|

市場調查報告書

商品編碼

2072849

美國室內農業:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)United States Indoor Farming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

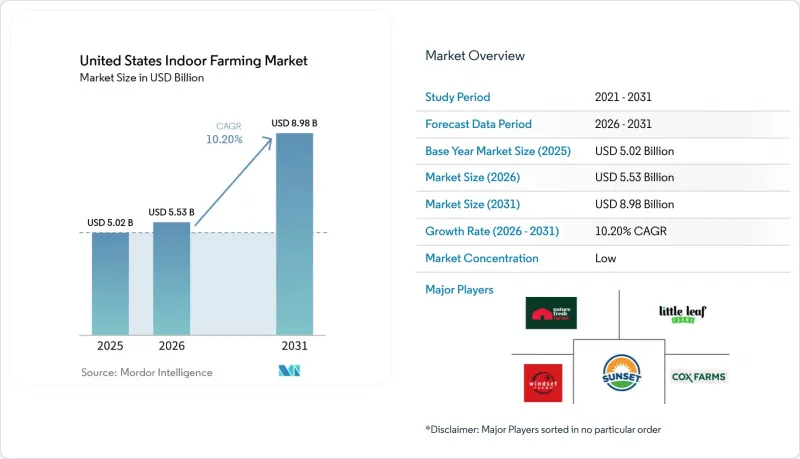

據 Mordor Intelligence 稱,2025 年美國室內農業市場價值 50.2 億美元,預計 2026 年將擴大到 55.3 億美元,到 2031 年將達到 89.8 億美元。

預計 2026 年至 2031 年的預測期內複合年成長率將達到 10.2%。

本報告按設施類型(溫室、室內垂直農場、貨櫃農場)、栽培系統(氣耕、氣耕、魚菜共生、土壤栽培、混合栽培)和作物類型(水果、蔬菜、香草、花卉和觀賞植物、幼苗和繁殖作物)進行分類。市場預測以美元計價。

美國室內農業市場趨勢與洞察

對本地生產的、不含農藥的農產品的需求

消費者對潔淨標示農產品的需求,為室內農業市場提供了穩定且永續的基礎,使其超越了短暫的高階小眾市場。消費者越來越希望產品在進入零售和餐飲通路之前,能夠清楚地了解其產地和處理過程。聯合國糧農組織(FAO)2024年的評估報告顯示,水耕生菜、番茄和草莓中幾乎檢測不到農藥殘留,這進一步凸顯了室內農業作為一種更乾淨的種植方式,對零售商和消費者都具有吸引力。這些優勢在美國西部各州尤其顯著,因為這些地區正在實施更嚴格的水資源政策和食品採購標準。此外,大型零售商正在將本地採購和可追溯性計劃從試驗計畫轉變為對供應商的強制性要求,這進一步推動了對室內種植農產品的需求。參與認證和可追溯的供應計劃通常需要加強監測、環境管理和自動化。因此,對相關系統的投資增加正在推動整個室內農業市場的發展。

全年穩定供應的要求

室內農業市場正獲得越來越多買家的支持,他們希望最大限度地減少新鮮農產品供應中斷的情況。露天農業中頻繁的召回和天氣相關的供應中斷迫使零售商和餐飲服務企業考慮採用能夠降低土壤和地表水污染風險的生產系統。室內設施提供了一個更可控的環境,使買家能夠以露天供應難以企及的方式管理食品安全、配送和品質一致性。這種轉變至關重要,因為如今農業合約的價值不僅取決於價格,還取決於全年供應的可靠性。醫院、大學和懲教機構等機構買家擴大採用本地採購模式,因為穩定的供應與產品品質同等重要。 AmplifiedAg 於 2025 年 9 月在南卡羅來納州美國首個監獄垂直農場進行的一次收割表明,該模式每年可供應約 21.7 公噸綠葉蔬菜,這反映了機構的全年需求。隨著越來越多的買家將穩定的本地採購視為採購要求,市場將受益於更長期、更穩定的採購協議。

高資本投資和能源強度

高昂的初始投資仍是室內農業領域最大的阻礙因素。這是因為專案的獲利能力必須涵蓋複雜的基礎設施和高能耗的營運成本。一項2025年的研究發現,在美國的大規模垂直農場中,照明、溫度控制和通風約佔總營運成本的25%,證實了能源成本是核心而非次要因素。在室內垂直農場中,人工照明消耗了總能源的60%至85%,是最大的能源負擔。這些成本構成了一項重大挑戰,因為它們是在建築結構、控制系統、灌溉系統和其他已安裝設備的折舊免稅額成本之上疊加的。 2025年發表在《能源雜誌》(Energy Journal)上的一項研究發現,將太陽能和電池儲能相結合可以將受控環境農業的額外能源成本降低25%,但系統整合的額外成本仍然導致高昂的初始資本需求。在加州和紐約州等工業電力成本高的市場,這項挑戰更加嚴峻。這是因為就對本地農產品的需求而言,這些州通常被認為是最具商業性吸引力的地區之一。在更廣泛的作物種類和設施模式下,提高效率的好處超過這些負擔之前,高成本仍將是室內農業產業面臨的主要障礙。

