|

市場調查報告書

商品編碼

2063753

雲端HCM平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Cloud HCM Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

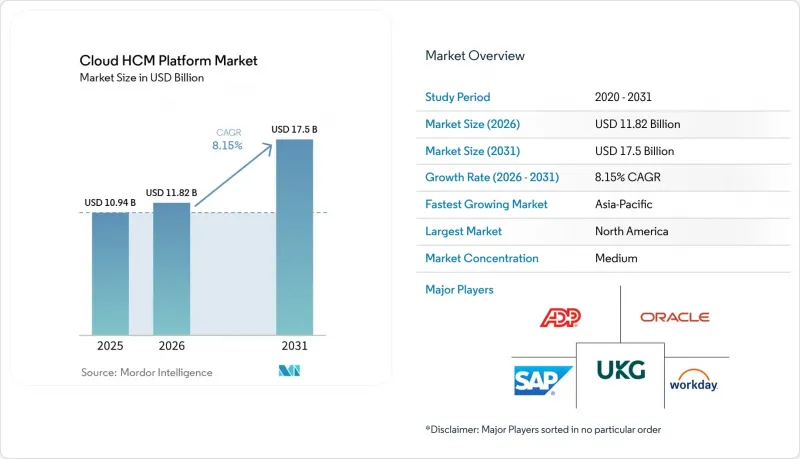

根據 Mordor Intelligence 預測,雲端 HCM 平台市場將從 2025 年的 109.4 億美元成長到 2026 年的 118.2 億美元,到 2031 年達到 175 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 8.15%。

本報告按部署模式(公共雲端、私有雲端、混合雲端)、組織規模(大型企業、中小企業)、應用領域(核心人力資源和人力資源管理、人才招聘和入職等)、產業(銀行、金融服務、保險等)和地區進行細分。市場預測以美元計價。

全球雲端HCM平台市場趨勢與洞察

利用人工智慧加速技能映射和人才情報分析

整合到領先平台中的技能推斷引擎如今能夠處理數十億個交易資料點,自動標記員工能力,推薦內部調動路徑,並縮短招募週期。光是 Workday Skills Cloud 每年就分析超過 8,000 億筆交易,而 SAP SuccessFactors 的動態技能架構則使企業能夠整合第三方本體,以符合特定職位。 Censia 和 Phenom 等專業合作夥伴聲稱,與關鍵字搜尋相比,發現潛在候選人的速度提高了 40%,這使得雇主能夠將現有員工重新安排到技能相似的崗位,並將招聘成本降低四分之一。這種效應在科技、專業服務和金融服務公司中尤其顯著,這些公司的平均技能半衰期已縮短至 2.5 年,動態人才智慧已成為董事會層面的優先事項。

大型企業中基於技能的人才規劃的興起

思科公司針對其3萬名員工推行基於技能的規劃,以及默克公司在全公司範圍內實施的技能分類系統,都顯示在人才設計中,能力而非靜態的職位名稱正日益受到重視。研究表明,基於技能的組織在高績效員工留任率方面提高了98%,新員工入職時間縮短了52%。為此,各平台正將技能本體和人工智慧驅動的技能差距分析功能直接整合到其核心人力資源系統中。 SAP的Joule Studio將於2025年發布,屆時人力資源團隊將能夠建立自訂代理,在無需IT干預的情況下識別技能差距並推薦培訓。實施工廠和臨床員工交叉培訓的製造和醫療保健公司報告稱,加班時間和空缺率均有所下降,但它們的成功取決於是否在運作前清理遺留數據並檢驗分類系統。

有關資料居住的法律法規正在增加本地化成本。

GDPR 和基於國家主權的相關法規強制要求在國內託管,迫使供應商維護重複的基礎設施和支援團隊。中國的網路安全法要求在中國境內部署獨立實例,印度和印尼也考慮類似的法規。將本地薪資核算系統與雲端人才管理模組結合的混合架構正逐漸成為一種經濟高效的解決方案,但雙重授權費用和複雜的資料同步抵消了預期的成本節約。

