|

市場調查報告書

商品編碼

2065426

北美獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

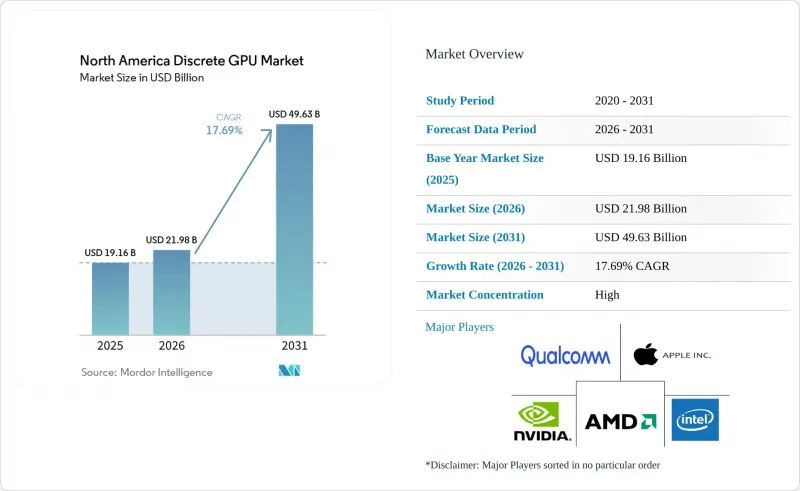

根據 Mordor Intelligence 預測,北美獨立 GPU 市場規模將從 2025 年的 191.6 億美元和 2026 年的 219.8 億美元成長到 2031 年的 496.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)%為 17.69%。

本報告按裝置應用(行動裝置和平板電腦、PC 和工作站、伺服器和資料中心加速器等)、記憶體類型(基於 GDDR 的 GPU 和基於 HBM 的 GPU)、效能等級(低成本 GPU、主流 GPU、高效能消費級 GPU 等)以及國家/地區(美國、加拿大等)進行細分。市場預測以美元 (USD) 為單位。

北美獨立GPU市場趨勢與洞察

資料中心人工智慧和機器學習工作負載的擴展

北美超大規模資料中心業者正在實施多吉瓦級採購框架,以加速頂級GPU的交付,並確保多代晶片的供應。 AMD與Meta達成的2026年至2030年供應協議包含一項機制,即在完成交付里程碑後授予股權認股權證,從而將供應商的資產負債表與客戶的產品藍圖緊密聯繫起來。 NVIDIA將Groq的叢集整合到Vera-Rubin平台中,將叢集分割為高吞吐量的訓練GPU和超低延遲的推理陣列,迫使競爭對手在每代幣成本而非單純的浮點運算效能(FLOPS)上展開競爭。美國能源局和國家標準與技術研究院(NIST)的新部署為聯邦政府資助的需求提供了基準。包括CoreWeave在內的獨立雲端服務供應商正在將其基礎設施部署擴展到美國區域城市和加拿大省份,進一步地域多角化。

AAA級遊戲對即時射線追蹤的需求正在激增。

RTX 50 系列顯示卡支援多幀生成,並將射線追蹤影格速率提升四倍,使即時路徑追蹤成為 AAA 級遊戲的標配功能。英特爾 Arc Battlemage 顯示卡搭載第二代射線追蹤核心,目標售價在 250 至 400 美元之間,定位為注重性價比的用戶之選,但其軟體生態系統仍不完善。隨著 GeForce NOW 等雲端遊戲服務從每個用戶共用虛擬 GPU 轉向每個用戶使用專用虛擬 GPU,雲端遊戲的蓬勃發展進一步推高了硬體需求。 240Hz 和 360Hz 顯示器的普及縮短了消費者的升級週期,並刺激了高階桌上型電腦的消費,與此同時,筆記型電腦的需求正轉向整合顯示卡解決方案。

先進節點的供應鏈波動與產能限制

台積電的CoWoS封裝是主要瓶頸,導致基於HBM3的GPU前置作業時間超過六個月。雖然亞利桑那州已開始試生產晶圓,但由於缺乏國內封裝系統,該公司不得不繼續使用成本高昂的跨太平洋運輸路線。美國國際技術安全與創新基金正在為加拿大和墨西哥的新生產線提供津貼,但地緣政治風險和良率不確定性仍然存在。三星3nm製程量產的延遲進一步加劇了風險,因為可供選擇的供應商範圍縮小了。

細分市場分析

預計到2025年,伺服器和加速器領域將佔據北美獨立GPU市場40.11%的佔有率,以18.22%的複合年成長率進一步鞏固其市場地位。該子部門仍然是訓練兆參數模型和即時推理叢集的首選部署方案。由此產生的採購規模吸引了光學、液冷和先進封裝等領域的價值鏈合作夥伴,進一步提高了市場進入門檻。雖然消費級PC和工作站仍然佔據較大的市場佔有率,但它們正面臨來自蘋果整合GPU以及搭載高通晶片的輕薄設備的替代效應。這些設備無需獨立GPU即可處理大部分專業創新工作負載。

