|

市場調查報告書

商品編碼

2062380

織物黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Fabric Glue - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

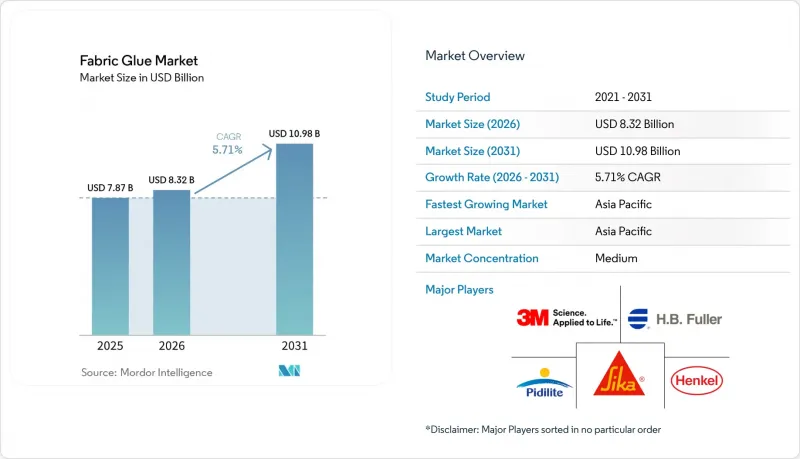

根據 Mordor Intelligence 預測,織物黏合劑市場規模將從 2025 年的 78.7 億美元成長到 2026 年的 83.2 億美元,到 2031 年將達到 109.8 億美元,2026 年至 2031 年的複合年成長率為 5.71%。

本報告黏合劑產品類型(臨時性和永久性織物黏合劑)、基材(水性(PVA、EVA 等)、分銷管道(線上市場等)、終端用戶產業(服飾等)以及地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球織物黏合劑市場趨勢及洞察

快速隨選時尚週期

快時尚平台每天推出數千個新的SKU(庫存單位),促使工廠從傳統的手工縫紉轉向自動化噴塗或輥塗粘合生產線,從而降低30-40%的人工成本。採用熱塑性熱熔膠黏合的聚酯纖維和尼龍混紡織物,其剝離強度可超過15 N/25 mm,足以滿足可經受10-20次洗滌的服裝需求。反應型聚氨酯和乙烯-醋酸乙烯酯共聚物因其即時黏性和極短的固化時間而成為首選。供應商最佳化流變性能,以確保在高速輸送機系統中高效混煉,避免拉絲現象。中國的加工商正在採用能夠以可變模式塗覆黏合劑的雙頭機器人,從而減少過度塗覆,並將材料用量降低8-10%。品牌商透過延長合約來鼓勵這些技術進步,從而確保對高利潤特種化學品的穩定需求。

技術紡織品(個人防護裝備、電子紡織品)用黏合劑需求激增

醫療、消防和危險物品處理防護衣現在需要使用多層複合材料來取代以往的弱點——接縫。黏合劑中階提供透氣屏障,有效阻隔液體,而導電層確保穿戴式感測器電路的完整性。漢高公司(Henkel AG & Co. KGaA)於2025年推出的銀箔填充聚氨酯,即使經過50次洗滌循環,其電阻率仍低於10 Ω/sq。日本軍方競標要求使用耐洗滌的黏合劑,能夠承受25萬次彎曲測試,這推動了混合聚合物網路的研究與開發。供應商也將目光投向醫療診斷領域,該領域所需的軟性電極必須能夠承受134 度C的高壓釜滅菌,而標準的乙烯-醋酸乙烯酯共聚物(EVA)無法滿足此要求。

醋酸乙烯酯和異丙醇的原料價格波動很大。

2024年至2025年間,醋酸乙烯單體價格在每噸950美元至1,150美元之間波動。這主要是由於中東供應中斷以及亞洲買家面臨的運輸挑戰所致。異丙醇價格與原油價格波動同步,並受到中國出口限制的影響,導致合約價格較2023年水準上漲12%至18%。由於買家在合約期間拒絕價格調整,南亞小規模混合商的毛利率下降了200至300個基點。兩家沒有避險工具的孟加拉生產商在2024年第四季出現虧損,並被擁有長期供應合約的大型競爭對手搶佔了市場佔有率。

