|

市場調查報告書

商品編碼

2064519

科技業薪酬管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Compensation Management In Technology Sector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

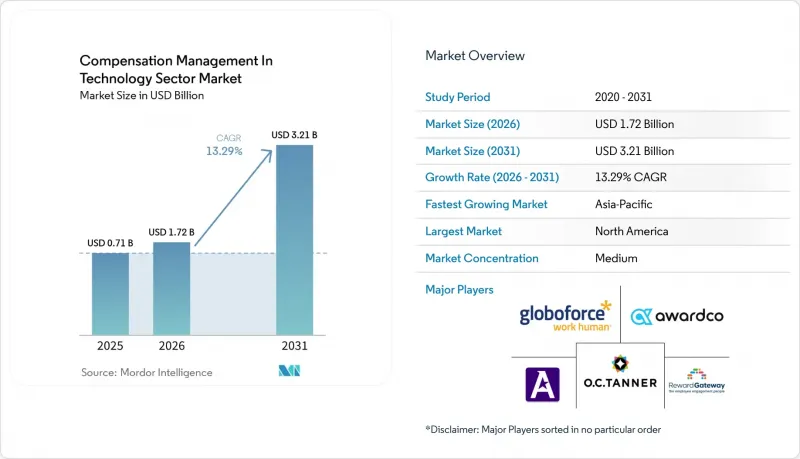

根據 Mordor Intelligence 預測,科技業的薪酬管理市場規模將在 2025 年達到 7.1 億美元,2026 年達到 17.2 億美元,2031 年達到 32.1 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 13.29%。

本報告按元件(軟體和服務)、部署類型(雲端、本地部署、混合部署)、企業規模(大型企業和中小企業)、功能(薪酬規劃、基本工資管理、獎勵薪酬管理等)和地區進行細分。市場預測以美元計價。

全球薪酬管理市場趨勢及技術領域洞察

關於薪酬透明度和公平性的合規期限

科技業的薪酬管理市場正受到合規期限的強烈推動,薪酬管理軟體正從一種可選的人力資源工具轉變為核心管理系統。歐盟《工資透明指令》規定的2026年6月7日截止日期迫使科技公司雇主在披露工資範圍、記錄工資確定過程以及檢驗內部工資差異方面比以往任何時候都更加嚴格。在美國,工資透明度法規正擴展到各州,通常要求發布遠距工作的雇主遵守針對同一職位的多項揭露要求。伊利諾伊州也增加了類似的薪資透明度要求,這增加了同時在多個司法管轄區招募的雇主的壓力。這使得能夠在單一系統中維護政策邏輯、核准歷史記錄和發布管理的、能夠感知不同司法管轄區的薪酬管理平台在科技行業的薪酬管理市場中更具價值。下一波針對大型雇主的報告義務可能會持續推動以合規為主導的積極採購活動,遠遠超出最初的揭露準備階段。

將雲端運算和人工智慧引入薪資工作流程

科技業的薪酬管理也正經歷著從年度薪酬週期轉變為持續決策支援的轉變。到2026年,81%的獎勵薪酬團隊將以某種形式使用人工智慧,其中重度人工智慧用戶對市場變化的準備率高達67%,遠高於使用頻率較低的用戶。一家平台重點介紹了其“人工智慧薪酬代理”,該代理利用來自700多家公司的即時市場數據和大規模的技能圖譜來輔助薪酬提案的製定,最終實現了94%的報價接受率,並將報價提交時間縮短了23%。另一家供應商則展示如何將人工智慧整合到其企業控制框架中,在符合SOC 2 Type II標準的環境中,透過添加生成式人工智慧功能,實現薪酬差距分析、預算情境建模和即時薪酬模擬。這些新產品的發布之所以對科技業的薪酬管理市場意義重大,是因為買家現在期望系統能夠根據不斷變化的情況動態地指導薪酬決策,而不僅僅是在周期結束後總結結果。將人工智慧與可審計性、管治和安全部署相結合的供應商,比將人工智慧定位為獨立功能的供應商更有可能贏得信任。

薪酬決策方面的預算限制正在減緩套房的擴張。

在科技業的薪酬管理市場,隨著科技公司收緊預算控制,採購週期持續放緩。許多公司優先保障核心規劃模組的部署,推遲在擴展分析、透明度或股權激勵功能方面的支出,直到員工人數和招募計畫更加明朗。這種情況在中小型科技公司中尤其明顯,雖然這些公司了解管治的必要性,但在謹慎的招募時期,部署大型平台並非總是合理的。雖然這種支出模式通常不會將薪酬管理軟體排除在藍圖之外,但它往往會導致分階段部署,並限制短期模組的擴展。在科技業的薪酬管理市場,這一趨勢有利於提供捆綁定價和豐富產品線的供應商,因為買家傾向於深化現有合作關係,而不是添加多個單一功能的工具。這一趨勢推動了大規模平台的發展,同時也為那些只專注於特定細分薪酬應用場景的小規模供應商帶來了挑戰。

