|

市場調查報告書

商品編碼

2066671

歐洲汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Europe Automotive Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

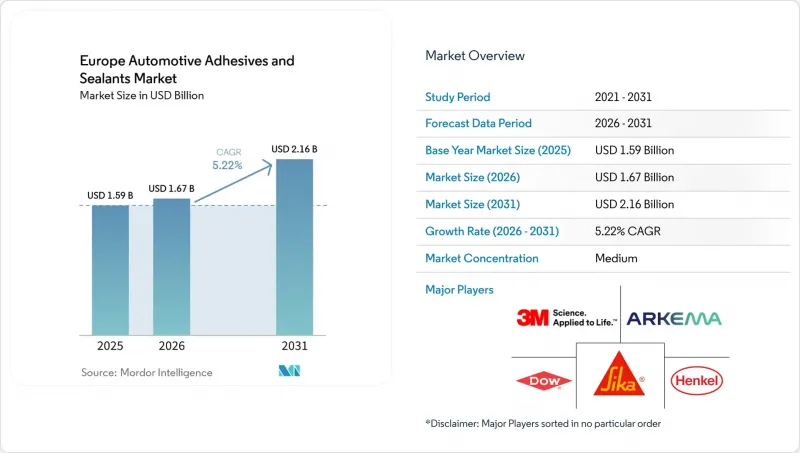

據 Mordor Intelligence 稱,2025 年歐洲汽車黏合劑和密封劑市值為 15.9 億美元,預計到 2031 年將從 2026 年的 16.7 億美元成長至 21.6 億美元,預測期(2026-2031 年)的複合年成長率為 5.22%。

本報告按樹脂類型(丙烯酸樹脂、氰基丙烯酸酯樹脂、環氧樹脂、聚氨酯樹脂、矽樹脂、VAE/EVA樹脂及其他樹脂)、技術(熱熔膠、反應型膠、密封膠、溶劑型膠、UV固化黏合劑和水性膠)以及地區(法國、德國、義大利、俄羅斯、西班牙、英國及其他歐洲國家)進行細分。市場預測以美元(USD)為單位。

歐洲汽車黏合劑和密封劑市場的趨勢和洞察

促進電動車和內燃機汽車的減重

鋁材、複合材料和複合結構正採用高剝離強度的聚氨酯和環氧樹脂黏合劑來取代傳統的點焊。這些黏合方法能有效分散載重並降低應力集中。 Hydro公司透過以鋁製零件取代鋼製零件,在保持90%材料可回收性的同時,減輕了30%的重量。 BMWi系列車型採用彈性體增強環氧樹脂將碳纖維粘合到鋁材上,解決了熱膨脹係數不匹配的問題,並保護了纖維。奧迪利用人工智慧(AI)驅動的有限元素模擬來評估潛在的化學成分,從而改進了配方開發週期並縮短了認證前置作業時間。歐盟的「汽車一攬子計畫」(包括18億歐元(21億美元)的電池激勵措施)鼓勵汽車製造商將車輛重量減輕100-150公斤。這一趨勢正在推動從傳統螺栓到現代黏合解決方案的轉變。

歐盟的VOC減量法規正在加速低VOC化學成分的開發。

歐盟指令2004/42/EC規定面漆中揮發性有機化合物(VOC)含量上限為每公升420公克(g/l)。該法規鼓勵配方研發人員採用更環保的方法,特別是水性和紫外光固化方法。漢高股份公司(Henkel AG & Co. KGaA)的「AQUENCE PL 5101」是一款單組分水性黏合劑,避免了雙組分混合黏合劑通常4小時操作期帶來的廢棄物。它還允許使用肥皂水清洗生產線。德莎(Tesa)的「52215超低VOC膠帶」在暖通空調(HVAC)行業中日益普及,它能夠粘合回收的聚丙烯密封件,並符合VDA 278客艙空氣品質標準。然而,這款膠帶也存在一個缺點:其初始黏性較低,導致固化時間較長。 Toyochem 的 UV 固化「TOYOMELT P-201」系列產品解決了這個難題,無需使用溶劑即可即時固化,耐熱溫度高達 100 度C。

