|

市場調查報告書

商品編碼

2064518

銀行、金融服務和保險 (BFSI) 行業的薪酬管理:市場佔有率分析、行業趨勢與統計數據、成長預測 (2026-2031)Compensation Management In BFSI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

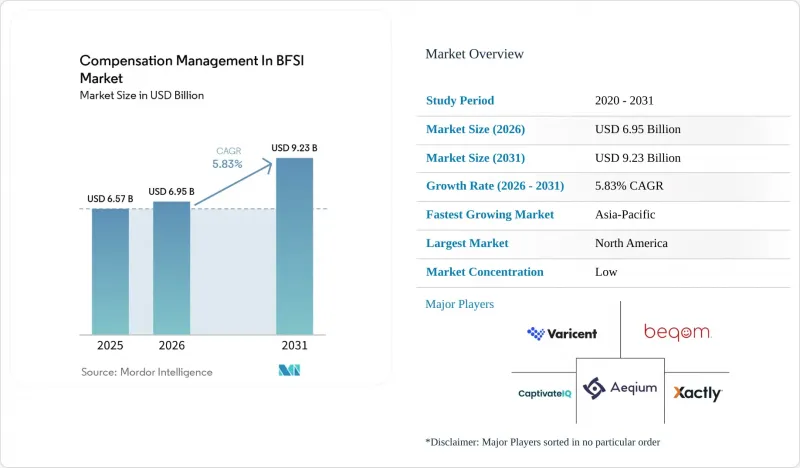

根據 Mordor Intelligence 預測,BFSI(銀行、金融服務和保險)薪酬管理市場規模預計在 2025 年達到 65.7 億美元,在 2026 年達到 69.5 億美元,在 2031 年達到 92.3 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 5.83%。

本報告按組件(軟體、服務)、薪酬職能(薪酬規劃、預算等)、部署方式(雲端、本地部署、混合部署)、組織規模(大型企業、中小企業)、最終用戶行業(銀行、保險等)和地區進行細分。市場預測以美元計價。

全球銀行、金融服務與保險(BFSI)薪酬管理市場趨勢與分析

將雲端運算和人工智慧 (AI) 引入薪酬運營

銀行、金融服務和保險 (BFSI) 行業的薪酬管理正從單純的記錄工具演變為支援即時場景建模、工作流程自動化和更強力的審計證據的平台。人工智慧平台正在幫助銀行和保險公司縮短以往依賴數週電子表格匯總的審核週期,轉而採用更快、更可控的工作流程。這種轉變有利於雲端交付,因為供應商可以在客戶環境中部署模型更新、合規性檢查和決策支援功能,而無需像本地部署那樣經歷漫長的升級週期,從而避免了速度減慢的問題。此外,在法規環境下,對與僱用相關的人工智慧工具日益嚴格的審查凸顯了可解釋性、偏差監控和人工監督的重要性。實際上,這使得那些已經提供管治的人工智慧層的供應商比那些試圖基於零散的薪酬數據構建臨時工具的金融機構更具優勢。

受監管員工複雜的浮動薪酬管理需求

銀行、金融服務和保險(BFSI)行業對薪酬管理的需求持續成長,原因很簡單:銀行和保險業的浮動薪酬管理難度遠高於其他許多行業。金融機構通常需要在多個司法管轄區同時管理短期獎勵、遞延薪資、結算條款、多幣種獎金池和長期績效評估系統。 2026年5月的一項針對金融服務業薪酬經理的調查發現,86%的受訪者認為薪酬體繫管理十分複雜,80%的受訪者表示過去三年參與獎勵計劃的積極性有所提高。隨著獎勵的覆蓋範圍從高階主管擴展到更廣泛的員工群體,人工管理在不增加錯誤率和削弱預算控制的情況下難以有效擴展。因此,BFSI行業對能夠透過方案建模、自動化計算和特定司法管轄區管理來應對日益複雜的薪酬體系,同時又不相應增加營運風險的薪酬管理方案的需求持續成長。

