|

市場調查報告書

商品編碼

2065621

中東和非洲室內農業:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle East And Africa Indoor Farming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

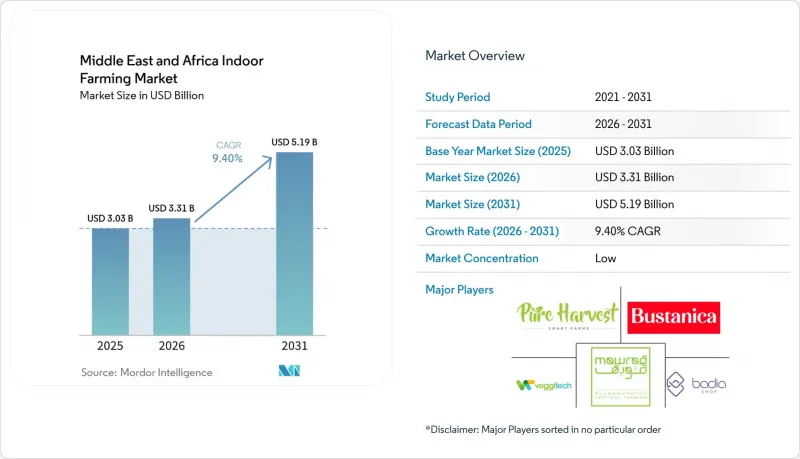

根據 Mordor Intelligence 預測,中東和非洲的室內農業市場規模將從 2025 年的 30.3 億美元和 2026 年的 33.1 億美元成長到 2031 年的 51.9 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 9.40%。

本報告按設施類型(溫室、室內垂直農場、貨櫃農場等)、栽培系統(水耕、氣耕等)、組件(硬體、軟體、服務)、作物類型(水果、蔬菜、香草、花卉和觀賞植物等)以及地區(中東和非洲)進行細分。市場預測以美元計價。

中東和非洲室內農業市場的趨勢和洞察

水資源短缺和耕地面積有限

水資源短缺是推動中東和非洲室內農業市場發展的主要動力。由於耕地有限且淡水資源匱乏,該地區正加速向資源高效型糧食生產系統轉型。這種轉型推動了對水耕和可控環境農業的投資,尤其是在海灣國家。一項針對「太陽能逆滲透水耕網室」的2025年研究強調了其經濟效益。用於水耕番茄的太陽能逆滲透(RO)系統生產的灌溉用水成本為每立方公尺1.05美元。相較之下,傳統公共水源的水價為每立方公尺2.52美元至3.20美元,這意味著用水成本降低了58%至68%。這種經濟和資源效率的提升正在促進室內農業的普及,增強該地區的糧食安全和農業永續性。

糧食安全和進口替代計劃

在中東和非洲,糧食安全和進口替代計畫正成為室內農業市場成長要素。各國政府日益重視國內農業生產,以減少對糧食進口的依賴。促進環境控制農業、溫室擴張和本地化供應鏈的政策正在刺激全部區域對先進農業技術的投資。這一趨勢在阿拉伯聯合大公國(阿拉伯聯合大公國)尤為顯著,該國的《2051年國家糧食安全戰略》強調,永續的國內糧食生產和現代農業技術是增強長期糧食韌性的關鍵優先事項。這些政策舉措正在改善全部區域室內農業項目的資金籌措、基礎設施建設和商業性信心。

高資本密集度及投資回收風險

高昂的初始投資仍然是中東和非洲室內農業市場面臨的一大挑戰,尤其是在沿岸地區以外的地區,因為在這些地區獲得專案資金更加困難。室內農業需要在溫室結構、封閉式栽培系統、照明、冷凍、灌溉、自動化和收穫後後處理方面進行大量前期投資,才能產生穩定的利潤。在海灣國家,由於許多計畫都能獲得政府支持,這種財務負擔相對可控。但在許多非洲市場,情況則截然不同,這些市場融資管道有限,長期供應合約也不普遍。挑戰不僅限於初始投資規模,還在於由於照明效率和控制軟體的進步,現有設備可能在幾年內過時。開發商如果建造沒有模組化升級選項的固定設施,就有可能落後於擁有更先進系統和更低營運成本的新型農場。因此,許多開發商優先考慮分階段部署、小規模入門模式或混合模式,而不是大規模封閉式農場設計。