細分市場分析

到2025年,溫室將占美國室內農業市場的67%,其成長主要得益於與全封閉式農場相比更低的資本投入和更少的能源依賴。同時,室內垂直農場預計到2031年將以12.5%的複合年成長率成長,成為成長最快的細分市場,這主要得益於高密度佈局、自動化以及對城市空間更有效率的利用。近期的一些項目,例如AmHydro在佛羅裡達州的“Harvest Singularity”設施,反映了2024年至2025年間的行業重組趨勢,即向根據作物生長階段量身定做的自動化模式和更加規範的擴大策略轉變。

貨櫃農場仍然是一個小眾市場,主要用於偏遠地區、機構和研究用途。 AmplifiedAg公司獲得美國農業部資助的貨櫃計畫以及與懲教機構的合作表明,即使它們對整體市場收入成長的貢獻有限,但其仍然具有重要的實際意義。溫室因其擴充性、易於操作和對人工照明的低依賴性,繼續為該行業提供穩定的收入基礎。此外,該領域也越來越關注國內市場。 GrowSpan公司在愛荷華州擴建的25,000平方英尺的Venro溫室,以及Prospiant公司推廣美國製造的溫室解決方案的努力,都表明美國正在向在地採購、減少對進口的依賴以及加強對溫室維修和擴建的支持力度轉變。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對本地生產的、不含農藥的農產品的需求

- 全年供應彈性要求

- 提高用水效率和土地生產力

- LED、自動化和暖通空調技術的進步

- 零售提貨協議提高了專案的資金籌措潛力。

- 美國農業部 (USDA) 為 CEA 的發展提供津貼和技術援助

- 市場限制因素

- 高資本投資和能源強度

- 農業和自動化領域技術工人及人員短缺。

- 垂直農業失敗造成的資金籌措缺口

- 分區、授權和公共產業。

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依設施類型

- 溫室

- 室內垂直農業

- 貨櫃農場

- 培訓系統

- 水耕法

- 氣耕

- 水耕法

- 土壤耕作和雜交系統

- 按作物類型

- 水果、蔬菜、香草

- 綠葉蔬菜

- 草藥

- 番茄

- 黃瓜

- 青椒

- 草莓和漿果

- 微型菜苗

- 花卉和觀賞植物

- 用於培育幼苗和育種的作物

- 水果、蔬菜、香草

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mastronardi Produce Ltd.(Sunset)

- Windset Farms

- Cox Enterprises, LLC

- Nature Fresh Farms

- Little Leaf Farms

- Village Farms International

- Houwelings

- BrightFarms

- Gotham Greens

- Local Bounti

- Revol Greens

- Pure Green Farms

- Superior Fresh

- Edible Garden AG

- Soli Organic

- Great Lakes Growers

- Springworks Farm

- AeroFarms

- 80 Acres Farms

- Oishii

第7章 市場機會與未來趨勢

According to Mordor Intelligence, the united states indoor farming market size was valued at USD 5.02 billion in 2025 and is projected to grow to USD 5.53 billion in 2026 and reach USD 8.98 billion by 2031, at a CAGR of 10.2% during the forecast period of 2026-2031.

This report is Segmented by Facility Type (Greenhouses, Indoor Vertical Farms, and Shipping-Container Farms), by Growing System (Hydroponics, Aeroponics, Aquaponics, Soil-Based, and Hybrid), and by Crop Type (Fruits, Vegetables, and Herbs, Flowers and Ornamentals, Nursery and Propagation Crops). The Market Forecasts are Provided in Terms of Value (USD).

United States Indoor Farming Market Trends and Insights

Demand for Pesticide-Free Local Produce

The demand for clean-label produce is providing the indoor farming market with a stable, sustained base, moving beyond a temporary premium niche. Consumers increasingly seek products with clear information about their origin and handling processes before reaching retail and foodservice channels. A 2024 FAO assessment reported near-zero pesticide detections in hydroponically grown lettuce, tomatoes, and strawberries, reinforcing the appeal of indoor farming as a cleaner growing method for both retailers and consumers. These benefits are particularly significant in Western states, where stricter water policies and grocery procurement standards are being implemented. Furthermore, large retailers are transitioning local sourcing and traceability initiatives from pilot programs to mandatory supplier requirements, driving increased demand for indoor-grown produce. Participation in certified, traceable supply programs often requires enhanced monitoring, environmental controls, and automation, which, in turn, drives higher system investments across the indoor farming market.