舊有系統整合和資料碎片化

銀行、金融服務和保險(BFSI)產業的薪酬管理仍面臨最持久的營運限制因素,即舊有系統整合和資料環境碎片化。 2026 年 5 月的一項調查發現,66% 的金融服務薪資負責人認為,多個服務供應商的存在是確保薪資資料準確性和一致性的障礙;64% 的負責人需要在多個法規環境下營運;77% 的負責人依賴跨司法管轄區的多個外包合作夥伴。這種分散化限制了現代薪酬管理軟體的價值,因為預測、分析和情境規劃的可靠性取決於其背後上游財務、人力資源和薪酬資料饋送的可靠性。 Zalaris 的研究表明,即使是丹麥銀行(Danske Bank)有限的薪資核算現代化工作,也需要分階段在全國範圍內部署,並進行大規模的變更管理,才能整合供應商並在整個北歐地區的運營中實現流程標準化。此外,beqom 對全球一級銀行的案例研究也凸顯了這個問題的嚴重性,該研究指出,為了進行真正有價值的分析,需要將 50 多個薪酬組成部分在自訂系統和 Excel 文件中進行匹配。

細分市場分析

預計到2025年,軟體收入將佔總收入的63.12%,BFSI(銀行、金融服務和保險)行業的薪酬管理將繼續圍繞可配置平台展開,該平台能夠適應規則變更而無需完全重新開發。這一趨勢反映了買家傾向於選擇能夠適應英國薪酬改革、歐盟薪資透明度要求以及不斷變化的獎勵計劃結構的系統,同時減少對內部IT重組的依賴。在軟體領域,監管機構和內部負責人對兼具計算精度、分析能力、工作流程管理以及清晰審計追蹤功能的工具的需求日益成長。這種轉變使得中型銀行和保險公司在需要更複雜的激勵和遞延薪酬功能時,更願意重新考慮獎勵人力資源套件。以軟體為中心的結構也反映出BFSI產業的薪資管理高度依賴跨司法管轄區的可設定規則引擎,而不是硬編碼到特定的區域薪資流程中。

服務是成長最快的領域,預計到2031年將維持8.06%的複合年成長率。這是因為許多金融機構在軟體能夠如預期運作之前,仍需要實施、整合和諮詢支援。當薪酬平台必須連接到核心銀行系統、人力資源主資料、薪資核算引擎、客戶關係管理工具和財務帳簿(這些系統並非基於通用薪資資料模型設計)時,對服務的需求就會增加。因此,諮詢、系統映射和分階段實施的成本可能會超過軟體授權本身的成本,尤其對於大型受監管的金融機構而言更是如此。這也意味著,銀行、金融服務和保險(BFSI)薪酬管理領域的業務收益相對穩定,因為客戶傾向於選擇那些已經了解其控制環境和歷史薪酬架構的供應商。在一個平台數量減少、功能深度增強的市場中,對這些服務的依賴成為提高合約續約率和維持供應商競爭力的重要因素。

到2025年,獎勵薪酬管理將佔據最大的功能佔有率,達到31.45%,這意味著銀行、金融服務和保險(BFSI)行業的薪酬管理仍將主要圍繞浮動薪酬管理。這反映了獎勵設計在銀行、保險、諮詢和交易等行業中的重要性,因為在這些行業中,任何錯誤或延遲支付都可能對收入和員工留任產生直接影響。在價值鏈的保險領域也出現了類似的趨勢,產業領導者仍然認為獎勵薪酬是保險公司營運面臨的重大挑戰。因此,專用的激勵性薪酬管理(ICM)工具仍然至關重要,因為它們比通用的人力資源模組更有效地管理複雜的公式、爭議、異常處理和拆分積分規則。這確保了即使企業不斷增強其規劃和分析能力,ICM 仍然是 BFSI 薪酬管理市場採購決策的核心。

薪酬分析和報告是成長最快的功能,預計到2031年將以6.11%的複合年成長率成長。這是因為合規性現在依賴合理的表格、差異追蹤以及跨多個規則集的及時證據。薪酬透明度、同工同酬審查以及對關鍵風險承擔者的管治都依賴於能夠解釋結果(而不僅僅是計算結果)的資料結構。這促使人們在共用資料模型中採用更緊密整合的方法,用於規劃、獎金管理、報告和薪資差距監控。基於機器學習的異常檢測也開始影響產品藍圖,因為買家希望在最終決策之前(而不是在報告發布之後)指出薪酬異常情況。隨著時間的推移,這意味著分析將擴大扮演控制層的角色,滲透到更廣泛的基於銀行、金融服務和保險(BFSI)行業的薪酬管理中,而不是作為一個獨立的模組。