細分市場分析

到2025年,溫室種植將在中東和非洲的室內農業市場中佔據最大佔有率,達到70.8%。這反映出該地區對擴充性、受保護的種植系統的偏好,這些系統能夠在生產控制和全封閉式垂直農場的運作複雜性之間取得平衡。溫室種植在海灣國家特別普及,高溫和缺水促使當地加強對氣候控制種植的投資。在阿拉伯聯合大公國和沙烏地阿拉伯,商業水耕溫室營運商正在擴大產能,以支持糧食安全戰略並確保全年蔬菜供應。此外,大規模溫室系統可容納更大的種植面積,單位基礎設施成本更低,因此在主糧作物生產方面更具商業性可行性。

預計2026年至2031年間,中東和非洲的貨櫃式室內農業市場將以12.8%的複合年成長率高速成長,主要驅動力是市場對可在都市區消費中心附近運營的模組化室內農業系統的需求不斷成長。貨櫃式農場的柔軟性使其對土地資源有限、資金預算不足或計劃進行試點規模擴張的市場極具吸引力。與大規模溫室和垂直農場設施相比,這些系統部署速度更快。室內垂直農業在海灣國家日益受到關注,但其擴張主要由資金雄厚、與零售商和機構建立了牢固合作關係的營運商推動。深水栽培(DWC)系統等專業設施形式繼續應用於高階農業市場、科研種植和受控試點項目。

到2025年,水耕法將佔據59.8%的最大佔有率,並繼續保持其在該地區環境控制農業中的主要種植系統地位。由於其營養供應可預測、作物品質穩定且與傳統土壤種植相比用水量較少,該系統持續廣泛應用。水耕系統在海灣國家尤其重要,這些地區水資源匱乏且氣候條件極端,精準灌溉對於商業性糧食生產至關重要。由於該技術在沙漠氣候和商業溫室環境中均已得到驗證,生產者繼續依賴水耕法種植番茄、黃瓜、辣椒、香草和綠葉等作物。

預計從2026年到2031年,氣耕將以15.6%的複合年成長率高速成長,成為成長最快的技術之一。這主要得益於人們對高效高價值作物種植系統以及都市區食品供應應用的日益成長的興趣。氣耕系統採用精細營養液霧化的方式,顯著降低用水量,縮短作物生長週期,並實現高密度生產。這項技術在供應綠葉蔬菜、香草、微型菜苗和特色產品方面正變得越來越重要,尤其是在零售、旅館和餐飲服務業。此外,魚菜共生和混合種植系統在一些專注於永續食品生產的特定項目中也備受關注,儘管在大多數區域市場,它們的商業性化應用率仍然低於水耕系統。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 水資源短缺和耕地面積有限

- 糧食安全和進口替代計劃

- 不含農藥殘留的新鮮本地農產品的需求

- 透過人工智慧、物聯網、LED和自動化來實現成長

- 政府支持資金推動農業技術發展

- 電力價格補貼和乾旱氣候研究本地化

- 市場限制因素

- 高資本密集度及投資回收風險

- 受控環境農業部門人員短缺

- 冷氣能耗強度和電網成本風險

- 進口投入品和不協調的CEA法規

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依設施類型

- 溫室

- 室內垂直農業

- 貨櫃農場

- 室內深水養殖系統

- 其他設施類型

- 培訓系統

- 水耕法

- 氣耕

- 水耕法

- 土壤耕作

- 混合

- 按組件

- 硬體

- 軟體

- 服務

- 按作物類型

- 水果、蔬菜、香草

- 花卉和觀賞植物

- 微型菜苗和特色作物

- 按地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 以色列

- 其他中東國家

- 非洲

- 南非

- 埃及

- 肯亞

- 其他非洲國家

- 中東

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Pure Harvest Smart Farms Ltd.

