|

市場調查報告書

商品編碼

2066664

歐洲EVA黏合劑:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031年)Europe EVA Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

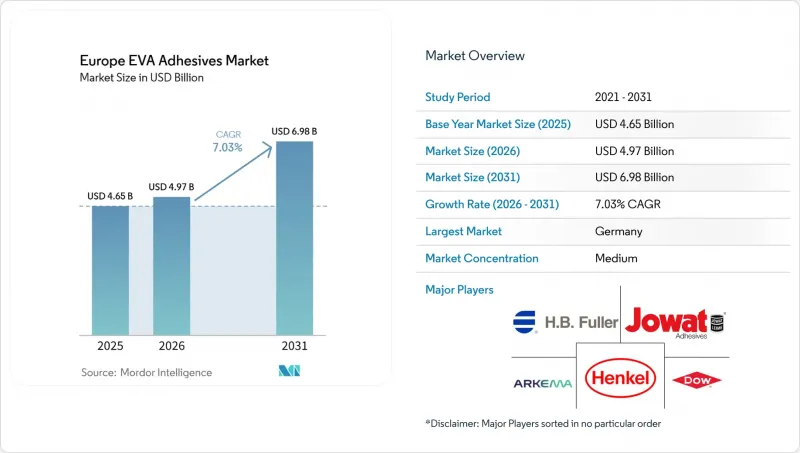

根據 Mordor Intelligence 預測,EVA黏合劑市場規模預計將在 2025 年達到 46.5 億美元,2026 年達到 49.7 億美元,到 2031 年達到 69.8 億美元,2026 年至 2031 年的複合年成長率為 7.03%。

本報告按技術(熱熔膠、溶劑型膠、水性膠)、終端用戶產業(航太、汽車、建築施工、鞋類和皮革、醫療、包裝、木工和細木工以及其他終端用戶產業)和地區(法國、德國、義大利、俄羅斯、西班牙、英國以及其他歐洲國家)進行細分。市場預測以美元計價。

歐洲EVA黏合劑市場趨勢與洞察

電子商務推動包裝需求爆炸性成長

電子商務物流商面臨許多挑戰,例如自動分揀過程中1.2公尺的跌落高度以及-15 度C至35 度C的溫度波動,這些都對澱粉基黏合劑的性能提出了嚴峻考驗。 EVA熱熔膠的釋放時間僅需8-12秒,即可在短短3秒內達到1.5牛/25毫米的初始黏合強度。這種高效性使得瓦楞紙板生產線能夠以400公尺/分鐘的速度運作而不會出現密封失效。儘管小包裹處理量已趨於穩定,但向親和性更高的單一材料包裝盒的轉變仍在持續推動黏合劑用量的成長。新的規範建議使用醋酸乙烯酯含量低於5%(重量比)的共聚物,並符合RecyClass和塑膠回收再利用的要求。阿科瑪於2024年12月收購陶氏的軟包裝黏合劑業務,凸顯了該行業對無溶劑配方的關注,尤其是那些符合雀巢過渡限制的配方。未來兩年,隨著轉換器製造商完成低伏安系統的測試,預計其影響將達到頂峰。隨著將這些系統推廣到多個工廠的計劃正在進行中,這一趨勢將尤為明顯。

歐盟的「翻新浪潮」正在推動建築黏合劑市場的發展。

「翻新浪潮」計畫旨在2030年將歐洲建築維修率提高到每年2%,並計畫投資722億歐元用於外牆和屋頂維修。用於將保溫板黏合到石牆上的EVA改性分散體,可避免機械錨固件造成的熱橋效應,並符合歐盟生態標章VOC標準。義大利和西班牙在這方面取得了快速進展,這得益於兩國政府的復甦計劃,這些計劃將歐盟35-40%的資金用於節能維修。水性EVA系統具有25-30分鐘的快速黏合時間——是醋酸乙烯酯均聚物的兩倍——這減輕了承包商的工作量,尤其是在熟練工人短缺15-20%的情況下。

在高性能細分市場中,POE 和 TPU 的競爭日益激烈。

基於茂金屬的聚烯彈性體是電動車電池組的理想候選材料,因為它們在應用中可減輕40%的重量,並且在150 度C下具有2000小時的耐熱性。固化的熱塑性聚氨酯(TPU)反應樹脂可實現15-18 MPa的重疊剪切強度,使鞋類製造商能夠完全消除縫合。這些替代材料的價格溢價為20-30%,但在需要減輕重量和高溫環境的應用中,它們具有顯著的價值。作為回應,EVA供應商正在推出VA含量為33-40%的等級,此舉導致原料成本增加了25-30%。