細分市場分析

到 2025 年,公共雲端將佔據雲端人力資本管理 (HCM) 平台市場 56.41% 的佔有率,這反映了 Workday 的多租戶 SaaS 模式的優勢,該模式無需本地硬體即可提供季度更新。混合模式正以 10.64% 的複合年成長率 (CAGR) 不斷擴張,隨著企業將公共雲端人才管理模組與本地薪資核算系統相結合以滿足資料主權法規,混合模式正變得越來越有吸引力。雖然雙重授權的經濟效益尚不明朗,但同時使用兩者可以避免通常與大規模全球部署相關的 600 萬至 1,200 萬美元的遷移成本。

混合部署越來越依賴Oracle Human Data Loader和SAP Integration Suite等即時連接器,從而實現日常資料同步,並降低薪資核算錯誤風險。第三方支援公司為傳統薪資系統提供折扣維護服務,進一步改變了成本效益的計算方式。 Gartner預測,到2028年,85%的企業將採用以雲端為中心的HR基礎設施,但受嚴格監管的產業可能長期維持混合模式。因此,隨著隱私法規的日益嚴格,混合配置的雲端HCM平台市場規模的成長速度可能會超過整體市場成長率。

到2025年,大型企業將佔據68.04%的收入佔有率,它們購買涵蓋全球薪資核算、分析和勞動力管理的端到端套件。同時,中小企業(SME)正以11.02%的複合年成長率成長,它們被低至每月6美元的員工定價以及90天內即可投入運作的承諾所吸引。中小企業的雲端HCM平台市場規模仍然較小,但隨著整合薪資核算、福利和考勤管理的輕量級套件取代電子表格,該市場正在快速擴張。

HiBob、Rippling 和 Deel 等供應商透過整合直覺的行動介面、IT 和人力資源整合以及跨國合規性來脫穎而出。儘管預算有限,68% 的中小企業 (SME) 仍傾向於採用雲端技術以避免基礎設施成本,但 46% 的企業仍然認為實施成本是一個障礙。免費增值模式和基於模板的入門流程正在降低這些障礙,預計即使大型企業的採用率趨於穩定,中小企業的兩位數採用率仍將持續。

區域分析

預計到2025年,北美地區將佔總收入的37.44%,這主要得益於高價值的聯邦契約,例如美國人事管理局價值1億美元的Workday契約,以及能源部技術現代化基金支持的3800萬美元實施項目。在加拿大和墨西哥,Workday的普及率穩定提升,這得益於SAP Joule將於2025年推出的西班牙語薪資解釋功能。供應商的主導地位顯而易見:在員工人數超過5000人的公司中,Workday、SAP和Oracle佔據了超過95%的企業決策權,並且在新採購意向調查中,Workday也處於領先地位。

亞太地區是成長最快的地區,複合年成長率達10.27%。 Darwinbox國際銷售額成長九倍,Ramco Systems在150個國家提供薪資核算服務,這些都顯示本地供應商正在將業務拓展到亞太地區以外。在日本,SmartHR以7萬名客戶企業領先國內市場,但全球供應商正面臨日益成長的本地化成本,因為他們需要為中國市場單獨運行系統以符合網路安全協議。印度即將實施的資料保護法和印尼第71/2019號法規增加了合規的複雜性,促使買家轉向擁有特定國家/地區薪資核算模組的供應商。

歐洲仍然是至關重要的市場,儘管其擴張速度放緩。由於GDPR和國家主權法規要求建立國內資料中心,Workday決定投資1.75億歐元(1.97億美元)在都柏林建立一個專門服務其歐洲客戶的人工智慧中心。 SAP憑藉與S/4HANA的深度整合以及涵蓋50多個國家的在地化薪資核算功能,在德國和法國保持著強勁的發展勢頭。同時, Oracle收購E.ON顯示其產品在受監管的公共產業越來越受歡迎。南美洲和中東及非洲地區在絕對規模上落後於其他國家,但正透過政府主導的數位轉型和行動優先的人才管理,獲得發展動力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 利用人工智慧加速技能映射和人才情報分析