區域分析

到2025年,北美將佔據37.66%的市場佔有率,成為銀行、金融服務和保險(BFSI)薪酬管理市場最大的市場。該地區受益於大型金融機構的集中、聯邦和州政府的廣泛監管,以及成熟的獎勵薪酬供應商基礎和豐富的薪酬管治工具。美國仍然是主要的需求中心,因為銀行、保險公司和資本市場公司在獎勵管治、經營團隊課責和薪酬資料管理方面面臨多層次的期望。此外,隨著金融機構競相在人工智慧、網路安全和定量分析領域招攬人才,基於技能的薪酬模型對於滿足那些無法完全融入傳統薪酬系統的人才需求也日益成長。雖然加拿大和墨西哥的市佔率仍然較小,但隨著金融機構擴大其數位化人力資源和薪資流程,這兩個國家仍在持續推動現代化需求。

歐洲是英國的薪酬改革以及其他國家法規(例如德國的IVV 5.0)迫使銀行和保險公司同時重新思考其職位架構、報告邏輯和浮動薪酬管治。德國的情況尤其突出,2026年5月的行業討論重點是BRUBEG和IVV 5.0的實施、薪酬透明化的準備工作以及將ESG關鍵績效指標納入浮動薪酬結構。因此,在歐洲,BFSI薪酬管理的格局並非由單一的採購模式決定,而是由各國的具體合規設計所驅動。南美洲仍處於起步階段,其中巴西扮演主導角色。在巴西,隨著零售銷售網路的擴張和新同工同酬報告要求的訂定,銀行在採用基於雲端的獎勵工具方面持謹慎態度。

亞太地區是成長最快的地區,預計到2031年將以6.49%的複合年成長率成長,並將繼續在銀行、金融服務和保險(BFSI)機構薪酬管理的下一階段發揮核心作用。亞太地區的需求反映了當地薪酬管治和浮動薪酬結構日益複雜,以及中國、印度、澳洲和日本等國積極推動人力資源技術現代化。該地區的金融機構正轉向能夠支援多營業單位報告、區域規則集以及與薪資和績效數據廣泛整合的系統。中東和非洲地區雖然目前的銷售額較小,但隨著海灣國家的銀行將其負責人薪酬管治與全球慣例接軌,以及南非企業積極響應日益成長的薪酬報告要求,這兩個地區的成長勢頭正在增強。這些趨勢共同推動了BFSI機構薪酬管理在區域內的更廣泛應用,儘管北美和歐洲目前仍佔據最大的市場佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 更嚴格的獎勵薪酬管治、追回和遞延規則。

- 歐盟工資透明度與同工同酬合規期限

- 將雲端運算和人工智慧引入薪酬運營

- 需要管理所有受監管員工的複雜浮動薪酬

- 保險和資產配置的現代化

- 針對人工智慧、網路安全、定量分析和監管技術領域的人才,提供基於技能的薪資溢價。

- 市場限制因素

- 舊有系統整合和資料碎片化

- 高度敏感的薪資資料面臨的隱私和網路安全限制

- 不同司法管轄區的賠償規則有差異

- 關於遞延薪酬和等效職位映射的審計負擔

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章:預測市場規模與成長率

- 按組件

- 軟體

- 服務

- 部署和整合服務

- 諮詢和顧問服務

- 支援和維護服務

- 獎勵函數

- 薪資規劃與預算

- 獎勵薪酬管理

- 獎金管理

- 薪酬分析/報告

- 糾正薪資差距和管理透明度

- 其他獎勵功能

- 透過供應方法

- 基於雲端的

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按最終用途行業分類

- 銀行

- 保險

- 資本市場與資產管理

- 信用合作社/住宅金融協會

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- beqom SA

- Xactly Corporation

- Varicent Software Inc.

- PerformanceCentre, Inc.

- CaptivateIQ, Inc.

- Aeqium, Inc.

- HRsoft, Inc.

- Decusoft, Inc.

