|

市場調查報告書

商品編碼

2073227

南美洲室內農業:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)South America Indoor Farming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

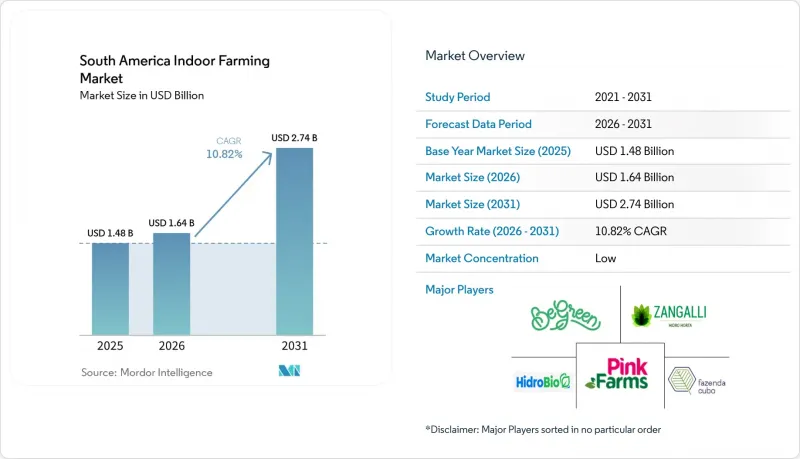

根據 Mordor Intelligence 預測,南美室內農業市場規模將從 2025 年的 14.8 億美元和 2026 年的 16.4 億美元成長到 2031 年的 27.4 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 10.82%。

本報告按栽培系統(氣耕、水耕、魚菜共生等)、設施類型(玻璃或聚碳酸酯溫室、室內垂直農場、貨櫃農場等)、作物類型(水果和蔬菜、香草和微型菜苗等)以及國家(巴西、阿根廷、智利等)進行細分。市場預測以美元計價。

南美洲室內農業市場趨勢與洞察

都市區對生鮮食品的需求不斷成長

都市化正在改變南美洲室內農夫生鮮食品的購買方式。根據巴西2024年的人口普查,都市化達到87.4%,這意味著很大一部分人口居住在大都會圈,食品的品質、保存期限和購買頻率比季節性供應更為重要。拉丁美洲和加勒比地區全部區域呈現類似的趨勢,81%的人口居住在都市區,這縮小了人們對食品安全問題的擔憂與商業性採購決策之間的差距。巴西2026年3月的零售數據顯示,每月銷售額創歷史新高,食品業的銷售額超過了整體零售業。這表明,都市區對透過常規通路銷售的生鮮食品的需求仍然強勁。這對南美的室內農夫市集具有重大意義,因為都市區超級市場和餐飲服務採購商需要全年穩定的供應、一致的品質標準和可追溯性,而這些並非露天農場總能提供的。最強勁的需求不再局限於聖保羅、聖地牙哥和波哥大。在庫里蒂巴、累西腓、麥德林和利馬北等區域性城市,正規零售網路正在擴張。城市地區的擴張為室內農業企業提供了更多空間,使其能夠開發更靠近需求中心的經營模式,而不再僅依賴少數大城市。

氣候變遷加劇,加速了保護性耕作方式的推廣應用。

由於氣候不穩定,南美洲室內農業市場越來越多的生產商和投資者正轉向保護性耕作。國際貨幣基金組織(IMF)於2025年3月發布的一份工作報告指出,南美的氣候壓力與反覆發生的干旱密切相關,報告顯示,在厄爾尼諾現象加劇的情況下,巴西每年可能遭遇兩次乾旱。巴西官方於2024年12月發布的作物調查顯示,該國作物產量較前一年顯著下降,印證了露天耕作的生產風險。 2025年食品通膨率也上升,顯示氣候壓力不僅限於農場層面,也波及到消費者和零售商。 AgroUrbana公司位於智利的Quiricula垂直農場提供了一個切實可行的反例。該農場每年可進行52個種植週期,同時用水量比露天耕作減少95%,這表明在可控條件下,作物產量可以與降雨波動脫鉤。這種轉變也正在改變農業風險的定價方式。室內設施正日益被視為食品供應鏈中的韌性基礎設施。這種重新定位進一步證明了對南美洲室內農業市場進行資本投資的合理性,對於擁有清晰分銷管道和強大技術管理能力的企業而言,收益尤其顯著。