- 大型企業中基於技能的人才規劃的興起

- 政府獎勵將人力資源系統遷移到雲端

- 全球薪資核算合規的複雜性正在迅速增加。

- 將生成式人工智慧副駕駛整合到 HCM 使用者介面中

- 產業專用的雲HCM加速器擴展

- 市場限制因素

- 有關資料居住的法律法規正在增加本地化成本。

- 傳統ERP系統中的持續整合瓶頸

- 中型企業整體擁有成本高

- 對供應商鎖定的擔憂阻礙了長期合約的簽訂。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按部署模式

- 公共雲端

- 私有雲端

- 混合雲端

- 按組織規模

- 大公司

- 中小企業

- 透過使用

- 核心人力資源與勞動力管理

- 薪資和薪資管理

- 人才招聘與入職

- 員工管理與考勤管理

- 學習與發展

- 績效管理與繼任者發展

- 人力資源分析與規劃

- 按行業分類

- 銀行業、金融服務業及保險業

- 醫療保健和生命科學

- 資訊科技/通訊

- 製造業

- 零售與電子商務

- 政府/公共部門

- 教育

- 酒店和旅遊

- 其他工業部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 東南亞

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Workday, Inc.

- SAP SE

- Oracle Corporation

- Automatic Data Processing, Inc.

- UKG Inc.

- Ceridian HCM Holding Inc.

- BambooHR LLC

- Paycom Software, Inc.

- Cornerstone OnDemand, Inc.

- PeopleStrategy, Inc.

- Rippling People Center, Inc.

- TriNet Group, Inc.

- Zenefits(YourPeople, Inc.)

- Gusto, Inc.

- Ramco Systems Limited

- Zoho Corporation Pvt. Ltd.

- The Sage Group plc

- Namely, Inc.

- HiBob Ltd.

- Darwinbox Digital Solutions Pvt. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the cloud HCM platform market size is expected to increase from USD 10.94 billion in 2025 to USD 11.82 billion in 2026 and reach USD 17.50 billion by 2031, growing at an 8.15% CAGR over 2026-2031.

This report is Segmented by Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR and Personnel Administration, Talent Acquisition and Onboarding, and More), Industry Vertical (Banking Financial Services and Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Cloud HCM Platform Market Trends and Insights

Accelerating AI-Driven Skill Mapping and Talent Intelligence

Skill inference engines embedded in leading platforms now process billions of transactional datapoints to auto-tag employee capabilities, surface internal mobility paths, and shorten hiring cycles. Workday Skills Cloud alone analyzes more than 800 billion transactions annually, while SAP SuccessFactors Dynamic Skills framework lets organizations integrate third-party ontologies for niche roles. Specialized partners such as Censia and Phenom claim 40% faster passive-candidate discovery versus keyword search, enabling employers to redeploy existing staff into skill-adjacent roles and cut recruiting costs by one-quarter. The effect is felt most in technology, professional-services, and financial-services companies where average skill half-life has dropped to 2.5 years, making dynamic talent intelligence a board-level priority.

Rise of Skills-Based Workforce Planning in Large Enterprises

Cisco's 30 000-employee shift to skills-based planning and Merck's enterprise-wide skills taxonomy show how competencies are replacing static jobs as the unit of workforce design. Research indicates skills-based organizations realize 98% higher high-performer retention and 52% faster ramp-up for new hires. Platforms respond by embedding skills ontologies and AI-driven gap analytics directly into core HR. SAP's 2025 launch of Joule Studio enables HR teams to build custom agents that pinpoint skill gaps and recommend training without IT intervention. Manufacturing and healthcare firms that cross-train production or clinical staff report lower overtime and vacancy rates, although success depends on cleansing legacy data and validating taxonomies before go-live.

Data Residency Legislation Increasing Localization Costs

GDPR and a patchwork of national sovereignty rules require in-country hosting, forcing vendors to duplicate infrastructure and support teams. China's cybersecurity laws demand separate Chinese instances, while India and Indonesia contemplate similar mandates. Hybrid architectures, on-premises payroll with cloud talent modules, are emerging as cost-effective workarounds, yet dual licenses and complex data synchronization erode anticipated savings.

