|

市場調查報告書

商品編碼

2063848

亞太地區LED外延片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Asia-Pacific LED Epitaxial Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

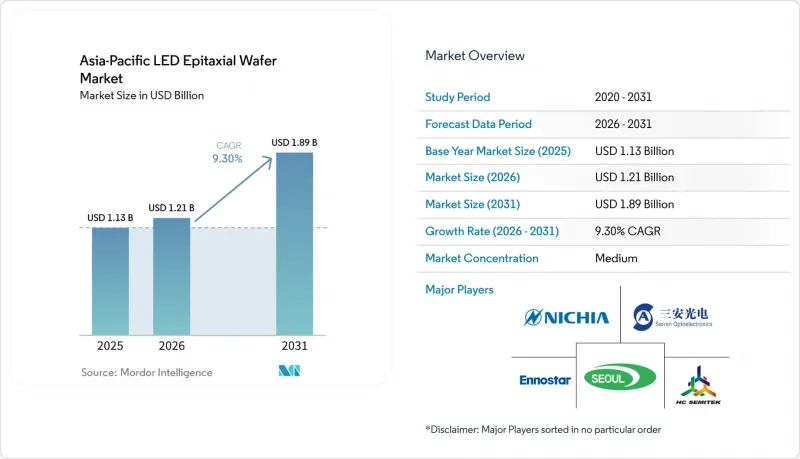

根據 Mordor Intelligence 預測,亞太地區 LED 外延晶片市場規模將從 2025 年的 11.3 億美元成長到 2026 年的 12.1 億美元,到 2031 年將達到 18.9 億美元,2026 年至 2031 年的複合年成長率為 9.3%。

本報告依材料系統(GaN基外延晶片、AlInGaP基外延晶片等)、基板類型(藍寶石、矽、碳化矽(SiC)、砷化鎵(GaAs))、晶片直徑(100mm及以下、150mm、200mm以上)及應用(照明、汽車照明、通用顯示器和背光等)進行通用分類。市場預測以美元(USD)計價。

亞太地區LED外延晶片市場的趨勢與洞察。

MicroLED和MiniLED應用範圍的擴大

預計到2026年,主動式矩陣Mini-LED電視將佔全球出貨量的10%,這要求晶圓製造商在整個6吋基板上實現小於±2nm的波長分檔,以避免在HDR環境下出現色彩偏移。一級汽車製造商已開始將Mini-LED背光整合到儀錶群,推動了對低缺陷GaN外延的需求。三星顯示器和LG顯示器正在投資建造用於穿戴式裝置的Micro-LED試點生產線。與傳統LED相比,該領域每平方公尺面板所需的晶圓面積高達10倍,導致所需數量大幅增加。小米的163吋原型機展示了其可擴展性,前提是量產良率必須保持在1ppm以下。這些項目將推高平均售價,因為任何效能波動都會導致下游轉移過程中的返工。

高亮度汽車頭燈的需求增加

聯合國歐洲經濟委員會 (UNECE) 和修訂後的中國 GB 標準現已允許使用光通量超過 3000 流明且能抑制眩光的自我調整驅動光束模組。日亞化學工業株式會社 (Nichia Corporation) 的 DominoPLS 裝置每個模組整合 16 個可尋址段,並符合 UNECE 和 GB 的光度測試要求。印度的 AIS-199 標準草案符合全球標準,並為矩陣式頭燈開闢了新的區域發展道路。汽車原始設備製造商 (OEM) 要求峰值波長為 450 nm ± 5 nm,位錯密度小於 1 × 10^8 cm⁻²,這迫使外延製造商轉向使用更大尺寸的藍寶石或碳化矽 (SiC)基板以及先進的緩衝層。

藍寶石基板供應鏈的波動

預計到2026年,中國將佔全球藍寶石晶棒供應量的40%以上,但任何出口限制或物流中斷都將對亞太地區的晶圓廠產生直接影響。當智慧型手機相機蓋板的需求與顯示器需求高峰期重疊時,前置作業時間會更長,4吋晶圓的價格在每片15美元到25美元之間波動。印度的生產連結獎勵計畫(PLI)規定,三年內基板的在地採購率必須達到25%,但由於印度國內沒有藍寶石錠生產商,晶圓廠被迫簽訂多年進口契約,這削弱了補貼帶來的效益。

