|

市場調查報告書

商品編碼

2066660

美國黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)United States Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

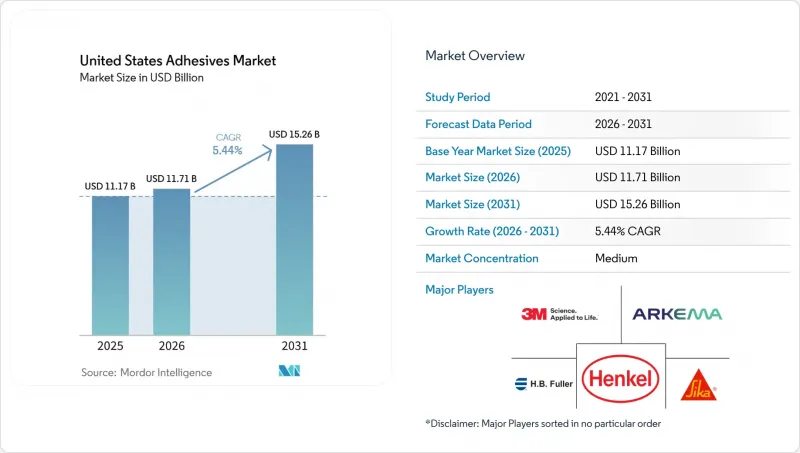

根據 Mordor Intelligence 預測,美國黏合劑市場預計將從 2025 年的 111.7 億美元成長到 2026 年的 117.1 億美元,到 2031 年達到 152.6 億美元,2026 年至 2031 年的複合年成長率為 5.44%。

本報告按樹脂(丙烯酸樹脂、氰基丙烯酸酯樹脂、環氧樹脂、聚氨酯樹脂、矽樹脂、VAE/EVA等)、工藝(熱熔型、反應型、溶劑型、UV固化型、水性)和終端用戶行業(航太、汽車、建築施工、鞋類和皮革製品、醫療、包裝、木工和細木工等)進行細分。市場預測以美元計價。

美國黏合劑市場趨勢與洞察

汽車製造業對輕量化的需求激增

汽車原始設備製造商 (OEM) 目前指定使用環氧樹脂和聚氨酯結構性黏著劑,以減少車身本體質量 10-15%,從而直接提升電動車的續航里程,並滿足最新的企業平均燃油經濟性 (CAFE) 目標。通用汽車 ( 目的地 ) 的 Ultium 平台採用導熱係數低於 0.3 瓦/米·開爾文 (W/(m*K)) 的環氧樹脂黏合劑,以抑制電池間的熱傳遞,同時保持超過 3 千伏的電絕緣性。新化學成分的認證需要 18-24 個月的時間,這不僅保護了現有製造商,也為能夠將介電強度和電磁耗散添加劑相結合以保護 800 伏特架構的矽膠專家開闢了利基市場。密西根州和俄亥俄州的區域一級供應商已經獲得了多年期 200 度C耐溫間隙填充矽膠的契約,這表明市場需求將持續到 2029 年。

電子商務的持續成長正在推動包裝黏合劑的需求。

隨著電子商務的興起(其在美國零售額中佔據了相當大的佔有率),瓦楞紙板製造商對熱熔膠和水性黏合劑的需求日益成長,這些膠粘劑即使在超過每分鐘300米的速度下也能快速固化,且不會影響初始強度。亞馬遜致力於用紙基填充材取代塑膠空氣枕,這推動了澱粉黏合劑和醋酸乙烯酯-乙烯(VAE)乳化的應用,這些乳液支持單一材料的回收流程。 VAE產品的價格溢價為20-25%,但能確保再生聚乙烯的純度。同時,瓦楞紙板製造商正在將運作厚度減薄至180克/平方米,這迫使他們改進流變性能,以確保即使在基材孔隙率降低的情況下也能均勻塗覆黏合劑。據報道,德克薩斯州和賓夕法尼亞州物流中心的工廠實行兩班倒以應對訂單高峰,這證實了包裝級瓦楞紙板的需求正保持著長期成長勢頭。

石油基原物料價格波動

儘管2026年初丙烯價格已從2024年中期的高峰迴落,但仍高度依賴墨西哥灣沿岸地區裂解裝置的停產以及地緣政治事件。現有合約結構對季度價格波動幾乎沒有對沖作用,導致加工商在下游價格調整生效前利潤率面臨壓力。生物基樹脂雖然能夠分散風險並對沖風險,但農作物價格的周期性波動以及對可再生信貸市場的風險敞口抵消了部分穩定性優勢。因此,黏合劑買家要求靈活的配方條款,允許填料替換,這使得庫存計劃和配方一致性變得更加複雜。