細分市場分析

在設計工作室中,可重新定位性比耐久性更為重要,臨時性黏合劑的應用日益廣泛,預計其年複合成長率將達到 6.10%。永久性黏合劑的需求主要來自鞋類、室內裝潢和家用紡織品行業,這些行業的黏合劑必須能夠經受多年的磨損和洗滌,預計到 2025 年,永久性黏合劑的銷售額將佔總銷售額的 59.11%。半永久性化學配方可在 15 分鐘內快速釋放,從而允許在熱交聯之前進行調整。例如,樂泰 MS 9650 是一種濕固化矽烷聚合物,在 24 小時後可達到 18 N/25 mm 的剝離強度,同時在組裝中仍可進行返工。

設計工作室傾向於使用無針原型製作,以避免在行銷攝影中損壞織物表面。線上教學展示了臨時噴劑如何輕鬆調整圖案,從而帶動了業餘愛好者和小規模品牌的需求。由於臨時和永久性黏合劑都必須遵守類似的揮發性有機化合物 (VOC) 和微塑膠法規,因此產品差異化主要體現在包裝和黏度控制上。用於工藝品的噴霧劑黏合劑價格高出 30-40%,反映出消費者更重視便利性而非樹脂成本。另一方面,工業買家仍然偏好大桶裝產品,以最佳化單位成本效益,從而維持了織物黏合劑市場的階梯式定價結構。

水性乳液揮發性有機化合物 (VOC) 含量接近零,符合美國環保署 (EPA) 1168 號法規,預計 2025 年的銷售額將佔總銷售額的 48.22%。然而,生物基分散體預計到 2031 年將以 6.51% 的複合年成長率成長。製造商正透過使用植物油衍生的多元醇來拓展織物黏合劑市場,這些多元醇的熔體黏度和固化速度可與乙烯-醋酸乙烯酯共聚物 (EVA) 相媲美,同時還能減少高達 40% 的碳足跡。黏合劑在高速生產線中仍然至關重要。例如,漢高股份公司 (Henkel AG & Co. KGaA) 的「Technomelt PUR 6260 ECO」含有 60% 的可再生材料,可在 180 度C下黏合彈性纖維而不會發生熱泛黃。

由於美國職業安全與健康管理局 (OSHA) 和歐盟 (EU) 的法規不斷增加合規成本,溶劑型氯丁橡膠的應用範圍正日益局限於皮革等小眾領域。然而,其快速粘合性能使其在運動鞋粘合應用中仍然發揮著重要作用。濕氣活化反應型聚氨酯 (PUR)黏合劑正逐漸成為需要經歷 50 次或以上洗滌考驗的技術紡織品應用的主流選擇。生物基黏合劑的發展面臨原料價格波動的挑戰。蓖麻油產量受季風模式的影響而波動,導致價格波動幅度高達 20%。混合生物基和石油化學成分的混合體係可以緩解這些價格波動,同時滿足生態標籤要求,並為擁有整合供應鏈的大型跨國公司提供競爭優勢。

區域分析

預計到2025年,亞太地區將佔總銷售額的43.45%,並預計在2031年之前實現6.81%的複合年成長率。這表明該地區正作為成品生產基地和成長市場發揮關鍵作用。在中國,華豐化學投資36億元人民幣(約5億美元)建造了一條年產20萬噸的氨綸生產線,該生產線將採用反應型聚氨酯(PUR)黏合劑進行彈性纖維層壓。此外,RAMPF集團於2026年7月在天津開設了一家聚氨酯系統工廠,投資800萬歐元(約850萬美元),旨在實現對汽車和運動服裝加工商的在地化供應。在印度,佔國內70%以上市場佔有率的Pidilite公司報告稱,在技術紡織品分散劑的推動下,其2026年第三季的銷售額成長了11%。同時,越南預計到 2024 年出口額將達到 440 億美元,目前是世界第二大紡織品出口國,它正在吸收從孟加拉轉移過來的訂單,並提振小批量生產用黏合劑的需求。