異氰酸酯價格波動

2026年初,中東地區緊張局勢升級,導致原物料供應路線中斷,二苯基甲烷二異氰酸酯(MDI)和甲苯二異氰酸酯(TDI)價格大幅上漲。據ICIS報告顯示,多元醇的平均價格在一週內上漲了每噸450美元。BASF和亨斯邁等製造商將價格提高了每噸100至300歐元(117.16至351.48美元),這對沒有長期合約的二級複合材料供應商構成了挑戰。運轉率維持在82%左右,預計在中國新增產能轉向出口導向產品之前,產能利用率的提升空間有限。電動車(EV)利潤率本已捉襟見肘,原始設備製造商(OEM)不願承擔成本上漲的壓力,這進一步擠壓了複合材料供應商的息稅折舊攤銷前利潤(EBITDA)。

細分市場分析

預計到2025年,聚氨酯的銷售額將佔總銷售額的26.63%。這主要得益於其高剝離強度(超過20兆帕)和抗衝擊性,這些特性對於電池機殼和車身本體組裝至關重要。漢高和陶氏等公司正在投資2,000萬美元,擴大在德國的反應熱熔膠生產線,以確保供應。同時,隨著汽車製造商(OEM)擴大採用低揮發性有機化合物(VOC)解決方案用於儀表板和頂棚,預計到2031年,醋酸乙烯酯和乙烯/乙烯-乙烯醋酸乙烯(VAE/EVA)水性化學品的複合年成長率將達到5.88%。環氧樹脂在模組封裝應用中仍佔據主導地位,一些創新技術不斷湧現,例如名古屋大學開發的環氧樹脂和熱可塑性橡膠(TPE)混合材料,其抗衝擊強度和長期耐久性可提升至傳統環氧樹脂的22倍。 WEVO-CHEMIE 的「WEVOSIL 28015 FL」等矽膠因其在高溫電池密封應用中表現出的彈性恢復能力,以及在 -40 度C至 +85 度C溫度循環下的耐受性,而備受關注。

VAE/EVA的成長並不意味著聚氨酯的衰落。相反,預計這兩種化學體系將共存,滿足車輛不同區域對動作溫度和模量的各種要求。例如,贏創的VPS SIVO 260矽烷促進劑可將聚氨酯與聚碳酸酯的黏合力提高27%,從而確保其在透明車頂結構中的效用。此外,隨著循環經濟相關法規推動BETA-氨基酯可剝離環氧樹脂的研究,未來十年內,此類樹脂在使用後可能更容易分解。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車和內燃機汽車的輕量化努力

- 歐盟的VOC減量法規正在加速低VOC化學技術的應用。

- 歐洲電動車電池組產量快速成長

- 線上機器人點膠技術提升了OEM廠商的加工能力。

- 整合式感測器的「智慧」結構性黏著劑現已上市。

- 市場限制因素

- 異氰酸酯價格波動

- 遵守 REACH 法規的成本

- 電池生產線高黏度塗佈設備短缺

- 新型生物基系統的OEM認證出現延誤

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 氰基丙烯酸酯

- 環氧樹脂

- 聚氨酯

- 矽酮

- VAE/EVA

- 其他樹脂

- 透過技術

- 熱熔膠

- 反應性

- 密封劑

- 溶劑型

- 紫外光固化黏合劑

- 水溶液

- 按地區

- 法國

- 德國

- 義大利

- 俄羅斯

- 西班牙

- 英國

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)和排名分析

- 公司簡介

- 3M

- Alpha Adhesives & Sealants

- Anabond Ltd.

- Arkema

- BASF

- DELO Industrial Adhesives

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian Adhesive

- Huntsman International LLC

- ITW Performance Polymers

- Jowat SE

- PARKER HANNIFIN CORP

- Permabond LLC

- PPG Industries

- Sika AG

- Uniseal Inc.

