|

市場調查報告書

商品編碼

2063931

人力資本管理(HCM)企業資源規劃:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031)Human Capital Management (HCM) Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

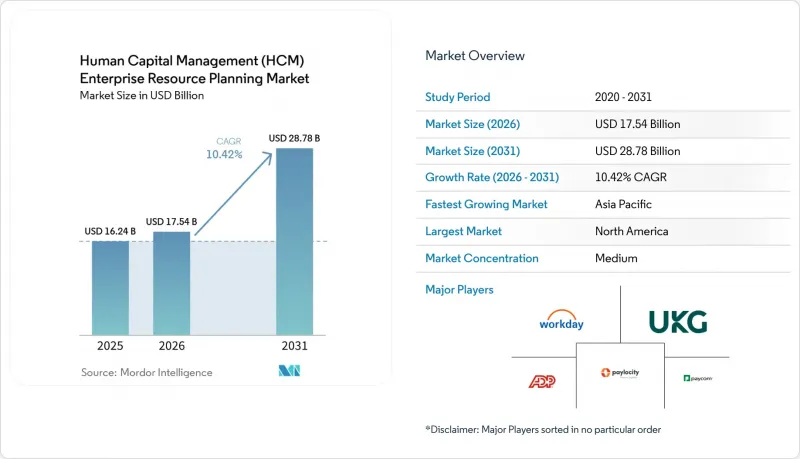

根據 Mordor Intelligence 預測,人力資本管理 (HCM) 企業資源規劃 (ERP) 市場將從 2026 年的 175.4 億美元成長到 2031 年的 287.8 億美元,2026 年至 2031 年的複合年成長率為 10.42%。

本報告按部署模式(雲端、本地部署、混合部署)、組織規模(中小企業、大型企業)、行業(製造業、銀行、金融服務和保險業、醫療保健業、零售和電子商務業、IT和電信業、政府部門及其他)、組件或模組(核心人力資源、人才管理及其他)以及地區進行細分。市場預測以美元計價。

全球人力資本管理 (HCM) 企業資源規劃市場趨勢與洞察

加速向雲端原生人力資源套件的轉型

企業正從本地部署的ERP附加元件遷移到雲端平台,以降低硬體成本並減輕升級負擔。 Oracle報告稱,2025會計年度其HCM雲端客戶將達到兩位數成長,並指出引進週期已從傳統系統的18-24個月縮短至6-9個月。 Workday 2026R1版本整合了AI代理,可解決日常諮詢,使人力資源負責人能夠專注於策略規劃。訂閱式定價將資本投資轉化為可變營運成本,使支出能夠根據人事費用的波動進行調整。 ADP的Lyric整合資料模型降低了整合開銷並縮短了部署時間。然而,與資料清理和工作流程重組相關的挑戰正在減緩高度客製化企業的轉型步伐。

對以分析主導的人才規劃的需求

預測分析有助於雇主預測技能缺口、最佳化人事費用預算並識別員工流失風險。 Workday 使用者利用人工智慧驅動的模型,將護理人員留任率提高了 50%。美國勞工統計局預測,到 2031 年,註冊護理師將出現 190 萬的缺口,這推動了對留任分析的需求。製造商正在利用技能智慧對員工進行機器人和積層製造等領域的再培訓,從而降低外部招募成本。 Oracle 的動態技能解決方案透過識別內部候選人,將招募時間縮短了約 30%。監管機構正在審查演算法偏見,美國聯邦就業機會委員會 (EEOC) 也發布了關於可解釋性的指導意見。

由於遺留ERP系統,遷移成本高昂

資料遷移可能需要 6 到 12 個月,並且可能需要支付高昂的諮詢費,費用可能高達年度訂閱費的 15% 到 20%。企業必須累計已支付的許可費計入損失,解決重複訂閱費問題,並重新培訓用戶,這些都會阻礙短期遷移。在製造業和醫療保健產業,處理工會的工作安排會增加系統重建的難度,並延長投資回收期。

細分市場分析

至2025年,雲端採用將佔人力資本管理(HCM)ERP市場62.13%的佔有率,預計到2031年將以15.12%的複合年成長率成長。純雲端訂單佔Workday新契約的85%,反映客戶對持續功能交付的偏好。政府和國防機構仍然堅持混合策略,將薪資核算引擎保留在本地以滿足安全要求。然而,維護雙堆疊解決方案會削弱成本節約,因此供應商正在逐步淘汰舊版本。