細分市場分析

2025年,丙烯酸樹脂的銷售額佔比達到28.85%,但受商品化壓力擠壓,利潤率受到擠壓,尤其是在感壓膠帶領域。環氧樹脂是航太領域關鍵結構材料的重要組成部分,玻璃化轉變溫度(Tg)超過180 度C的產品價格居高不下。聚氨酯因其優異的抗衝擊性,在軟包裝和板材層壓領域佔據主導地位。氰基丙烯酸酯則用於電子產品和外科縫線等小眾快速黏合應用。 VAE/EVA共聚物為包裝產業提供經濟高效的熱熔樹脂,但其耐熱性較低,限制了其在汽車產業的應用。特種酚醛樹脂、聚醯亞胺樹脂和厭氧樹脂雖然市佔率較小,但盈利豐厚,對化學穩定性和熱穩定性要求極高。預計2026年至2031年間,矽酮產品將以6.45%的複合年成長率成長,主要成長動力來自高溫電動車(EV)動力系統和穿戴式醫療設備的應用。電池組設計人員需要選用能夠承受150–200 度C高溫、不易碎裂、絕緣性能超過3千伏且具有良好散熱性能的間隙填充矽酮材料。醫療設備製造商則優先選擇符合國際標準化組織(ISO)10993生物相容性標準的壓敏黏著劑,用於14天血糖值監測貼片。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 汽車製造業對輕量化的需求激增

- 電子商務的持續成長正在推動包裝黏合劑市場的發展。

- 美國住宅建設和住宅量增加

- 大型木造建築中混合黏結技術的應用

- 聯邦政府針對低揮發性有機化合物(VOC)生物基化學品的「生物清潔」激勵計劃

- 市場限制因素

- 石油基原物料價格波動

- 對溶劑型塗料的VOC排放制定嚴格的法規

- 精密黏合劑應用領域技術純熟勞工短缺

- 價值鏈分析

- 分銷通路分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 氰基丙烯酸酯

- 環氧樹脂

- 聚氨酯

- 矽酮

- VAE/EVA

- 其他樹脂

- 透過技術

- 熱熔膠

- 反應性

- 溶劑型

- 紫外線固化型

- 水溶液

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 鞋類和皮革

- 衛生保健

- 包裝

- 木工和細木工

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Arkema

- Ashland Global Holdings

- Avery Dennison Corporation

- BASF SE

- Dow

- Dymax Corporation

- Franklin International

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- Jowat SE

- MAPEI SpA

- Momentive Performance Materials

- Parker Hannifin(LORD)

- Permabond LLC

- PPG Industries

- Royal Adhesives & Sealants

- RPM International Inc.

- Sika AG

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states adhesives market size is expected to increase from USD 11.17 billion in 2025 to USD 11.71 billion in 2026 and reach USD 15.26 billion by 2031, growing at a CAGR of 5.44% over 2026-2031.

This report is Segmented by Resin (Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA, and More), Technology (Hot-Melt, Reactive, Solvent-Borne, UV Cured, and Water-Borne), and End-User Industry (Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, Woodworking and Joinery, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Adhesives Market Trends and Insights

Surge in Lightweighting Demand in Automotive Manufacturing

Automotive original equipment manufacturers (OEMs) now specify epoxy and polyurethane structural adhesives that can shave 10%-15% from body-in-white mass, translating directly into longer electric vehicle range and compliance with the latest Corporate Average Fuel Economy (CAFE) targets. General Motors' Ultium platform deploys thermally conductive epoxy lines below 0.3 Watts per meter-Kelvin (W/(m*K)) to curb cell-to-cell heat propagation, while maintaining electrical isolation over 3 kilovolts. The lengthy 18-24 month qualification window for new chemistries shields incumbents but opens niches for silicone specialists able to pair dielectric strength with electromagnetically dissipative additives that protect 800-volt architectures. Regional Tier-1 suppliers in Michigan and Ohio have already booked multi-year contracts for gap-filler silicones rated to 200°C, signaling a sustained pull through 2029.

Continued Growth in E-Commerce Boosting Packaging Adhesives

With e-commerce accounting for a significant share of United States retail sales, corrugators demand hot-melt and water-borne adhesives that cure fast without sacrificing green strength at speeds topping 300 meters per minute. Amazon's pledge to replace plastic air pillows with paper filler has driven uptake of starch- and vinyl-acetate-ethylene (VAE) emulsions compatible with mono-material recycling streams. These VAE systems command 20%-25% price premiums but ensure polyethylene reclaim purity. Meanwhile, carton producers are thinning board calipers to 180 g/m2, forcing rheology upgrades so adhesive lay-down remains consistent despite reduced substrate porosity. Logistics hubs in Texas and Pennsylvania report double-shift plant utilization to meet peak fulfillment seasons, underscoring the secular momentum behind packaging grades.

Petro-Feedstock Price Volatility

Early 2026 propylene prices dipped from mid-2024 peaks but remain highly sensitive to Gulf Coast cracker outages and geopolitical events . Contract structures seldom hedge quarterly swings, exposing converters to margin squeezes before downstream price adjustments can take effect. Although bio-attributed resins offer a diversification hedge, they import exposure to crop-price cycles and renewable-credit markets, offsetting some stability gains. Adhesive buyers, therefore, demand flexible-formulation clauses allowing filler substitutions, complicating inventory planning and formulation consistency.