細分市場分析

截至2025年,軟體將佔科技業薪酬管理市場71.12%的佔有率,而服務預計到2031年將以15.23%的複合年成長率成長。這一細分錶明,軟體訂閱仍將是主要的收入來源,但購買者對平臺本身以外的支援需求日益成長。科技業薪酬管理市場對服務需求的成長源自於僅靠內部團隊難以完成諸如跨國薪酬設計、工作流程設定、資料遷移和政策協調等任務。這也反映出對服務的需求不斷增加,因為科技公司的薪酬調整往往會同時影響人力資源、財務、經理、負責人和法務團隊。

因此,科技業的薪酬管理模式正在轉向軟體和服務相互補充而非爭奪預算的模式。擁有系統化和整合的薪酬數據的組織往往能夠更快地做出決策,並以更小的干擾適應工作環境的變化。這使得實施和諮詢支援的價值日益凸顯。這種結果差異意義重大,因為許多科技公司的雇主購買的不僅是工具,而是薪酬管治的營運模式。企業合約中安全和合規條款的日益普及也推動了服務需求,這要求供應商和實施合作夥伴在初始部署之後繼續參與其中。

預計到2025年,基於雲端的部署將佔據68.45%的市場佔有率,而混合部署預計到2031年將以14.89%的複合年成長率成長。雲端的主導地位反映了市場對託管基礎設施、便利更新以及與現代人力資源系統無縫整合的強勁需求。然而,科技業的薪酬管理並非簡單地從本地遷移到雲端。許多大型企業仍在運作難以輕易替換的系統。對於那些既需要雲端的分析能力和工作流程柔軟性,又因敏感記錄、資料居住需求或傳統企業架構而需要本地管理的企業而言,混合模式正日益受到青睞。

科技業薪資管理市場對混合解決方案的日益青睞源自於薪資數據很少集中於單一平台。大型企業可能同時使用雲端人力資源資訊系統 (HRIS)、本地部署的財務工具、獨立的股權激勵管理系統以及區域性薪資核算系統,因此,相較於完全替換現有系統,混合化薪資管理階層更為實用。 2026 年,在符合 SOC 2 Type II 標準的安全環境下發布的「Compose Insights」和「Predictive Compensation」表明,供應商正在設計能夠滿足日益嚴格的公司管治要求的產品,而不是假定所有購買者都希望採用簡單的純雲端架構。因此,混合解決方案的成長反映了全球科技企業對支援混合環境的持續需求,而非科技業薪酬管理市場的暫時性轉型。

區域分析

2025年,北美將佔據全球科技業薪酬管理市場41.05%的佔有率。該地區的主導地位源於美國擁有大量科技雇主,同時,積極的薪酬資訊揭露法規確保了薪酬管治始終是至關重要的問題。科羅拉多的執法記錄,包括根據《同工同酬法》提出的糾正建議和罰款,顯示合規風險並非紙上談兵,而是實實在存在的。加拿大對跨國營運的雇主提出了更嚴格的報告要求。同時,墨西哥則受到其美國和歐洲母公司所製定的薪酬管治標準的影響。

到2025年,歐洲將成為全球第二大區域市場,其中德國、英國和法國將是主要的需求中心。歐盟的《工資透明指令》正在從結構上推動歐洲科技產業的薪資管理市場發展,因為雇主被迫制定更正式和規範的薪資流程。歐洲各國之間的差異也增加了工作量,要求雇主根據當地的資訊揭露、文件記錄和員工協商法規調整區域薪酬策略。在德國,由於已經建立了工資透明框架,許多雇主專注於升級現有系統,而不是從零開始建立。在南美洲,巴西和阿根廷仍然是最活躍的市場,因為跨國科技公司通常會在當地法規完全強制執行之前,就將北美或歐洲的薪資標準應用於其營運。

亞太地區是成長最快的地區,預計到2031年,科技業的薪酬管理市場將以16.73%的複合年成長率成長。印度、韓國和東南亞是推動這一成長的主要力量,這得益於科技業對薪酬管理的日益成長的需求,以及分散式工程模式下對更強力的薪酬管治的需求。中國仍然非常重要,但當地的資料法規和採用偏好使得混合模式和在地化模式比簡單的純雲端服務更合適。在中東和非洲地區,薪資管理的應用尚處於早期階段,但隨著該地區科技企業在跨國公司薪資標準下不斷擴張,阿拉伯聯合大公國、沙烏地阿拉伯、南非和奈及利亞等國對薪資管理的興趣正在穩步成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 遵守工資透明度和工資平等規定的最後期限

