|

市場調查報告書

商品編碼

2064538

亞太地區液冷GPU(圖形處理器):市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Asia-Pacific Graphics Processing Unit (GPU) Liquid Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

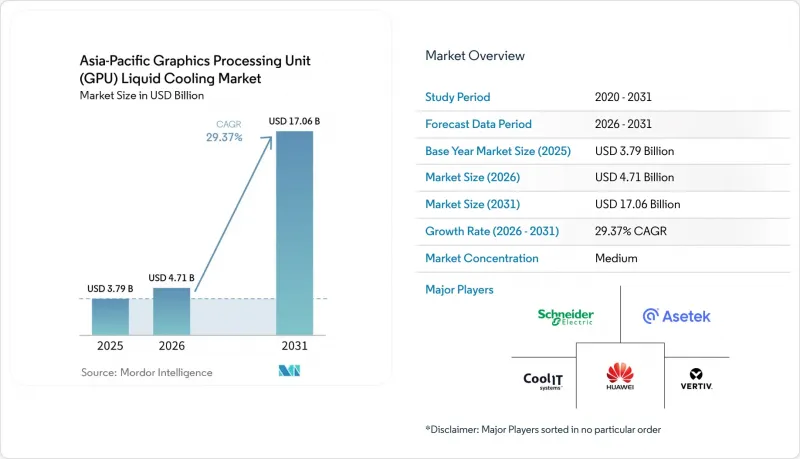

根據 Mordor Intelligence 預測,亞太地區 GPU(圖形處理單元)液冷市場規模預計將從 2025 年的 37.9 億美元成長到 2026 年的 47.1 億美元,然後在 2031 年達到 170.6 億美元,2026 年至 2031 年的複合年成長率為 29.7%。

本報告按冷卻方式(單相水冷、雙相水冷)、冷卻等級(組件級冷卻、伺服器/機架級冷卻)、部署方式(超大規模/雲端、企業級、邊緣AI、其他)、GPU功率密度(小於300W、300W-700W、大於700W)和地區進行細分。市場預測以美元(USD)計價。

亞太地區GPU液冷市場趨勢與分析

人工智慧主導的超大規模擴展正在推動液冷技術的應用。

阿里巴巴、三星SDS、OpenAI和Global Switch等公司營運的資料中心,其機架單機功耗超過100千瓦,GPU單機功耗高達1200瓦。在這樣的環境下,風冷並不經濟。阿里巴巴的飛天平台已在浸沒式冷卻槽中運作超過10萬顆GPU,PUE值僅1.09,從而將資料中心的能源運作降低了約一半。 2026年3月,三星SDS在龜尾市啟動了一座60兆瓦人工智慧園區的建設。該專案投資4,273億韓元(約3.2億美元)用於混合液冷基礎設施,彰顯了三星對DTC(直接晶片)系統的長期信心。 Global Switch香港公司已將其液冷容量提升了30兆瓦,而Nxera位於新加坡大士的資料中心則為政府主導的人工智慧工作負載安裝了一套58兆瓦的熱水循環系統。因此,亞太地區的GPU液冷市場正跟隨超大規模資料中心業者的發展趨勢。隨著GPU車型尺寸的不斷增加,散熱預算也從最佳化轉向徹底取代風冷系統。

東亞和東南亞的能源效率法規

日本經濟產業省規定,到2030年,資料中心的PUE值必須達到1.4,而從2029年起,新建設資料中心的PUE值必須達到1.3,這實際上禁止了在潮濕氣候下使用傳統冷卻器。中國的冷卻器能源效率標示制度和省級電力分配方案也同樣鼓勵在晶片級而非機房級進行散熱的設施。聯想的「海王星」冰水機組的進水溫度僅為45°C,這使得營運商能夠回收廢熱,繞過消耗高達40%設施電力的冷卻器,並滿足新的碳排放預算要求。新加坡的「綠色資料中心藍圖」進一步加大了壓力,將新的電力分配與已證實的PUE值提升掛鉤。因此,亞太地區的GPU液冷市場正受益於將能源效率作為獲取電力和土地的先決條件的政策。