在人力資本管理 (HCM) ERP 市場,採用按用戶收費系統的平台越來越受到青睞,這種模式允許企業根據經濟週期靈活調整支出。 Oracle HCM Cloud 25A 凸顯了創新差距,它比本地部署客戶提前數月向用戶提供了 AI 薪資匹配功能。儘管資料居住的法規可能會延緩歐洲和亞太地區的全端部署,但許多跨國公司更傾向於區域本地化而非混合架構。

到2025年,大型企業將佔總收入的57.23%,它們需要符合審計要求的控制措施、多休閒薪資核算系統以及高級整合功能,以提高平均合約價值。它們也在與採購相關的學習和分析解決方案,這進一步拉大了它們與中小企業在人力資本管理ERP市場的佔有率差距。同時,由於中小企業可以透過簡化入職流程來降低IT成本,因此它們的複合年成長率(CAGR)高達13.72%。

Gusto、BambooHR 和 HiBob 提供的訂閱方案可在 90 天內完成系統運作。 Workday 於 2024 年發布了其中型企業版,進軍 500-2500 名員工規模的企業市場。雖然中小企業優先考慮行動應用、嵌入式支付和便利的合規性,但由於許多企業最初忽略了繼任計畫和學習功能,因此仍有成長空間。供應商之所以關注這一細分市場,是因為其客戶解約率率低,提升銷售潛力大,從而提升了整個人力資本管理 (HCM) ERP 市場的客戶終身價值 (LTV)。

區域分析

受嚴格的多州薪資核算法規和早期採用雲端運算的推動,北美地區在2025年佔總收入的34.97%。美國國稅局降低了W-2表格電子申報的閾值,加速了中型企業的轉型。隨著大多數公司完成轉型的第一階段,並傾向於購買人工智慧附加元件而非全套解決方案,成長速度正在放緩。

亞太地區預計將成為成長最快的地區,預測期內複合年成長率將達到13.94%。由於商品及服務稅(GST)和社會保障體系改革,薪資管理日益複雜,因此採用針對特定國家的薪資核算引擎至關重要。澳洲和紐西蘭的雲端採用率很高,而印尼和越南由於基礎設施挑戰依然存在,進展較為緩慢。

歐洲的發展趨勢以合規為主導。這是因為《一般資料保護規則》(GDPR) 強制要求在本地進行資料處理,而《臨時工指令》則要求重新計算工資。供應商在德國、荷蘭和愛爾蘭營運區域資料中心。東歐也從中受益,波蘭和羅馬尼亞的共享服務中心不斷擴張。中東地區在「沙烏地阿拉伯2030願景」的勞動改革下蓬勃發展,但除南非和埃及外,非洲仍處於發展階段。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速向雲端原生人力資源套件的轉型

- 基於分析的勞動力規劃需求

- 跨國公司薪資核算合規性的複雜性

- 遠距和混合辦公室模式的興起

- 人工智慧驅動的人才招聘和留任工具

- 人力資本管理與物聯網賦能的工人安全系統的整合

- 市場限制因素

- 由於遺留ERP系統,遷移成本高昂

- 對資料隱私和主權的擔憂

- 人力資源和資訊技術負責人缺乏執行技能

- 中型企業對供應商鎖定問題的擔憂

- 產業價值鏈分析

- 監理情勢

- 宏觀經濟因素對市場的影響

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 小型企業

- 大公司

- 按行業

- 製造業

- BFSI

- 醫療保健

- 零售與電子商務

- 資訊科技/通訊

- 政府機構

- 其他

- 按組件或模組

- 核心人力資源

- 薪資核算

- 人才管理

- 人力資源管理

- 學習與發展

- 其他模組

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Workday Inc.

- Ultimate Kronos Group, Inc.

- Ceridian HCM Holding Inc.

- Automatic Data Processing, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Cornerstone OnDemand, Inc.

- Bamboo HR LLC

- Namely Inc.

- Zoho Corporation Pvt. Ltd.

- Ramco Systems Limited

- PeopleStrategy, Inc.

- Gusto, Inc.

- TriNet Zenefits LLC

- HiBob Ltd.

- The Sage Group plc

- Epicor Software Corporation

- Unit4 NV

- Infor (US), Inc.