- 將雲端運算和人工智慧引入薪資工作流程

- 人工智慧、雲端運算和網路安全領域對稀缺人才的競爭日益激烈。

- 從企業電子表格過渡到符合審計要求的薪資體系

- 去中心化技術團隊對多邊獎勵管治的需求日益成長

- 由於年度薪資調查數據很快就會過時,因此需要對需求進行即時基準測試。

- 市場限制因素

- 受預算限制而做出的薪資決定正在減緩套房的擴張速度。

- 整合人力資源資訊系統、薪資系統、股權系統和財務系統的複雜性。

- 由於技能溢價降低,技術崗位的薪資審查變得越來越頻繁。

- 關於工資來源的錯誤訊息以及地區間工資水準的摩擦削弱了人們對正規工資制度的信心。

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 基於雲端的

- 現場

- 混合

- 按公司規模

- 大公司

- 小型企業

- 功能性別

- 薪酬計劃

- 基本薪資管理

- 獎勵薪酬管理

- 股票期權激勵管理

- 糾正薪資差距和管理透明度

- 薪酬分析與報告

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Payscale, Inc.

- Salary.com, LLC

- beqom SA

- Xactly Corporation

- CaptivateIQ, Inc.

- Varicent US Opco Corporation

- PerformanceCentre, Inc.

- HRSoft, Inc.

- Trove Information Technologies, Inc. dba Pave

- Compa Technologies, Inc.

- Syndio Solutions, Inc.

- Trusaic, Inc.

- Sysarb AB

- Aeqium, Inc.

- OpenComp, Inc.

- Everstage Inc.

- CellarStone, Inc.

- PayAnalytics hf.

- BullseyeEngagement LLC

- Iconixx Software Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the compensation management in technology sector market is projected to be USD 0.71 billion in 2025, USD 1.72 billion in 2026, and reach USD 3.21 billion by 2031, growing at a CAGR of 13.29% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Functionality (Compensation Planning, Base Pay Management, Incentive Compensation Management, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Compensation Management In Technology Sector Market Trends and Insights

Pay Transparency and Pay Equity Compliance Deadlines

The compensation management market in the technology sector is receiving a strong push from compliance deadlines, turning compensation software into a core control system rather than an optional HR tool. The June 7, 2026, deadline under the EU Pay Transparency Directive has forced technology employers to prepare pay-range disclosures, document pay decisions, and review internal pay gaps with much greater discipline. In the United States, pay transparency rules have also expanded across states, and employers posting remote roles must often align a single job opening with multiple disclosure obligations. Illinois has added similar expectations around salary transparency, increasing the pressure on employers that hire across multiple jurisdictions simultaneously. This is making jurisdiction-aware compensation platforms more valuable for compensation management in technology sector market, as they can maintain policy logic, approval history, and posting controls in a single system. The next wave of reporting obligations for employers with larger workforces is likely to keep compliance-led buying active well beyond the first round of disclosure preparation.

Cloud and AI Adoption In Compensation Workflows

Compensation management in technology sector industry is also being shaped by the shift from annual compensation cycles to continuous decision support. In 2026, 81% of incentive compensation teams reported using AI in some capacity, and extensive users showed a 67% preparedness rate for market shifts, much higher than lighter users. One platform highlighted its AI Pay and Compensation Agent, which leverages real-time market data from over 700 enterprises and a large skills graph to support pay recommendations, achieving a 94% offer acceptance rate and a 23% reduction in time-to-offer. Another vendor added generative AI capabilities for pay equity analysis, budget scenario modeling, and real-time compensation simulation inside a SOC 2 Type II-compliant environment, showing how providers are embedding AI into enterprise control frameworks. In the compensation management market for the technology sector, these launches matter because buyers now expect systems to dynamically guide pay decisions as conditions change, not just summarize results after the cycle closes. Vendors that keep AI tied to auditability, governance, and secure deployment are likely to gain more trust than those positioning AI as a stand-alone feature.