高額的資金和能源需求

高昂的初始成本仍是南美洲室內農業市場整體擴張的最大障礙。根據Pink Farms披露,到2025年,能源成本將佔營運支出的40%,僅此一項就足以解釋為何許多設施難以在試點規模之外進行擴張,除非電力供應條件得到保障。在藉貸成本高且長期企劃案融資有限的市場中,資金負擔更為沉重。這減緩了糧食安全狀況嚴峻但商業資金籌措困難的地區(例如哥倫比亞內陸、巴西北部和秘魯部分地區)的擴張速度。在阿根廷,貨幣貶值導致進口氣候控制系統和照明設備的成本大幅上漲,加劇了類似的問題。雖然小規模經營者可以透過溫室模式進入市場,但高密度室內垂直農場仍需大量投資才能達到獲利的成本水準。因此,南美洲室內農業市場在富裕的都市區比在本地生產能填補最大供應缺口的地區成長更快。

細分市場分析

2025年,水耕技術在南美洲室內農業市場佔據48.2%的佔有率,並持續維持其主導地位,這主要得益於商業溫室經營者對標準化營養供應、更短種植週期和高效水資源管理系統的青睞。同時,土壤栽培也獲得了轉型溫室農戶的支持,他們希望降低技術複雜性並與有機農業相容。因此,水耕系統在可控環境農業(CEF)中生產的綠葉蔬菜、香草和高階園藝作物方面仍然佔據商業性主導地位。

預計到2031年,氣耕將以15.1%的複合年成長率成長,成為南美洲室內農業市場成長最快的系統。這一成長主要得益於人們對節水、精準營養管理和氣候適應型生產系統日益成長的需求。自巴拉那州於2026年推出水耕認證體系,以及巴西農業研究公司(Embrapa)推動封閉回路型氣耕農業研究以來,市場對先進室內農業技術的商業性信心穩步提升。此外,結合了水耕穩定性氣耕耕效率的混合農業系統,正吸引全部區域越來越多的投資,用於生產高價值作物。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 都市區對生鮮食品的需求不斷成長

- 由於氣候變遷加劇,保護性耕作方法的採用正在不斷推進。

- 加大對溫室和水耕技術的投資

- 提高LED和自動化技術的成本效益

- 現代零售和餐飲服務業的擴張

- 引進熱帶適應性雜交種子

- 市場限制因素

- 需要大量的資金和精力。

- 缺乏受控環境下的農業專業知識

- 外匯波動影響進口技術

- 基礎設施和電力供應不穩定

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 培訓系統

- 水耕法

- 氣耕

- 水耕法

- 土壤耕作

- 混合

- 依設施類型

- 玻璃或聚碳酸酯溫室

- 室內垂直農業

- 貨櫃農場

- 室內深水養殖系統

- 其他設施類型

- 按作物類型

- 水果和蔬菜

- 綠葉蔬菜

- 番茄

- 黃瓜

- 辣椒粉和辣椒

- 草莓

- 其他水果和蔬菜

- 香草和微型菜苗

- 羅勒

- 薄荷

- 歐芹和香菜

- 其他香草和微型菜苗

- 花卉和觀賞植物

- 鮮切花

- 盆栽觀賞植物

- 其他

- 水果和蔬菜

- 國家

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 秘魯

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Pink Farms

- BeGreen Fazendas Urbanas

- AgroUrbana

- HidroBio SA

- Raiz Vertical Farms Inc.

- Aguap Fazenda Urbana

- Cubo Farm

- Hidrohorta Zangalli

- Colheita Urbana

- VerdeVida

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america indoor farming market size is projected to grow from USD 1.48 billion in 2025 and USD 1.64 billion in 2026 to USD 2.74 billion by 2031, registering a CAGR of 10.82% between 2026 and 2031.

This report is Segmented by Growing System (Aeroponics, Hydroponics, Aquaponics, and More), by Facility Type (Glass or Poly Greenhouses, Indoor Vertical Farms, Container Farms, and More), by Crop Type (Fruits and Vegetables, Herbs and Microgreens, and More), and by Country ( Brazil, Argentina, Chile, and More). The Market Forecasts are Provided in Terms of Value (USD).