北美和歐洲市場正穩步成長,儘管成長放緩,這主要是由於市場日趨成熟以及監管日益嚴格。在歐盟,微塑膠法規要求對配方進行調整,採用生物基或不脫落的化學成分,這使得研發週期延長了一年。在美國,馬裡蘭州、維吉尼亞和賓州等州級揮發性有機化合物 (VOC) 法規將黏合劑的排放限制在每公升 50-150 克 (g/L),加速了向水性或熱熔體系的轉變。墨西哥的近岸外包趨勢正在推動黏合劑消費,因為美國品牌需要更可靠的供應鏈。此外,技術紡織品和汽車生產線從亞洲的轉移也推動了對前置作業時間更短的高性能聚氨酯 (PUR) 和紫外光固化黏合劑的需求。

儘管南美洲和中東/非洲地區的市場佔有率較小,但這些產業卻擁有巨大的成長潛力。 Pidilite 透過與經銷商建立合作關係,成功打入非洲市場,並觸達手工藝品和家具製造商,實現了 40% 的年成長率。在巴西,紡織業正向出口導向技術布料轉型,而歐洲買家也正在進行嚴格的永續性審核,因此對 Bluesign 認證的黏合劑的需求日益成長。土耳其加入歐盟後,對低 VOC 和符合微塑膠標準的黏合劑的需求也隨之增加。在南非,汽車座椅供應商正轉向使用低排放量黏合劑,以滿足歐洲目的地設備製造商 (OEM) 制定的車內空氣品質標準,預計這一趨勢也將蔓延至當地的家具和服裝產業。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 按需時尚的快速週期

- 技術紡織品(個人防護裝備、電子紡織品)黏合技術的蓬勃發展

- 生物基聚合物的技術進步為縫紉材料的替代品提供了可能。

- 在服裝廠引入低能耗冷黏合工藝

- 尋求軟性生產黏合劑的電商微型品牌

- 市場限制因素

- 醋酸乙烯酯和異丙醇的原料價格波動很大。

- 與合成黏合劑相關的微塑膠排放法規

- 收緊溶劑黏合劑的工人暴露限值

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 臨時織物黏合劑

- 永久性織物黏合劑

- 透過基礎化學

- 水性(PVA、EVA)

- 溶劑型(氯丁橡膠、聚氨酯)

- 熱熔膠(EVA、TPU)

- 反應性聚氨酯

- 生物基分散體

- 透過分銷管道

- 網路市集

- 手工藝品專賣店

- 超級市場和大賣場

- 紡織原料批發商

- 廠商直銷

- 按最終用戶行業分類

- 服飾和服飾

- 家用紡織品

- 鞋類和皮革製品

- 汽車內部裝潢建材和內裝裝飾

- 家具和床墊

- 手工藝、DIY和嗜好

- 工業防護纖維

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)和排名分析

- 公司簡介

- 3M

- Arkema

- Beacon Adhesives Inc.

- Buhnen GmbH & Co. KG

- CHEMENCE

- Eclectic Products, LLC

- Gorilla Glue, Inc

- HB Fuller Company

- Henkel AG & Co. KGaA

- iLoveToCreate

- Mitreapel

- Permabond

- Permatex Inc.

- Pidilite Industries Ltd.

- Sika AG

- Therm O Web

- Weldbond Adhesives

第7章 市場機會與未來展望

According to Mordor Intelligence, the fabric glue market size is expected to grow from USD 7.87 billion in 2025 to USD 8.32 billion in 2026 and is forecast to reach USD 10.98 billion by 2031 at 5.71% CAGR over 2026-2031.

