|

市場調查報告書

商品編碼

2063458

南美洲合約物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)South America Contract Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

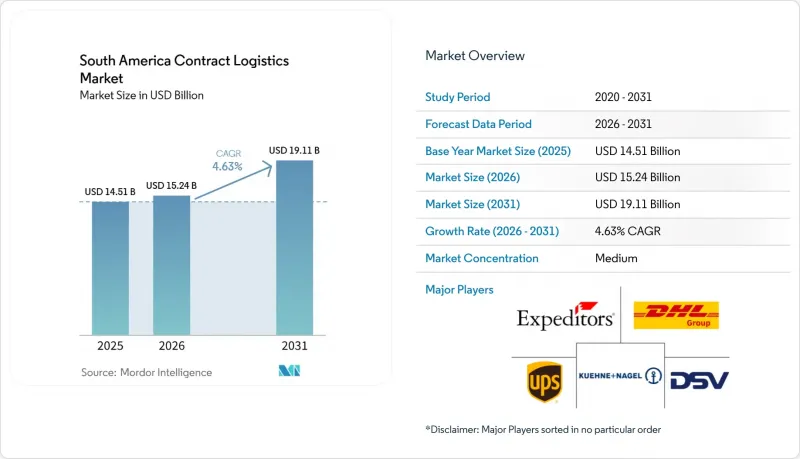

據 Mordor Intelligence 稱,2025 年南美合約物流市場價值 145.1 億美元,預計到 2031 年將從 2026 年的 152.4 億美元成長至 191.1 億美元,預測期(2026-2031 年)複合年成長率為 4.63%。

電子商務履約、汽車組裝近岸外包以及低溫運輸法規正在重塑服務組合,而多年期美元計價合約則有助於規避外匯風險,並支持高容量、技術驅動型物流中心的快速擴張。本報告按服務類型(運輸、倉儲物流及其他)、合約期限(1-3年、3年以上)、終端用戶行業(製造業及汽車業、食品飲料業、零售及電商業及其他)以及國家/地區(巴西、阿根廷、智利、哥倫比亞、秘魯及其他南美國家)進行細分。市場預測以美元計價。

南美合約物流市場的趨勢與洞察

電子商務的快速成長以及對當日達和隔日達服務的需求。

平台營運商已將物流成本從可變成本轉變為固定成本。這是因為在佔區域電商交易量60%的主要路線上,履約速度對於市場佔有率至關重要。 Mercado Libre計畫在2025年將其在巴西的物流中心數量加倍,達到21個,新增88萬平方公尺的倉儲面積,並在聖保羅、里約熱內盧和貝洛奧裡藏特實現當日送達。隨後,Shopee於2026年3月在聖保羅開設了一個22萬平方公尺的倉庫,將從下單到出貨的時間縮短至12小時以內。亞馬遜位於巴西利亞的履約中心(6.7萬平方公尺)由CEVA公司在11週內建成,每天可處理13.5萬個包裹。在阿根廷,已有30%的線上訂單在24小時內送達,庫存位於科爾多瓦和羅薩裡奧附近。在巴西的逆向物流流程中,檢驗、重新包裝和轉售進口商品的供應商(這些商品面臨 77% 的總合稅負)可獲得 8-12% 的額外利潤。

汽車生產和出口成長

近岸外包緩解了中美之間的緊張關係,並確保符合美墨加協定(USMCA)嚴格的在地採購規定。比亞迪位於卡馬卡利的工廠預計到2025年年產量將達到15萬輛,在投資10.6億美元後,計劃到2026年底將產量加倍,這就需要在生產線30分鐘車程內設立一個專門的序列中心。長城汽車正在建造一個價值200億美元的綜合設施,日產汽車已在其雷森德工廠投資5.4億美元引入第二班次,從而實現每天12條零件配送路線。預計到2026年7月,巴西的電動車關稅將達到35%,這將加速本地組裝,並提高電池模組安裝、軟體刷寫和合規標籤的溢價。墨西哥395萬輛的產量已成為區域政府競相效法的標竿。

道路和港口基礎設施瓶頸

儘管桑托斯港在2025年處理了130萬標準箱(TEU),但平均停留時間仍為4-5天,是巴拿馬運河沿線同等規模港口的兩倍,因為Tekon 10項目要到2040年才能全面運作。在瓦爾帕萊索港,85%運往聖地牙哥的貨物依賴卡車運輸,導致每個貨櫃額外增加150-200美元的成本,運輸時間最多增加一天。金融危機期間,阿根廷的基礎設施網路劣化,70%的高速公路不符合標準,使運輸公司的維護成本增加了高達20%。

細分市場分析

預計到2025年,運輸服務將佔南美洲合約物流市場佔有率的62.87%,凸顯了該大陸的龐大規模——目前仍有60%的貨物依靠卡車運輸。附加價值服務預計將成長6.18%,受益於可降低高達25%庫存成本的延期策略以及與揭露再生材料含量相關的新標籤要求。

