|

市場調查報告書

商品編碼

2066672

北美汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)North America Automotive Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

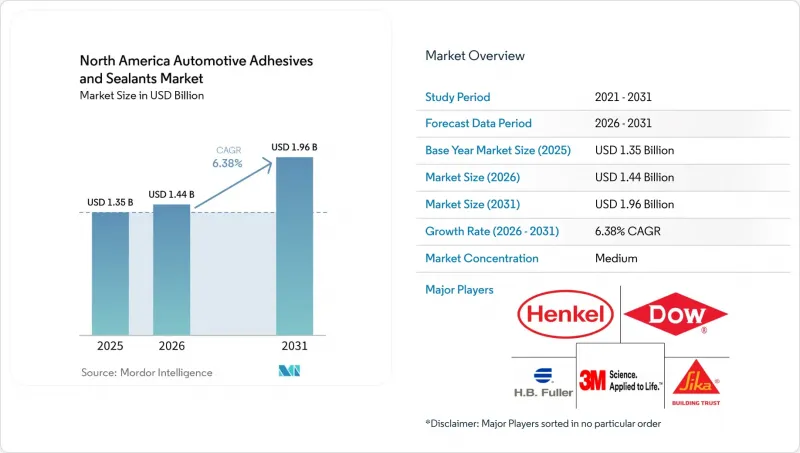

根據 Mordor Intelligence 預測,北美汽車黏合劑和密封劑市場將從 2025 年的 13.5 億美元成長到 2026 年的 14.4 億美元,然後在 2031 年達到 19.6 億美元,2026 年至 2031 年的複合年成長率為 6.38%。

本報告按樹脂類型(聚氨酯、丙烯酸酯、氰基丙烯酸酯、環氧樹脂、矽酮、VAE/EVA 及其他樹脂)、技術類型(反應型、熱熔型、密封型、溶劑型、UV固化型和水性型)以及地區(美國、加拿大和墨西哥)進行細分。市場預測以美元(USD)為單位。

北美汽車黏合劑和密封劑市場的趨勢和洞察。

電動車專用黏合劑需求激增

對超級工廠的投資正在重新定義黏合劑的規格。Panasonic能源位於堪薩斯州的工廠要求環氧樹脂的導熱係數超過 2 W/m*K,而大眾汽車位於安大略省的工廠已批准使用矽基導熱界面材料,該材料在 3000 次熱循環後仍能保持 80% 的粘合強度。特斯拉和 LG 在密西根州的合資企業正在使用可在 10 秒內完全固化的紫外線固化化學品,用於點膠機器人,從而實現自動化產品的生產,縮短生產週期,同時又不影響介電性能。一項價值 1 億美元的聯邦津貼正在支持固態電池封裝的研究和開發,這推動了對符合 UL 94 V-0 阻燃標準的阻燃黏合劑的需求。

在整個美墨加協定範圍內強制減重。

美墨加協定(USMCA)的在地採購要求規定正在加速從鋼材轉向鋁材和碳纖維複合材料的轉變,而這些材料無法焊接。預計2025年7月,墨西哥製造車輛的在地化含量合規率將達到76.1%,兩年內成長8個百分點。在福特F-150 Lightning和通用Silverado EV車型中,採用耐衝擊環氧樹脂將鋁擠壓件粘合到鋼製副車架上,而相關的表面處理底漆使黏合劑系統的成本增加了8%至12%。

石油基樹脂原料價格波動

BASF和萬華意外停產導致2026年3月TDI現貨價格上漲8.13%。同時,關鍵原料苯胺受天然氣價格飆升和海運費用上漲的影響,在2024年第四季上漲了18%。 2025年,由於中國生產商為達到碳排放強度目標而減產,丙烯酸單體供應收緊了12%,為北美混煉商的利潤率帶來了壓力。儘管混煉商採用了季度調整條款,但受年度合約約束的一級供應商在2025年面臨4000萬至6000萬美元的利潤下滑。

細分市場分析

由於聚氨酯適用於結構黏合、降低噪音、振動與聲振粗糙度 (NVH) 以及接縫密封,預計到 2025 年,其在北美汽車黏合劑和密封劑市場的需求佔比將達到 25.35%。然而,隨著內裝製造商優先考慮低溫活化,預計 VAE/EVA 樹脂到 2031 年將以 6.45% 的複合年成長率成長。低溫活化可降低 30% 的烘箱能耗,並有助於回收。環氧樹脂仍然是碰撞安全關鍵連接件(需要超過 25 MPa 的拉伸強度)的必備材料,而矽膠樹脂由於其在 -40 度C至 +150 度C的溫度範圍內具有穩定性,在電池溫度控管應用中的使用日益增多。丙烯酸樹脂(包括氰基丙烯酸酯)因其無需固定裝置即可在 60 秒內固化的特點,在感測器支架等小眾快速組裝應用中備受關注。此外,“其他樹脂”,如聚醯亞胺,在隔熱應用中獲得了很高的利潤率。