細分市場分析

2025年,氮化鎵(GaN)晶圓出貨量佔比達68.40%,主要成長動力來自通用照明、汽車和顯示器背光等領域。隨著各地政府採用無汞紫外線C波段(UV-C)消毒技術,亞太地區AlGaN LED外延晶圓市場預計到2031年將以12.87%的複合年成長率成長。日亞化學工業株式會社(Nichia Corporation)的280奈米裝置實現了7.4%的電光轉換效率,展現了其商業性可行性,並有助於供水事業採購。

目前,通用型GaN(用於燈泡)和滿足波長均勻性±2 nm、缺陷密度小於1 cm²等規格的高階GaN或AlGaN晶圓的價格呈現兩極化。 AlGaN中鋁含量的增加提高了開裂風險,促使製造商嘗試使用氮化鋁緩衝層和脈衝橫向生長方法。因此,材料選擇取決於產能、外延應力和日益成長的紫外線需求(尤其是在醫療滅菌領域)之間的平衡。

由於藍寶石具有良好的晶格匹配性和成熟的反應釜化學工藝,預計到2025年,其市場佔有率將達到55.67%。矽基基板的複合年成長率(CAGR)為13.58%,這得益於200毫米晶圓的普及和半導體級測量技術的進步,從而降低了單晶片成本。 Innoscience公司在8吋GaN-on-SiIC晶圓上實現了97%的良率,這得益於其採用了梯度AlGaN緩衝層和即時應力監測技術。

碳化矽由於成本高出3-5倍,仍然是一種小眾材料,但它為高電流LED提供了無與倫比的導熱性能。砷化鎵用於紅色和琥珀色AlInGaP,但其直徑有極限。因此,亞太地區LED外延晶片市場的佔有率平衡取決於顯示器和汽車行業的客戶是優先考慮成本還是散熱裕度。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府對該地區半導體製造業的補貼

- 微型LED和迷你LED的應用範圍不斷擴大

- 對高亮度汽車頭燈的需求不斷成長

- 都市區智慧照明的快速部署

- 提高氮化鎵/碳化矽晶片的良率

- 增加對UV-C LED殺菌系統的投資

- 市場限制因素

- MOCVD設備需要高額資本投入

- 藍寶石基板供應鏈波動

- 大直徑矽晶圓熱失配的挑戰

- 新創公司知識產權許可的障礙

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依材料體系

- 基於氮化鎵的外延晶片

- AlInGaP外延晶片

- AlGaN外延晶片

- 按基板類型

- 藍寶石

- 矽

- 碳化矽(SiC)

- 砷化鎵(GaAs)

- 依晶圓直徑

- 100毫米或更小

- 150 mm

- 200毫米或以上

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 紫外線消毒

- 工業和專用照明

- 國家

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Vendor Market Positioning

- 公司簡介

- Nichia Corporation

- Epistar Corporation

- Sanan Optoelectronics Co., Ltd.

- Osram Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Wolfspeed, Inc.

- HC Semitek Corporation

- Genesis Photonics Inc.

- Opto Tech Corporation

- Bridgelux, Inc.

- Lumileds Holding BV

- Lextar Electronics Corporation

- Showa Denko KK

- Unistars Corporation

- Everlight Electronics Co., Ltd.

- Tyntek Corporation

- Epileds Technologies Inc.

- Focus Lightings Tech Co., Ltd.

- Sino-American Silicon Products Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific lED epitaxial wafer market size is expected to grow from USD 1.13 billion in 2025 to USD 1.21 billion in 2026 and is forecast to reach USD 1.89 billion by 2031 at 9.3% CAGR over 2026-2031.

This report is Segmented by Material System (GaN-Based Epitaxial Wafers, Alingap Epitaxial Wafers, and More), Substrate Type (Sapphire, Silicon, Silicon Carbide (SiC), Gallium Arsenide (GaAs)), Wafer Diameter (Up To 100 Mm, 150 Mm, 200 Mm and Above), and Application (General Lighting, Automotive Lighting, Displays and Backlighting and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific LED Epitaxial Wafer Market Trends and Insights

Expansion of Micro-LED and Mini-LED Applications

Active-matrix Mini-LED televisions reached 10% penetration in global shipments in 2026, compelling wafer makers to achieve wavelength binning tighter than +-2 nm across 6-inch substrates to avoid color-shift artifacts under HDR conditions. Tier-1 automakers have begun equipping high-end instrument clusters with Mini-LED backlights, reinforcing demand for low-defect GaN epitaxy. Samsung Display and LG Display are funding Micro-LED pilot lines for wearables, where each square meter of panel uses up to ten-times more wafer area than conventional LEDs, multiplying volume requirements. Xiaomi's 163-inch prototype validated scalability, contingent on mass-transfer yields below one-ppm defect rates. These projects elevate average selling prices because every performance drift incurs rework in downstream transfer processes.