前期資本投入高,且現有設施維修複雜。

維修直接冷卻式(DTC)系統每千瓦的成本為 500 至 800 美元,是空冷系統升級成本的兩倍多,而且需要分階段過渡,同時還要確保運作時間不受影響。營運商通常需要加固管道、升級泵浦的電氣設備並改造消防系統,這會將投資回收期延長至 3 至 5 年,對於機架密度低於 50 千瓦的場所來說,這無疑是一個阻礙。由於客製化設計會影響規模經濟效益,許多現有設施的業主往往等到熱負荷限制迫使他們徹底搬遷時才進行改造,而不是選擇分階段維修。

細分市場分析

到2025年,單相解決方案將佔據亞太地區GPU液冷市場74.51%的佔有率,這一地位得益於成熟的水循環系統與標準設施基礎設施的整合。聯想Neptune和HPE ProLiant XD685的進水溫度為45 度C,PUE值保持在1.1左右,並為熟悉冷水機組的維護人員提供了易於上手的維護模式。到2025年,兩相系統的市佔率將僅為25.49%,但其複合年成長率高達32.17%,這主要得益於ZutaCore和三菱重工成功地將機架級部分PUE值控制在1.01左右,並消除了機房閒置頻段中的水污染。

NVIDIA GB200 和 AMD MI300X 等晶片的功耗已突破 1000 瓦大關。一旦達到此閾值,傳統的冷卻方式將因水冷散熱裕度有限以及所需流量對水泵的高功耗而效率低下。這促使人們對替代冷卻方案,尤其是兩相冷卻系統,產生了濃厚的興趣。開利對 ZutaCore 的投資以及特靈對 LiquidStack 的收購,凸顯了產業正在發生的重大轉變。這些暖通空調產業巨頭的策略性舉措,顯示了他們對兩相冷卻技術藍圖的信心,該路線圖旨在提高效率和擴充性。因此,預計到 2028 年,亞太地區的 GPU 液冷市場將轉向介電液體,這標誌著冷卻技術的重大變革。

預計到2025年,組件級冷板將佔亞太地區GPU液冷市場55.72%的佔有率。這與超大規模資料中心業者專注於最佳化單一晶片的趨勢相符。這些冷板旨在提供晶片級冷卻,對於管理超大規模環境中GPU的高發熱量至關重要。 Supermicro的DLC-2是該領域的領先解決方案,能夠排放92%的伺服器熱量。這項能力使營運商能夠無縫整合GPU和CPU節點,而無需對機架進行大規模改造。同時,託管業者擴大採用機架級冷卻液分配單元(CDU)來簡化散熱流程。這些單元將散熱視為共用服務,提供集中式冷卻方案,從而簡化操作並提高效率。

機架級解決方案,例如 ZutaCore 的 2 兆瓦機架末端 CDU 和 CoolIT 的 CHx500 堆疊式冷卻器,正成為 Equinix 和 STT GDC 等大型營運商維修中不可或缺的一部分。這些解決方案使設施所有者能夠繼續管理關鍵方面,例如指標、維護和服務等級協定 (SLA)。隨著機架級服務交付以 31.60% 的複合年成長率 (CAGR) 成長,市場正在經歷冷卻策略的重大轉變。租戶正在拋棄每個機架獨立的管道配置,轉而選擇冷卻即服務 (CaaS)。這種模式與市場向多租戶 AI叢集的轉變相契合,後者需要可擴展且高效的冷卻解決方案來支援高效能運算需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人工智慧主導的超大規模擴展的普及正在推動液冷技術的應用。

- 東亞和東南亞的能源效率強制法規

- 5G網路中邊緣AI推理節點的快速擴展

- 大城市資料中心土地資源受限,導致機架級密度不斷增加。

- 現成的液態相容共存容量

- 冷卻劑化學技術的進步使得非導電兩相設計成為可能。

- 市場限制因素

- 前期資本投入高,且現有設施的維修複雜。

- 新興市場缺乏熟練人員來處理液冷系統的維護和運作(O&M)。

- 精密冷板和快速接頭的供應鏈瓶頸

- 關於雙相電介質中 PFAS 法規的不確定性

- 產業價值鏈與供應鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章:預測市場規模與成長率

- 透過冷卻法

- 單相液體冷卻

- 兩相液冷

- 冷卻程度

- 組件級冷卻

- 伺服器/機架級冷卻

- 透過部署方法

- 超大規模/雲

- 公司

- 政府和研究機構(高效能運算)