VAE/EVA的成長與OEM廠商提高再生材料含量的努力相契合。同時,漢高公司60%生物基聚氨酯的問世表明,聚氨酯可以在不犧牲5 MPa以下搭接剪切強度的前提下實現永續性目標。環氧樹脂供應商正在開發增強型樹脂,以解決不同材料連接處熱膨脹係數的差異。矽膠樹脂生產商正致力於將介電強度提高到20 kV/mm以上,以滿足高壓電池設計的要求。氰基丙烯酸酯樹脂開發商正在推出紫外光和濕氣固化相結合的技術,用於光照無法到達的區域,從而拓展其在ADAS模組自動化生產線的應用。總體而言,樹脂的選擇正朝著兼顧機械性能、降低能耗和提高使用壽命結束後的可回收性這三個方面的化學成分方向發展,這反映了北美汽車黏合劑和密封劑市場正在發生的變化。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車專用擔保要求的激增

- 美墨加協定中的輕量化要求

- 透過OEM過渡到複合材料白車身結構

- 電池超級工廠快速擴張

- 一級製造商引進智慧固化生產線

- 愛爾蘭共和國的供應鏈回流

- 市場限制因素

- 石油基樹脂原料價格波動

- 高溫下可回收性的局限性

- 美國職業安全與健康管理局對異氰酸酯暴露的監測

- 生物基化學品規模化生產的風險

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 聚氨酯

- 丙烯酸纖維

- 氰基丙烯酸酯

- 環氧樹脂

- 矽酮

- VAE/EVA

- 其他樹脂

- 透過技術

- 反應性

- 熱熔膠

- 密封劑

- 溶劑型

- 紫外線固化型

- 水溶液

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Arkema

- Ashland

- Avery Dennison Corp.

- Dow

- DuPont

- Dymax

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International

- ITW Performance Polymers

- Jowat SE

- MasterBond

- Matrix Adhesives Group

- PARKER HANNIFIN CORP

- Permabond LLC

- Sika AG

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america automotive adhesives and sealants market size is expected to grow from USD 1.35 billion in 2025 to USD 1.44 billion in 2026 and is forecast to reach USD 1.96 billion by 2031 at 6.38% CAGR over 2026-2031.

This report is Segmented by Resin (Polyurethane, Acrylic, Cyanoacrylate, Epoxy, Silicone, VAE/EVA, and Other Resins), Technology (Reactive, Hot-Melt, Sealants, Solvent-Borne, UV-Cured, and Water-Borne), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Automotive Adhesives And Sealants Market Trends and Insights

Surging EV-Specific Bonding Requirements

Gigafactory investments are redefining adhesive specifications. Panasonic Energy's Kansas plant requires epoxies with thermal conductivity exceeding 2 W/m*K, while Volkswagen's Ontario facility has approved silicone thermal interface materials that retain 80% bond strength after 3,000 thermal cycles. Dispensing robots at the Tesla-LG joint venture in Michigan utilize UV-cured chemistries that achieve a tack-free state in under 10 seconds, enabling automation-compatible products that reduce cycle times without compromising dielectric performance. Federal grants worth USD 100 million are supporting R&D into solid-state cell encapsulation, driving demand for flame-retardant adhesives that meet UL 94 V-0 flammability standards.

Lightweighting Mandates Across USMCA

USMCA content rules are accelerating the transition from steel to aluminum and carbon-fiber composites, which cannot be welded. Compliance rates for Mexican-origin vehicles reached 76.1% by July 2025, an increase of 8 percentage points over two years. Ford's F-150 Lightning and GM's Silverado EV rely on crash-resistant epoxies to bond aluminum extrusions to steel subframes, with associated surface-preparation primers now contributing an 8-12% increase in adhesive system costs.

Raw-Material Volatility for Petro-Resins

Unplanned outages at BASF and Wanhua caused TDI spot prices to rise by 8.13% in March 2026, while aniline, a key feedstock, increased by 18% in Q4 2024 due to gas price spikes and higher ocean freight costs. Acrylic monomer supply tightened by 12% in 2025 as Chinese producers reduced output to meet carbon-intensity targets, squeezing margins for North American compounders. While formulators implemented quarterly adjustment clauses, Tier-1 suppliers bound by annual contracts faced USD 40-60 million in margin erosion during 2025.

