|

市場調查報告書

商品編碼

2065613

AI原生HCM平台:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)AI-Native HCM Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

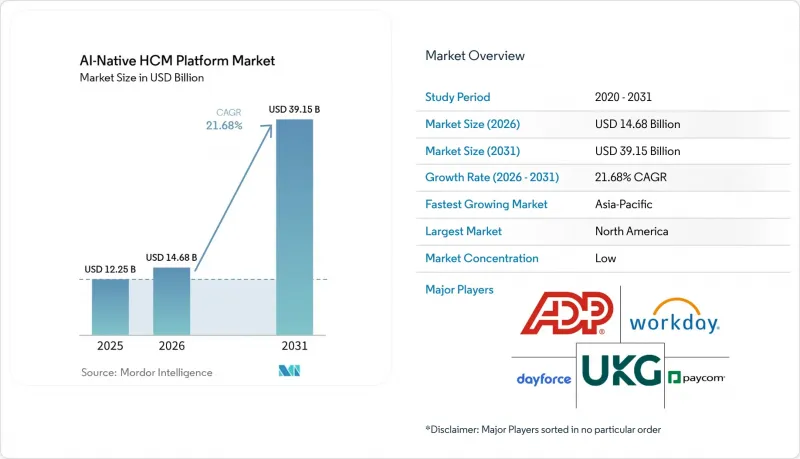

根據 Mordor Intelligence 預測,人工智慧原生 HCM 平台的市場規模預計將從 2025 年的 122.5 億美元成長到 2026 年的 146.8 億美元,然後在 2031 年達到 391.5 億美元,2026 年至 2031 年的複合年成長率為 21.68%。

本報告按元件(平台軟體和服務)、部署模式(雲端部署、本地部署、混合部署)、企業規模(大型企業和中小企業)、應用程式(例如人才招聘)、最終用戶產業(例如銀行、金融服務和保險、醫療保健和生命科學)以及地區進行細分。市場預測以價值(美元)表示。

全球人工智慧原生HCM平台市場趨勢及洞察

AI 副駕駛從試點階段過渡到「系統記錄」工作流程

AI原生HCM平台市場最大的成長要素源自於從孤立的用例向生產工作流程的轉變,這種轉變將取代傳統的基於菜單的HR工作模式。到2026年,買家將不再僅僅詢問輔助工具能否回答問題,而是會關注這些工具能否在記錄系統中完成多階段任務,並具備清晰的權限和審計追蹤。根據SHRM的研究,92%的首席人力資源長(CHRO)預計2026年將進一步整合AI,高於2025年的83%。此外,39%的人力資源部門已經採用了AI,其中招聘(27%)、人力資源技術管理(21%)和學習與發展(17%)是應用最廣泛的領域。這種採用模式表明,人力資源部門在將AI轉化為日常營運的基礎架構方面,比許多其他後勤部門部門進展更快。 Workday在2026年3月透過全球發布Sana強化了這一方向,並在2026年5月透過將Sana自助服務代理整合到Microsoft 365 Copilot中進一步擴展了該模式。這使得員工能夠在日常工作環境中執行與人力資源相關的操作,而無需切換到單獨的應用程式。因此,人工智慧原生HCM平台市場正從單純提案平台轉向提供可操作的平台,而這種轉變正在穩步提高合約續約和擴展決策的門檻。

基於技能的人才規劃正成為決定是否實施人力資本管理 (HCM) 的關鍵標準。

在原生人工智慧HCM平台市場,基於技能的人才規劃在採購決策中扮演著越來越重要的角色。這是因為靜態的崗位架構已無法跟上企業內部角色重塑的腳步。負責人越來越重視那些能夠推斷技能、持續更新分類並將人才規劃與不斷變化的業務需求相銜接的平台。這種轉變使得技能智慧不再只是一個附加模組,而是成為招募、內部調動、重新部署和學習等各環節的架構控制點。影響採購決策的人員組成也在發生變化,財務主管和業務部門負責人不再僅僅將人才能力視覺化視為一個狹隘的人力資源流程問題,而是將其視為企業規劃框架的一部分。能夠展示檢驗的技能供需庫、更完善的重新部署邏輯以及人才數據與規劃工作流程緊密整合的供應商,正在原生人工智慧HCM平台市場中贏得更多關注。因此,產品藍圖正朝著嵌入式推論功能、分類管理以及能夠將技能資料轉換為實際員工部署行動的管理工具方向發展。