Year-Round Supply Resilience Requirements

The indoor farming market is also gaining support from buyers who want fewer disruptions in fresh produce supply. Repeated recall events and weather-related disruptions in field agriculture pushed retailers and foodservice operators to examine production systems that can reduce exposure to soil and surface-water contamination risks. Indoor facilities offer a more controlled setting, which helps buyers manage food safety, timing, and consistency in ways open-field supply cannot always match. This shift matters because produce contracts are now judged not only on price but also on reliability throughout the year. Institutional buyers such as hospitals, universities, and correctional systems are becoming more active in local procurement models because stable supply matters as much as product quality in those settings. AmplifiedAg's September 2025 harvest at the first United States prison vertical farm in South Carolina showed that this model can supply around 21.7 metric tons of leafy greens annually, giving a practical example of year-round institutional demand. As more buyers treat resilient local sourcing as a procurement need, the market stands to benefit from longer and more stable purchase agreements.

High Capex and Energy Intensity

High upfront spending remains the single largest limit on the indoor farming sector because project economics must cover both complex infrastructure and energy-heavy operations. A 2025 study found that lighting, temperature control, and ventilation accounted for around 25% of total operating costs at large United States vertical farms, which confirms that utility spending is central rather than secondary. Artificial lighting accounts for the largest energy burden in enclosed vertical farms, consuming 60-85% of total energy. These cost layers are challenging because they sit on top of depreciation from structures, controls, irrigation systems, and other installed equipment. A 2025 Energy Journal study found that combined photovoltaic and battery storage could reduce excessive energy costs in controlled environment agriculture by 25%, but the added system integration costs still raise the starting capital requirement. High industrial electricity costs in markets such as California and New York deepen this challenge because those states are often among the most commercially attractive for local produce demand. Until efficiency gains outweigh those burdens across more crop types and facility models, cost intensity will remain a major brake on the indoor farming industry.

Other drivers and restraints analyzed in the detailed report include:

- Water-Efficiency and Land-Productivity Gains

- LED, Automation, and Climate-Control Advances

- Skilled Labor and Agronomy-Automation Talent Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Greenhouses accounted for 67% of the United States indoor farming market share in 2025, leading the sector due to lower capital requirements and reduced energy dependence compared to fully enclosed farms. Meanwhile, indoor vertical farms are projected to be the fastest-growing segment, growing at a 12.5% CAGR through 2031, driven by denser layouts, automation, and more efficient use of urban space. Recent projects, such as AmHydro's Harvest Singularity facility in Florida, reflect a shift toward crop-stage-specific automation and more disciplined expansion strategies following the 2024-2025 industry shakeout.

Shipping-container farms remain a niche segment, mainly serving remote, institutional, and research applications. AmplifiedAg's USDA (United States Department of Agriculture)-funded container projects and correctional facility partnerships highlight their continued practical relevance despite limited contribution to overall market revenue growth. Greenhouses continue to provide the industry's stable revenue base due to their scalability, operational familiarity, and lower reliance on artificial lighting. The segment is also becoming more domestically focused. GrowSpan's 25,000-square-foot Venlo greenhouse expansion in Iowa and Prospiant's push toward United States-manufactured greenhouse solutions indicate a broader shift toward local sourcing, reduced import dependence, and stronger support for greenhouse retrofits and expansions across the United States.

Complete Report Scope:

- By Facility Type

- Greenhouses

- Indoor Vertical Farms

- Shipping-container Farms

- By Growing System

- Hydroponics

- Aeroponics

- Aquaponics

- Soil-based and Hybrid Systems

- By Crop Type

- Fruits, Vegetables, and Herbs

- Leafy Greens

- Herbs

- Tomatoes

- Cucumbers

- Peppers

- Strawberries and Berries

- Microgreens

- Flowers and Ornamentals

- Nursery and Propagation Crops

- Fruits, Vegetables, and Herbs

List of Companies Covered in this Report:

- Mastronardi Produce Ltd. (Sunset)