- Wacker Chemie AG

- Wurth Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe automotive adhesives and sealants market size was valued at USD 1.59 billion in 2025 and is estimated to grow from USD 1.67 billion in 2026 to reach USD 2.16 billion by 2031, at a CAGR of 5.22% during the forecast period (2026-2031).

This report is Segmented by Resin (Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA, Other Resins), Technology (Hot Melt, Reactive, Sealants, Solvent-Borne, UV-Cured Adhesives, Water-Borne), and Geography (France, Germany, Italy, Russia, Spain, United Kingdom, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Automotive Adhesives And Sealants Market Trends and Insights

Lightweighting Drive for EV and ICE Vehicles

Aluminum, composites, and mixed-material architectures are replacing traditional spot-welds with high-peel polyurethane and epoxy bonds. These bonding methods distribute loads effectively and reduce stress concentrations. Hydro achieved a 30% reduction in mass by replacing steel closures with aluminum, maintaining the material's 90% recyclability. BMW's i-Series used elastomer-toughened epoxies to bond carbon fiber to aluminum, addressing thermal-expansion mismatches and protecting the fibers. Audi has improved its formulation cycles by utilizing artificial intelligence (AI)-driven finite-element simulations to evaluate potential chemistries, reducing qualification lead times. The European Union (EU) Automotive Package, which includes a EUR 1.8 billion (USD 2.10 billion) battery incentive, is encouraging original equipment manufacturers (OEMs) to reduce vehicle weight by 100-150 kilograms. This trend is driving the shift from traditional bolts to modern adhesive solutions.

EU VOC-Reduction Regulations Accelerate Low-VOC Chemistries

Directive 2004/42/EC has set a cap of 420 grams per liter (g/l) for volatile organic compounds (VOCs) in topcoats. This regulation is nudging formulators towards more eco-friendly routes, specifically water-borne and ultraviolet (UV)-cure methods. Henkel AG & Co. KGaA's AQUENCE PL 5101, a one-component water-borne adhesive, eliminates the typical four-hour pot-life waste associated with two-part mixes. It also allows line flushes using soapy water. Tesa's 52215 Ultra-Low-VOC tape is making progress in the heating, ventilation, and air conditioning (HVAC) sector, bonding recycled polypropylene seals while adhering to VDA 278 cabin-air standards. However, this tape has a drawback: its lower initial tack extends fixture times. Toyochem's UV-curable TOYOMELT P-201 series addresses this challenge, offering instant curing and 100°C heat resistance, all without the use of solvents.

Isocyanate Price Volatility

In early 2026, prices for Methylene Diphenyl Diisocyanate (MDI) and Toluene Diisocyanate (TDI) increased significantly due to Middle-East tensions disrupting feedstock supply routes. ICIS reported a polyol midpoint price increase of USD 450 per ton within a week. Producers such as BASF and Huntsman implemented price increases ranging from EUR 100 to 300 (USD 117.16 to 351.48) per ton, creating challenges for Tier-2 formulators without long-term contracts. Utilization rates remain around 82%, providing limited relief until new Chinese production capacity transitions to export-grade materials. Original Equipment Manufacturers (OEMs), already under pressure from electric vehicle (EV) margin constraints, are resisting cost pass-throughs, further compressing formulation EBITDA.

Other drivers and restraints analyzed in the detailed report include:

- Surge in European EV Battery-Pack Production

- In-Line Robotic Dispensing Boosts OEM Throughput

- REACH Chemical-Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane accounted for 26.63% of the projected 2025 revenue, driven by its high peel strength (greater than 20 MPa) and impact resilience, which are critical for battery enclosures and body-in-white assemblies. Companies such as Henkel and Dow have invested USD 20 million in expanding a German reactive hot-melt production line to ensure supply. Meanwhile, vinyl acetate ethylene/ethylene vinyl acetate (VAE/EVA) water-borne chemistries are expected to grow at a compound annual growth rate (CAGR) of 5.88% through 2031, as original equipment manufacturers (OEMs) increasingly adopt low-volatile organic compound (VOC) solutions for dashboards and roof-liners. Epoxies continue to dominate module potting applications, with innovations such as Nagoya University's epoxy-thermoplastic elastomer (TPE) hybrid demonstrating 22X impact strength, indicating long-term durability. Silicones, including WEVO-CHEMIE's WEVOSIL 28015 FL, are gaining traction in high-temperature battery seals, meeting the demands of -40°C to +85°C cycling with elastic recovery.