- Softworks Workforce Management Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the human capital management (HCM) enterprise resource planning (ERP) market size is projected to expand from USD 17.54 billion in 2026 to USD 28.78 billion by 2031, registering a CAGR of 10.42% over 2026-2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Organization Size (Small and Medium Enterprises, and Large Enterprises), Industry Vertical (Manufacturing, BFSI, Healthcare, Retail and E-Commerce, IT and Telecom, Government, and More), Component or Module (Core HR, Talent Management, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Human Capital Management (HCM) Enterprise Resource Planning Market Trends and Insights

Accelerated Transition to Cloud-Native HR Suites

Organizations are migrating from on-premise ERP add-ons to cloud platforms that cut hardware expense and reduce upgrade pain. Oracle reported double-digit HCM Cloud customer growth in fiscal 2025, citing deployment cycles of 6-9 months compared with 18-24 months on legacy stacks. Workday's 2026R1 embedded AI agents that resolve routine queries, freeing HR staff for strategic planning. Subscription pricing converts capital outlays into variable operating costs, aligning spend with headcount volatility. ADP's Lyric unified data model reduces integration overhead and shortens implementation time. Still, data-cleansing challenges and workflow re-engineering slow heavily customized enterprises.

Demand for Analytics-Driven Workforce Planning

Predictive analytics help employers anticipate skills gaps, optimize labor budgets, and flag attrition risk. Workday users achieved 50% better nurse retention via AI-driven models. The U.S. Bureau of Labor Statistics projects a shortfall of 1.9 million registered nurses by 2031, intensifying demand for retention analytics. Manufacturers deploy skills intelligence to retrain workers on robotics and additive manufacturing, lowering external hiring costs. Oracle's Dynamic Skills surfaces internal candidates, cutting time-to-fill by about 30%. Regulators are watching algorithmic bias, and the EEOC has issued guidance on explainability.

High Switching Costs From Legacy ERP

Data migration can last 6-12 months and require costly consultants, reaching 15-20% of annual subscription fees. Enterprises must write off sunk licenses, pay overlapping subscriptions, and retrain users, deterring near-term moves. Customized union scheduling in manufacturing and healthcare raises re-engineering hurdles, stretching payback periods.

Other drivers and restraints analyzed in the detailed report include:

- Compliance Complexity in Multi-Country Payroll

- Rise of Remote and Hybrid Work Models

- Data Privacy and Sovereignty Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments accounted for 62.13% of the human capital management ERP market in 2025 and are expected to grow at a 15.12% CAGR through 2031. Pure cloud bookings represented 85% of Workday's new deals, reflecting customer preference for continuous feature delivery. Hybrid strategies persist for governments and defense agencies that keep payroll engines on-premise to satisfy security mandates. However, maintaining dual stacks undercuts savings, and vendors are phasing out legacy versions.

The human capital management ERP market increasingly rewards platforms that align fees with active headcount, allowing firms to flex spend during cycles. Oracle HCM Cloud 25A pushed AI payroll reconciliation to subscribers months ahead of on-premise clients, underscoring the innovation gap. Data-residency rules may slow full-stack adoption in Europe and Asia-Pacific, but most multinationals prefer localized regions over hybrid builds.

Large enterprises contributed 57.23% revenue in 2025 and require audit-ready controls, multi-ledger payroll, and deep integrations that lift average contract values. They also buy adjacent learning and analytics, widening the human capital management ERP market share gap versus smaller firms. Yet small and medium enterprises post the faster 13.72% CAGR as simplified onboarding trims IT overhead.

Gusto, BambooHR, and HiBob offer flat-rate bundles that complete go-lives in under 90 days. Workday launched a mid-market edition in 2024, entering the 500-2,500 employee band. SMEs value mobile apps, embedded payments, and hands-off compliance, though many skip succession and learning at first pass, leaving expansion potential. Vendors court this segment because low churn and upsell headroom lift lifetime value across the human capital management ERP market.

Geography Analysis

North America contributed 34.97% of 2025 revenue, driven by strict multi-state payroll laws and early cloud adoption. The IRS cut the W-2 e-file threshold, accelerating migration among mid-sized employers. Growth is plateauing as most enterprises finish first-wave migrations and now purchase AI add-ons rather than full suites.

Asia-Pacific is projected to be the fastest-growing region, with a compound annual growth rate (CAGR) of 13.94% during the forecast period. The implementation of in-country payroll engines has become crucial as Goods and Services Tax (GST) and social insurance reforms introduce additional layers of complexity into payroll management. Australia and New Zealand demonstrate high levels of cloud adoption, whereas Indonesia and Vietnam are experiencing slower progress due to persistent infrastructure challenges.

Europe's trajectory is compliance-driven, as the GDPR requires local data processing and the Posted Workers Directive requires payroll recalculations. Vendors run regional data centers in Germany, the Netherlands, and Ireland. Eastern Europe benefits as shared-services hubs grow in Poland and Romania. The Middle East is expanding under Saudi Vision 2030 workforce reforms, whereas Africa remains nascent outside South Africa and Egypt.