高度敏感的人力資源資料的管治和問責要求

由於人力資源系統處理與薪酬、績效、休假、身分和員工行為相關的高度敏感記錄,因此管治仍然是人工智慧原生人力資本管理(HCM)平台市場面臨的最大限制因素。採購團隊現在要求從評估初期就具備可解釋性、文件化、可審計性和人工監督,而不是將這些視為以後再處理的法律細節。報告發現,雖然49%部署或試用人工智慧的組織已經制定了員工人工智慧政策,但只有25%的組織認為他們的政策「清晰且具有前瞻性」。此外,在美國人口最多的19個州(這些州已實施人工智慧就業法),57%的人力資源負責人不知道這些法律的存在。在歐洲,歐盟人工智慧法案和GDPR為就業相關的人工智慧提供了更嚴格的法規結構,要求在這些系統上市之前,必須考慮高風險使用控制、人工監督和資料影響。人工智慧原生HCM平台市場也面臨巨大的財務風險。第 99 條規定,違規行為最高可處以 3,500 萬歐元的罰款。根據美國國稅局 2025 年的平均年度外匯計算,這相當於約 3,790 萬美元,或全球整體年銷售額的 7%。雖然這會延緩一些採購決策,但對於那些早期在其平台中整合可解釋性和結果記錄功能的供應商來說,卻是一大利好。

細分市場分析

平台軟體仍然是AI原生HCM平台市場中最大的組成部分,預計到2025年將佔總收入的66.41%。這意味著核心套件仍然佔據大部分支出,因為買家正在將人力資源記錄、勞動力智慧和自動化功能整合到單一平台中。這反映了市場對AI核心HCM平台和決策引擎的需求,這些平台和引擎能夠整合先前分散在不同工具中的工作流程。從實際角度來看,軟體仍然是企業採購的重要組成部分,因為企業首先需要一個能夠整合人才資料、流程規則和AI驅動操作的基礎系統。同時,由於AI在人力資源領域的應用涉及敏感的員工記錄和業務關鍵型工作流程,買家越來越重視軟體層的管治和安全功能。從這個意義上講,平台軟體在2025年仍將是AI原生HCM平台市場規模的核心組成部分。

同時,預計到2031年,服務業的複合年成長率將達到23.12%,超過平台軟體的成長速度。這顯示大規模部署的實際複雜性。由於人工智慧原生平台部署在各種不同的環境中,而非全新的環境中,企業正在增加在實施設計、跨國部署支援、合規諮詢和模型管治的支出。對於那些缺乏能夠建立勞動力智慧模型並管理人力資源、IT、法律和財務等跨職能部門責任的內部團隊的組織而言,這種趨勢尤其明顯。軟體市場佔有率和服務成長率之間的差距表明,人工智慧原生人力資本管理(HCM)平台產業仍處於建構階段,營運變革與產品功能同樣重要。這也意味著,即使軟體功能趨於整合,擁有強大服務生態系統的供應商也能更好地保護客戶價值。在人工智慧原生HCM平台市場,服務不再只是軟體的補充支援層,而是部署邏輯本身不可或缺的一部分。

預計到2025年,雲端採用將佔人工智慧原生HCM平台市場收入的72.41%,凸顯了SaaS優先的採購模式仍是核心人力資源現代化的主流方向。雲端仍然是首選,因為與傳統的本地部署環境相比,它能為買家提供更快的版本發布、更廣泛的整合選項以及更便捷的AI功能存取。這也與用戶對整合套件的普遍偏好相符,這些套件能夠從通用記錄層支援自助服務、分析和工作流程編配。對雲端的集中需求表明,人工智慧原生HCM平台市場仍然由那些旨在定期更新和持續模型改進的平台驅動。買家仍然認為,雲端是整合人力資源、薪資和勞動力智慧的最實用方式,無需在任何本地環境中重建這些關係。

