|

市場調查報告書

商品編碼

2065431

歐洲獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)Europe Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

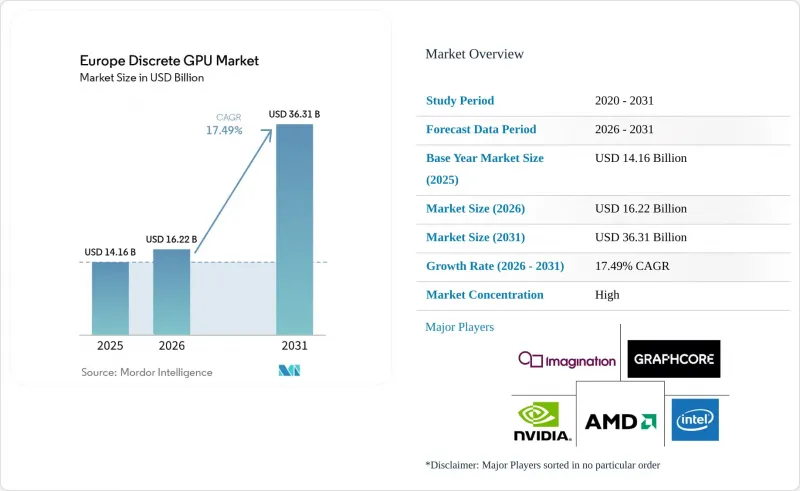

根據 Mordor Intelligence 預測,獨立 GPU 市場將從 2026 年的 162.2 億美元成長到 2031 年的 363.1 億美元,2026 年至 2031 年的複合年成長率為 17.49%。

本報告按裝置應用(行動裝置和平板電腦、PC 和工作站、伺服器和資料中心加速器等)、記憶體類型(基於 GDDR 的 GPU 和基於 HBM 的 GPU)、效能等級(低成本 GPU、主流 GPU、高效能消費級 GPU 等)以及國家/地區(德國、英國、法國等)進行細分。市場預測以美元 (USD) 為單位。

歐洲獨立GPU市場的趨勢與洞察

擴大在歐洲資料中心部署生成式人工智慧工作負載

為了滿足注重隱私的人工智慧推理和訓練需求,歐洲的超大規模資料中心業者和主權雲端服務供應商正以前所未有的規模部署獨立GPU。德國電信的慕尼黑人工智慧工廠將於2026年初投入運作,屆時將配備1萬塊Blackwell GPU,凸顯了本地運算主權的重要性。管理體制的分散阻礙了跨國資源共用,導致每塊GPU的需求量增加,採購合約期限延長。即使是像Meta這樣的美國平台,目前也在歐洲購買了6吉瓦的MI450容量,以符合本地化規則。即將推出的《人工智慧責任指令》將進一步促使企業轉向本地推理架構,從而進一步鞏固未來多年的市場需求。

歐盟氣候目標加速了電動車和高級駕駛輔助系統(ADAS)的運算需求。

嚴格的淨零排放標準和內燃機逐步淘汰計畫迫使汽車製造商採用獨立GPU來實現L3-L4級自動駕駛。儘管NVIDIA的DRIVE Thor系統晶片將於2025年開始提供樣品,但一級供應商仍在將其與Ada系列獨立GPU結合使用,以處理即時感測器融合。德國工廠已透過將Omniverse RTX 6000 Ada顯示卡引入其數位雙胞胎生產線完成了維修,而法國OEM廠商則繼續利用基於GPU的模型重訓練進行空中下載(OTA)更新。隨著歐盟7排放標準即將實施,獨立GPU很可能在兩個車型週期內應用於量產車型。

先進節點代工廠的供應鏈波動

歐洲嚴重依賴一家亞洲晶圓代工廠提供5奈米以下製程的產能。台積電優先滿足智慧型手機和超大規模資料中心業者大規模積體電路(ASIC)的2奈米訂單,可能導致其分配給獨立GPU的產能按季度減少。同時,三星的3奈米製程良率不佳,阻礙了雙源製程的普及。此外,儘管市場對先進的CoWoS封裝需求旺盛,但目前的訂單仍超過供應量。展望未來,英特爾晶圓代工服務計畫在2027年實現18埃製程的量產。然而,缺乏HBM整合的專業知識是一個挑戰,這將在可預見的未來限制歐洲GPU供應商的供應多元化。

細分市場分析

預計到2025年,伺服器和資料中心加速器將佔據獨立GPU市場佔有率的39.61%,並將以18.11%的複合年成長率成長至2031年。這一成長反映了超大規模資料中心業者和自主雲端計畫(例如Mistral AI投資8.3億歐元(8.881億美元)的巴黎叢集)的發展。同時,在消費級PC領域,獨立GPU正逐漸被推向內容創作等專業細分市場,因為日常任務通常由整合式顯示卡處理。儘管汽車和ADAS(高級駕駛輔助系統)領域的需求較小,但隨著梅賽德斯-奔馳和寶馬等公司將獨立GPU應用於L3級自動駕駛檢驗,該領域正呈現兩位數的成長。

