|

市場調查報告書

商品編碼

2063860

中國GPU液冷市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)China GPU Liquid Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

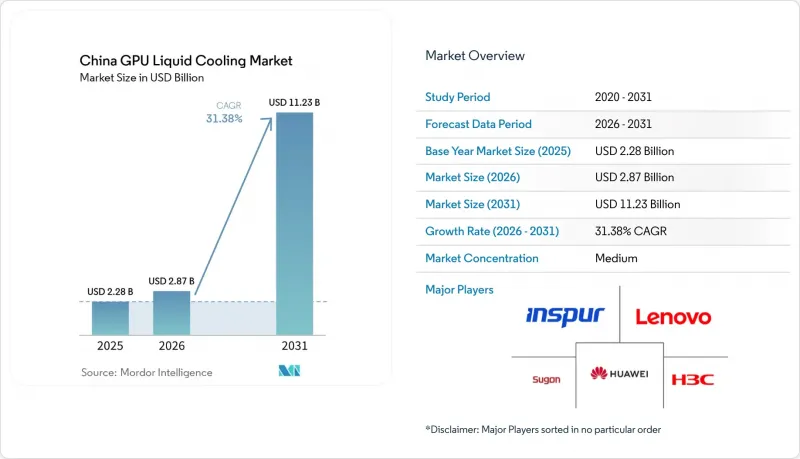

據 Mordor Intelligence 稱,2025 年中國 GPU 液冷市場規模為 22.8 億美元,預計到 2031 年將從 2026 年的 28.7 億美元成長至 112.3 億美元,預測期(2026-2031 年)複合年成長率為 31.38%。

本報告按冷卻方式(單相液冷和兩相液冷)、冷卻等級(組件級冷卻和伺服器/機架級冷卻)、部署方式(超大規模/雲端、企業級、政府/科研高效能運算、邊緣人工智慧)、GPU功率密度(低於300W、300W-700W、高於700W)以及地區進行細分。市場預測以美元計價。

中國GPU液冷市場的趨勢與洞察

中國超大規模資料中心人工智慧訓練工作負載的採用率快速成長

中國超大規模資料中心業者資料中心營運商正將叢集從數十千兆次浮點運算(petaflops)擴展到數百千兆次浮點運算(petaflops),而液冷技術即使在利用率超過 80% 的情況下也能穩定 GPU 結溫。阿里雲三年基礎建設計劃投資 527 億美元,將冷板機架置於下一代語言模型訓練的核心位置,以防止風扇功耗降低整體 PUE 值。百度正在維修現有設施,以應對熱負荷成長四倍的情況。同時,騰訊已將其人工智慧領域的投資翻番,計劃到 2026 年投入 50 億美元,並安裝可為每個機架維持 100-200kW 功率的浸沒式冷卻槽。對國產人工智慧模型的持續需求使得 GPU 利用率維持在高位,而只有液冷技術才能滿足這項需求。

隨著 GPU 功率密度超過 700W,液冷散熱變得不可或缺。

NVIDIA 的 Vera Rubin 系列顯示卡將於 2026 年下半年上市,標配液冷散熱,單板功耗超過 1000W,旗艦 AI 訓練機架無需再配備風冷系統。台達電子已推出一款 1.5MW 的冷卻液分配單元,可用於 15 個 100kW 的 NVL72 機架;華為的液冷 800G 交換器則能有效防止網路交換矩陣元件過熱降頻。從經濟角度來看,水冷散熱也具有顯著優勢,因為它能提高面積,並降低空調設備的成本。

與從空冷系統維修相比,初始資本支出(CAPEX)更高。

冷板組件、快速連接器和冷配電單元 (CDU) 會使初始預算增加 40% 至 60%,這對每機架閾值低於 50 kW 的營運商來說構成了一道障礙。組件成本集中在金屬加工和精密加工領域,而這些領域的規模經濟效應尚不成熟。然而,根據英特爾的總體擁有成本 (TCO) 比較研究,一旦每機架的功耗超過 100 kW,由於空調成本降低和空間利用率提高,投資可在五年內收回。像美的這樣的製造商正在透過投資 1.38 億美元來建造大批量 CDU 工廠來降低這一障礙,目標是在 2028 年前將單位成本降低高達 30%。