- PureFacts Financial Solutions

- Akeron Srl

- Fintary Technologies, Inc.

- ComTrack Inc.

- Bentega AS

- Forma AI Inc.

- Iconixx Software Corporation

- Optymyze Pte. Ltd.

- Everstage Inc.

- Commissionly Limited

- CellarStone, Inc.

- Compport Private Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the compensation management in BFSI market size is projected to be USD 6.57 billion in 2025, USD 6.95 billion in 2026, and reach USD 9.23 billion by 2031, growing at a CAGR of 5.83% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Compensation Functionality (Compensation Planning and Budgeting, and More), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-Use Industry (Banking, Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Compensation Management In BFSI Market Trends and Insights

Cloud and Artificial Intelligence Adoption in Compensation Operations

The compensation management in BFSI market is moving away from record-keeping tools and toward platforms that support live scenario modeling, workflow automation, and stronger audit evidence. AI-enabled platforms are helping banks and insurers compress review cycles that once depended on weeks of spreadsheet consolidation into faster, more controlled workflows. This shift favors cloud delivery because vendors can push model updates, compliance checks, and decision-support features across client environments without the long upgrade cycles that often slow on-premises estates. It also underscores the importance of explainability, bias monitoring, and human oversight, as employment-related AI tools now face greater scrutiny in regulated environments. In practice, that gives an edge to vendors that already offer governed AI layers, rather than institutions trying to build ad hoc tools around fragmented compensation data.

Need to Manage Complex Variable Pay across Regulated Workforces

The compensation management in BFSI market continues to draw demand from the simple fact that variable pay in banking and insurance is harder to administer than in most other sectors. Financial institutions often manage short-term incentives, deferred awards, clawback provisions, multi-currency bonus pools, and long-term performance structures across multiple jurisdictions simultaneously. A May 2026 survey of financial services reward leaders found that 86% saw compensation system management as complex and 80% reported broader participation in incentive programs over the prior 3 years. As incentive eligibility expands beyond senior leaders and into larger employee populations, manual administration becomes harder to scale without higher error rates and weaker budget control. That is why the compensation management in BFSI market keeps benefiting from demand for plan modeling, automated calculation, and jurisdiction-aware administration that can absorb rising pay complexity without adding equal levels of operating risk.

Legacy System Integration and Data Fragmentation

The compensation management in BFSI market still faces its most persistent operational restraint in the form of legacy system integration and fragmented data estates. A May 2026 survey found that 66% of financial services compensation leaders saw multiple service providers as a barrier to accurate and consistent pay data, 64% worked across several regulatory environments, and 77% relied on multiple outsourcing partners across jurisdictions. That fragmentation limits the value of modern compensation software because forecasting, analytics, and scenario planning are only as reliable as the upstream finance, HR, and payroll feeds behind them. Zalaris showed how even a focused payroll modernization at Danske Bank required phased country rollouts and heavy change management to consolidate vendors and standardize processes across Nordic operations. A beqom case study on a global tier-1 bank also illustrated the scale of the issue, with more than 50 compensation components needing reconciliation across custom systems and Excel files before analytics could add full value.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Incentive Pay Governance, Clawback, and Deferral Rules

- European Union Pay Transparency and Equal Pay Compliance Deadlines

- Sensitive Pay Data Privacy and Cybersecurity Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 63.12% of revenue in 2025, which kept the compensation management in BFSI market centered on configurable platforms that can absorb rule changes without full redevelopment. This lead reflected buyer preference for systems that can adapt to UK remuneration reform, EU pay transparency obligations, and evolving incentive plan structures, with less reliance on internal IT rebuilds. Within the software layer, demand has shifted toward tools that combine calculation accuracy with analytics, workflow control, and clear audit evidence for regulators and internal reviewers. That shift has made mid-market banks and insurers more willing to reconsider generic HR suites when they need deeper incentive compensation and deferred award functionality. The software-heavy structure also reflects how strongly the compensation management in BFSI market depends on rule engines that can be configured across jurisdictions rather than hard-coded around one local pay process.