South America Indoor Farming Market Trends and Insights

Rising Urban Demand for Fresh Produce

Urbanization is changing how fresh food is bought across the South America indoor farming market. Brazil's Census, published in 2024, showed an urbanization rate of 87.4%, which placed a very large share of the population inside metro supply zones where quality, shelf life, and frequency matter more than seasonal availability. The same broad pattern is visible across Latin America and the Caribbean, where 81% of people were urban, which narrowed the distance between food insecurity concerns and commercial sourcing decisions. March 2026 retail data in Brazil also showed record monthly sales, with the food segment outperforming broader retail activity, which signaled sustained urban demand for fresh products sold through formal channels. This matters for the South American indoor farming market because urban supermarkets and food-service buyers need year-round volumes, stable specifications, and traceability that open-field supply does not always provide. The strongest demand is no longer limited to Sao Paulo, Santiago, and Bogota, because secondary cities such as Curitiba, Recife, Medellin, and Lima Norte are also expanding their formal retail footprint. That widening urban map gives indoor operators more room to replicate their model near demand centers instead of depending only on a few primary metros.

Climate Volatility Increasing Protected Cultivation Adoption

Climate instability is pushing more growers and investors toward protected production in the South America indoor farming market. An International Monetary Fund working paper published in March 2025 linked South America's weather stress to recurring droughts, and it recorded Brazil at 2 drought events per year under an El Nino-amplified pattern. Brazil's official crop survey released in December 2024 showed that the country's harvest declined significantly year over year, which reinforced the production risk attached to open-field farming. Food inflation also increased in 2025, which showed that weather pressure was reaching consumers and retailers rather than staying only at the farm level. AgroUrbana's Quilicura vertical farm in Chile offers a practical counterpoint, because it reported 52 crop cycles per year with 95% less water than field farming, proving that controlled environments can separate output from rainfall volatility. This shift is changing how agricultural risk is priced, since indoor assets are increasingly treated as resilience infrastructure inside food supply chains. That reclassification improves the case for capital deployment in the South America indoor farming market, especially for operators with clear offtake and strong technical control.

High Capital and Energy Requirements

High upfront cost is still the clearest barrier to wider deployment across the South America indoor farming market. Pink Farms' disclosures showed that energy represented 40% of operating expenditure in 2025, and this alone explains why many facilities struggle to scale beyond pilot size without access to favorable power terms. The capital burden is even harder in markets where debt remains expensive and long-tenor project finance is limited. This slows expansion in places where food insecurity is strong but commercial funding is weak, including inland Colombia, northern Brazil, and parts of Peru. Argentina faces a sharper version of the same issue because imported climate systems and lighting become far more expensive after currency depreciation cycles. Smaller operators can enter with greenhouse models, but dense indoor vertical farms still need large investment before they reach a viable cost base. The result is that the South America indoor farming market grows faster in wealthier urban corridors than in the places where local production could solve the biggest supply gaps.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Greenhouse and Hydroponic Investments

- Improving Light Emitting Diode and Automation Cost Economics

- Limited Controlled-Environment Agronomy Expertise

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hydroponics accounted for 48.2% of the South America indoor farming market share in 2025, maintaining its leading position due to the preference of commercial greenhouse operators for standardized nutrient delivery, faster crop cycles, and efficient water management systems. At the same time, soil-based indoor cultivation gained traction among transitional greenhouse farms seeking lower technological complexity and compatibility with organic cultivation. As a result, hydroponic systems remained commercially dominant for leafy vegetables, herbs, and premium horticultural crops produced within controlled-environment farming operations.

Aeroponics is estimated to grow at a 15.1% CAGR through 2031, making it the fastest-growing system in the South America indoor farming market. This growth is driven by increasing prioritization of water efficiency, precision nutrient management, and climate-resilient production systems. Since Parana introduced hydroponic certification pathways in 2026 and Embrapa advanced research on closed-loop aeroponic cultivation, commercial confidence in advanced indoor growing technologies has steadily increased. Additionally, hybrid cultivation systems that combine hydroponic stability with aeroponic efficiency are attracting growing investment for high-value crop production across the region.

Complete Report Scope:

- By Growing System

- Hydroponics

- Aeroponics

- Aquaponics

- Soil-based

- Hybrid

- By Facility Type

- Glass or Poly Greenhouses

- Indoor Vertical Farms

- Container Farms

- Indoor Deep-Water Culture Systems

- Other Facility Type

- By Crop Type

- Fruits and Vegetables

- Leafy Greens

- Tomato

- Cucumber

- Bell Pepper and Chili Pepper

- Strawberry

- Other Fruits and Vegetables

- Herbs and Microgreens

- Basil

- Mint

- Parsley and Cilantro

- Other Herbs and Microgreens

- Flowers and Ornamentals

- Cut Flowers

- Potted Ornamentals

- Others

- Fruits and Vegetables

- By Country

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

List of Companies Covered in this Report:

- Pink Farms

- BeGreen Fazendas Urbanas

- AgroUrbana

- HidroBio S.A.

- Raiz Vertical Farms Inc.