Other drivers and restraints analyzed in the detailed report include:

- Rising U.S. Residential Construction and Housing Starts

- Adoption of Hybrid Bonding for Mass-Timber Construction

- Stringent VOC Emission Limits on Solvent-Borne Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylics retained 28.85% of 2025 revenue, but commoditization pressures margins, especially in pressure-sensitive tapes. Epoxies remain indispensable for aerospace primary structures, commanding premium prices for Tg values exceeding 180°C. Polyurethanes dominate flexible packaging and panel lamination, prized for impact resilience, whereas cyanoacrylates serve niche rapid-bonding roles in electronics and surgical closures. VAE/EVA copolymers supply cost-effective hot-melts in packaging, though limited heat resistance curtails automotive uptake. Specialty phenolic, polyimide, and anaerobic resins occupy small but lucrative segments demanding extreme chemical or thermal stability. Silicone grades are forecast to grow at a 6.45% CAGR from 2026 to 2031, on the back of high-temperature electric vehicle (EV) drivetrains and wearable-healthcare use cases. Battery-pack designers specify gap-filler silicones that withstand 150-200°C without embrittlement, delivering dielectric insulation above 3 kilovolts while dissipating heat. Medical device firms value silicone pressure-sensitives for 14-day glucose-monitor adhesion, ensuring International Organization for Standardization (ISO) 10993 biocompatibility.

List of Companies Covered in this Report:

- 3M

- Arkema

- Ashland Global Holdings

- Avery Dennison Corporation

- BASF SE

- Dow

- Dymax Corporation

- Franklin International

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- Jowat SE

- MAPEI S.p.A.

- Momentive Performance Materials

- Parker Hannifin (LORD)

- Permabond LLC

- PPG Industries

- Royal Adhesives & Sealants

- RPM International Inc.

- Sika AG

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in lightweighting demand in automotive manufacturing

- 4.2.2 Continued growth in e-commerce boosting packaging adhesives

- 4.2.3 Rising U.S. residential construction and housing starts

- 4.2.4 Adoption of hybrid bonding for mass-timber construction

- 4.2.5 Federal "Buy Clean" incentives for low-VOC bio-based chemistries

- 4.3 Market Restraints

- 4.3.1 Petro-feedstock price volatility

- 4.3.2 Stringent VOC emission limits on solvent-borne systems

- 4.3.3 Skilled-labor shortage for precision adhesive application

- 4.4 Value Chain Analysis

- 4.5 Distribution Channel Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Hot-Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV-Cured

- 5.2.5 Water-borne

- 5.3 By End-User Industry

- 5.3.1 Aerospace

- 5.3.2 Automotive

- 5.3.3 Building and Construction

- 5.3.4 Footwear and Leather

- 5.3.5 Healthcare

- 5.3.6 Packaging

- 5.3.7 Woodworking and Joinery

- 5.3.8 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland Global Holdings

- 6.4.4 Avery Dennison Corporation

- 6.4.5 BASF SE

- 6.4.6 Dow

- 6.4.7 Dymax Corporation

- 6.4.8 Franklin International

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Huntsman International LLC

- 6.4.12 Illinois Tool Works Inc.

- 6.4.13 Jowat SE

- 6.4.14 MAPEI S.p.A.

- 6.4.15 Momentive Performance Materials

- 6.4.16 Parker Hannifin (LORD)

- 6.4.17 Permabond LLC

- 6.4.18 PPG Industries

- 6.4.19 Royal Adhesives & Sealants

- 6.4.20 RPM International Inc.

- 6.4.21 Sika AG

- 6.4.22 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

眼科黏合劑市場規模、佔有率和成長分析:按產品類型、應用、適應症、最終用戶和地區分類-2026-2033年產業預測

眼科黏合劑市場規模、佔有率和成長分析:按產品類型、應用、適應症、最終用戶和地區分類-2026-2033年產業預測 2026-2030年全球黏合劑市場

2026-2030年全球黏合劑市場 丙烯酸樹脂黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、分銷方式、地區和競爭格局分類,2021-2031年智慧黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年

丙烯酸樹脂黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、分銷方式、地區和競爭格局分類,2021-2031年智慧黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年 織物黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

織物黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 電子產業PUR黏合劑市場規模、佔有率和成長分析:按功能/類型、應用、終端用戶產業、包裝、分銷管道和地區分類-2026-2033年產業預測亞太地區EVA黏合劑:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲EVA黏合劑:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031年)

電子產業PUR黏合劑市場規模、佔有率和成長分析:按功能/類型、應用、終端用戶產業、包裝、分銷管道和地區分類-2026-2033年產業預測亞太地區EVA黏合劑:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲EVA黏合劑:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031年) 北美基材黏合劑市場規模、佔有率和趨勢分析報告:按樹脂類型、技術、應用、國家和細分市場預測(2026-2033 年)

北美基材黏合劑市場規模、佔有率和趨勢分析報告:按樹脂類型、技術、應用、國家和細分市場預測(2026-2033 年) 全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測

全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測