Rising Demand for High-Brightness Automotive Headlamps

UNECE and updated Chinese GB regulations now allow adaptive-driving-beam modules that exceed 3 000 lumens while controlling glare. Nichia's DominoPLS devices integrate 16 addressable segments per module, meeting both UNECE and GB photometric test requirements. India's draft AIS-199 standard aligns with global norms, opening a new regional route for matrix headlamps. Automotive OEMs stipulate peak wavelengths at 450 nm +-5 nm and dislocation densities below 1 X 10^8 cm-2, pushing epitaxial houses toward larger sapphire or SiC substrates with advanced buffer stacks.

Supply Chain Volatility of Sapphire Substrates

China will supply more than 40% of global sapphire ingots by 2026, but any export controls or logistical disruptions will instantly reverberate across Asia-Pacific fabs. Lead times stretch when smartphone camera-cover demand overlaps display peaks, sending 4-inch wafer prices swinging between USD 15 and USD 25 apiece. India's PLI rules require 25% local substrate value within three years, yet no domestic ingot producer exists, forcing fabs to lock multi-year import contracts that dilute subsidy benefits.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Urban Smart-Lighting Initiatives

- Government Subsidies for Regional Semiconductor Manufacturing

- High Capital Expenditure for MOCVD Tools

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

GaN wafers dominated 68.40% of shipments in 2025 on the back of general lighting, automotive, and display backlighting. The Asia-Pacific LED Epitaxial Wafer market size for AlGaN is projected to expand at 12.87% CAGR through 2031 as municipalities adopt mercury-free UV-C disinfection. Nichia's 280 nm devices, delivering 7.4% wall-plug efficiency, validated commercial viability and sparked procurement from water-utility operators.

Pricing now bifurcates between commoditized GaN for bulbs and premium GaN or AlGaN wafers meeting +-2 nm wavelength uniformity and sub-1 cm-2 defect specs. Elevated aluminum fractions in AlGaN raise cracking risks, so producers are experimenting with aluminum-nitride buffer layers and pulsed lateral overgrowth. Material selection thus hinges on balancing throughput, epitaxial stress, and emerging UV demand, especially for healthcare sterilization.

Sapphire held 55.67% share in 2025 because of favorable lattice matching and mature reactor chemistries. Silicon substrates, growing at a 13.58% CAGR, leverage 200 mm wafer availability and semiconductor-grade metrology to reduce the cost per die. Innoscience demonstrated 97% yield on 8-inch GaN-on-silicon wafers after implementing graded AlGaN buffers and real-time stress monitoring.

Silicon carbide remains a niche due to a 3-5X cost premium, yet offers unmatched thermal conductivity for high-current LEDs. Gallium-arsenide serves red-amber AlInGaP but is diameter-limited. The Asia-Pacific LED Epitaxial Wafer market share balance, therefore, depends on whether display and automotive clients prioritize cost or thermal headroom.

List of Companies Covered in this Report:

- Nichia Corporation

- Epistar Corporation

- Sanan Optoelectronics Co., Ltd.

- Osram Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Wolfspeed, Inc.

- HC Semitek Corporation

- Genesis Photonics Inc.

- Opto Tech Corporation

- Bridgelux, Inc.

- Lumileds Holding B.V.

- Lextar Electronics Corporation

- Showa Denko K.K.

- Unistars Corporation

- Everlight Electronics Co., Ltd.

- Tyntek Corporation

- Epileds Technologies Inc.

- Focus Lightings Tech Co., Ltd.