Services are the fastest-growing component, with a projected CAGR of 8.06% through 2031, because many institutions still need implementation, integration, and advisory support before software can perform as intended. Services demand rises when compensation platforms must connect to core banking systems, HR master data, payroll engines, CRM tools, and finance ledgers that were never designed around a common pay data model. That makes consulting, system mapping, and phased rollout more expensive to replace than the software license itself, especially at large, regulated institutions. It also means service revenue is relatively durable in the compensation management in BFSI market because clients tend to retain providers that already understand their control environment and historical compensation architecture. In a market moving toward fewer, deeper platforms, that service dependency becomes a practical source of contract stickiness and vendor defense.

Incentive compensation management held the largest functionality share at 31.45% in 2025, which shows how much of the compensation management in BFSI market still revolves around variable pay administration. That position reflects the financial importance of incentive design across banking, insurance, advisory, and trading roles, where errors or payment delays can quickly affect revenue production and employee retention. The insurance side of the value chain reinforces that pattern, since commercial leaders continue to identify incentive compensation as a leading challenge in carrier operations. Dedicated ICM tools, therefore, remain central because they can manage complex formulas, disputes, exceptions, and split-credit rules with more consistency than broad HR modules. That keeps ICM at the core of buying decisions in the compensation management market in BFSI, even as firms also upgrade planning or analytics capabilities.

Compensation analytics and reporting is the fastest-growing functionality, with a CAGR of 6.11% through 2031, because compliance now depends on defensible tables, variance tracking, and timely evidence across several rule sets. Pay transparency, equal pay review, and material risk taker governance all rely on data structures that can explain outcomes, not just calculate them. That is pushing planning, bonus management, reporting, and pay equity monitoring closer together inside shared data models. Machine learning-based anomaly detection is also starting to influence product roadmaps, as buyers want compensation outliers flagged before decisions are finalized, rather than after reports are published. Over time, that makes analytics less of a standalone module and more of a control layer running through the broader compensation management in BFSI market.

Geography Analysis

North America held a 37.66% share in 2025, which gave the region the largest position in the compensation management in BFSI market size. The region benefits from the concentration of large financial institutions, broad federal and state oversight, and a mature vendor base for incentive compensation and broader pay governance tools. The United States remains the main demand center because banks, insurers, and capital markets firms face layered expectations on incentive governance, executive accountability, and pay data control. The region also shows a growing need for skills-based pay modeling as institutions compete for AI, cyber, and quantitative talent that does not cleanly fit within legacy compensation bands. Canada and Mexico remain smaller contributors, but both continue to support modernization demand as financial institutions expand digital HR and compensation processes.

Europe is the most regulation-heavy geography in the compensation management in BFSI market, and that raises both urgency and design complexity. The June 2026 pay transparency transposition deadline, UK remuneration reform, and national overlays such as Germany's IVV 5.0 have forced banks and insurers to review job architecture, reporting logic, and variable pay governance simultaneously. Germany stands out because industry discussion in May 2026 focused heavily on BRUBEG and IVV 5.0 implementation, pay transparency readiness, and ESG KPI integration into variable pay structures. That makes Europe a region where the compensation management in BFSI market share is shaped less by a single buying pattern and more by country-specific compliance design. South America remains at an earlier stage, led by Brazil, where banks have been more selective in adopting cloud-based incentive tools as they expand retail distribution and respond to new equal-pay reporting expectations.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 6.49% through 2031, which keeps it central to the next phase of the compensation management in BFSI market. Demand in APAC reflects aggressive HR technology modernization across China, India, Australia, and Japan, as well as rising complexity in local pay governance and variable reward structures. Institutions in the region are moving toward systems that can support multi-entity reporting, localized rule sets, and broader integration with payroll and performance data. The Middle East and Africa are smaller in current revenue terms, but both regions are showing more momentum as Gulf banks align executive pay governance with global practices and South African firms address widening pay reporting expectations. Together, these trends support a broader geographic spread of adoption even though North America and Europe still hold the largest current weight in the compensation management in BFSI market.

- beqom SA

- Xactly Corporation

- Varicent Software Inc.

- PerformanceCentre, Inc.

- CaptivateIQ, Inc.

- Aeqium, Inc.

- HRsoft, Inc.

- Decusoft, Inc.

- PureFacts Financial Solutions

- Akeron S.r.l.

- Fintary Technologies, Inc.

- ComTrack Inc.