Budget-Constrained Pay Decisions Delay Suite Expansion

The compensation management market in the technology sector still faces slower buying cycles as technology employers move into tighter budget-control periods. Many companies protect the core planning module first and delay spending on analytics, transparency, or equity extensions until headcount and hiring plans become clearer. This is especially visible among smaller technology firms that understand the governance need but cannot always defend a broader platform rollout during periods of hiring caution. The spending pattern does not usually remove compensation software from the roadmap, but it does stretch deployment into phases and reduce short-term module expansion. In the compensation management in technology sector market, this favors vendors with bundled pricing and a wider product footprint, as buyers often prefer to deepen an existing relationship rather than add several point tools. That dynamic supports large platforms while making it harder for smaller vendors that cover only one narrow compensation use case.

Other drivers and restraints analyzed in the detailed report include:

- Competition for Scarce AI, Cloud, And Cybersecurity Talent

- Enterprise Shift from Spreadsheets to Audit-Ready Compensation Systems

- Integration Complexity Across HRIS, Payroll, Equity, And Finance Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 71.12% of the compensation management in the technology sector market in 2025, while services are projected to expand at a 15.23% CAGR through 2031. That split shows that software subscriptions remain the revenue base, but it also shows that buyers increasingly need support beyond the platform itself. In the compensation management market in the technology sector, demand for services is rising because multi-country compensation design, workflow setup, data migration, and policy alignment are difficult to execute with internal teams alone. The need for services also reflects the fact that compensation changes within technology firms often affect HR, finance, managers, recruiters, and legal teams simultaneously.

The compensation management in the technology sector is therefore moving toward a model in which software and services reinforce each other rather than compete for budget. Organizations with clean, connected compensation data tend to make faster decisions and adjust to labor shifts with less disruption, which increases the perceived value of implementation and advisory support. That outcome gap matters because many technology employers are not buying a tool alone; they are buying an operating model for compensation governance. Service demand is also supported by the growing use of security and compliance commitments in enterprise contracts, which pushes vendors and implementation partners to stay involved after the initial rollout.

Cloud-based deployment commanded 68.45% share in 2025, while hybrid deployment is forecast to grow at a 14.89% CAGR through 2031. The leading cloud position reflects the strong preference for managed infrastructure, easier updates, and smoother integration with modern HR systems. Even so, compensation management in the technology sector is not moving in a straight line from on-premises to the cloud, because many large employers still operate systems they cannot quickly replace. Hybrid models are gaining traction where employers want cloud analytics and workflow flexibility but still need local control for sensitive records, data residency requirements, or older enterprise architecture.

The compensation management market in the technology sector is seeing hybrid adoption rise because compensation data rarely resides in a single place. A large employer may use a cloud HRIS, on-premises finance tools, separate equity administration, and regional payroll systems, making a blended compensation layer more practical than a full replacement. The 2026 launch of Compose Insights and Predictive Compensation in a secure, SOC 2 Type II-compliant environment demonstrated that vendors are designing products that meet stricter enterprise governance expectations rather than assuming every buyer wants a simple cloud-only setup. As a result, hybrid growth is not a temporary transition in compensation management in technology sector market; it reflects a durable need to support mixed estates across global technology organizations.

Geography Analysis

North America accounted for 41.05% of the global compensation management in the technology sector market in 2025. The region leads because the United States combines a large technology employer base with active pay disclosure rules that keep compensation governance high on the agenda. Colorado's enforcement record, including citation fines issued under the Equal Pay for Equal Work Act, shows that compliance risk is real rather than theoretical. COLORADO CDLE. Canada adds another layer of reporting expectations for cross-border employers, while Mexico is being influenced by compensation governance standards set by U.S. and European parent companies.

Europe was the second-largest regional market in 2025, with Germany, the United Kingdom, and France acting as the main demand centers. The compensation management market in the technology sector is receiving a structural boost in Europe because the EU Pay Transparency Directive has forced employers to prepare for a more formal, documented compensation process. National differences within Europe are also increasing the workload, as employers must adapt their regional compensation strategy to local disclosure, documentation, and employee consultation rules. Germany already had an established pay transparency framework, so many employers there are focused on upgrading existing systems rather than starting from scratch. Across South America, Brazil and Argentina remain the most active markets because multinational technology employers often apply North American and European compensation standards to their operations before local regulations fully require it.

Asia-Pacific is the fastest-growing region, and the compensation management market size in the technology sector is forecast to grow at a 16.73% CAGR through 2031. India, South Korea, and Southeast Asia are driving much of that momentum because technology hiring is expanding and distributed engineering models need stronger pay governance. China remains important, but local data controls and deployment preferences make hybrid or locally adapted models more relevant than simple cloud-only offerings. In the Middle East and Africa, adoption is earlier in the cycle, yet the United Arab Emirates, Saudi Arabia, South Africa, and Nigeria are drawing steady interest as regional technology operations grow under multinational compensation standards.