混合部署仍然是成長最快的模式,預計到2031年將以22.68%的複合年成長率成長。這意味著實際的購買行為比單純的「雲端優先」模式更為多樣化。在監管嚴格的行業和注重資料主權的市場中,通常無法在預測期內將所有薪資、身分或員工記錄遷移到第三方基礎設施。此外,大型企業也面臨一個實際挑戰:即使前端HCM層能夠儘早遷移,更換薪資核算引擎和相關系統也可能需要數年時間。這就催生了對能夠提供基於雲端的AI推理、分析和使用者體驗,同時又能解決本地資料限制的平台的需求。雖然本地部署的佔有率正在下降,但對於那些員工資料處理不僅受技術因素監管,還受法律或製度限制的客戶而言,本地部署仍然佔據重要地位。因此,在AI原生HCM平台產業,那些將混合架構定位為深思熟慮的產品策略而非臨時妥協方案的供應商,仍然備受青睞。

區域分析

北美仍是人工智慧原生HCM平台市場最大的區域貢獻者,在2025年佔40.12%的銷售額。該地區受益於許多大型企業已積極參與人工智慧項目,以及成熟的企業軟體採購環境,從而加快了評估和購買週期。具體而言,北美在2025年佔據人工智慧原生HCM平台市場40.12%的佔有率,主要歸功於其買家在雲端HCM採用、人工智慧概念驗證以及與多功能平台整合方面比其他地區更為先進。此外,預計該地區的競爭格局將在2026年呈現兩極分化,老牌供應商將繼續在與大型企業的合約續約中保持優勢,而快速發展的新興企業則透過縮短部署時間,在中小型企業市場迅速崛起。

預計到2031年,亞太地區將以24.47%的複合年成長率成長,成為人工智慧原生HCM平台市場成長最快的區域板塊。該地區提供待開發區HCM部署路徑,使許多買家能夠繞過舊有系統的束縛,從而避免在成熟的西方市場中自動化進程受阻。重新評估優先考慮速度和人工智慧整合的商業模式,正在重塑日本、韓國、澳洲和東南亞首席人力資源長(CHRO)的優先事項。印度是一個特別重要的市場,因為亞太地區誕生的供應商正在向海外出口人工智慧原生HCM功能,而不再僅限於國內市場。中國憑藉其龐大的規模和獨特的市場特徵,仍然是一個重要的市場,因為本地數據居住要求和政府合規要求會影響平台設計。同時,在澳洲、韓國和東南亞國家,數位轉型(DX)計畫和雇主對現代化勞動力管理系統日益成長的需求,也持續推動HCM的普及。

預計到2025年,以德國、英國和法國為首的歐洲將佔據人工智慧原生HCM平台收入的很大一部分。該地區的短期採購行為更取決於供應商能否有效滿足歐盟框架下的薪酬透明度法規、人工智慧風險分類以及資料處理義務,而非功能比較。南美洲和中東及非洲地區尚處於早期應用階段,但仍是重要的成長區域,在這些市場中,行動優先、人力智慧整合的平台正在迅速發展,而傳統的桌面人力資源系統尚未完全普及。巴西和沙烏地阿拉伯在各自的次區域中扮演著核心角色,而奈及利亞和南非則在非洲脫穎而出,跨國公司正透過人才管理現代化計畫持續支持第一波基於雲端的HCM應用浪潮。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- AI 副駕駛:從試點階段過渡到工作流程記錄系統