北美獨立顯示卡市場中,汽車ADAS節點憑藉其小巧的基數和需要安全認證協處理器的區域架構,呈現出最強勁的成長動能。遊戲主機與攜帶式裝置正透過混合策略模糊細分市場的界限,將AMD Ryzen Z1 APU與外接GPU擴充座結合,但獨立顯示卡的銷售量仍較為有限。邊緣設備、工業無人機和視訊協作設備越來越依賴高通的系統晶片),這拖累了低功耗獨立顯示卡的未來銷售量。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- AAA級遊戲對即時射線追蹤的需求激增

- 雲端遊戲平台需要GPU伺服器,這類平台發展迅速。

- 資料中心人工智慧和機器學習工作負載的擴展

- 高刷新率顯示器在電競領域的日益普及,縮短了GPU的更換週期。

- 政府主導的半導體政策正在推動國內GPU製造業的發展。

- 汽車製造商向集中式區域架構的轉變,推動了對 ADAS(高級駕駛輔助系統)獨立 GPU 協處理器的需求增加。

- 市場限制因素

- 由於先進節點產能受限,供應鏈出現波動

- 平均售價 (ASP) 的上漲使得高階 GPU 對一般消費者來說難以負擔。

- 美國一些州收緊了資料中心的能源法規,限制了GPU機架的密度。

- 對GPU供應商商品搭售行為的反壟斷審查可能會延遲產品發布。

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按設備和應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機和掌上型遊戲機

- 汽車/ADAS

- 其他嵌入式和邊緣設備

- 按記憶體類型

- 配備 GDDR 記憶體的 GPU

- 配備 HBM 記憶體的 GPU

- 按績效水準

- 低成本GPU(100美元以下)

- 主流GPU(100-400美元)

- 高效能消費級GPU(400美元至1200美元)

- 資料中心/AI加速器GPU(超過1200美元)

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Qualcomm Technologies Inc.

- Apple Inc.

- Imagination Technologies Ltd.

- Arm Ltd.

- Samsung Electronics Co. Ltd.

- MediaTek Inc.

- Graphcore Ltd.

- Cerebras Systems Inc.

- Tenstorrent Inc.

- Broadcom Inc.

- ASUSTeK Computer Inc.

- Micro-Star International Co. Ltd.

- Gigabyte Technology Co. Ltd.

- Sapphire Technology Ltd.

- Zotac Technology Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america discrete GPU market size is projected to expand from USD 19.16 billion in 2025 and USD 21.98 billion in 2026 to USD 49.63 billion by 2031, registering a 17.69% CAGR between 2026 to 2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, and More), Memory Type (GDDR-Based GPUs and HBM-Based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and More), and Country (United States, Canada, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America Discrete GPU Market Trends and Insights

Expanding AI and ML Workloads in Data Centers

North American hyperscalers are executing multi-gigawatt purchase frameworks that front-load deliveries of top-bin GPUs, locking in allocation across several silicon generations. AMD's 2026-2030 supply agreement with Meta vests equity warrants against shipment milestones, intertwining vendor balance sheets with customer roadmaps. NVIDIA's integration of Groq's LP30 into the Vera-Rubin platform splits clusters into high-throughput training GPUs and ultra-low-latency inference arrays, forcing rivals to compete on cost-per-token rather than raw FLOPS. New installations at the U.S. Department of Energy and the National Institute of Standards and Technology ensure a baseline of federally funded demand. CoreWeave and other independent cloud providers are broadening infrastructure footprints into secondary U.S. metros and Canadian provinces, further localizing GPU capacity.

Surging Demand for Real-Time Ray Tracing in AAA Gaming Titles

The RTX 50 Series enables multi-frame generation, quadrupling ray-traced frame rates, making real-time path tracing the default in big-budget titles. Intel's Arc Battlemage targets the USD 250-USD 400 band with second-generation ray-tracing cores, positioning the brand as a cost-conscious alternative, though software ecosystem gaps remain. Growth in cloud gaming compounds hardware pull-through as services such as GeForce NOW shift from shared to dedicated virtual GPUs per subscriber. Widespread adoption of 240 Hz and 360 Hz monitors compresses consumer upgrade cycles, anchoring premium desktop spend even as notebook demand migrates to integrated solutions.

Supply Chain Volatility of Advanced Nodes Capacity Constraints

TSMC's CoWoS packaging is the principal bottleneck, with HBM3 GPU lead times exceeding 6 months. Although pilot wafer output in Arizona has started, the lack of on-shore packaging still forces costly trans-Pacific loops. The U.S. International Technology Security and Innovation Fund is subsidizing new lines in Canada and Mexico, yet geopolitical and yield uncertainties persist. Samsung's delayed 3 nm ramp narrows alternative sourcing, further concentrating risk.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM Shift to Centralized Zonal Architectures Demanding Discrete GPU Co-Processors for ADAS

- Rapid Growth of Cloud Gaming Platforms Requiring GPU Servers

- Rising ASPs Making High-End GPUs Unaffordable for Mainstream Consumers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The servers and accelerators segment accounted for 40.11% of the North America discrete GPU market share in 2025, a position it is expected to reinforce with an 18.22% CAGR. This sub-sector remains the preferred deployment target for trillion-parameter model training and real-time inference clusters. The resulting procurement scale is attracting value-chain partners in optics, liquid cooling, and advanced packaging, deepening entry barriers. Consumer PCs and workstations, while still sizeable, face a substitution effect from Apple's integrated GPUs and Qualcomm-powered thin-and-light designs that meet most professional creation workloads without discrete cards.