Other drivers and restraints analyzed in the detailed report include:

- OEM Shift to Mixed-Material Body-in-White

- Rapid Growth of Battery Gigafactories

- Limited High-Temperature Recyclability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane accounted for 25.35% of the 2025 demand in the North America automotive adhesives and sealants market due to its adaptability in structural bonding, NVH damping, and seam sealing. However, VAE/EVA resins are anticipated to grow at a 6.45% CAGR through 2031, as interior-trim manufacturers prioritize low-temperature activation, which reduces oven energy consumption by 30% and supports recycling efforts. Epoxy remains critical for crash-critical joints requiring tensile strength above 25 MPa, while silicone usage is increasing in battery thermal-management applications due to its stability across a temperature range of -40 °C to +150 °C. Acrylics, including cyanoacrylates, are gaining traction in niche rapid-assembly applications, such as sensor brackets, due to their sub-60-second fixture-free curing times. Additionally, "other resins," such as polyimides, command premium margins in thermal-barrier applications.

The growth of VAE/EVA aligns with OEM commitments to increase recycled content, while Henkel's 60% bio-based polyurethane demonstrates how polyurethanes can meet sustainability goals without compromising lap-shear strength below 5 MPa. Epoxy suppliers are developing toughened grades to address differential expansion in mixed-material joints, and silicone formulators are enhancing dielectric strength beyond 20 kV/mm to meet the requirements of high-voltage battery designs. Cyanoacrylate developers are integrating UV and moisture curing for shadowed areas, expanding their use in automated ADAS module production lines. Overall, resin selection is shifting toward chemistries that balance mechanical performance with reduced energy consumption and improved end-of-life recyclability, reflecting the ongoing transition in the North America automotive adhesives and sealants market.

List of Companies Covered in this Report:

- 3M

- Arkema

- Ashland

- Avery Dennison Corp.

- Dow

- DuPont

- Dymax

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International

- ITW Performance Polymers

- Jowat SE

- MasterBond

- Matrix Adhesives Group

- PARKER HANNIFIN CORP

- Permabond LLC

- Sika AG

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging EV-specific bonding requirements

- 4.2.2 Lightweighting mandates across USMCA

- 4.2.3 OEM shift to mixed-material body-in-white

- 4.2.4 Rapid growth of battery gigafactories

- 4.2.5 Tier-1 adoption of smart curing lines

- 4.2.6 IRA-driven reshoring of supply chains

- 4.3 Market Restraints

- 4.3.1 Raw-material volatility for petro-resins

- 4.3.2 Limited high-temperature recyclability

- 4.3.3 OSHA scrutiny on isocyanate exposure

- 4.3.4 Scale-up risk for bio-based chemistries

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Polyurethane

- 5.1.2 Acrylic

- 5.1.3 Cyanoacrylate

- 5.1.4 Epoxy

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Reactive

- 5.2.2 Hot-melt

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 UV-cured

- 5.2.6 Water-borne

- 5.3 By Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 Avery Dennison Corp.

- 6.4.5 Dow

- 6.4.6 DuPont

- 6.4.7 Dymax

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Huntsman International

- 6.4.11 ITW Performance Polymers

- 6.4.12 Jowat SE

- 6.4.13 MasterBond

- 6.4.14 Matrix Adhesives Group

- 6.4.15 PARKER HANNIFIN CORP

- 6.4.16 Permabond LLC

- 6.4.17 Sika AG

- 6.4.18 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

汽車黏合劑和密封劑市場預測至2034年-按產品類型、樹脂類型、技術、車輛類型、基材、應用、銷售管道和地區分類的全球分析

汽車黏合劑和密封劑市場預測至2034年-按產品類型、樹脂類型、技術、車輛類型、基材、應用、銷售管道和地區分類的全球分析 2026-2030年全球汽車密封劑市場

2026-2030年全球汽車密封劑市場 中東和非洲汽車黏合劑和密封劑市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

中東和非洲汽車黏合劑和密封劑市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 汽車黏合劑市場:2026-2032年全球市場預測(按產品類型、形態、車輛類型、應用、分銷管道和最終用戶分類)

汽車黏合劑市場:2026-2032年全球市場預測(按產品類型、形態、車輛類型、應用、分銷管道和最終用戶分類) 汽車黏合劑市場報告:按技術、樹脂類型、車輛類型、應用和地區分類(2026-2034 年)

汽車黏合劑市場報告:按技術、樹脂類型、車輛類型、應用和地區分類(2026-2034 年) 全球汽車黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球汽車黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球汽車黏合劑市場報告

2026年全球汽車黏合劑市場報告 汽車密封劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

汽車密封劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年