- Aguap Fazenda Urbana

- Cubo Farm

- Hidrohorta Zangalli

- Colheita Urbana

- VerdeVida

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising urban demand for fresh produce

- 4.2.2 Climate volatility increasing protected cultivation adoption

- 4.2.3 Expanding greenhouse and hydroponic investments

- 4.2.4 Improving LED and automation cost economics

- 4.2.5 Growing modern retail and foodservice expansion

- 4.2.6 Adoption of tropicalized hybrid seed varieties

- 4.3 Market Restraints

- 4.3.1 High capital and energy requirements

- 4.3.2 Limited controlled-environment agronomy expertise

- 4.3.3 Currency volatility affecting imported technologies

- 4.3.4 Inconsistent infrastructure and electricity availability

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Growing System

- 5.1.1 Hydroponics

- 5.1.2 Aeroponics

- 5.1.3 Aquaponics

- 5.1.4 Soil-based

- 5.1.5 Hybrid

- 5.2 By Facility Type

- 5.2.1 Glass or Poly Greenhouses

- 5.2.2 Indoor Vertical Farms

- 5.2.3 Container Farms

- 5.2.4 Indoor Deep-Water Culture Systems

- 5.2.5 Other Facility Type

- 5.3 By Crop Type

- 5.3.1 Fruits and Vegetables

- 5.3.1.1 Leafy Greens

- 5.3.1.2 Tomato

- 5.3.1.3 Cucumber

- 5.3.1.4 Bell Pepper and Chili Pepper

- 5.3.1.5 Strawberry

- 5.3.1.6 Other Fruits and Vegetables

- 5.3.2 Herbs and Microgreens

- 5.3.2.1 Basil

- 5.3.2.2 Mint

- 5.3.2.3 Parsley and Cilantro

- 5.3.2.4 Other Herbs and Microgreens

- 5.3.3 Flowers and Ornamentals

- 5.3.3.1 Cut Flowers

- 5.3.3.2 Potted Ornamentals

- 5.3.4 Others

- 5.3.1 Fruits and Vegetables

- 5.4 By Country

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Pink Farms

- 6.4.2 BeGreen Fazendas Urbanas

- 6.4.3 AgroUrbana

- 6.4.4 HidroBio S.A.

- 6.4.5 Raiz Vertical Farms Inc.

- 6.4.6 Aguap Fazenda Urbana

- 6.4.7 Cubo Farm

- 6.4.8 Hidrohorta Zangalli

- 6.4.9 Colheita Urbana

- 6.4.10 VerdeVida

7 Market Opportunities and Future Outlook

美國室內農業:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

美國室內農業:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 室內農業市場規模、佔有率、趨勢和預測:按設施類型、作物類型、組件、種植系統和地區分類,2026-2034 年中東和非洲室內農業:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

室內農業市場規模、佔有率、趨勢和預測:按設施類型、作物類型、組件、種植系統和地區分類,2026-2034 年中東和非洲室內農業:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 室內農業市場-全球產業規模、佔有率、趨勢、機會、預測:種植技術、設施類型、組成部分、作物類型、地區及競爭格局,2021-2031年

室內農業市場-全球產業規模、佔有率、趨勢、機會、預測:種植技術、設施類型、組成部分、作物類型、地區及競爭格局,2021-2031年 室內農業技術市場:全球市場預測(依產品類型、作物類型、耕作方式、自動化程度和最終用戶分類)-2026年至2032年

室內農業技術市場:全球市場預測(依產品類型、作物類型、耕作方式、自動化程度和最終用戶分類)-2026年至2032年 2026年全球室內農業市場報告2026年全球室內農業技術市場報告

2026年全球室內農業市場報告2026年全球室內農業技術市場報告 室內農業市場規模、佔有率和趨勢分析報告:按組件、設施類型、作物類別、種植機制、地區和細分市場分類 - 預測,2026-2033 年日本室內農業市場報告:按設施類型、作物類型、組件、種植系統和地區分類,2026-2034年

室內農業市場規模、佔有率和趨勢分析報告:按組件、設施類型、作物類別、種植機制、地區和細分市場分類 - 預測,2026-2033 年日本室內農業市場報告:按設施類型、作物類型、組件、種植系統和地區分類,2026-2034年 室內農業技術市場規模、佔有率和成長分析(按種植系統、設施類型、作物類型和地區分類)-2026-2033年產業預測

室內農業技術市場規模、佔有率和成長分析(按種植系統、設施類型、作物類型和地區分類)-2026-2033年產業預測