細分市場分析

預計到2025年,單相架構將在中國GPU液冷市場佔據73.20%的最大市場佔有率,這主要得益於其與標準42U機架的兼容性以及相對便捷的維護。Delta的4RU和6RU機架內CDU透過快拆軟管連接至支援Neptune技術的聯想伺服器,無需改動現有管路即可為H100和H200 GPU提供冷卻。在大多數業者逐步淘汰機櫃、轉而採用液冷方案的維修項目中,這一細分市場仍佔據主導地位。相較之下,在兆瓦級AI訓練中心,雙相浸沒式系統已成為首選。曙光科技的C8000 V3.0水箱每個機架可實現900kW的冷卻能力,將PUE值降低至1.04,同時釋放占地面積用於建構更高密度的網路架構。由於 Vera Rubin 的單機功率超過 1 kW,儘管流體成本較高,但採購仍將傾向於 700 W 以上功率密度的兩相系統。 ODM 和超大規模企業在 2026 年下半年先導計畫將決定浸沒式冷卻技術在中國整個 GPU 液冷市場新建設專案中取代冷板冷卻技術的步伐。

根據市場趨勢,到2026年,中國新建資料中心中約有22%將運作某種形式的液冷技術,其中兩相浸沒式液冷僅佔4%。這種差距主要歸因於市場對液冷技術的接受度較低以及含氟冷卻液成本較高,但超大規模資料中心業者高度重視浸沒式液冷的優勢,因為它無需維護冷板。英特爾和阿里雲已在100kW機架中驗證了單相液冷浸沒式液冷的有效性,其PUE值達到1.09,這代表了一種介於冷板和液冷之間的折中方案。隨著GPU功耗的增加,兩相系統將實現最快成長,並在未來中國GPU液冷市場中構成比更重要的地位。

到2025年,組件級冷卻將佔總支出的55.45%。這主要是因為GPU廠商提供的參考設計都整合了冷板。節點級升級簡化了企業的計費方式,並允許營運商僅針對關鍵任務機架進行升級。銀輪股份有限公司等一級汽車熱交換器製造商透過改進微通道板並實現98%的批次間一致性,增強了超大規模企業的信心。然而,整合歧管和線上CDU的機架級系統正以31.76%的複合年成長率成長,並隨著超大規模企業追求150kW及以上機櫃的需求,不斷擴大其在中國GPU液冷市場的佔有率。 XFusion的FusionPoD消除了熱通道,在144個CPU和GPU的容量下實現了1.06的pPUE值。此外,H3C的800G液冷交換機將網路整合到同一流體迴路中,消除了空氣間隙。

機架式解決方案整合了管道、洩漏偵測和監控功能,從而縮短了資料中心機房的施工時間。這些一體化機架通常採用ISO貨櫃運輸,可直接用起重機吊到區域人工智慧中心尚未完工的建築物中,進一步縮短了計算投入使用的時間。對於在北京、上海等城市地區維修託管設施的營運商而言,組件式冷板仍然是首選,因為它們無需切割混凝土即可安裝新的設備迴路。因此,這兩種解決方案將並存,但到2031年,最大的營收成長點將出現在機架式解決方案上,這將成為推動中國GPU液冷市場規模擴大的主要動力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 在中國,人工智慧訓練工作負載在超大規模資料中心的應用正在快速成長。

- 政府獎勵節能型資料中心冷卻

- 隨著 GPU 功率密度超過 700W,水冷散熱變得不可或缺。

- 依照「東數據西計算」方針,快速發展底層人工智慧計算叢集。

- ODM 伺服器製造商越來越傾向於採用身臨其境型式 GPU 參考設計。

- 對先進GPU的出口限制正加速國內水冷加速器的研發;