The growth of VAE/EVA does not signal the decline of polyurethanes; instead, both chemistries are expected to coexist, addressing varying requirements for operating temperature and modulus across vehicle zones. For instance, Evonik's VPS SIVO 260 silane promoters enhance polycarbonate adhesion by 27%, ensuring polyurethane remains relevant for transparent roof architectures. Additionally, circular-economy regulations are driving research into beta-amino-ester debondable epoxies, signaling a potential shift toward easier end-of-life disassembly in the coming decade.

List of Companies Covered in this Report:

- 3M

- Alpha Adhesives & Sealants

- Anabond Ltd.

- Arkema

- BASF

- DELO Industrial Adhesives

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian Adhesive

- Huntsman International LLC

- ITW Performance Polymers

- Jowat SE

- PARKER HANNIFIN CORP

- Permabond LLC

- PPG Industries

- Sika AG

- Uniseal Inc.

- Wacker Chemie AG

- Wurth Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lightweighting drive for EV and ICE vehicles

- 4.2.2 EU VOC-reduction regulations accelerate low-VOC chemistries

- 4.2.3 Surge in European EV battery-pack production

- 4.2.4 In-line robotic dispensing boosts OEM throughput

- 4.2.5 Sensor-embedded "smart" structural adhesives emerge

- 4.3 Market Restraints

- 4.3.1 Isocyanate price volatility

- 4.3.2 REACH chemical-compliance costs

- 4.3.3 Shortage of high-viscosity dosing equipment for battery lines

- 4.3.4 OEM certification delays for novel bio-based systems

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Hot-Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 UV-Cured Adhesives

- 5.2.6 Water-borne

- 5.3 By Geography

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/(%)Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Alpha Adhesives & Sealants

- 6.4.3 Anabond Ltd.

- 6.4.4 Arkema

- 6.4.5 BASF

- 6.4.6 DELO Industrial Adhesives

- 6.4.7 Dow

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Hubei Huitian Adhesive

- 6.4.11 Huntsman International LLC

- 6.4.12 ITW Performance Polymers

- 6.4.13 Jowat SE

- 6.4.14 PARKER HANNIFIN CORP

- 6.4.15 Permabond LLC

- 6.4.16 PPG Industries

- 6.4.17 Sika AG

- 6.4.18 Uniseal Inc.

- 6.4.19 Wacker Chemie AG

- 6.4.20 Wurth Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

汽車黏合劑和密封劑市場預測至2034年-按產品類型、樹脂類型、技術、車輛類型、基材、應用、銷售管道和地區分類的全球分析

汽車黏合劑和密封劑市場預測至2034年-按產品類型、樹脂類型、技術、車輛類型、基材、應用、銷售管道和地區分類的全球分析 2026-2030年全球汽車密封劑市場

2026-2030年全球汽車密封劑市場 中東和非洲汽車黏合劑和密封劑市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

中東和非洲汽車黏合劑和密封劑市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美汽車黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 汽車黏合劑市場:2026-2032年全球市場預測(按產品類型、形態、車輛類型、應用、分銷管道和最終用戶分類)

汽車黏合劑市場:2026-2032年全球市場預測(按產品類型、形態、車輛類型、應用、分銷管道和最終用戶分類) 汽車黏合劑市場報告:按技術、樹脂類型、車輛類型、應用和地區分類(2026-2034 年)

汽車黏合劑市場報告:按技術、樹脂類型、車輛類型、應用和地區分類(2026-2034 年) 全球汽車黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球汽車黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球汽車黏合劑市場報告

2026年全球汽車黏合劑市場報告 汽車密封劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

汽車密封劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年