25 kilograms per vehicle. ArcelorMittal's multi-phase integration process for Chinese sedans combines ultra-high-strength steel with aluminum closures, a pairing unsuitable for resistance spot-welding due to the risk of galvanic corrosion. In 2025, Seres adopted magnesium die-cast subframes, specifying epoxy structural adhesives that achieve lap-shear strength exceeding 10 megapascals (MPa) without requiring surface pretreatment. Japanese tier-one suppliers report that silyl-modified-polymer sealants, which cure at ambient temperatures, reduce cycle times by eliminating the need for bake ovens. These advancements are embedding adhesives more deeply into high-volume platforms scheduled for launch between 2027 and 2030.

Weight-Reduction Mandates Under China VI and CAFE Norms

China's implementation of China VI B standards in January 2026 will reduce particulate matter thresholds by 30% and nitrogen oxide (NOx) limits by 50%, while real-driving-emissions testing will enhance enforcement. Additionally, original equipment manufacturers (OEMs) must achieve a fleet average of 3.3 liters per 100 kilometers (L/100 km) by 2030, driving the substitution of steel with adhesive-bonded aluminum and composites that eliminate the need for energy-intensive heat tunnels. Hyundai and Kia are following a similar approach, using reactive hot-melts on tailgates and hoods to reduce weight by 3-5 kilograms per closure. Japan's Stage 4 regulations, effective in 2026, extend lightweighting requirements to vans and mini-trucks, increasing supplier demand for qualified one-component polyurethanes.

Volatility in Isocyanate and Epoxy Feedstock Prices

Unplanned methylene diphenyl diisocyanate (MDI) outages and fluctuations in crude oil prices caused spot-market variations through 2025, reducing the margins of smaller ASEAN formulators by 200-300 basis points. The epoxy market weakened in early 2026, leading some suppliers to delay research and development initiatives and capacity expansion plans. DIC's new Chiba epoxy unit, subsidized to ensure domestic supply, highlights the significant capital investment required to manage raw material risks. While silyl-modified polymer alternatives help reduce isocyanate exposure, they remain limited by thermal-aging constraints above 120°C.

Other drivers and restraints analyzed in the detailed report include:

- Uptick in EV Battery-Pack Gasketing Demand

- Start-Ups Commercializing Bio-Based Polyurethane Chemistries

- OEM Push Toward Mechanical Fastening for Ease of Repair

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane is expected to account for 27.25% of the Asia-Pacific Automotive Adhesives & Sealants market share in 2025, driven by its 400% elongation and moisture-curing properties, which are suitable for mixed-substrate joints. Henkel's thermal-conductive polyurethane grades, offering thermal conductivity of 1.2-3.4 watts per meter-kelvin (W/m*K), are widely used in bonding electric vehicle (EV) modules. Epoxy adhesives are utilized in under-hood applications requiring resistance to temperatures up to 180°C, while silicone adhesives are preferred for high-voltage battery packs due to their dielectric strength exceeding 10 kilovolts per millimeter (kV/mm).

Vinyl acetate ethylene/ethylene vinyl acetate (VAE/EVA) water-borne systems, though currently smaller in market share, are projected to grow at a compound annual growth rate (CAGR) of 6.55% through 2031. Their cost-effectiveness and compliance with volatile organic compound (VOC) regulations make them suitable for applications such as headliners and door panels in India. These adhesives help original equipment manufacturers (OEMs) meet Japan's in-cabin formaldehyde limit of 100 micrograms per cubic meter (µg/m3) without requiring ultraviolet (UV) lamp investments. The market for VAE/EVA adhesives is expected to expand significantly, supported by increased regional production capacity from domestic suppliers.

List of Companies Covered in this Report:

- 3M

- Arkema

- Ashland

- DIC Corporation

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International

- ITW Performance Polymers

- Jowat SE

- PARKER HANNIFIN CORP

- Permabond LLC

- Pidilite Industries Ltd.

- PPG Industries, Inc.

- Shanghai Huitian New Material Co., Ltd

- SHINSUNG PETROCHEMICAL

- Sika AG

- THREEBOND INTERNATIONAL, INC

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 OEM preference for multi-material body-in-white designs

- 4.2.2 Weight-reduction mandates under China VI and CAFE norms

- 4.2.3 Uptick in EV battery pack gasketing demand

- 4.2.4 Start-ups commercialising bio-based polyurethane chemistries

- 4.2.5 Emergence of low-surface-energy composite adhesives

- 4.3 Market Restraints

- 4.3.1 Volatility in isocyanate and epoxy feedstock prices

- 4.3.2 OEM push toward mechanical fastening for ease-of-repair

- 4.3.3 Stringent VOC caps in Japan and South Korea

- 4.3.4 Skill-gap in robot-dispensing programming at Tier-2 plants

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Hot-Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 UV-Cured Adhesives

- 5.2.6 Water-borne

- 5.3 By Geography

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Singapore

- 5.3.8 South Korea

- 5.3.9 Thailand

- 5.3.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/(%)Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 DIC Corporation

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Huntsman International

- 6.4.9 ITW Performance Polymers

- 6.4.10 Jowat SE

- 6.4.11 PARKER HANNIFIN CORP

- 6.4.12 Permabond LLC

- 6.4.13 Pidilite Industries Ltd.

- 6.4.14 PPG Industries, Inc.

- 6.4.15 Shanghai Huitian New Material Co., Ltd

- 6.4.16 SHINSUNG PETROCHEMICAL

- 6.4.17 Sika AG

- 6.4.18 THREEBOND INTERNATIONAL, INC

- 6.4.19 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

汽車黏合劑和密封劑市場預測至2034年-按產品類型、樹脂類型、技術、車輛類型、基材、應用、銷售管道和地區分類的全球分析

汽車黏合劑和密封劑市場預測至2034年-按產品類型、樹脂類型、技術、車輛類型、基材、應用、銷售管道和地區分類的全球分析 2026-2030年全球汽車密封劑市場

2026-2030年全球汽車密封劑市場 中東和非洲汽車黏合劑和密封劑市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

中東和非洲汽車黏合劑和密封劑市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 汽車黏合劑市場:2026-2032年全球市場預測(按產品類型、形態、車輛類型、應用、分銷管道和最終用戶分類)

汽車黏合劑市場:2026-2032年全球市場預測(按產品類型、形態、車輛類型、應用、分銷管道和最終用戶分類) 汽車黏合劑市場報告:按技術、樹脂類型、車輛類型、應用和地區分類(2026-2034 年)

汽車黏合劑市場報告:按技術、樹脂類型、車輛類型、應用和地區分類(2026-2034 年) 全球汽車黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球汽車黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球汽車黏合劑市場報告

2026年全球汽車黏合劑市場報告 汽車密封劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

汽車密封劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年