- 邊緣人工智慧

- 按GPU功率密度

- 小於300瓦

- 300W~700W

- 700瓦或以上

- 按地區

- 中國

- 日本

- 韓國

- 印度

- 東南亞

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- CoolIT Systems Inc.

- Asetek A/S

- Vertiv Holdings Co.

- Schneider Electric SE

- Huawei Technologies Co., Ltd.

- Iceotope Technologies Limited

- Submer Technologies Sl.

- LiquidStack Holdings, Inc.

- ZutaCore Ltd.

- JetCool Technologies Inc.

- Boyd Corporation

- Fujitsu Limited

- Inspur Electronic Information Industry Co., Ltd.

- Mitsubishi Electric Corporation

- Sugon Information Industry Co., Ltd.

- Rittal GmbH & Co. KG

- Green Revolution Cooling Inc.

- Lenovo Group Limited

- Hewlett Packard Enterprise Company

- Alibaba Cloud(Alibaba Group Holding Limited)

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific graphics processing unit (GPU) liquid cooling market size is expected to grow from USD 3.79 billion in 2025 to USD 4.71 billion in 2026 and is forecast to reach USD 17.06 billion by 2031 at 29.37% CAGR over 2026-2031.

This report is Segmented by Cooling Type (Single-Phase Liquid Cooling, and Two-Phase Liquid Cooling), Cooling Level (Component-Level Cooling, and Server/Rack-Level Cooling), Deployment (Hyperscale/Cloud, Enterprise, Edge AI, and More), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Graphics Processing Unit (GPU) Liquid Cooling Market Trends and Insights

Mainstream AI-Led Hyperscale Expansions Drive Liquid-Cooling Adoption

Alibaba, Samsung SDS, OpenAI, and Global Switch are commissioning facilities where racks surpass 100 kilowatts, and GPUs draw up to 1,200 watts, a regime that renders air cooling uneconomic. Alibaba's Feitian platform already operates more than 100,000 GPUs in immersion tanks at PUE 1.09, cutting facility energy bills by roughly one-half. Samsung SDS broke ground on a 60 megawatt AI campus in Gumi in March 2026 that allocates KRW 427.3 billion (USD 320 million) to hybrid liquid infrastructure, underscoring long-term confidence in direct-to-chip systems. Global Switch Hong Kong added 30 megawatts of liquid-cooled capacity, while Nxera's DC Tuas in Singapore installed 58 megawatts of warm-water loops for sovereign AI workloads. The Asia-Pacific GPU liquid cooling market, therefore, follows hyperscalers' cadence: as model sizes inflate, cooling budgets shift from optimization to outright replacement of air systems.

Mandatory Energy-Efficiency Regulations Across East and South-East Asia

Japan's Ministry of Economy, Trade, and Industry requires PUE 1.4 by 2030 and PUE 1.3 for new builds from 2029, effectively outlawing traditional chillers in humid climates. China's energy labeling for chillers and its provincial power-quota regime likewise favor facilities that remove heat at the chip rather than at the room level. Lenovo's Neptune operates at 45 °C inlets, letting operators reuse waste heat, bypass chillers that consume up to 40% of facility power, and meet emerging carbon budgets. Singapore's Green Data Center Roadmap adds further pressure by tying new electricity allotments to demonstrated PUE improvements. Consequently, the Asia-Pacific GPU liquid cooling market benefits from a policy that makes efficiency a prerequisite for power and land access.