- 市場限制因素

- 與空冷系統維修相比,初始資本投入較高。

- 組件級冷板解決方案標準化的局限性

- 政府工作負載中水冷雲部署需要經過嚴格的網路安全核准流程。

- 地緣政治緊張局勢下供應鏈對進口介電液體的依賴

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 透過冷卻法

- 單相液體冷卻

- 兩相液冷

- 透過冷卻水平

- 組件級冷卻

- 伺服器/機架級冷卻

- 不同的發展

- 超大規模/雲

- 公司

- 政府和研究機構(高效能運算)

- 邊緣人工智慧

- 按GPU功率密度

- 小於300瓦

- 300W~700W

- 超過700瓦

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Inspur Group

- Lenovo Group Limited

- Huawei Technologies Co., Ltd.

- Sugon Information Industry Co., Ltd.

- H3C Technologies Co., Ltd.

- Tencent Holdings Ltd.

- Alibaba Group Holding Limited

- Baidu, Inc.

- Giga Computing Technology Co., Ltd.

- ASUSTeK Computer Inc.

- Super Micro Computer, Inc.

- NVIDIA Corporation

- CoolIT Systems Inc.

- Asetek A/S

- LiquidStack Holding Limited

- Submer Technologies SL

- Envicool Technology Co., Ltd.

- Delta Electronics, Inc.

- Phytium Technology Co., Ltd.

- China Mobile Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the china gPU liquid cooling market size was valued at USD 2.28 billion in 2025 and estimated to grow from USD 2.87 billion in 2026 to reach USD 11.23 billion by 2031, at a CAGR of 31.38% during the forecast period (2026-2031).

This report is Segmented by Cooling Type (Single-Phase Liquid Cooling, and Two-Phase Liquid Cooling), Cooling Level (Component-Level Cooling, and Server/Rack-Level Cooling), Deployment (Hyperscale/Cloud, Enterprise, Government and Research HPC, and Edge AI), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

China GPU Liquid Cooling Market Trends and Insights

Surging Adoption of AI Training Workloads in Chinese Hyperscale Data Centers

Chinese hyperscalers are scaling clusters from tens to hundreds of petaflops, and liquid cooling keeps junction temperatures stable even when utilization exceeds 80%. Alibaba Cloud's USD 52.7 billion, three-year infrastructure plan places cold-plate racks at the center of next-generation language-model training, preventing fan energy from eroding overall PUE. Baidu is retrofitting legacy facilities after thermal loads quadrupled, while Tencent doubled AI capex to USD 5 billion for 2026, deploying immersion tanks that sustain 100-200 kW per rack. Sustained demand for sovereign AI models ensures continuous GPU utilization that only liquid cooling can support.

Rising GPU Power Densities Beyond 700 W Necessitating Liquid Cooling

NVIDIA's Vera Rubin family arrives in H2 2026 with liquid cooling as standard and board power at or above 1,000 W, eliminating air systems for flagship AI training racks. Delta Electronics already offers 1.5 MW coolant distribution units sized for fifteen 100 kW NVL72 racks, while Huawei's liquid-cooled 800 G switches prevent thermal throttling in fabric elements. Economics also favor liquid cooling-higher density allows smaller footprints and lowers HVAC overhead.

High Upfront CAPEX Compared With Air Cooling Retrofits

Cold-plate assemblies, quick connectors, and CDUs can lift initial budgets 40-60%, discouraging operators below the 50 kW per rack threshold. Component costs are concentrated in metallurgy and precision machining, areas where scale economies are still maturing. Intel's comparative TCO study, however, shows breakeven in under five years once racks top 100 kW, thanks to lower HVAC bills and higher space utilization. Manufacturers such as Midea are investing USD 138 million in high-volume CDU plants to reduce unit pricing by up to 30% before 2028, easing this barrier.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Build-Out of Provincial AI Computing Clusters Aligned With "East Data West Compute

- Export Restrictions on Advanced GPUs Accelerating Domestic Liquid-Cooled Accelerator R&D