This report is Segmented by Product Type (Temporary Fabric Glue and Permanent Fabric Glue), Base Chemistry (Water-Based (PVA, EVA) and More), Distribution Channel (Online Marketplaces, and More), End-User Industry (Clothing and Apparel and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Fabric Glue Market Trends and Insights

Rapid On-Demand Fashion Cycles

Fast-fashion platforms introduce thousands of new stock-keeping units (SKUs) daily, prompting factories to replace traditional sequential sewing with automated spray or roller adhesive lines, reducing labor requirements by 30-40%. Polyester and nylon blends bonded with thermoplastic hot-melts achieve peel strengths exceeding 15 N/25 mm, sufficient for garments designed to endure 10-20 wash cycles. Instant tack and minimal cure times make reactive polyurethane and ethylene-vinyl-acetate copolymers favorable choices. Suppliers are optimizing rheology to ensure formulations operate efficiently on high-speed conveyor systems without stringing. Chinese converters have adopted dual-head robots capable of dispensing adhesives in variable patterns, reducing overspray and cutting material usage by 8-10%. Brands incentivize such technological advancements with extended contracts, ensuring consistent demand for higher-margin specialty chemistries.

Surge in Technical-Textile Bonding (PPE, E-Textiles)

Protective garments for healthcare, firefighting, and hazardous-material handling now require multi-layer laminates, replacing stitched seams that previously served as weak points. Adhesive interlayers provide liquid-tight yet breathable barriers, while conductive grades ensure circuit integrity for wearable sensors. Henkel AG & Co. KGaA's silver-flake-filled polyurethane, introduced in 2025, maintains resistivity below 10 Ω/sq even after 50 wash cycles. Military tenders in Japan demand wash-durable bonds capable of withstanding 250,000-cycle flex testing, driving research and development (R&D) into hybrid polymer networks. Suppliers are also targeting medical diagnostics, where flexible electrodes must endure autoclave sterilization at 134°C, a challenge that standard ethylene-vinyl acetate (EVA) cannot meet.

Volatile Vinyl-Acetate and Isopropanol Feedstock Prices

Vinyl-acetate monomer prices ranged between USD 950 and USD 1,150 per ton during 2024-2025, influenced by Middle-East supply disruptions and freight challenges affecting Asian buyers. Isopropanol prices followed crude oil volatility and were impacted by Chinese export restrictions, leading to contract values increasing by 12-18% compared to 2023 levels. Small South-Asian formulators experienced gross margin reductions of 200-300 basis points as buyers resisted mid-contract price adjustments. Without hedging mechanisms, two Bangladeshi producers reported negative margins in Q4 2024, losing market share to larger competitors with long-term supply agreements.

Other drivers and restraints analyzed in the detailed report include:

- Bio-Based Polymer Breakthroughs Enabling Sewing Replacement

- Adoption of Low-Energy Cold-Bonding Processes

- Microplastic-Shedding Regulations on Synthetic Glues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Temporary formulations are expected to grow at a compound annual growth rate (CAGR) of 6.10%, gaining adoption in design studios where repositionability is prioritized over durability. Permanent grades accounted for 59.11% of 2025 revenue, driven by demand in footwear, upholstery, and home textiles, where adhesives must withstand years of wear and laundering. Semi-permanent chemistries, offering 15-minute open times, enable adjustments before thermal crosslinking. For example, Loctite MS 9650, a moisture-curing silane polymer, achieves a peel strength of 18 N/25 mm after 24 hours while allowing rework during assembly.

Design studios prefer pin-free prototyping as it preserves fabric surfaces for marketing photography. Online tutorials highlight how temporary sprays facilitate pattern adjustments, boosting demand among hobbyists and small brands. Since both temporary and permanent adhesives must comply with identical volatile organic compound (VOC) and microplastic regulations, differentiation focuses on packaging and viscosity control. Craft-oriented aerosols command a 30-40% price premium, reflecting consumer preference for convenience over resin cost. Industrial buyers, however, continue to favor bulk drums to optimize unit economics, maintaining a tiered pricing structure within the fabric glue market.