- Emirates Bustanica LLC(Emirates Flight Catering Co. LLC)

- VeggiTech Hydroponic Technologies Private Limited(SNASCO Holding Company)

- Mowreq Specialized Agriculture Company

- Badia Al Sahra Agricultural LLC

- AeroFarms, LLC

- Crop One Holdings, Inc.

- Netafim Ltd.(Orbia Advance Corporation, SAB de CV)

- Richel Group SAS

- Signify Holding BV(Signify NV)

- Argus Control Systems Limited(Conviron Group)

- Certhon Build BV(DENSO Corporation)

- KUBO Tuinbouwprojecten BV

- Priva Holding BV

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east and Africa Indoor Farming Market size is projected to expand from USD 3.03 billion in 2025 and USD 3.31 billion in 2026 to USD 5.19 billion by 2031, registering a CAGR of 9.40% between 2026 and 2031.

This report is Segmented by Facility Type (Greenhouses, Indoor Vertical Farms, Container Farms, and More), by Growing System (Hydroponics, Aeroponics, and More), by Component (Hardware, Software, and Services), by Crop Type (Fruits, Vegetables, and Herbs, Flowers and Ornamentals, and More), and by Geography (Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Middle East And Africa Indoor Farming Market Trends and Insights

Water Scarcity and Arable-Land Constraints

Water scarcity significantly drives the indoor farming market in the Middle East and Africa. With limited arable land and minimal freshwater resources, the region increasingly turns to resource-efficient food production systems. This shift has spurred investments in hydroponics and controlled-environment agriculture, particularly in Gulf economies. A 2025 study highlighted in "Solar-Powered RO-Hydroponic Net House" showcased the economic benefits: a solar-powered reverse osmosis system for hydroponic tomato farming generated irrigation-grade water at USD 1.05/m3. In contrast, conventional utility supplies ranged from USD 2.52 to 3.20/m3, marking a 58-68% reduction in water costs. Such economic and resource efficiencies are propelling the adoption of indoor farming, bolstering food security and agricultural sustainability in the region.

Food-Security and Import-Substitution Programs

Food security and import substitution programs are emerging as significant growth drivers for the indoor farming market in the Middle East and Africa. Governments are increasingly focusing on domestic agricultural production to reduce dependence on food imports. Policies promoting controlled-environment agriculture, greenhouse expansion, and localized supply chains are fostering investments in advanced farming technologies across the region. This trend is particularly evident in the United Arab Emirates (UAE), where the National Food Security Strategy 2051 emphasizes sustainable domestic food production and modern agricultural technologies as critical priorities for enhancing long-term food resilience. Such policy initiatives are improving access to financing, infrastructure development, and commercial confidence in indoor farming projects throughout the region.

High Capital Intensity and Payback Risk

High initial investment continues to be a significant challenge for the indoor farming market in the Middle East and Africa, particularly outside the Gulf region, where securing project financing is more difficult. Indoor farming requires substantial upfront expenditures for greenhouse structures, enclosed growing systems, lighting, cooling, irrigation, automation, and post-harvest handling before generating consistent revenue. This financial burden is more manageable in Gulf countries with sovereign-backed projects compared to many African markets, where access to credit is limited, and long-term supply contracts are less prevalent. The challenge is not only the scale of the initial investment but also the risk that current equipment may become outdated within a few years due to advancements in lighting efficiency and control software. Operators who construct rigid facilities without modular upgrade options risk falling behind newer farms equipped with more advanced systems and lower operating costs. As a result, many developers prioritize phased rollouts, smaller-scale entry models, or hybrid formats over large-scale enclosed farm designs.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Local Fresh Pesticide-Residue-Free Produce

- AI, IoT, LED, and Automation Gains

- Cooling-Energy Intensity and Grid-Cost Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Middle East and Africa indoor farming market share for the greenhouse segment accounted for the largest 70.8% in 2025, reflecting the region's preference for scalable protected cultivation systems that balance production control with lower operating complexity than fully enclosed vertical farms. Greenhouse adoption is particularly strong in Gulf countries, where high temperatures and water scarcity drive investments in climate-controlled cultivation. In the United Arab Emirates and Saudi Arabia, commercial hydroponic greenhouse operators are expanding production capacity to support food security strategies and ensure a year-round vegetable supply. Additionally, large greenhouse systems are more commercially viable for staple crop production due to their ability to support larger cultivation areas and lower per-unit infrastructure costs.

