|

市場調查報告書

商品編碼

2065436

英國獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031)United Kingdom Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

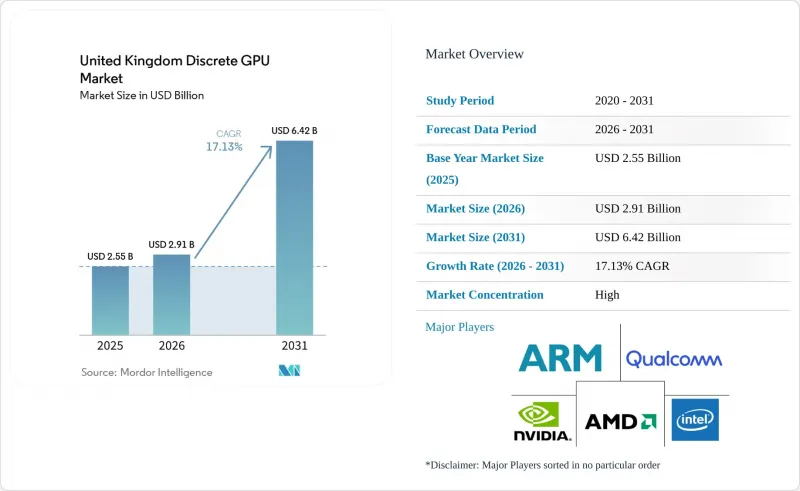

根據 Mordor Intelligence 預測,英國獨立 GPU 市場規模將從 2025 年的 25.5 億美元成長到 2026 年的 29.1 億美元,然後在 2031 年達到 64.2 億美元,2026 年至 2031 年的複合年成長率為 17.13%。

本報告按裝置應用(行動裝置和平板電腦、PC 和工作站、伺服器和資料中心加速器等)、記憶體類型(基於 GDDR 的 GPU 和基於 HBM 的 GPU)以及效能等級(低成本 GPU、主流 GPU、高效能消費級 GPU 等)進行細分。市場預測以美元 (USD) 為單位。

英國獨立顯示卡市場的趨勢與洞察

英國人工智慧新創企業爆炸性成長,對高階GPU的需求日益成長

在Nscale完成16億英鎊(20億美元)的資金籌措,用於為基礎模型開發者部署高密度GPU叢集之後,創業融資在2025年達到頂峰。資本集中於倫敦和劍橋導致該地區機架空間短缺,資料中心利用率超過了60%的行業標準。 Fractile AI的低精度運算技術可將功耗降低高達90%,從而擴大了對成本敏感的訓練工作負載的應用範圍。 NVIDIA承諾在2026年底前向英國客戶供應超過12萬台H200和Blackwell Ultra設備,確保在全球供不應求的情況下也能獲得供應。

政府對超級計算的投資

這項耗資20億英鎊的「運算路線圖」以Isambard-AI和愛丁堡國際資料中心為核心,計畫在2027年將英國的人工智慧研究資源擴大20倍。 Isambard-AI已向Nightingale AI在14個英國國家醫療服務系統(NHS)分支機構開展的聯邦學習試點計畫提供了100萬GPU小時的運算能力。人工智慧安全研究所發布的監管指南要求進行透明的模型風險評估,而提供合規承包工具的硬體供應商將獲得優先待遇。

台灣供應鏈對代工廠的依賴

英國客戶從台積電 (TSMC) 採購大量先進 GPU,而這種依賴關係被英國當局認為極易受到地緣政治變化的影響。由於與英國脫歐相關的原產地基準值,部分組裝的基板難以獲得關稅豁免,導致海關延誤和庫存緊張。儘管英國已製定透過歐盟晶圓廠實現多元化的計劃,但預計到 2028 年之前情況不會有所改善。

細分市場分析

2025年,「伺服器和資料中心加速器」佔據了英國獨立GPU市場39.59%的佔有率,超過了所有其他類別。這主要得益於CoreWeave公司斥資10億英鎊(約12.7億美元)在其倫敦工廠部署H200晶片。受人工智慧主權法規的推動,預計到2031年,英國伺服器用獨立GPU市場將以17.55%的複合年成長率成長。曾經佔據出貨量領先地位的個人電腦和工作站,隨著企業開始從支援GPU的虛擬機器串流傳輸桌面環境,其市佔率已下降至約28%。遊戲主機和攜帶式設備也為總銷售額做出了貢獻。同時,汽車和ADAS(高級駕駛輔助系統)設備也佔據了一定的市場佔有率,這主要得益於捷豹路虎採用了DRIVE Orin晶片。