由於 PlayStation 5 和 Xbox Series X 的硬體生命週期將延長至 2028 年,遊戲主機市場仍保持穩定。行動裝置依賴整合 GPU,獨立 GPU 的普及率僅限於小眾遊戲平板電腦。工業視覺和醫療成像系統雖然收入穩健但較為溫和,漫長的認證流程也減緩了其成長速度。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- CPU-GPU整合方面的限制正在推動對獨立GPU的需求。

- 擴大在歐洲資料中心部署生成式人工智慧工作負載

- 歐洲獨立顯示卡市場

- 即時射線追蹤技術在3A遊戲的普及

- 歐盟氣候目標正在加速電動車和高級駕駛輔助系統(ADAS)運算需求的成長。

- 由於開放原始碼GPU驅動程式的成熟,整體擁有成本降低。

- 根據歐盟晶片法對國內GPU製造提供補貼

- 市場限制因素

- 領先節點代工廠的供應鏈波動

- 加密貨幣市場低迷後,通路庫存過剩。

- 歐盟加強資料中心能源效率監管。

- HBM價格上漲,對車載OEM廠商的利潤率帶來越來越大的壓力。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按設備和應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機和掌上型遊戲機

- 汽車/ADAS

- 其他嵌入式和邊緣設備

- 按記憶體類型

- 配備 GDDR 記憶體的 GPU

- 配備 HBM 記憶體的 GPU

- 按績效水準

- 低成本GPU(100美元以下)

- 主流GPU(100-400美元)

- 高效能消費級GPU(400美元至1200美元)

- 資料中心/AI加速器GPU(超過1200美元)

- 按地區

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Imagination Technologies Ltd.

- Graphcore Ltd.

- Kalray SA

- ASUStek Computer Inc.

- Micro-Star International Co. Ltd.

- GIGABYTE Technology Co. Ltd.

- Sapphire Technology Ltd.

- Palit Microsystems Ltd.

- ZOTAC Technology Ltd.

- Colorful Technology Co. Ltd.

- PNY Technologies Inc.

- ASRock Inc.

- Leadtek Research Inc.

- KFA2(Galaxy Microsystems)

第7章 市場機會與未來展望

According to Mordor Intelligence, the discrete GPU market size is projected to expand from USD 16.22 billion in 2026 to USD 36.31 billion by 2031, registering a CAGR of 17.49% over 2026-2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, and More), Memory Type (GDDR-Based GPUs and HBM-Based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and More), and Country (Germany, United Kingdom, France, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Discrete GPU Market Trends and Insights

Rising Adoption of Generative AI Workloads in European Data Centers

European hyperscalers and sovereign cloud providers are deploying discrete GPUs at unprecedented scale to meet privacy-centric AI inference and training mandates. Deutsche Telekom's Munich AI Factory came online in early 2026 with 10,000 Blackwell GPUs, demonstrating the need for localized compute sovereignty. Fragmented regulatory regimes prevent cross-border pooling, inflating per-unit GPU requirements and lengthening purchase commitments. Even U.S. platforms such as Meta now provision 6 gigawatts of MI450 capacity in Europe to meet localization rules.A forthcoming AI liability directive will further push enterprises toward on-premises inference stacks, reinforcing multiyear demand visibility.

EU Climate Targets Accelerating EV and ADAS Compute Requirements

Strict net-zero and internal-combustion-phase-out timelines compel automakers to embed discrete GPUs for Level 3-4 autonomy. NVIDIA's DRIVE Thor system-on-chip samples in 2025, but tier-one suppliers still pair it with discrete Ada-generation GPUs to manage real-time sensor fusion. German plants have already retrofitted their digital twin production lines with Omniverse RTX 6000 Ada boards, while French OEMs continue to rely on GPU-accelerated model retraining for over-the-air updates. Expected Euro 7 particulate rules will push discrete GPUs into mass-market vehicles within two model cycles.

Supply Chain Volatility in Advanced Node Foundries

Europe relies heavily on a single Asian foundry for sub-5-nanometer capacity. TSMC, prioritizing 2-nanometer orders for smartphones and hyperscaler ASICs, risks quarterly cutbacks to discrete GPU allocations. Meanwhile, Samsung's struggles with yields at the 3-nanometer node have dissuaded dual sourcing. Additionally, while advanced CoWoS packaging sees high demand, it is currently oversubscribed. Looking ahead, Intel Foundry Services aims for 18-angstrom production by 2027. However, their lack of expertise in HBM integration poses challenges, restricting immediate supply diversification for GPU vendors in Europe.