High Up-Front Capex and Retrofit Complexity for Brownfield Facilities

Direct-to-chip retrofits cost USD 500-USD 800 per kilowatt, more than double air-cooling upgrades, and demand phased cutovers that must preserve uptime. Operators often need structural reinforcement for pipes, electrical upgrades for pumps, and revised fire suppression, stretching payback to three to five years and deterring sites with rack densities below 50 kilowatts. Custom engineering erodes economies of scale, so many legacy owners wait until thermal ceilings force a wholesale move rather than incremental retrofits.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of Edge-AI Inference Nodes in 5G Networks

- Data-Center Land Constraints in Tier-1 Cities Boost Rack-Level Density

- Limited Skilled Workforce for Liquid-Cooling O&M Across Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase solutions accounted for 74.51% of the Asia-Pacific GPU liquid cooling market share in 2025, a position built on mature water loops that integrate with standard facility infrastructure. Lenovo Neptune and HPE ProLiant XD685 operate at 45 °C inlets, achieve a PUE of near 1.1, and provide a familiar maintenance model for staff already versed in chilled-water plants. Two-phase systems, although only 25.49% in 2025, are racing ahead at 32.17% CAGR as ZutaCore and Mitsubishi Heavy Industries prove rack-level partial PUE near 1.01 and remove facility water from the white space.

Chips such as the NVIDIA GB200 and AMD MI300X are pushing past the 1,000-watt mark. At this threshold, water's thermal headroom becomes limited, and the required flow rates demand significant pump power, making traditional cooling methods less efficient. This has led to increased interest in alternative cooling solutions, particularly two-phase cooling systems. Carrier's investment in ZutaCore, coupled with Trane's acquisition of LiquidStack, underscores a pivotal shift in the industry. These strategic moves by HVAC behemoths highlight their confidence in two-phase cooling roadmaps, which offer enhanced efficiency and scalability. As a result, the Asia-Pacific GPU liquid cooling market is expected to pivot towards dielectric fluids by 2028, marking a significant transformation in cooling technologies.

In 2025, component-level cold plates accounted for 55.72% of the Asia-Pacific GPU liquid cooling market, aligning with hyperscalers' focus on optimizing individual chips. These cold plates are designed to provide per-chip cooling, which is critical for managing the high heat output of GPUs in hyperscale environments. Supermicro's DLC-2, a prominent solution in this space, boasts the ability to extract 92% of server heat. This capability allows operators to seamlessly integrate GPU and CPU nodes without requiring extensive rack modifications. On the other hand, colocation operators are increasingly adopting rack-level coolant distribution units (CDUs) to streamline heat removal processes. These units treat heat removal as a shared service, offering a centralized approach to cooling that simplifies operations and enhances efficiency.

Rack-level solutions, such as ZutaCore's 2 megawatt end-of-row CDU and CoolIT's CHx500 stack, are becoming integral to retrofits by major players like Equinix and STT GDC. These solutions enable landlords to maintain control over critical aspects such as metering, maintenance, and service level agreements (SLAs). With rack-level offerings growing at a 31.60% CAGR, the market is witnessing a significant shift in cooling strategies. Tenants are moving away from individually plumbing racks and are instead subscribing to cooling as a service. This model aligns with the market's transition toward multi-tenant AI clusters, which demand scalable and efficient cooling solutions to support their high-performance computing needs.

List of Companies Covered in this Report:

- CoolIT Systems Inc.

- Asetek A/S

- Vertiv Holdings Co.

- Schneider Electric SE

- Huawei Technologies Co., Ltd.

- Iceotope Technologies Limited

- Submer Technologies Sl.

- LiquidStack Holdings, Inc.

- ZutaCore Ltd.

- JetCool Technologies Inc.

- Boyd Corporation

- Fujitsu Limited

- Inspur Electronic Information Industry Co., Ltd.

- Mitsubishi Electric Corporation

- Sugon Information Industry Co., Ltd.

- Rittal GmbH & Co. KG

- Green Revolution Cooling Inc.