資料中心的擴張導致對高功耗HBM記憶體板的需求集中,產品供應也因此轉向平均售價更高的高級產品。然而,英國英國醫療服務體系(NHS)的診斷先導計畫傾向於選擇功耗和足夠的張量吞吐量之間取得平衡的中階記憶體板,這表明部署模式正在趨於多樣化。隨著倫敦的機架空間日益緊張,超大規模超大規模資料中心業者正在蘇格蘭和英格蘭北部部署新的叢集,以利用當地電網的低延遲,並根據區域重新分配記憶體板,而不會影響國內整體銷售量成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 英國人工智慧新創企業爆炸性成長,對高階GPU的需求日益成長

- 政府對超級運算的投資(例如,前沿人工智慧工作小組)

- 雲端遊戲在英國。

- 汽車製造商向集中式ADAS計算平台的遷移

- 消費者對 4K/8K 和 VR 遊戲體驗的需求

- 在英國國家醫療服務體系(NHS)診斷領域擴展邊緣人工智慧推理

- 市場限制因素

- 台灣供應鏈對代工廠的依賴

- 高昂的電力成本阻礙了本地GPU群聚的廣泛應用。

- 平行程式設計人才庫技能短缺

- 英國脫歐後貿易協定相關的進口關稅存在不確定性

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按設備和應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機和掌上型遊戲機

- 汽車/ADAS

- 其他嵌入式和邊緣設備

- 按記憶體類型

- 配備 GDDR 記憶體的 GPU

- 配備 HBM 記憶體的 GPU

- 按績效水準

- 低成本GPU(100美元以下)

- 主流GPU(100-400美元)

- 高效能消費級GPU(400美元至1200美元)

- 資料中心/AI加速器GPU(超過1200美元)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- ARM Ltd.

- Imagination Technologies Ltd.

- Graphcore Ltd.

- Apple Inc.

- MediaTek Inc.

- Alibaba Group Holding Ltd.(T-Head)

- Baidu Inc.(Kunlun)

- Huawei Technologies Co. Ltd.(HiSilicon)

- Tenstorrent Inc.

- ASUSTeK Computer Inc.

- Zotac Technology Ltd.

- Sapphire Technology Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the united kingdom discrete GPU market size is expected to grow from USD 2.55 billion in 2025 to USD 2.91 billion in 2026 and is forecast to reach USD 6.42 billion by 2031 at a 17.13% CAGR over 2026-2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, and More), Memory Type (GDDR-Based GPUs and HBM-Based GPUs), and Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and More). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Discrete GPU Market Trends and Insights

Explosive Growth in UK AI Start-Ups Demanding High-End GPUs

Venture funding peaked in 2025 as Nscale closed GBP 1.6 billion (USD 2.0 billion) to deploy GPU-dense clusters that serve foundation-model developers. Capital concentration in London and Cambridge triggers localized rack-space shortages, pushing datacenter utilization above the industry norm of 60%. Fractile AI's low-precision arithmetic reduces power draw by up to 90%, widening the addressable base for cost-sensitive training workloads. NVIDIA pledged to deliver more than 120,000 H200 and Blackwell Ultra units to UK customers by late 2026, locking in supply despite global shortages.

Government Supercomputing Investments

The GBP 2 billion Compute Roadmap scales national AI Research Resource twenty-fold by 2027, anchored by Isambard-AI and the Edinburgh International Data Facility. Isambard-AI has already delivered one million GPU hours to Nightingale AI's federated learning pilot across 14 NHS. Regulatory guidance from the AI Safety Institute requires transparent model risk assessments, rewarding hardware vendors that offer turnkey compliance tooling.

Supply Chain Exposure to Taiwan Foundries

UK customers source a significant portion of their advanced GPUs from Taiwan Semiconductor Manufacturing Company, a reliance that officials deem "very exposed" to geopolitical upheavals. Due to Brexit's rules of origin thresholds, partially assembled boards face hurdles to achieving duty-free status, resulting in customs delays and straining inventory buffers. Even with plans for diversification through EU fabs, relief isn't expected until 2028.