Automotive ADAS nodes, though starting from a smaller base, exhibit the sharpest slope within the North America discrete GPU market, helped by zonal architectures that require safety-certified co-processors. Gaming consoles and handhelds adopt hybrid strategies, such as AMD Ryzen Z1 APUs paired with external GPU docks, blurring segment lines but keeping discrete revenue modest. Edge devices, industrial drones, and video collaboration appliances increasingly rely on Qualcomm system-on-chips, trimming prospective unit volumes for low-power discrete boards.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Qualcomm Technologies Inc.

- Apple Inc.

- Imagination Technologies Ltd.

- Arm Ltd.

- Samsung Electronics Co. Ltd.

- MediaTek Inc.

- Graphcore Ltd.

- Cerebras Systems Inc.

- Tenstorrent Inc.

- Broadcom Inc.

- ASUSTeK Computer Inc.

- Micro-Star International Co. Ltd.

- Gigabyte Technology Co. Ltd.

- Sapphire Technology Ltd.

- Zotac Technology Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Real-Time Ray Tracing in AAA Gaming Titles

- 4.2.2 Rapid Growth of Cloud Gaming Platforms Requiring GPU Servers

- 4.2.3 Expanding AI and ML Workloads in Data Centers

- 4.2.4 Increasing Penetration of High-Refresh-Rate E-Sports Monitors Raising GPU Upgrade Cycles

- 4.2.5 Government-Funded Semiconductor Initiatives Boosting Domestic GPU Manufacturing

- 4.2.6 Automotive OEM Shift to Centralized Zonal Architectures Demanding Discrete GPU Co-Processors for ADAS

- 4.3 Market Restraints

- 4.3.1 Supply Chain Volatility of Advanced Nodes Capacity Constraints

- 4.3.2 Rising ASPs Making High-End GPUs Unaffordable for Mainstream Consumers

- 4.3.3 Escalating Data Center Energy Regulations Limiting GPU Rack Density in Some U.S. States

- 4.3.4 Antitrust Scrutiny on GPU Vendor Bundling Practices Potentially Delaying Product Launches

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-Based GPUs

- 5.2.2 HBM-Based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (Less than USD 100)

- 5.3.2 Mainstream GPUs (USD 100-USD 400)

- 5.3.3 High-Performance Consumer GPUs (USD 400-USD 1,200)

- 5.3.4 Data Center / AI Accelerator GPUs (Greater than USD 1,200)

- 5.4 By Counrty

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies Inc.

- 6.4.5 Apple Inc.

- 6.4.6 Imagination Technologies Ltd.

- 6.4.7 Arm Ltd.

- 6.4.8 Samsung Electronics Co. Ltd.

- 6.4.9 MediaTek Inc.

- 6.4.10 Graphcore Ltd.

- 6.4.11 Cerebras Systems Inc.

- 6.4.12 Tenstorrent Inc.

- 6.4.13 Broadcom Inc.

- 6.4.14 ASUSTeK Computer Inc.

- 6.4.15 Micro-Star International Co. Ltd.

- 6.4.16 Gigabyte Technology Co. Ltd.

- 6.4.17 Sapphire Technology Ltd.

- 6.4.18 Zotac Technology Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

離散半導體市場規模、佔有率、趨勢和預測:按類型、最終用戶和地區分類(2026-2034 年)

離散半導體市場規模、佔有率、趨勢和預測:按類型、最終用戶和地區分類(2026-2034 年) 歐洲獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)英國獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031)

歐洲獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)英國獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031) 2026年全球射頻和微波小訊號電晶體市場報告2026年全球射頻微波功率電晶體市場報告

2026年全球射頻和微波小訊號電晶體市場報告2026年全球射頻微波功率電晶體市場報告 離散半導體全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

離散半導體全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 離散半導體市場:按類型、最終用戶和地區分類

離散半導體市場:按類型、最終用戶和地區分類 離散半導體市場分析及至2035年預測:按類型、產品、技術、應用、材料類型、裝置、最終用戶、功能、安裝模式和解決方案分類用於分立元件的矽晶圓:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

離散半導體市場分析及至2035年預測:按類型、產品、技術、應用、材料類型、裝置、最終用戶、功能、安裝模式和解決方案分類用於分立元件的矽晶圓:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 離散半導體市場:按組件、產品類型、材料、應用和銷售管道- 全球預測 2026-2032

離散半導體市場:按組件、產品類型、材料、應用和銷售管道- 全球預測 2026-2032