- Windset Farms

- Cox Enterprises, LLC

- Nature Fresh Farms

- Little Leaf Farms

- Village Farms International

- Houwelings

- BrightFarms

- Gotham Greens

- Local Bounti

- Revol Greens

- Pure Green Farms

- Superior Fresh

- Edible Garden AG

- Soli Organic

- Great Lakes Growers

- Springworks Farm

- AeroFarms

- 80 Acres Farms

- Oishii

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for pesticide-free local produce

- 4.2.2 Year-round supply resilience requirements

- 4.2.3 Water-efficiency and land-productivity gains

- 4.2.4 LED, automation, and climate-control advances

- 4.2.5 Retail offtake contracts improving project financeability

- 4.2.6 USDA (United States Department of Agriculture) grants and technical assistance for CEA buildouts

- 4.3 Market Restraints

- 4.3.1 High capex and energy intensity

- 4.3.2 Skilled labor and agronomy-automation talent shortages

- 4.3.3 Financing gap after vertical farming failures

- 4.3.4 Zoning, permitting, and utility-interconnection delays

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Facility Type

- 5.1.1 Greenhouses

- 5.1.2 Indoor Vertical Farms

- 5.1.3 Shipping-container Farms

- 5.2 By Growing System

- 5.2.1 Hydroponics

- 5.2.2 Aeroponics

- 5.2.3 Aquaponics

- 5.2.4 Soil-based and Hybrid Systems

- 5.3 By Crop Type

- 5.3.1 Fruits, Vegetables, and Herbs

- 5.3.1.1 Leafy Greens

- 5.3.1.2 Herbs

- 5.3.1.3 Tomatoes

- 5.3.1.4 Cucumbers

- 5.3.1.5 Peppers

- 5.3.1.6 Strawberries and Berries

- 5.3.1.7 Microgreens

- 5.3.2 Flowers and Ornamentals

- 5.3.3 Nursery and Propagation Crops

- 5.3.1 Fruits, Vegetables, and Herbs

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Mastronardi Produce Ltd. (Sunset)

- 6.4.2 Windset Farms

- 6.4.3 Cox Enterprises, LLC

- 6.4.4 Nature Fresh Farms

- 6.4.5 Little Leaf Farms

- 6.4.6 Village Farms International

- 6.4.7 Houwelings

- 6.4.8 BrightFarms

- 6.4.9 Gotham Greens

- 6.4.10 Local Bounti

- 6.4.11 Revol Greens

- 6.4.12 Pure Green Farms

- 6.4.13 Superior Fresh

- 6.4.14 Edible Garden AG

- 6.4.15 Soli Organic

- 6.4.16 Great Lakes Growers

- 6.4.17 Springworks Farm

- 6.4.18 AeroFarms

- 6.4.19 80 Acres Farms

- 6.4.20 Oishii

7 Market Opportunities and Future Trends

南美洲室內農業:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

南美洲室內農業:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 室內農業市場規模、佔有率、趨勢和預測:按設施類型、作物類型、組件、種植系統和地區分類,2026-2034 年中東和非洲室內農業:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

室內農業市場規模、佔有率、趨勢和預測:按設施類型、作物類型、組件、種植系統和地區分類,2026-2034 年中東和非洲室內農業:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 室內農業市場-全球產業規模、佔有率、趨勢、機會、預測:種植技術、設施類型、組成部分、作物類型、地區及競爭格局,2021-2031年

室內農業市場-全球產業規模、佔有率、趨勢、機會、預測:種植技術、設施類型、組成部分、作物類型、地區及競爭格局,2021-2031年 室內農業技術市場:全球市場預測(依產品類型、作物類型、耕作方式、自動化程度和最終用戶分類)-2026年至2032年

室內農業技術市場:全球市場預測(依產品類型、作物類型、耕作方式、自動化程度和最終用戶分類)-2026年至2032年 2026年全球室內農業市場報告2026年全球室內農業技術市場報告

2026年全球室內農業市場報告2026年全球室內農業技術市場報告 室內農業市場規模、佔有率和趨勢分析報告:按組件、設施類型、作物類別、種植機制、地區和細分市場分類 - 預測,2026-2033 年日本室內農業市場報告:按設施類型、作物類型、組件、種植系統和地區分類,2026-2034年

室內農業市場規模、佔有率和趨勢分析報告:按組件、設施類型、作物類別、種植機制、地區和細分市場分類 - 預測,2026-2033 年日本室內農業市場報告:按設施類型、作物類型、組件、種植系統和地區分類,2026-2034年 室內農業技術市場規模、佔有率和成長分析(按種植系統、設施類型、作物類型和地區分類)-2026-2033年產業預測

室內農業技術市場規模、佔有率和成長分析(按種植系統、設施類型、作物類型和地區分類)-2026-2033年產業預測