Other drivers and restraints analyzed in the detailed report include:

- Rising Cloud Gaming Adoption Across the UK

- Automotive OEMs Shift to Centralized ADAS Compute Platforms

- High Electricity Costs Limiting On-Prem GPU Farms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers and Datacenter Accelerators controlled 39.59% of the United Kingdom discrete GPU market in 2025, eclipsing all other categories as CoreWeave earmarked GBP 1 billion (USD 1.27 billion) for London facilities powered by H200 silicon. The United Kingdom's discrete GPU market for server-class boards is projected to grow at a 17.55% CAGR to 2031, driven by AI sovereignty mandates. PCs and Workstations, once the shipment leader, slipped to about 28% share as enterprises stream desktop environments from GPU-enabled virtual machines. Gaming Consoles and Handhelds contributed to the total revenue. Meanwhile, Automotive and ADAS devices secured a share, bolstered by Jaguar Land Rover's adoption of the DRIVE Orin silicon.

Datacenter build-outs funnel demand toward power-hungry, HBM-equipped cards, tilting the mix toward premium average selling prices. NHS diagnostic pilots, however, prefer mid-tier boards that balance watt draw with sufficient tensor throughput, signaling pockets of diversified adoption. As London rack space tightens, hyperscalers are positioning new clusters in Scotland and the North to exploit shorter wait times for grid connections, redistributing regional card allocations without denting national volume growth.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- ARM Ltd.

- Imagination Technologies Ltd.

- Graphcore Ltd.

- Apple Inc.

- MediaTek Inc.

- Alibaba Group Holding Ltd. (T-Head)

- Baidu Inc. (Kunlun)

- Huawei Technologies Co. Ltd. (HiSilicon)

- Tenstorrent Inc.

- ASUSTeK Computer Inc.

- Zotac Technology Ltd.

- Sapphire Technology Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive Growth in UK AI Start-Ups Demanding High-End GPUs

- 4.2.2 Government Supercomputing Investments (e.g., Frontier AI Taskforce)

- 4.2.3 Rising Cloud Gaming Adoption Across the UK

- 4.2.4 Automotive OEMs' Shift to Centralized ADAS Compute Platforms

- 4.2.5 Consumer Demand for 4K/8K and VR-Ready Gaming Experiences

- 4.2.6 Expansion of Edge AI Inference in NHS Diagnostics

- 4.3 Market Restraints

- 4.3.1 Supply Chain Exposure to Taiwan Foundries

- 4.3.2 High Electricity Costs Limiting On-Prem GPU Farms

- 4.3.3 Skills Shortage in Parallel-Programming Talent Pool

- 4.3.4 Import Tariff Uncertainty Post Brexit Trade Deals

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-Based GPUs

- 5.2.2 HBM-Based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (Less than USD 100)

- 5.3.2 Mainstream GPUs (USD 100-USD 400)

- 5.3.3 High-Performance Consumer GPUs (USD 400-USD 1,200)

- 5.3.4 Data Center / AI Accelerator GPUs (Greater than USD 1,200)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies Inc.

- 6.4.5 Samsung Electronics Co. Ltd.

- 6.4.6 ARM Ltd.

- 6.4.7 Imagination Technologies Ltd.

- 6.4.8 Graphcore Ltd.

- 6.4.9 Apple Inc.

- 6.4.10 MediaTek Inc.

- 6.4.11 Alibaba Group Holding Ltd. (T-Head)

- 6.4.12 Baidu Inc. (Kunlun)

- 6.4.13 Huawei Technologies Co. Ltd. (HiSilicon)

- 6.4.14 Tenstorrent Inc.

- 6.4.15 ASUSTeK Computer Inc.

- 6.4.16 Zotac Technology Ltd.

- 6.4.17 Sapphire Technology Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

離散半導體市場規模、佔有率、趨勢和預測:按類型、最終用戶和地區分類(2026-2034 年)

離散半導體市場規模、佔有率、趨勢和預測:按類型、最終用戶和地區分類(2026-2034 年) 北美獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)歐洲獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)歐洲獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 2026年全球射頻和微波小訊號電晶體市場報告2026年全球射頻微波功率電晶體市場報告

2026年全球射頻和微波小訊號電晶體市場報告2026年全球射頻微波功率電晶體市場報告 離散半導體全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

離散半導體全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 離散半導體市場:按類型、最終用戶和地區分類

離散半導體市場:按類型、最終用戶和地區分類 離散半導體市場分析及至2035年預測:按類型、產品、技術、應用、材料類型、裝置、最終用戶、功能、安裝模式和解決方案分類用於分立元件的矽晶圓:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

離散半導體市場分析及至2035年預測:按類型、產品、技術、應用、材料類型、裝置、最終用戶、功能、安裝模式和解決方案分類用於分立元件的矽晶圓:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 離散半導體市場:按組件、產品類型、材料、應用和銷售管道- 全球預測 2026-2032

離散半導體市場:按組件、產品類型、材料、應用和銷售管道- 全球預測 2026-2032