- 基於技能的人才規劃正成為人力資本管理實施的關鍵選擇標準。

- 雲端人力資源的現代化和套件的整合正在推動人工智慧嵌入式平台的普及。

- 員工自助服務和經理支援工具的需求持續成長

- 需要統一各公司間分散的技能分類系統。

- 透過即時就業數據和員工記錄的現代化,改善人工智慧環境。

- 市場限制因素

- 敏感人事資料的管治和可解釋性要求

- 傳統薪資核算和身分管理系統正在減緩端到端自動化流程。

- 歐盟人工智慧法和員工代表延長銷售週期的義務。

- 技能本體與勞動力資料標準之間存在互通性差距。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 平台軟體

- AI核心HCM平台

- 人工智慧副駕駛和互動式人力資源助手

- 勞動力智慧與決策引擎

- 技能智慧平台

- 自主人力資源工作流程自動化平台

- 人工智慧管治、安全和合規平台

- 服務

- 平台軟體

- 按部署模式

- 雲

- 現場

- 混合實現

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 透過使用

- 人才獲取、招募和候選人情報

- 人力資源管理與員工洞察

- 薪資、補償與福利情報

- 人員規劃、分析與決策情報

- 學習、技能分析、內部遷移

- 員工體驗、人力資源服務交付、人工智慧助手

- 自主人力資源工作流程自動化

- 人工智慧管治、合規和員工風險管理

- 按最終用戶行業分類

- BFSI

- 醫療保健和生命科學

- 資訊科技/通訊

- 零售與電子商務

- 工業製造

- 政府/公共部門

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Workday, Inc.

- Dayforce, Inc.

- UKG Inc.

- ADP, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Paychex, Inc.

- Paycor HCM, Inc.

- BambooHR LLC

- Personio SE and Co. KG

- HiBob Ltd.

- Darwinbox Digital Solutions Private Limited

- Rippling, Inc.

- Deel Inc.

- Remote Technology, Inc.

- Factorial HR, SL

- Employment Hero Pty Ltd

- PayFit SAS

- Humaans Ltd

- ZingHR India Private Limited

- Namely, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the aI-Native hCM platform market size is expected to grow from USD 12.25 billion in 2025 to USD 14.68 billion in 2026 and is forecast to reach USD 39.15 billion by 2031 at 21.68% CAGR over 2026-2031.

This report is Segmented by Component (Platform Software, and Services), Deployment Model (Cloud, On-Premises, and Hybrid Deployment), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Application (Talent Acquisition, and More), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI-Native HCM Platform Market Trends and Insights

Artificial Intelligence Copilots Moving From Pilot To System Of Record Workflows

The strongest growth force in the AI-Native HCM Platform Market is the shift of AI assistants from isolated use cases into production workflows that replace older menu-based HR interaction patterns. By 2026, buyers are no longer asking only whether copilots can answer questions; they are asking whether those tools can complete multistep tasks inside systems of record with clear permissions and audit trails. SHRM noted that 92% of CHROs expected further AI integration in 2026, up from 83% in 2025, and AI was already deployed in 39% of HR functions, led by recruiting at 27%, HR technology administration at 21%, and learning and development at 17%. That adoption pattern shows HR moving faster than many other back-office functions in turning AI into day-to-day operating infrastructure. Workday reinforced this direction in March 2026 with the global release of Sana, and then expanded the model in May 2026 by bringing Sana Self-Service Agent into Microsoft 365 Copilot, placing HR actions within an employee's normal work environment rather than requiring a switch back to a separate application. The AI-Native HCM Platform Market is therefore moving toward platforms that can execute, not just suggest, and that shift is steadily raising the bar for renewal and expansion decisions.

Skills-Based Workforce Planning Becoming A Core HCM Buying Criterion

Skills-based workforce planning has moved closer to the center of buying decisions in the AI-Native HCM Platform Market because static job architectures no longer support the pace of role redesign taking place across enterprises. Buyers are placing more emphasis on platforms that can infer skills, maintain living taxonomies, and connect workforce planning to changing business demand. That change is making skills intelligence less of a side module and more of an architectural control point for hiring, internal mobility, redeployment, and learning. It also changes who influences purchases, because finance leaders and business unit heads now view workforce capability visibility as part of enterprise planning discipline rather than a narrow HR process issue. Vendors that can show verified skills supply and demand libraries, better redeployment logic, and tighter links between workforce data and planning workflows are gaining more attention in the AI-Native HCM Platform Market. This is also pushing product roadmaps toward embedded inference, taxonomy management, and manager-facing tools that translate skills data into staffing actions.