- Lenovo Group Limited

- Hewlett Packard Enterprise Company

- Alibaba Cloud (Alibaba Group Holding Limited)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream AI-led Hyperscale Expansions Drive Liquid-Cooling Adoption

- 4.2.2 Mandatory Energy-Efficiency Regulations Across East and South-East Asia

- 4.2.3 Rapid Growth of Edge-AI Inference Nodes in 5G Networks

- 4.2.4 Data-Center Land Constraints in Tier-1 Cities Boost Rack-Level Density

- 4.2.5 Availability of Turn-key Liquid-Ready Colocation Capacity

- 4.2.6 Advancements in Coolant Chemistry Enabling Non-Conductive Two-Phase Designs

- 4.3 Market Restraints

- 4.3.1 High Up-Front Capex and Retrofit Complexity for Brownfield Facilities

- 4.3.2 Limited Skilled Workforce for Liquid-Cooling O&M Across Emerging Markets

- 4.3.3 Supply-Chain Bottlenecks in Precision Cold Plates and Quick Disconnects

- 4.3.4 PFAS Regulatory Uncertainty for Two-Phase Dielectric Fluids

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cooling Type

- 5.1.1 Single-Phase Liquid Cooling

- 5.1.2 Two-Phase Liquid Cooling

- 5.2 By Cooling Level

- 5.2.1 Component-Level Cooling

- 5.2.2 Server / Rack-Level Cooling

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.3.4 Edge AI

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

- 5.5 By Geography

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 South Korea

- 5.5.4 India

- 5.5.5 Southeast Asia

- 5.5.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CoolIT Systems Inc.

- 6.4.2 Asetek A/S

- 6.4.3 Vertiv Holdings Co.

- 6.4.4 Schneider Electric SE

- 6.4.5 Huawei Technologies Co., Ltd.

- 6.4.6 Iceotope Technologies Limited

- 6.4.7 Submer Technologies Sl.

- 6.4.8 LiquidStack Holdings, Inc.

- 6.4.9 ZutaCore Ltd.

- 6.4.10 JetCool Technologies Inc.

- 6.4.11 Boyd Corporation

- 6.4.12 Fujitsu Limited

- 6.4.13 Inspur Electronic Information Industry Co., Ltd.

- 6.4.14 Mitsubishi Electric Corporation

- 6.4.15 Sugon Information Industry Co., Ltd.

- 6.4.16 Rittal GmbH & Co. KG

- 6.4.17 Green Revolution Cooling Inc.

- 6.4.18 Lenovo Group Limited

- 6.4.19 Hewlett Packard Enterprise Company

- 6.4.20 Alibaba Cloud (Alibaba Group Holding Limited)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

亞太地區GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國GPU液冷市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

亞太地區GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國GPU液冷市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 2026-2030年全球人工智慧資料中心液冷市場

2026-2030年全球人工智慧資料中心液冷市場 人工智慧資料中心液冷市場:2034 年預測-按冷卻方式、組件、冷卻劑類型、技術、最終用戶和地區分類的全球分析

人工智慧資料中心液冷市場:2034 年預測-按冷卻方式、組件、冷卻劑類型、技術、最終用戶和地區分類的全球分析 資料中心液冷市場:依冷卻技術、組件、液體類型、基礎架構層、資料中心類型、最終用戶產業和資料中心規模分類-2026年至2032年全球市場預測

資料中心液冷市場:依冷卻技術、組件、液體類型、基礎架構層、資料中心類型、最終用戶產業和資料中心規模分類-2026年至2032年全球市場預測 資料中心液冷市場報告:按組件、資料中心類型、最終用途、應用和地區分類(2026-2034 年)

資料中心液冷市場報告:按組件、資料中心類型、最終用途、應用和地區分類(2026-2034 年) 全球資料中心液冷市場:按組件、最終用戶、冷卻介質、資料中心類型、冷卻類型、企業和地區分類 - 預測(至 2033 年)

全球資料中心液冷市場:按組件、最終用戶、冷卻介質、資料中心類型、冷卻類型、企業和地區分類 - 預測(至 2033 年) 全球資料中心液冷閥市場:按閥門類型、冷卻類型、資料中心類型和地區分類 - 預測(至 2032 年)

全球資料中心液冷閥市場:按閥門類型、冷卻類型、資料中心類型和地區分類 - 預測(至 2032 年)