The Middle East and Africa indoor farming market size for container farms is projected to grow at the fastest CAGR of 12.8% from 2026 to 2031, supported by rising demand for modular indoor farming systems that can operate close to urban consumption centers. The flexibility of container farms makes them appealing in markets with limited land availability, smaller capital budgets, or pilot-scale expansion plans. These systems also enable faster deployment compared to large greenhouse or vertical farming facilities. While indoor vertical farms are gaining attention in Gulf countries, their expansion is primarily concentrated among well-funded operators with strong retail or institutional partnerships. Specialty facility formats, such as Deep Water Culture (DWC) systems, continue to serve premium produce markets, research cultivation, and controlled pilot applications.

Hydroponics accounted for the largest share of 59.8% in 2025, maintaining its position as the leading growing system in controlled-environment agriculture operations within the region. This system remains widely adopted due to its ability to ensure predictable nutrient delivery, consistent crop quality, and reduced water consumption compared to traditional soil-based cultivation. Hydroponic systems are particularly significant in Gulf countries, where water scarcity and extreme climate conditions necessitate precision irrigation for commercial food production. Growers continue to rely on hydroponics for crops such as tomatoes, cucumbers, peppers, herbs, and leafy greens, as the technology has demonstrated a strong operational track record in desert climates and commercial greenhouse environments.

Aeroponics is projected to grow at the highest CAGR of 15.6% from 2026 to 2031, driven by increasing interest in high-efficiency cultivation systems for premium crops and urban food supply applications. Aeroponic systems utilize fine nutrient mist delivery methods, which significantly reduce water usage while enabling rapid crop cycles and high-density production. This technology is gaining relevance for leafy greens, herbs, microgreens, and specialty produce, particularly for supply to retail, hospitality, and foodservice sectors. Additionally, aquaponics and hybrid growing systems are attracting attention in specific projects focused on sustainable food production, although their commercial adoption remains lower than hydroponic systems across most regional markets.

List of Companies Covered in this Report:

- Pure Harvest Smart Farms Ltd.

- Emirates Bustanica LLC (Emirates Flight Catering Co. LLC)

- VeggiTech Hydroponic Technologies Private Limited (SNASCO Holding Company)

- Mowreq Specialized Agriculture Company

- Badia Al Sahra Agricultural L.L.C.

- AeroFarms, LLC

- Crop One Holdings, Inc.

- Netafim Ltd. (Orbia Advance Corporation, S.A.B. de C.V.)

- Richel Group SAS

- Signify Holding B.V. (Signify N.V.)

- Argus Control Systems Limited (Conviron Group)

- Certhon Build B.V. (DENSO Corporation)

- KUBO Tuinbouwprojecten B.V.

- Priva Holding B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Water scarcity and arable-land constraints