Sensitive HR Data Governance And Explainability Requirements

Governance remains the clearest restraint on the AI Native HCM Platform Market because HR systems handle highly sensitive records tied to compensation, performance, leave, identity, and employee behavior. Procurement teams are now asking for explainability, documentation, auditability, and human oversight controls at the start of evaluation rather than treating them as legal details to resolve later. Reports show that 49% of organizations using or piloting AI had workforce AI policies, yet only 25% of that group described those policies as clear and future-proof, and 57% of HR professionals in the 19 most populous U.S. states with active AI employment laws were unaware that those laws existed. In Europe, the EU AI Act and the GDPR set a stricter regulatory framework for employment-related AI and require controls on high-risk uses, human oversight, and data impact considerations before those systems can be placed on the market. The AI Native HCM Platform Market also faces a significant financial risk threshold, as Article 99 allows penalties of up to EUR 35 million, which the 2025 IRS yearly average exchange rate reference places at approximately USD 37.9 million, or 7% of global annual turnover for non-compliance. This is slowing some purchase decisions, but it is also rewarding vendors that built explainability and outcome logging into their platforms earlier.

Other drivers and restraints analyzed in the detailed report include:

- Cloud HR Modernization And Suite Consolidation Favoring AI-Embedded Platforms

- Demand For Continuous Employee Self-Service And Manager Assistants

- Legacy Payroll And Identity Stacks Slowing End-To-End Automation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform software remained the largest component in the AI-Native HCM Platform Market and held 66.41% of 2025 revenue, which means core suites still capture most spending when buyers consolidate HR records, workforce intelligence, and automation capabilities in one platform. That position reflects demand for AI core HCM platforms and decision engines that unify workflows previously spread across separate tools. In practical terms, software still anchors most enterprise purchasing because organizations first need the base system where people data, process rules, and AI actions can sit together. At the same time, buyers are placing greater weight on governance and security features within the software layer, as AI use in HR now touches sensitive employee records and business-critical workflows. In that sense, platform software continues to define the operating center of the AI-Native HCM Platform Market size in 2025.

Services, however, are projected to expand at a 23.12% CAGR through 2031, faster than platform software, which points to the real complexity of deployment at scale. Enterprises are spending more on implementation design, multi-country rollout support, compliance advisory, and model governance because AI-native platforms are being deployed across varied environments rather than in clean, greenfield settings. This pattern is especially visible in organizations that lack internal teams capable of configuring workforce intelligence models or managing cross-functional ownership between HR, IT, legal, and finance. The gap between software share and service growth suggests that the AI-Native HCM Platform Industry is still in a build-out phase, where operating change matters almost as much as product functionality. It also means that vendors with strong service ecosystems can protect account value even as software features converge. In the AI-Native HCM Platform Market, services are no longer a support layer around software; they are part of the adoption logic itself.

Cloud deployment accounted for 72.41% of 2025 revenue in the AI-Native HCM Platform Market, underscoring that SaaS-first buying behavior continues to define the mainstream direction of core HR modernization. Cloud remained the default because it offers buyers faster releases, broader integration options, and easier access to AI capabilities than older on-premises environments. It also aligns with the broader preference for unified suites that can support self-service, analytics, and workflow orchestration from a common record layer. The concentration of demand in cloud shows that the AI-Native HCM Platform Market size still rests on platforms designed for regular updates and continuous model improvement. Buyers continue to view the cloud as the most practical way to connect HR, payroll, and workforce intelligence without rebuilding those relationships locally in every environment.