- Supply Chain Dependency on Imported Dielectric Fluids Amid Geopolitical Tensions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase architectures captured the largest China GPU liquid cooling market share at 73.20% in 2025, buoyed by compatibility with standard 42U racks and relatively simple maintenance. Delta's 4 RU and 6 RU in-rack CDUs connect quick-release hoses to Neptune-enabled Lenovo servers that cool H100 and H200 GPUs without plumbing changes to facility loops. This segment still wins most retrofit projects where operators migrate cabinets gradually to liquid. In contrast, two-phase immersion is already the preferred choice for megawatt-class AI training halls: Sugon's C8000 V3.0 tanks achieve 900 kW per rack, shaving PUE to 1.04 and freeing floor space for denser network fabrics. Because power envelopes for Vera Rubin exceed 1 kW per device, the above-700 W density band will tilt procurement toward two-phase systems despite their higher fluid budgets. ODM and hyperscale pilots in H2 2026 will determine the pace at which immersion replaces cold plates for greenfield builds across the China GPU liquid cooling market.

Adoption patterns indicate that roughly 22% of new Chinese data centers commissioned in 2026 integrated some form of liquid cooling, of which two-phase immersion accounted for only 4%. The gap arises from training inertia and the higher cost of fluorinated fluids, yet hyperscalers value immersion's ability to eliminate cold plates from maintenance schedules. Intel and Alibaba Cloud validated single-phase immersion to 100 kW racks at 1.09 PUE, demonstrating a mid-step that could blur boundaries between cold-plate and immersion approaches. As GPU wattage climbs, two-phase systems will absorb the fastest growth slice, reinforcing their role in the future mix of the China GPU liquid cooling market.

Component-level cooling held 55.45% of 2025 spending, mainly because GPU vendors ship reference designs with integrated cold plates. Upgrades on a node-by-node basis simplify billing for enterprises and allow operators to target only mission-critical racks. Tier-1 automotive heat-exchange companies like Yinlun Co. have adapted microchannel plates achieving 98% batch-to-batch consistency, boosting trust among hyperscale buyers. However, rack-level systems, featuring integrated manifolds and in-line CDUs, are growing at a 31.76% CAGR and gaining share of the China GPU liquid cooling market size as hyperscalers chase 150 kW-plus cabinets. XFusion's FusionPoD eliminates hot aisles, delivering pPUE of 1.06 across 144 CPUs plus GPUs, and H3C's 800 G liquid-cooled switch ties the network into the same fluid loop, removing air gaps.

Rack solutions bundle plumbing, leak detection, and monitoring, which lowers engineering time on the data-hall floor. These all-inclusive racks, often shipped in ISO containers, can be craned into bare shells at provincial AI hubs, shortening time-to-compute. For operators retrofitting downtown Beijing or Shanghai colocation, component cold plates remain favored because they avoid cutting concrete for new facility loops. Therefore, both levels will coexist; yet the strongest revenue delta to 2031 sits with racks, adding scale to the China GPU liquid cooling market size.

List of Companies Covered in this Report:

- Inspur Group

- Lenovo Group Limited

- Huawei Technologies Co., Ltd.

- Sugon Information Industry Co., Ltd.

- H3C Technologies Co., Ltd.

- Tencent Holdings Ltd.

- Alibaba Group Holding Limited

- Baidu, Inc.

- Giga Computing Technology Co., Ltd.

- ASUSTeK Computer Inc.

- Super Micro Computer, Inc.

- NVIDIA Corporation

- CoolIT Systems Inc.

- Asetek A/S

- LiquidStack Holding Limited

- Submer Technologies SL

- Envicool Technology Co., Ltd.

- Delta Electronics, Inc.

- Phytium Technology Co., Ltd.