- 4.2.2 Food-security and import-substitution programs

- 4.2.3 Demand for local fresh pesticide-residue-free produce

- 4.2.4 AI, IoT, LED, and automation gains

- 4.2.5 Sovereign-wealth-backed agritech expansion

- 4.2.6 Utility-tariff support and arid-climate research localization

- 4.3 Market Restraints

- 4.3.1 High capital intensity and payback risk

- 4.3.2 Controlled-environment agronomy talent gaps

- 4.3.3 Cooling-energy intensity and grid-cost exposure

- 4.3.4 Imported inputs and non-harmonized CEA regulations

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Facility Type

- 5.1.1 Greenhouses

- 5.1.2 Indoor Vertical Farms

- 5.1.3 Container Farms

- 5.1.4 Indoor Deep Water Culture Systems

- 5.1.5 Other Facility Types

- 5.2 By Growing System

- 5.2.1 Hydroponics

- 5.2.2 Aeroponics

- 5.2.3 Aquaponics

- 5.2.4 Soil-based

- 5.2.5 Hybrid

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By Crop Type

- 5.4.1 Fruits, Vegetables, and Herbs

- 5.4.2 Flowers and Ornamentals

- 5.4.3 Microgreens and Specialty Crops

- 5.5 By Geography

- 5.5.1 Middle East

- 5.5.1.1 Saudi Arabia

- 5.5.1.2 United Arab Emirates

- 5.5.1.3 Israel

- 5.5.1.4 Rest of Middle East

- 5.5.2 Africa

- 5.5.2.1 South Africa

- 5.5.2.2 Egypt

- 5.5.2.3 Kenya

- 5.5.2.4 Rest of Africa

- 5.5.1 Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials as Available, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 Pure Harvest Smart Farms Ltd.

- 6.4.2 Emirates Bustanica LLC (Emirates Flight Catering Co. LLC)

- 6.4.3 VeggiTech Hydroponic Technologies Private Limited (SNASCO Holding Company)

- 6.4.4 Mowreq Specialized Agriculture Company

- 6.4.5 Badia Al Sahra Agricultural L.L.C.

- 6.4.6 AeroFarms, LLC

- 6.4.7 Crop One Holdings, Inc.

- 6.4.8 Netafim Ltd. (Orbia Advance Corporation, S.A.B. de C.V.)

- 6.4.9 Richel Group SAS

- 6.4.10 Signify Holding B.V. (Signify N.V.)

- 6.4.11 Argus Control Systems Limited (Conviron Group)

- 6.4.12 Certhon Build B.V. (DENSO Corporation)

- 6.4.13 KUBO Tuinbouwprojecten B.V.

- 6.4.14 Priva Holding B.V.

7 Market Opportunities and Future Outlook

室內農業市場規模、佔有率、趨勢和預測:按設施類型、作物類型、組件、種植系統和地區分類,2026-2034 年

室內農業市場規模、佔有率、趨勢和預測:按設施類型、作物類型、組件、種植系統和地區分類,2026-2034 年 室內農業市場-全球產業規模、佔有率、趨勢、機會、預測:種植技術、設施類型、組成部分、作物類型、地區及競爭格局,2021-2031年

室內農業市場-全球產業規模、佔有率、趨勢、機會、預測:種植技術、設施類型、組成部分、作物類型、地區及競爭格局,2021-2031年 室內農業技術市場:全球市場預測(依產品類型、作物類型、耕作方式、自動化程度和最終用戶分類)-2026年至2032年

室內農業技術市場:全球市場預測(依產品類型、作物類型、耕作方式、自動化程度和最終用戶分類)-2026年至2032年 2026年全球室內農業市場報告2026年全球室內農業技術市場報告

2026年全球室內農業市場報告2026年全球室內農業技術市場報告 室內農業市場規模、佔有率和趨勢分析報告:按組件、設施類型、作物類別、種植機制、地區和細分市場分類 - 預測,2026-2033 年日本室內農業市場報告:按設施類型、作物類型、組件、種植系統和地區分類,2026-2034年

室內農業市場規模、佔有率和趨勢分析報告:按組件、設施類型、作物類別、種植機制、地區和細分市場分類 - 預測,2026-2033 年日本室內農業市場報告:按設施類型、作物類型、組件、種植系統和地區分類,2026-2034年 室內農業技術市場規模、佔有率和成長分析(按種植系統、設施類型、作物類型和地區分類)-2026-2033年產業預測

室內農業技術市場規模、佔有率和成長分析(按種植系統、設施類型、作物類型和地區分類)-2026-2033年產業預測 室內農業市場規模、佔有率和成長分析(按設施類型、組件、機制、類別和地區分類)-2026-2033年產業預測

室內農業市場規模、佔有率和成長分析(按設施類型、組件、機制、類別和地區分類)-2026-2033年產業預測 室內農業設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

室內農業設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測