- Bentega AS

- Forma AI Inc.

- Iconixx Software Corporation

- Optymyze Pte. Ltd.

- Everstage Inc.

- Commissionly Limited

- CellarStone, Inc.

- Compport Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening Incentive Pay Governance, Clawback, and Deferral Rules

- 4.2.2 European Union Pay Transparency and Equal Pay Compliance Deadlines

- 4.2.3 Cloud and Artificial Intelligence Adoption in Compensation Operations

- 4.2.4 Need to Manage Complex Variable Pay Across Regulated Workforces

- 4.2.5 Insurance and Wealth Distribution Modernization

- 4.2.6 Skills-Based Pay Premiums for Artificial Intelligence, Cyber, Quant, and Regulatory Technology Talent

- 4.3 Market Restraints

- 4.3.1 Legacy System Integration and Data Fragmentation

- 4.3.2 Sensitive Pay Data Privacy and Cybersecurity Constraints

- 4.3.3 Cross-Jurisdiction Remuneration Rule Divergence

- 4.3.4 Auditability Burden for Deferred Awards and Equal-Value Job Mapping

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration Services

- 5.1.2.2 Consulting and Advisory Services

- 5.1.2.3 Support and Maintenance Services

- 5.2 By Compensation Functionality

- 5.2.1 Compensation Planning and Budgeting

- 5.2.2 Incentive Compensation Management

- 5.2.3 Bonus Management

- 5.2.4 Compensation Analytics and Reporting

- 5.2.5 Pay Equity and Transparency Management

- 5.2.6 Other Compensation Functionalities

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-Sized Enterprises

- 5.5 By End-Use Industry

- 5.5.1 Banking

- 5.5.2 Insurance

- 5.5.3 Capital Markets and Asset Management

- 5.5.4 Credit Unions and Building Societies

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 beqom SA

- 6.4.2 Xactly Corporation

- 6.4.3 Varicent Software Inc.

- 6.4.4 PerformanceCentre, Inc.

- 6.4.5 CaptivateIQ, Inc.

- 6.4.6 Aeqium, Inc.

- 6.4.7 HRsoft, Inc.

- 6.4.8 Decusoft, Inc.

- 6.4.9 PureFacts Financial Solutions

- 6.4.10 Akeron S.r.l.

- 6.4.11 Fintary Technologies, Inc.

- 6.4.12 ComTrack Inc.

- 6.4.13 Bentega AS

- 6.4.14 Forma AI Inc.

- 6.4.15 Iconixx Software Corporation

- 6.4.16 Optymyze Pte. Ltd.

- 6.4.17 Everstage Inc.

- 6.4.18 Commissionly Limited

- 6.4.19 CellarStone, Inc.

- 6.4.20 Compport Private Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

人力資本管理市場:按組件、授權模式、組織規模、部署和產業分類-2026-2032年全球市場預測

人力資本管理市場:按組件、授權模式、組織規模、部署和產業分類-2026-2032年全球市場預測 AI原生HCM平台:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)可組合式 HCM 平台:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)科技業薪酬管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)人力資本管理(HCM)企業資源規劃:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031)

AI原生HCM平台:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)可組合式 HCM 平台:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)科技業薪酬管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)人力資本管理(HCM)企業資源規劃:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031) 薪資和薪酬管理平台市場預測至2034年-按薪資處理階段、薪酬類型、平台功能、部署模式和最終用戶分類的全球分析雲端HCM平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

薪資和薪酬管理平台市場預測至2034年-按薪資處理階段、薪酬類型、平台功能、部署模式和最終用戶分類的全球分析雲端HCM平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 人力資本管理市場規模、佔有率和成長分析:按交付類型、部署類型、最終用戶產業、組織規模和地區分類-2026-2033年產業預測

人力資本管理市場規模、佔有率和成長分析:按交付類型、部署類型、最終用戶產業、組織規模和地區分類-2026-2033年產業預測 人力資本管理市場規模、佔有率、趨勢和預測:按組件、部署類型、行業和地區分類,2026-2034 年

人力資本管理市場規模、佔有率、趨勢和預測:按組件、部署類型、行業和地區分類,2026-2034 年 2026年全球人力資本管理市場報告

2026年全球人力資本管理市場報告