細分市場分析

到2025年,水性分散體將佔市場需求的45.20%。然而,預計到2031年,熱熔膠將以7.89%的年複合成長率(CAGR)超越水性分散體。由於無需乾燥箱,製造商每生產1公斤產品可節省0.8-1.2千瓦時的電力。這還能騰出15-20公尺的生產線空間,考慮到目前高昂的能源價格,這是一個顯著的優勢。在汽車產業,一級供應商利用機器人組裝中8-12秒的開啟時間,實現了每小時50輛的生產效率。與水性替代品所需的停留時間相比,這相當於大幅增加了40%。在材料性能方面,可交聯EVA熱熔膠在80 度C下可達到12-15兆帕的搭接剪切強度。這顯示其與傳統的反應型聚氨酯產品相比具有成本競爭力。由於職場對揮發性有機化合物(VOC)含量的限制日益嚴格,預計溶劑型聚氨酯的市佔率明年將繼續下降。雖然高階鞋履和皮革製品等小眾應用領域仍有其市場,但反應型聚氨酯正逐步蠶食這些領域的市場佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務推動包裝需求爆炸性成長

- 歐盟的「翻新浪潮」正在推動建築黏合劑市場的發展。

- 向基於 REACH 法規的低 VOC 水基平台過渡

- 電動車製造商正在推動電動車內裝減重。

- 高價值的生物基EVA等級產品正擴大被高階市場所採用。

- 市場限制因素

- 原料(乙烯和VAM)價格波動

- 在高性能細分市場中,POE 和 TPU 的競爭日益激烈。

- 廢舊EVA黏合層壓板回收利用的障礙

- 價值鏈分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 透過技術

- 熱熔膠

- 溶劑型

- 水溶液

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 鞋類和皮革

- 衛生保健

- 包裝

- 木工和細木工

- 其他終端用戶產業

- 國家

- 法國

- 德國

- 義大利

- 俄羅斯

- 西班牙

- 英國

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M Company

- Arkema

- Avery Dennison Corp.

- BASF SE

- Beardow Adams

- Celanese Corp.

- Dow

- Follmann Chemie GmbH

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman Corp.

- Jowat SE

- Klebchemie MG Becker GmbH

- LyondellBasell Industries

- Paramelt BV

- Sika AG

- Soudal Holding NV

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the EVA-based adhesives market size is projected to be USD 4.65 billion in 2025, USD 4.97 billion in 2026, and reach USD 6.98 billion by 2031, growing at a CAGR of 7.03% from 2026 to 2031.

This report is Segmented by Technology (Hot Melt, Solvent-Borne, Water-Borne), End-User Industry (Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, Woodworking and Joinery, Other End-User Industries), and Geography (France, Germany, Italy, Russia, Spain, United Kingdom, Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

Europe EVA Adhesives Market Trends and Insights

Explosive Growth of E-commerce-driven Packaging Demand

E-commerce shippers face challenges with automated sortation drops of 1.2 m and temperature fluctuations ranging from -15 °C to 35 °C, testing the limits of starch glues. EVA hot melts, offering 8-12 second open times, achieve a green strength of 1.5 N/25 mm in just three seconds. This efficiency allows corrugators to operate at 400 m/min without seal failures. While parcel growth has stabilized, the shift towards mono-material boxes, which are more compatible with recycling, continues to drive up adhesive volumes. New specifications now favor copolymers with less than 5 wt% vinyl acetate, as they successfully meet the RecyClass- Association of Plastic Recyclers (APR) CG-01 protocols. Arkema's acquisition of Dow's flexible-packaging adhesive line in December 2024 highlights the industry's focus on solvent-free formulations, especially those aligning with Nestle's migration limits. Over the next two years, as converters complete trials on low-VA systems, their influence is set to peak, especially with plans to scale these systems across multiple plants.

EU Renovation Wave Boosting Construction Adhesives

By 2030, the Renovation Wave aims to boost Europe's building-renovation rate to 2% annually, directing EUR 72.2 billion towards facade and roof enhancements. EVA-modified dispersions, which bond insulation panels to masonry, sidestep the thermal bridges associated with mechanical anchors and meet the EU Ecolabel VOC standards. Thanks to their national recovery plans, which allocate 35-40% of EU funds for energy retrofits, Italy and Spain are rapidly advancing. Water-borne EVA systems, boasting tack times of 25-30 minutes, twice that of vinyl-acetate homopolymers, are easing labor demands for installers, especially amidst a 15-20% shortage in trade skills.