Hybrid deployment is still the fastest-growing model and is projected to expand at a 22.68% CAGR through 2031, which means real buying behavior is more mixed than a simple cloud-first story would suggest. Regulated sectors and data-sovereign markets often cannot move every payroll, identity, or worker record into third-party infrastructure within the forecast window. Large enterprises also face the practical problem that payroll engines and adjacent systems may take years to replace, even when the front-end HCM layer moves earlier. This creates demand for platforms that can address local data constraints while still providing cloud-based AI inference, analytics, and user experience. On-premises deployment is losing share, but it remains important in accounts where worker data handling is governed by legal or institutional limits rather than by technology alone. The AI-Native HCM Platform Industry, therefore, continues to reward vendors that treat hybrid architecture as a deliberate product path rather than a temporary compromise.

Geography Analysis

North America held 40.12% of 2025 revenue and remained the largest regional contributor to the AI Native HCM Platform Market. The region benefited from a dense base of large enterprises already active in AI programs and from a mature enterprise software-buying environment that enabled faster evaluation and purchasing cycles. In practical terms, North America accounted for 40.12% of the AI Native HCM Platform Market share in 2025 because buyers there were further along in cloud HCM adoption, AI experimentation, and multi-function platform consolidation. The region also showed a split competitive pattern in 2026, with incumbents retaining strength in large enterprise renewals while faster-moving challengers gained traction in mid-market and SME accounts through shorter deployment windows.

Asia Pacific is projected to expand at a 24.47% CAGR through 2031, making it the fastest-growing regional bloc in the AI Native HCM Platform Market. The region benefits from greenfield cloud HCM deployment paths that let many buyers bypass the legacy drag that slows automation in mature Western markets. CEO reassessment of operating models for speed and AI integration is reshaping CHRO priorities across Japan, South Korea, Australia, and Southeast Asia. India is especially important because vendors born in APAC are exporting AI native HCM capabilities rather than remaining purely domestic suppliers. China remains important as a large but distinct market where local data residency and government compliance requirements shape platform design, while Australia, South Korea, and Southeast Asian economies continue to support adoption through digital transformation programs and rising employer demand for modern workforce systems.

Europe accounted for meaningful 2025 revenue in the AI Native HCM Platform Market, led by Germany, the United Kingdom, and France. The region's near-term buying behavior is being shaped less by feature comparison alone and more by how well vendors can handle pay transparency rules, AI risk classification, and data processing obligations under the EU framework. South America, the Middle East, and Africa are earlier-stage regions, but they remain important growth territories where mobile-first and AI-embedded platforms are gaining traction in markets that did not fully institutionalize older desktop HR stacks. Brazil and Saudi Arabia serve as anchor markets in their respective sub-regions, while Nigeria and South Africa stand out across Africa as multinational employers continue to support first-wave cloud HCM adoption through workforce modernization programs.

- Workday, Inc.

- Dayforce, Inc.

- UKG Inc.

- ADP, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Paychex, Inc.

- Paycor HCM, Inc.

- BambooHR LLC

- Personio SE and Co. KG

- HiBob Ltd.

- Darwinbox Digital Solutions Private Limited

- Rippling, Inc.

- Deel Inc.

- Remote Technology, Inc.

- Factorial HR, S.L.

- Employment Hero Pty Ltd

- PayFit SAS

- Humaans Ltd

- ZingHR India Private Limited

- Namely, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Artificial Intelligence Copilots Moving From Pilot to System of Record Workflows

- 4.2.2 Skills-Based Workforce Planning Becoming a Core HCM Buying Criterion

- 4.2.3 Cloud HR Modernization and Suite Consolidation Favoring AI-Embedded Platforms

- 4.2.4 Demand for Continuous Employee Self-Service and Manager Assistants

- 4.2.5 Need to Harmonize Fragmented Skills Taxonomies Across Enterprises

- 4.2.6 Real-Time Employment Data and Worker Record Modernization Improving AI Context