- Sino-American Silicon Products Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Subsidies for Regional Semiconductor Manufacturing

- 4.2.2 Expansion of Micro-LED and Mini-LED Applications

- 4.2.3 Rising Demand for High-Brightness Automotive Headlamps

- 4.2.4 Rapid Urban Smart-Lighting Initiatives

- 4.2.5 Advancements in GaN-on-SiC Wafer Yields

- 4.2.6 Growing Investments in UV-C LED Sterilization Systems

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure for MOCVD Tools

- 4.3.2 Supply Chain Volatility of Sapphire Substrates

- 4.3.3 Thermal Mismatch Challenges in Large-Diameter Silicon Wafers

- 4.3.4 Intellectual-Property (IP) Licensing Barriers for Start-ups

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material System

- 5.1.1 GaN-based Epitaxial Wafers

- 5.1.2 AlInGaP Epitaxial Wafers

- 5.1.3 AlGaN Epitaxial Wafers

- 5.2 By Substrate Type

- 5.2.1 Sapphire

- 5.2.2 Silicon

- 5.2.3 Silicon Carbide (SiC)

- 5.2.4 Gallium Arsenide (GaAs)

- 5.3 By Wafer Diameter

- 5.3.1 Upto 100 mm

- 5.3.2 150 mm

- 5.3.3 200 mm and Above

- 5.4 By Application

- 5.4.1 General Lighting

- 5.4.2 Automotive Lighting

- 5.4.3 Displays and Backlighting

- 5.4.4 UV Sterilization

- 5.4.5 Industrial and Specialty Lighting

- 5.5 By Country

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 South Korea

- 5.5.5 Rest of the Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Market Positioning

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Epistar Corporation

- 6.4.3 Sanan Optoelectronics Co., Ltd.

- 6.4.4 Osram Opto Semiconductors GmbH

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Wolfspeed, Inc.

- 6.4.7 HC Semitek Corporation

- 6.4.8 Genesis Photonics Inc.

- 6.4.9 Opto Tech Corporation

- 6.4.10 Bridgelux, Inc.

- 6.4.11 Lumileds Holding B.V.

- 6.4.12 Lextar Electronics Corporation

- 6.4.13 Showa Denko K.K.

- 6.4.14 Unistars Corporation

- 6.4.15 Everlight Electronics Co., Ltd.

- 6.4.16 Tyntek Corporation

- 6.4.17 Epileds Technologies Inc.

- 6.4.18 Focus Lightings Tech Co., Ltd.

- 6.4.19 Sino-American Silicon Products Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中國LED外延片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

中國LED外延片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 氮化鎵裝置市場預測至2034年-按產品類型、元件、電壓範圍、最終用戶和地區分類的全球分析氮化鎵基LED外延片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)氮化鎵矽基(GaN-on-Si)LED外延片:市佔率分析、產業趨勢與統計數據以及成長預測(2026-2031年)

氮化鎵裝置市場預測至2034年-按產品類型、元件、電壓範圍、最終用戶和地區分類的全球分析氮化鎵基LED外延片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)氮化鎵矽基(GaN-on-Si)LED外延片:市佔率分析、產業趨勢與統計數據以及成長預測(2026-2031年) 2026-2034年全球氮化鎵工業裝置市場規模、佔有率、趨勢與成長分析報告

2026-2034年全球氮化鎵工業裝置市場規模、佔有率、趨勢與成長分析報告 氮化鎵半導體裝置市場:2026-2032年全球市場預測(按裝置類型、晶圓尺寸、應用和最終用途產業分類)矽基基板的氮化鎵(GaN)晶圓:市佔率分析、產業趨勢與統計、成長預測(2026-2031)氮化鎵雷達系統市場:按類型、組件、頻寬、組件範圍和應用分類-2026年至2032年全球預測

氮化鎵半導體裝置市場:2026-2032年全球市場預測(按裝置類型、晶圓尺寸、應用和最終用途產業分類)矽基基板的氮化鎵(GaN)晶圓:市佔率分析、產業趨勢與統計、成長預測(2026-2031)氮化鎵雷達系統市場:按類型、組件、頻寬、組件範圍和應用分類-2026年至2032年全球預測 氮化鎵半導體市場:依產品、組件、晶圓尺寸、最終用途、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測

氮化鎵半導體市場:依產品、組件、晶圓尺寸、最終用途、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測 高頻氮化鎵半導體市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、材料類型、裝置、部署類型、最終用戶和功能分類

高頻氮化鎵半導體市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、材料類型、裝置、部署類型、最終用戶和功能分類