Rising Competition from POE & TPU in High-Performance Niches

Metallocene polyolefin elastomers, which shave off 40% of application weight, endure 2,000 hours at 150 °C, making them prime candidates for EV battery packs. After curing, thermoplastic-polyurethane reactives achieve a lap-shear strength of 15-18 MPa, allowing footwear brands to eliminate stitching altogether. While these alternatives come with a 20-30% price premium, they offer significant value in weight-sensitive or high-temperature settings. In response, EVA suppliers are introducing grades with 33-40% VA content, but this move escalates raw material costs by 25 to 30%.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Low-VOC/Water-borne Platforms Under REACH

- OEM Push for Lightweight EV Interiors

- End-of-Life Recycling Barriers for EVA-Bonded Laminates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, water-borne dispersions commanded a 45.20% share of the market demand. However, hot melts are on a trajectory to surpass them, boasting a 7.89% CAGR projected through 2031. By eliminating drying ovens, manufacturers can save between 0.8 to 1.2 kWh for every kilogram produced. This also frees up 15 to 20 meters of line space, which is a crucial advantage given the current surge in energy prices. In the automotive segment, tier-1 suppliers are capitalizing on 8 to 12 second open times for robotic assembly, achieving a rate of 50 units per hour. This marks a significant 40% improvement over the dwell times required for water-borne alternatives. In terms of material performance, crosslinkable EVA hot melts are now achieving lap-shear strengths of 12 to 15 MPa at 80 °C. This presents a cost-effective challenge to traditional polyurethane reactives. For solvent-borne systems, a continued decline is expected as workplace VOC ceilings tighten next year. While niche applications in luxury footwear and leather remain, even in these segments, polyurethane reactives are gradually encroaching on market share.

List of Companies Covered in this Report:

- 3M Company

- Arkema

- Avery Dennison Corp.

- BASF SE

- Beardow Adams

- Celanese Corp.

- Dow

- Follmann Chemie GmbH

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman Corp.

- Jowat SE

- Klebchemie M.G. Becker GmbH

- LyondellBasell Industries

- Paramelt B.V.

- Sika AG

- Soudal Holding N.V.

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive growth of e-commerce-driven packaging demand

- 4.2.2 EU Renovation Wave boosting construction adhesives

- 4.2.3 Shift to low-VOC/water-borne platforms under REACH

- 4.2.4 OEM push for light-weight EV interiors

- 4.2.5 High-VA, bio-based EVA grades gaining premium adoption

- 4.3 Market Restraints

- 4.3.1 Feed-stock (ethylene and VAM) price volatility

- 4.3.2 Rising competition from POE and TPU in high-performance niches

- 4.3.3 End-of-life recycling barriers for EVA-bonded laminates

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Hot Melt

- 5.1.2 Solvent-borne

- 5.1.3 Water-borne

- 5.2 By End-User Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Footwear and Leather

- 5.2.5 Healthcare

- 5.2.6 Packaging

- 5.2.7 Woodworking and Joinery

- 5.2.8 Other End-user Industries

- 5.3 By Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M Company

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corp.

- 6.4.4 BASF SE

- 6.4.5 Beardow Adams

- 6.4.6 Celanese Corp.

- 6.4.7 Dow

- 6.4.8 Follmann Chemie GmbH

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Huntsman Corp.

- 6.4.12 Jowat SE

- 6.4.13 Klebchemie M.G. Becker GmbH

- 6.4.14 LyondellBasell Industries

- 6.4.15 Paramelt B.V.

- 6.4.16 Sika AG

- 6.4.17 Soudal Holding N.V.

- 6.4.18 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

眼科黏合劑市場規模、佔有率和成長分析:按產品類型、應用、適應症、最終用戶和地區分類-2026-2033年產業預測

眼科黏合劑市場規模、佔有率和成長分析:按產品類型、應用、適應症、最終用戶和地區分類-2026-2033年產業預測 2026-2030年全球黏合劑市場

2026-2030年全球黏合劑市場 丙烯酸樹脂黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、分銷方式、地區和競爭格局分類,2021-2031年智慧黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年

丙烯酸樹脂黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、分銷方式、地區和競爭格局分類,2021-2031年智慧黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年 織物黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

織物黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 電子產業PUR黏合劑市場規模、佔有率和成長分析:按功能/類型、應用、終端用戶產業、包裝、分銷管道和地區分類-2026-2033年產業預測亞太地區EVA黏合劑:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

電子產業PUR黏合劑市場規模、佔有率和成長分析:按功能/類型、應用、終端用戶產業、包裝、分銷管道和地區分類-2026-2033年產業預測亞太地區EVA黏合劑:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 北美基材黏合劑市場規模、佔有率和趨勢分析報告:按樹脂類型、技術、應用、國家和細分市場預測(2026-2033 年)美國黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

北美基材黏合劑市場規模、佔有率和趨勢分析報告:按樹脂類型、技術、應用、國家和細分市場預測(2026-2033 年)美國黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測

全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測