- 4.3 Market Restraints

- 4.3.1 Sensitive HR Data Governance and Explainability Requirements

- 4.3.2 Legacy Payroll and Identity Stacks Slowing End-to-End Automation

- 4.3.3 EU AI Act and Works Council Obligations Extending Sales Cycles

- 4.3.4 Interoperability Gaps Across Skills Ontologies and Labor Data Standards

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform Software

- 5.1.1.1 AI Core HCM Platforms

- 5.1.1.2 AI Copilots and Conversational HR Assistants

- 5.1.1.3 Workforce Intelligence and Decision Engines

- 5.1.1.4 Skills Intelligence Platforms

- 5.1.1.5 Autonomous HR Workflow Automation Platforms

- 5.1.1.6 AI Governance, Security and Compliance Platforms

- 5.1.2 Services

- 5.1.1 Platform Software

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid Deployment

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Talent Acquisition, Recruiting and Candidate Intelligence

- 5.4.2 Workforce Administration and Employee Intelligence

- 5.4.3 Payroll, Compensation and Benefits Intelligence

- 5.4.4 Workforce Planning, Analytics and Decision Intelligence

- 5.4.5 Learning, Skills Intelligence and Internal Mobility

- 5.4.6 Employee Experience, HR Service Delivery and AI Assistants

- 5.4.7 Autonomous HR Workflow Automation

- 5.4.8 AI Governance, Compliance and Workforce Risk Management

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Workday, Inc.

- 6.4.2 Dayforce, Inc.

- 6.4.3 UKG Inc.

- 6.4.4 ADP, Inc.

- 6.4.5 Paycom Software, Inc.

- 6.4.6 Paylocity Holding Corporation

- 6.4.7 Paychex, Inc.

- 6.4.8 Paycor HCM, Inc.

- 6.4.9 BambooHR LLC

- 6.4.10 Personio SE and Co. KG

- 6.4.11 HiBob Ltd.

- 6.4.12 Darwinbox Digital Solutions Private Limited

- 6.4.13 Rippling, Inc.

- 6.4.14 Deel Inc.

- 6.4.15 Remote Technology, Inc.

- 6.4.16 Factorial HR, S.L.

- 6.4.17 Employment Hero Pty Ltd

- 6.4.18 PayFit SAS

- 6.4.19 Humaans Ltd

- 6.4.20 ZingHR India Private Limited

- 6.4.21 Namely, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

人力資本管理市場:按組件、授權模式、組織規模、部署和產業分類-2026-2032年全球市場預測

人力資本管理市場:按組件、授權模式、組織規模、部署和產業分類-2026-2032年全球市場預測 可組合式 HCM 平台:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)科技業薪酬管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)銀行、金融服務和保險 (BFSI) 行業的薪酬管理:市場佔有率分析、行業趨勢與統計數據、成長預測 (2026-2031)人力資本管理(HCM)企業資源規劃:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031)

可組合式 HCM 平台:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)科技業薪酬管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)銀行、金融服務和保險 (BFSI) 行業的薪酬管理:市場佔有率分析、行業趨勢與統計數據、成長預測 (2026-2031)人力資本管理(HCM)企業資源規劃:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031) 薪資和薪酬管理平台市場預測至2034年-按薪資處理階段、薪酬類型、平台功能、部署模式和最終用戶分類的全球分析雲端HCM平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

薪資和薪酬管理平台市場預測至2034年-按薪資處理階段、薪酬類型、平台功能、部署模式和最終用戶分類的全球分析雲端HCM平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 人力資本管理市場規模、佔有率和成長分析:按交付類型、部署類型、最終用戶產業、組織規模和地區分類-2026-2033年產業預測

人力資本管理市場規模、佔有率和成長分析:按交付類型、部署類型、最終用戶產業、組織規模和地區分類-2026-2033年產業預測 人力資本管理市場規模、佔有率、趨勢和預測:按組件、部署類型、行業和地區分類,2026-2034 年

人力資本管理市場規模、佔有率、趨勢和預測:按組件、部署類型、行業和地區分類,2026-2034 年 2026年全球人力資本管理市場報告

2026年全球人力資本管理市場報告