- Workday Inc.

- Ultimate Kronos Group, Inc.

- Ceridian HCM Holding Inc.

- Automatic Data Processing, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Cornerstone OnDemand, Inc.

- Bamboo HR LLC

- Namely Inc.

- Zoho Corporation Pvt. Ltd.

- Ramco Systems Limited

- PeopleStrategy, Inc.

- Gusto, Inc.

- TriNet Zenefits LLC

- HiBob Ltd.

- The Sage Group plc

- Epicor Software Corporation

- Unit4 N.V.

- Infor (US), Inc.

- Softworks Workforce Management Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Transition to Cloud-Native HR Suites

- 4.2.2 Demand for Analytics-Driven Workforce Planning

- 4.2.3 Compliance Complexity in Multi-Country Payroll

- 4.2.4 Rise of Remote and Hybrid Work Models

- 4.2.5 AI-Powered Talent Acquisition and Retention Tools

- 4.2.6 Integration of HCM with IoT-Enabled Workforce Safety Systems

- 4.3 Market Restraints

- 4.3.1 High Switching Costs from Legacy ERP

- 4.3.2 Data Privacy and Sovereignty Concerns

- 4.3.3 Implementation Skill Shortage Among HR-IT Staff

- 4.3.4 Vendor Lock-In Fear in Mid-Market Enterprises

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Industry Vertical

- 5.3.1 Manufacturing

- 5.3.2 BFSI

- 5.3.3 Healthcare

- 5.3.4 Retail and E-commerce

- 5.3.5 IT and Telecom

- 5.3.6 Government

- 5.3.7 Other Industry Verticals

- 5.4 By Component

- 5.4.1 Core HR

- 5.4.2 Payroll

- 5.4.3 Talent Management

- 5.4.4 Workforce Management

- 5.4.5 Learning and Development

- 5.4.6 Other Modules

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday Inc.

- 6.4.2 Ultimate Kronos Group, Inc.

- 6.4.3 Ceridian HCM Holding Inc.

- 6.4.4 Automatic Data Processing, Inc.

- 6.4.5 Paycom Software, Inc.

- 6.4.6 Paylocity Holding Corporation

- 6.4.7 Cornerstone OnDemand, Inc.

- 6.4.8 Bamboo HR LLC

- 6.4.9 Namely Inc.

- 6.4.10 Zoho Corporation Pvt. Ltd.

- 6.4.11 Ramco Systems Limited

- 6.4.12 PeopleStrategy, Inc.

- 6.4.13 Gusto, Inc.

- 6.4.14 TriNet Zenefits LLC

- 6.4.15 HiBob Ltd.

- 6.4.16 The Sage Group plc

- 6.4.17 Epicor Software Corporation

- 6.4.18 Unit4 N.V.

- 6.4.19 Infor (US), Inc.

- 6.4.20 Softworks Workforce Management Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

人力資本管理市場:按組件、授權模式、組織規模、部署和產業分類-2026-2032年全球市場預測

人力資本管理市場:按組件、授權模式、組織規模、部署和產業分類-2026-2032年全球市場預測 AI原生HCM平台:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)可組合式 HCM 平台:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)科技業薪酬管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)銀行、金融服務和保險 (BFSI) 行業的薪酬管理:市場佔有率分析、行業趨勢與統計數據、成長預測 (2026-2031)

AI原生HCM平台:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)可組合式 HCM 平台:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)科技業薪酬管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)銀行、金融服務和保險 (BFSI) 行業的薪酬管理:市場佔有率分析、行業趨勢與統計數據、成長預測 (2026-2031) 薪資和薪酬管理平台市場預測至2034年-按薪資處理階段、薪酬類型、平台功能、部署模式和最終用戶分類的全球分析雲端HCM平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

薪資和薪酬管理平台市場預測至2034年-按薪資處理階段、薪酬類型、平台功能、部署模式和最終用戶分類的全球分析雲端HCM平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 人力資本管理市場規模、佔有率和成長分析:按交付類型、部署類型、最終用戶產業、組織規模和地區分類-2026-2033年產業預測

人力資本管理市場規模、佔有率和成長分析:按交付類型、部署類型、最終用戶產業、組織規模和地區分類-2026-2033年產業預測 人力資本管理市場規模、佔有率、趨勢和預測:按組件、部署類型、行業和地區分類,2026-2034 年

人力資本管理市場規模、佔有率、趨勢和預測:按組件、部署類型、行業和地區分類,2026-2034 年 2026年全球人力資本管理市場報告

2026年全球人力資本管理市場報告