Other drivers and restraints analyzed in the detailed report include:

- Integration of Generative AI Copilots Into HCM User Interfaces

- Surge in Global Payroll Compliance Complexity

- Persistent Integration Bottlenecks With Legacy ERP Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Public cloud accounted for 56.41% of the cloud HCM platform market in 2025, reflecting Workday's multi-tenant SaaS model that delivers quarterly updates without on-premises hardware. Hybrid models hold growing appeal, expanding at a 10.64% CAGR as enterprises pair public-cloud talent modules with on-premises payroll to satisfy data-sovereignty statutes. Dual-license economics remain delicate, yet coexistence avoids the USD 6-12 million migration costs typical of large global rollouts.

Hybrid deployments increasingly rely on real-time connectors such as Oracle Human Data Loader and SAP Integration Suite, enabling daily synchronization while mitigating payroll-error risk. Third-party support firms offering discounted maintenance for legacy payroll further shift the cost-benefit calculus. Gartner expects 85% of enterprises to operate cloud-centered HR infrastructure by 2028, but regulated sectors will keep hybrid models for the long term. The cloud HCM platform market size for hybrid setups is therefore positioned to outpace overall growth as privacy mandates tighten.

Large enterprises held 68.04% revenue share in 2025, purchasing end-to-end suites spanning global payroll, analytics, and workforce management. SMEs, however, are growing at 11.02% CAGR, attracted to per-employee pricing that starts at USD 6 monthly and promises go-lives inside 90 days. The cloud HCM platform market size for SMEs is still small, yet rising quickly as lightweight suites bundle payroll, benefits, and time tracking to displace spreadsheets.

Vendors such as HiBob, Rippling, and Deel differentiate via intuitive mobile interfaces, IT-HR convergence, and embedded multi-country compliance. Despite tight budgets, 68% of SMEs prefer cloud deployments to avoid infrastructure costs, with 46% still citing implementation expense as a barrier. Freemium entry tiers and template-driven onboarding lower those hurdles, suggesting sustained double-digit SME adoption even as enterprise penetration plateaus.

Geography Analysis

North America generated 37.44% of 2025 revenue, anchored by high-value federal contracts such as the U.S. Office of Personnel Management's USD 100 million Workday award and the Department of Energy's USD 38 million Technology Modernization Fund-backed rollout. Canada and Mexico show steady uptake, supported by SAP Joule's 2025 Spanish-language payroll explanations. Vendor dominance is stark: Workday, SAP, and Oracle influence over 95% of enterprise decisions at firms with more than 5 000 employees, with Workday leading new-buyer consideration surveys.

Asia-Pacific is the fastest-growing territory at a 10.27% CAGR. Darwinbox's 9-times international revenue surge and Ramco Systems' 150-country payroll reach illustrate home-grown vendors scaling beyond regional borders. Japan's SmartHR leads domestic share with 70 000 tenants, while global providers must operate separate Chinese instances to comply with cybersecurity protocols, inflating localization costs. India's impending data-protection law and Indonesia's Regulation 71/2019 add to compliance complexity, steering buyers toward vendors with country-specific payroll modules.

Europe remains material despite slower expansion. GDPR and national sovereignty statutes compel in-country data centers, prompting Workday to commit EUR 175 million (USD 197 million) to an AI center in Dublin tailored for European customers. SAP's deep integration with S/4HANA and localized payroll spanning 50-plus countries sustains traction in Germany and France, while Oracle's E.ON win underlines growing acceptance in regulated utilities. South America, the Middle East, and Africa trail in absolute value yet gain momentum through government digitization mandates and mobile-first workforce management.

- Workday, Inc.

- SAP SE

- Oracle Corporation

- Automatic Data Processing, Inc.

- UKG Inc.

- Ceridian HCM Holding Inc.

- BambooHR LLC

- Paycom Software, Inc.

- Cornerstone OnDemand, Inc.

- PeopleStrategy, Inc.

- Rippling People Center, Inc.

- TriNet Group, Inc.

- Zenefits (YourPeople, Inc.)

- Gusto, Inc.

- Ramco Systems Limited

- Zoho Corporation Pvt. Ltd.

- The Sage Group plc

- Namely, Inc.

- HiBob Ltd.