Other drivers and restraints analyzed in the detailed report include:

- Subsidies Under the EU Chips Act for Local GPU Manufacturing

- Proliferation of Real-Time Ray Tracing in AAA Games

- Escalating HBM Pricing Pressures on Board OEM Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers and datacenter accelerators captured 39.61% of the discrete GPU market share in 2025 and will rise at an 18.11% CAGR through 2031. This expansion mirrors hyperscaler and sovereign-cloud commitments such as Mistral AI's EUR 830 million (USD 888.1 million) Paris cluster. Meanwhile, consumer PCs offload routine tasks to integrated graphics, pushing discrete GPUs into specialized content-creation niches. Automotive and ADAS demand, although smaller, records double-digit growth as Mercedes-Benz and BMW embed discrete GPUs for Level-3 autonomy validation.

Gaming consoles remain flat because PlayStation 5 and Xbox Series X hardware cycles run until 2028. Mobile devices rely on integrated GPUs, limiting discrete penetration to niche gaming tablets. Industrial vision and medical-imaging systems contribute steady but modest revenue, slowed by lengthy certification timelines.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Imagination Technologies Ltd.

- Graphcore Ltd.

- Kalray SA

- ASUStek Computer Inc.

- Micro-Star International Co. Ltd.

- GIGABYTE Technology Co. Ltd.

- Sapphire Technology Ltd.

- Palit Microsystems Ltd.

- ZOTAC Technology Ltd.

- Colorful Technology Co. Ltd.

- PNY Technologies Inc.

- ASRock Inc.

- Leadtek Research Inc.

- KFA2 (Galaxy Microsystems)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 CPU-GPU Integration Constrains Adds Stand-Alone GPU Demand

- 4.2.2 Rising Adoption of Generative AI Workloads in European Data Centers

- 4.2.2.1 Europe Discrete GPU Market

- 4.2.3 Proliferation of Real-Time Ray Tracing in AAA Games

- 4.2.4 EU Climate Targets Accelerating EV and ADAS Compute Requirements

- 4.2.5 Open-Source GPU Driver Maturity Lowering Total Cost of Ownership

- 4.2.6 Subsidies Under EU Chips Act for Local GPU Manufacturing

- 4.3 Market Restraints

- 4.3.1 Supply Chain Volatility in Advanced Node Foundries

- 4.3.2 Channel Inventory Gluts Post-Crypto Down-Cycles

- 4.3.3 Tightened EU Energy-Efficiency Regulations on Data Centers

- 4.3.4 Escalating HBM Pricing Pressures on Board OEM Margins

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-based GPUs

- 5.2.2 HBM-based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (Less than USD 100)

- 5.3.2 Mainstream GPUs (USD 100-USD 400)

- 5.3.3 High-Performance Consumer GPUs (USD 400-USD 1,200)

- 5.3.4 Data Center / AI Accelerator GPUs (Greater than USD 1,200)

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Imagination Technologies Ltd.

- 6.4.5 Graphcore Ltd.

- 6.4.6 Kalray SA

- 6.4.7 ASUStek Computer Inc.

- 6.4.8 Micro-Star International Co. Ltd.

- 6.4.9 GIGABYTE Technology Co. Ltd.

- 6.4.10 Sapphire Technology Ltd.

- 6.4.11 Palit Microsystems Ltd.

- 6.4.12 ZOTAC Technology Ltd.

- 6.4.13 Colorful Technology Co. Ltd.

- 6.4.14 PNY Technologies Inc.

- 6.4.15 ASRock Inc.

- 6.4.16 Leadtek Research Inc.

- 6.4.17 KFA2 (Galaxy Microsystems)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

離散半導體市場規模、佔有率、趨勢和預測:按類型、最終用戶和地區分類(2026-2034 年)

離散半導體市場規模、佔有率、趨勢和預測:按類型、最終用戶和地區分類(2026-2034 年) 北美獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)英國獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031)

北美獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)英國獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031) 2026年全球射頻和微波小訊號電晶體市場報告2026年全球射頻微波功率電晶體市場報告

2026年全球射頻和微波小訊號電晶體市場報告2026年全球射頻微波功率電晶體市場報告 離散半導體全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

離散半導體全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 離散半導體市場:按類型、最終用戶和地區分類

離散半導體市場:按類型、最終用戶和地區分類 離散半導體市場分析及至2035年預測:按類型、產品、技術、應用、材料類型、裝置、最終用戶、功能、安裝模式和解決方案分類用於分立元件的矽晶圓:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

離散半導體市場分析及至2035年預測:按類型、產品、技術、應用、材料類型、裝置、最終用戶、功能、安裝模式和解決方案分類用於分立元件的矽晶圓:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 離散半導體市場:按組件、產品類型、材料、應用和銷售管道- 全球預測 2026-2032

離散半導體市場:按組件、產品類型、材料、應用和銷售管道- 全球預測 2026-2032