- Payscale, Inc.

- Salary.com, LLC

- beqom SA

- Xactly Corporation

- CaptivateIQ, Inc.

- Varicent US Opco Corporation

- PerformanceCentre, Inc.

- HRSoft, Inc.

- Trove Information Technologies, Inc. dba Pave

- Compa Technologies, Inc.

- Syndio Solutions, Inc.

- Trusaic, Inc.

- Sysarb AB

- Aeqium, Inc.

- OpenComp, Inc.

- Everstage Inc.

- CellarStone, Inc.

- PayAnalytics hf.

- BullseyeEngagement LLC

- Iconixx Software Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pay Transparency and Pay Equity Compliance Deadlines

- 4.2.2 Cloud and AI Adoption in Compensation Workflows

- 4.2.3 Competition for Scarce AI, Cloud, and Cybersecurity Talent

- 4.2.4 Enterprise Shift from Spreadsheets to Audit-Ready Compensation Systems

- 4.2.5 Growing Need for Multi-Country Compensation Governance in Distributed Tech Teams

- 4.2.6 Real-Time Benchmarking Demand as Annual Salary Surveys Age Too Quickly

- 4.3 Market Restraints

- 4.3.1 Budget-Constrained Pay Decisions Delay Suite Expansion

- 4.3.2 Integration Complexity Across HRIS, Payroll, Equity, and Finance Systems

- 4.3.3 Skill Premium Compression Forces Frequent Repricing of Tech Roles

- 4.3.4 Salary-Source Misinformation and Location-Pay Friction Undermine Trust in Formal Pay Programs

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Functionality

- 5.4.1 Compensation Planning

- 5.4.2 Base Pay Management

- 5.4.3 Incentive Compensation Management

- 5.4.4 Equity Compensation Management

- 5.4.5 Pay Equity and Transparency Management

- 5.4.6 Compensation Analytics and Reporting

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Payscale, Inc.

- 6.4.2 Salary.com, LLC

- 6.4.3 beqom SA

- 6.4.4 Xactly Corporation

- 6.4.5 CaptivateIQ, Inc.

- 6.4.6 Varicent US Opco Corporation

- 6.4.7 PerformanceCentre, Inc.

- 6.4.8 HRSoft, Inc.

- 6.4.9 Trove Information Technologies, Inc. dba Pave

- 6.4.10 Compa Technologies, Inc.

- 6.4.11 Syndio Solutions, Inc.

- 6.4.12 Trusaic, Inc.

- 6.4.13 Sysarb AB

- 6.4.14 Aeqium, Inc.

- 6.4.15 OpenComp, Inc.

- 6.4.16 Everstage Inc.

- 6.4.17 CellarStone, Inc.

- 6.4.18 PayAnalytics hf.

- 6.4.19 BullseyeEngagement LLC

- 6.4.20 Iconixx Software Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

人力資本管理市場:按組件、授權模式、組織規模、部署和產業分類-2026-2032年全球市場預測

人力資本管理市場:按組件、授權模式、組織規模、部署和產業分類-2026-2032年全球市場預測 AI原生HCM平台:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)可組合式 HCM 平台:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)銀行、金融服務和保險 (BFSI) 行業的薪酬管理:市場佔有率分析、行業趨勢與統計數據、成長預測 (2026-2031)人力資本管理(HCM)企業資源規劃:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031)

AI原生HCM平台:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)可組合式 HCM 平台:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)銀行、金融服務和保險 (BFSI) 行業的薪酬管理:市場佔有率分析、行業趨勢與統計數據、成長預測 (2026-2031)人力資本管理(HCM)企業資源規劃:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031) 薪資和薪酬管理平台市場預測至2034年-按薪資處理階段、薪酬類型、平台功能、部署模式和最終用戶分類的全球分析雲端HCM平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

薪資和薪酬管理平台市場預測至2034年-按薪資處理階段、薪酬類型、平台功能、部署模式和最終用戶分類的全球分析雲端HCM平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 人力資本管理市場規模、佔有率和成長分析:按交付類型、部署類型、最終用戶產業、組織規模和地區分類-2026-2033年產業預測

人力資本管理市場規模、佔有率和成長分析:按交付類型、部署類型、最終用戶產業、組織規模和地區分類-2026-2033年產業預測 人力資本管理市場規模、佔有率、趨勢和預測:按組件、部署類型、行業和地區分類,2026-2034 年

人力資本管理市場規模、佔有率、趨勢和預測:按組件、部署類型、行業和地區分類,2026-2034 年 2026年全球人力資本管理市場報告

2026年全球人力資本管理市場報告