- Darwinbox Digital Solutions Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating AI-Driven Skill Mapping and Talent Intelligence

- 4.2.2 Rise of Skills-Based Workforce Planning in Large Enterprises

- 4.2.3 Government Incentives for Cloud Migration of HR Systems

- 4.2.4 Surge in Global Payroll Compliance Complexity

- 4.2.5 Integration of Generative AI Copilots Into HCM User Interfaces

- 4.2.6 Expansion of Industry-Specific Cloud HCM Accelerators

- 4.3 Market Restraints

- 4.3.1 Data Residency Legislation Increasing Localization Costs

- 4.3.2 Persistent Integration Bottlenecks With Legacy ERP Stacks

- 4.3.3 High Total Cost of Ownership for Mid-Market Buyers

- 4.3.4 Vendor Lock-In Concerns Limiting Long-Term Contract Commitments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Public Cloud

- 5.1.2 Private Cloud

- 5.1.3 Hybrid Cloud

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises (SMEs)

- 5.3 By Application

- 5.3.1 Core HR and Personnel Administration

- 5.3.2 Payroll and Compensation Management

- 5.3.3 Talent Acquisition and Onboarding

- 5.3.4 Workforce Management and Time Tracking

- 5.3.5 Learning and Development

- 5.3.6 Performance and Succession Management

- 5.3.7 HR Analytics and Planning

- 5.4 By Industry Vertical

- 5.4.1 Banking, Financial Services and Insurance

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 IT and Telecommunications

- 5.4.4 Manufacturing

- 5.4.5 Retail and E-Commerce

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Hospitality and Travel

- 5.4.9 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Southeast Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday, Inc.

- 6.4.2 SAP SE

- 6.4.3 Oracle Corporation

- 6.4.4 Automatic Data Processing, Inc.

- 6.4.5 UKG Inc.

- 6.4.6 Ceridian HCM Holding Inc.

- 6.4.7 BambooHR LLC

- 6.4.8 Paycom Software, Inc.

- 6.4.9 Cornerstone OnDemand, Inc.

- 6.4.10 PeopleStrategy, Inc.

- 6.4.11 Rippling People Center, Inc.

- 6.4.12 TriNet Group, Inc.

- 6.4.13 Zenefits (YourPeople, Inc.)

- 6.4.14 Gusto, Inc.

- 6.4.15 Ramco Systems Limited

- 6.4.16 Zoho Corporation Pvt. Ltd.

- 6.4.17 The Sage Group plc

- 6.4.18 Namely, Inc.

- 6.4.19 HiBob Ltd.

- 6.4.20 Darwinbox Digital Solutions Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

人力資本管理市場:按組件、授權模式、組織規模、部署和產業分類-2026-2032年全球市場預測

人力資本管理市場:按組件、授權模式、組織規模、部署和產業分類-2026-2032年全球市場預測 AI原生HCM平台:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)可組合式 HCM 平台:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)科技業薪酬管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)銀行、金融服務和保險 (BFSI) 行業的薪酬管理:市場佔有率分析、行業趨勢與統計數據、成長預測 (2026-2031)人力資本管理(HCM)企業資源規劃:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031)

AI原生HCM平台:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)可組合式 HCM 平台:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)科技業薪酬管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)銀行、金融服務和保險 (BFSI) 行業的薪酬管理:市場佔有率分析、行業趨勢與統計數據、成長預測 (2026-2031)人力資本管理(HCM)企業資源規劃:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031) 薪資和薪酬管理平台市場預測至2034年-按薪資處理階段、薪酬類型、平台功能、部署模式和最終用戶分類的全球分析

薪資和薪酬管理平台市場預測至2034年-按薪資處理階段、薪酬類型、平台功能、部署模式和最終用戶分類的全球分析 人力資本管理市場規模、佔有率和成長分析:按交付類型、部署類型、最終用戶產業、組織規模和地區分類-2026-2033年產業預測

人力資本管理市場規模、佔有率和成長分析:按交付類型、部署類型、最終用戶產業、組織規模和地區分類-2026-2033年產業預測 人力資本管理市場規模、佔有率、趨勢和預測:按組件、部署類型、行業和地區分類,2026-2034 年

人力資本管理市場規模、佔有率、趨勢和預測:按組件、部署類型、行業和地區分類,2026-2034 年 2026年全球人力資本管理市場報告

2026年全球人力資本管理市場報告