Water-based emulsions contributed 48.22% of 2025 revenue due to their near-zero volatile organic compound (VOC) profiles, aligning with Environmental Protection Agency (EPA) Rule 1168. However, bio-based dispersions are projected to grow at a CAGR of 6.51% through 2031. Manufacturers are expanding the fabric glue market by utilizing vegetable-oil polyols, which match the melt viscosity and set speed of ethylene-vinyl acetate (EVA) while reducing carbon footprints by up to 40%. Hot-melt adhesives remain critical for high-speed production lines; for instance, Henkel AG & Co. KGaA's Technomelt PUR 6260 ECO, with 60% renewable content, bonds elastane without thermal yellowing at 180°C.

Solvent-based neoprenes are increasingly confined to niche applications like leather due to rising compliance costs under Occupational Safety and Health Administration (OSHA) and European Union (EU) regulations. However, their instant tack keeps them relevant for athletic footwear bonding. Reactive polyurethane (PUR) adhesives, which crosslink under moisture, dominate technical textile applications requiring wash durability beyond 50 cycles. The growth of bio-based adhesives faces challenges from feedstock volatility, as castor-oil harvests fluctuate with monsoon patterns, causing 20% price swings. Hybrid systems blending bio-based and petrochemical components mitigate this volatility while qualifying for eco-labels, providing large multinationals with integrated supply chains a competitive advantage.

Geography Analysis

Asia-Pacific accounted for 43.45% of the projected 2025 revenue and is expected to achieve a 6.81% compound annual growth rate (CAGR) through 2031, highlighting its role as a production hub and a growth market for finished goods. In China, Huafon Chemical is investing RMB 3.6 billion (USD 500 million) in a 200,000 tons per year spandex production line, which will utilize reactive polyurethane (PUR) adhesives for elastane lamination. Additionally, RAMPF Group inaugurated a EUR 8 million (USD 8.5 million) polyurethane systems plant in Tianjin in July 2026 to localize supply for automotive and sportswear converters. In India, Pidilite, which holds over 70% of the domestic market share, reported an 11% Q3 FY26 revenue growth driven by technical-textile dispersions. Meanwhile, Vietnam, now the second-largest textile exporter with USD 44 billion in shipments in 2024, is absorbing orders rerouted from Bangladesh, boosting adhesive demand for short-run production.

North America and Europe collectively contribute stable but slower growth due to market maturity and stringent regulations. In the European Union, microplastic regulations are prompting reformulations toward bio-based or non-shedding chemistries, extending development cycles by up to a year. In the United States, state-level volatile organic compound (VOC) regulations in Maryland, Virginia, and Pennsylvania limit adhesive emissions to 50-150 grams per liter (g/L), encouraging a shift toward water-based or hot-melt systems. Mexico's nearshoring trend is driving adhesive consumption closer to U.S. brands seeking resilient supply chains. Technical-textile and automotive production lines migrating from Asia are increasing demand for high-performance polyurethane (PUR) and ultraviolet (UV)-curable adhesives with short lead times.

South America and the Middle East-Africa regions represent smaller market shares but offer areas of significant growth. Pidilite's expansion into African markets is achieving 40% annual growth, leveraging distributor partnerships to reach craft and furniture manufacturers. In Brazil, the textile sector is shifting toward export-oriented technical fabrics, necessitating Bluesign-approved adhesives as European buyers enforce sustainability audits. Turkey's customs-union access to the European Union is driving demand for low-VOC, microplastic-compliant adhesives. In South Africa, automotive seat suppliers are transitioning to low-emission hot-melts to comply with European original equipment manufacturer (OEM) cabin air quality standards, a trend expected to extend into local furniture and apparel subsectors.

- 3M

- Arkema

- Beacon Adhesives Inc.

- Buhnen GmbH & Co. KG

- CHEMENCE

- Eclectic Products, LLC

- Gorilla Glue, Inc

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- iLoveToCreate

- Mitreapel

- Permabond

- Permatex Inc.

- Pidilite Industries Ltd.