- China Mobile Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of AI Training Workloads in Chinese Hyperscale Data Centers

- 4.2.2 Government Incentives for Energy Efficient Data Center Cooling

- 4.2.3 Rising GPU Power Densities Beyond 700W Necessitating Liquid Cooling

- 4.2.4 Rapid Build-Out of Provincial AI Computing Clusters Aligned With "East Data West Compute" Program

- 4.2.5 Growing Preference for Immersion-Ready GPU Reference Designs by ODM Server Makers

- 4.2.6 Export Restrictions on Advanced GPUs Accelerating Domestic Liquid-Cooled Accelerator R&D

- 4.3 Market Restraints

- 4.3.1 High Upfront CAPEX Compared With Air Cooling Retrofits

- 4.3.2 Limited Standardization Across Component-Level Cold Plate Solutions

- 4.3.3 Stringent Cybersecurity Approval Processes for Liquid-Cooled Cloud Deployments in Government Workloads

- 4.3.4 Supply Chain Dependency on Imported Dielectric Fluids Amid Geopolitical Tensions

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Bargaining Power of Buyers

- 4.7.5 Threat of Substitutes

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cooling Type

- 5.1.1 Single-Phase Liquid Cooling

- 5.1.2 Two-Phase Liquid Cooling

- 5.2 By Cooling Level

- 5.2.1 Component-Level Cooling

- 5.2.2 Server / Rack-Level Cooling

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.3.4 Edge AI

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Inspur Group

- 6.4.2 Lenovo Group Limited

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Sugon Information Industry Co., Ltd.

- 6.4.5 H3C Technologies Co., Ltd.

- 6.4.6 Tencent Holdings Ltd.

- 6.4.7 Alibaba Group Holding Limited

- 6.4.8 Baidu, Inc.

- 6.4.9 Giga Computing Technology Co., Ltd.

- 6.4.10 ASUSTeK Computer Inc.

- 6.4.11 Super Micro Computer, Inc.

- 6.4.12 NVIDIA Corporation

- 6.4.13 CoolIT Systems Inc.

- 6.4.14 Asetek A/S

- 6.4.15 LiquidStack Holding Limited

- 6.4.16 Submer Technologies SL

- 6.4.17 Envicool Technology Co., Ltd.

- 6.4.18 Delta Electronics, Inc.

- 6.4.19 Phytium Technology Co., Ltd.

- 6.4.20 China Mobile Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 Whitespace and Unmet Need Assessment

亞太地區GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區液冷GPU(圖形處理器):市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

亞太地區GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲GPU散熱解決方案:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區液冷GPU(圖形處理器):市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 2026-2030年全球人工智慧資料中心液冷市場

2026-2030年全球人工智慧資料中心液冷市場 人工智慧資料中心液冷市場:2034 年預測-按冷卻方式、組件、冷卻劑類型、技術、最終用戶和地區分類的全球分析

人工智慧資料中心液冷市場:2034 年預測-按冷卻方式、組件、冷卻劑類型、技術、最終用戶和地區分類的全球分析 資料中心液冷市場:依冷卻技術、組件、液體類型、基礎架構層、資料中心類型、最終用戶產業和資料中心規模分類-2026年至2032年全球市場預測

資料中心液冷市場:依冷卻技術、組件、液體類型、基礎架構層、資料中心類型、最終用戶產業和資料中心規模分類-2026年至2032年全球市場預測 資料中心液冷市場報告:按組件、資料中心類型、最終用途、應用和地區分類(2026-2034 年)

資料中心液冷市場報告:按組件、資料中心類型、最終用途、應用和地區分類(2026-2034 年) 全球資料中心液冷市場:按組件、最終用戶、冷卻介質、資料中心類型、冷卻類型、企業和地區分類 - 預測(至 2033 年)

全球資料中心液冷市場:按組件、最終用戶、冷卻介質、資料中心類型、冷卻類型、企業和地區分類 - 預測(至 2033 年) 全球資料中心液冷閥市場:按閥門類型、冷卻類型、資料中心類型和地區分類 - 預測(至 2032 年)

全球資料中心液冷閥市場:按閥門類型、冷卻類型、資料中心類型和地區分類 - 預測(至 2032 年)