- Sika AG

- Therm O Web

- Weldbond Adhesives

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid On-Demand Fashion Cycles

- 4.2.2 Surge in Technical-Textile Bonding (PPE, E-Textiles)

- 4.2.3 Bio-Based Polymer Breakthroughs Enabling Sewing Replacement

- 4.2.4 Adoption of Low-Energy Cold-Bonding Processes in Apparel Factories

- 4.2.5 E-commerce Micro-Brands Demanding Flexible Production Adhesives

- 4.3 Market Restraints

- 4.3.1 Volatile Vinyl-Acetate and Isopropanol Feedstock Prices

- 4.3.2 Micro-Plastic-Shedding Regulations on Synthetic Glues

- 4.3.3 Worker-Exposure Limits Tightening on Solvent-Based Adhesives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Temporary Fabric Glue

- 5.1.2 Permanent Fabric Glue

- 5.2 By Base Chemistry

- 5.2.1 Water-Based (PVA, EVA)

- 5.2.2 Solvent-Based (Neoprene, PU)

- 5.2.3 Hot-Melt (EVA, TPU)

- 5.2.4 Reactive PUR

- 5.2.5 Bio-Based Dispersions

- 5.3 By Distribution Channel

- 5.3.1 Online Marketplaces

- 5.3.2 Specialty Craft Stores

- 5.3.3 Supermarkets and Hypermarkets

- 5.3.4 Textile Raw-Material Distributors

- 5.3.5 Direct-to-Factory

- 5.4 By End-User Industry

- 5.4.1 Clothing and Apparel

- 5.4.2 Home Textiles

- 5.4.3 Footwear and Leather Goods

- 5.4.4 Automotive Upholstery and Interiors

- 5.4.5 Furniture and Mattress

- 5.4.6 Crafts, DIY and Hobby

- 5.4.7 Industrial Protective Textiles

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Beacon Adhesives Inc.

- 6.4.4 Buhnen GmbH & Co. KG

- 6.4.5 CHEMENCE

- 6.4.6 Eclectic Products, LLC

- 6.4.7 Gorilla Glue, Inc

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 iLoveToCreate

- 6.4.11 Mitreapel

- 6.4.12 Permabond

- 6.4.13 Permatex Inc.

- 6.4.14 Pidilite Industries Ltd.

- 6.4.15 Sika AG

- 6.4.16 Therm O Web

- 6.4.17 Weldbond Adhesives

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

眼科黏合劑市場規模、佔有率和成長分析:按產品類型、應用、適應症、最終用戶和地區分類-2026-2033年產業預測

眼科黏合劑市場規模、佔有率和成長分析:按產品類型、應用、適應症、最終用戶和地區分類-2026-2033年產業預測 2026-2030年全球黏合劑市場

2026-2030年全球黏合劑市場 丙烯酸樹脂黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、分銷方式、地區和競爭格局分類,2021-2031年智慧黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年

丙烯酸樹脂黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、分銷方式、地區和競爭格局分類,2021-2031年智慧黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年 電子產業PUR黏合劑市場規模、佔有率和成長分析:按功能/類型、應用、終端用戶產業、包裝、分銷管道和地區分類-2026-2033年產業預測

電子產業PUR黏合劑市場規模、佔有率和成長分析:按功能/類型、應用、終端用戶產業、包裝、分銷管道和地區分類-2026-2033年產業預測 亞太地區EVA黏合劑:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

亞太地區EVA黏合劑:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 北美基材黏合劑市場規模、佔有率和趨勢分析報告:按樹脂類型、技術、應用、國家和細分市場預測(2026-2033 年)

北美基材黏合劑市場規模、佔有率和趨勢分析報告:按樹脂類型、技術、應用、國家和細分市場預測(2026-2033 年) 全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測

全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測 電子黏合劑市場:按材料、產品類型、應用和地區分類

電子黏合劑市場:按材料、產品類型、應用和地區分類 2026年全球磁磚黏合劑市場報告

2026年全球磁磚黏合劑市場報告