預計阿根廷批准使用鉸接式卡車(Bittren)將使陸上運輸受益,每托盤成本將降低12%。目前,鐵路僅佔巴西貨運量的15%,但烏爾基薩鐵路的現代化改造預計將在2028年前將多達200萬噸的貨物從公路轉移到鐵路。空運貨物主要為藥品和生鮮產品,經由瓜魯柳斯機場運輸,目前托運人正在預訂停機坪旁的冷藏庫。海運量的成長與杜拜環球港務集團(DP World)計畫在2026年將桑托斯港的吞吐能力提升至170萬標準箱的目標相符,也反映了南美合約物流市場貨櫃吞吐量的強勁成長趨勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務的快速成長以及對當日達和隔日達服務的需求。

- 汽車生產和出口成長

- 基礎設施現代化計劃

- 北美和歐盟供應鏈的離岸外包

- 農產品和疫苗的低溫運輸需求

- 區域城市的計量型第三方物流微型倉配

- 市場限制因素

- 道路和港口基礎設施瓶頸

- 複雜的跨境海關與稅收制度

- 長期第三方物流合約中的外匯波動風險

- 熟練倉庫工人短缺

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 電子商務(國內和跨境)分析

- 逆向物流的考量

- 地緣政治事件的影響

第5章 市場規模與成長預測

- 按服務類型

- 運輸

- 路

- 鐵路

- 航空

- 海

- 倉儲/物流

- 附加價值服務(組裝、貼標、套件包裝)

- 運輸

- 按合約期限

- 1-3年

- 3年或以上

- 按最終用戶行業分類

- 製造業/汽車

- 食品/飲料

- 零售與電子商務

- 醫療和藥品

- 化學品

- 其他行業

- 國家

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 秘魯

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Supply Chain

- DSV Solutions

- Kuehne+Nagel

- CEVA Logistics(CMA CGM)

- Maersk Logistics & Services

- DP World

- JSL Logistica

- ID Logistics

- GEODIS

- UPS Supply Chain Solutions

- FedEx Logistics

- Andreani Logistica

- Penske Logistics

- Hellmann Worldwide Logistics

- Grupo TASA Logistica

- TPC Logistica

- Yusen Logistics

- R0hlig Logistics

- Expeditors

- Crane Worldwide Logistics

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america contract logistics market size was valued at USD 14.51 billion in 2025 and estimated to grow from USD 15.24 billion in 2026 to reach USD 19.11 billion by 2031, at a CAGR of 4.63% during the forecast period (2026-2031).

E-commerce fulfillment, near-shoring of automotive assembly, and cold-chain mandates are reshaping service portfolios, while multiyear, dollar-denominated contracts hedge currency swings and underpin the rapid build-out of high-throughput, technology-enabled distribution centers. This report is Segmented by Service Type (Transportation, Warehousing & Distribution, and More), by Contract Duration (1-3 Years, Above 3 Years), by End-User Industry (Manufacturing & Automotive, Food & Beverage, Retail & E-Commerce, and More), and by Country (Brazil, Argentina, Chile, Colombia, Peru, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

South America Contract Logistics Market Trends and Insights

E-Commerce Boom and Same- or Next-Day Fulfillment Demand

Platform operators converted logistics from a variable cost into a fixed asset because fulfillment speed now dictates share in corridors that host 60% of regional e-commerce volume. Mercado Libre doubled Brazilian distribution centers to 21 by 2025, adding 880,000 square meters and securing same-day delivery in Sao Paulo, Rio de Janeiro, and Belo Horizonte. Shopee followed by opening a 220,000-square-meter Sao Paulo warehouse in March 2026, cutting order-to-dispatch time below 12 hours. Amazon's 67,000-square-meter Brasilia fulfillment center, built by CEVA in eleven weeks, processes 135,000 packages daily. Argentina already delivers 30% of online orders within 24 hours, pushing inventory closer to Cordoba and Rosario. Reverse-logistics flows in Brazil earn 8-12% incremental margin for providers who inspect, repackage, and relist imports that face a combined 77% tax burden.

Automotive Production and Export Growth

Near-shoring mitigates U.S.-China tensions and ensures compliance with strict USMCA content rules. BYD's Camacari plant reached 150,000 units in 2025 and, following a USD 1.06 billion investment, will double output by the end of 2026, requiring dedicated sequencing centers within 30 minutes of the production line. Great Wall Motors is constructing a USD 20 billion complex, while Nissan invested USD 540 million to add a second shift in Resende, enabling twelve daily milk-run circuits. Rising EV tariffs in Brazil, set to reach 35% by July 2026, are accelerating local assembly and increasing the premium for battery-module installation, software flashing, and compliance labeling. Mexico's 3.95 million-unit output serves as a benchmark that regional governments aim to emulate.

Road and Port Infrastructure Bottlenecks

Santos moved 1.3 million TEU in 2025, yet still averages four to five-day dwell times, double that of Panama Canal peers, because the Tecon 10 project will only reach full capacity in 2040. Valparaiso relies on trucks for 85% of its Santiago-bound cargo, adding USD 150-200 per container and up to a full day of transit. Argentina's network downgraded during its fiscal crisis, leaving 70% of highways below acceptable standards and inflating carrier maintenance costs by up to 20%.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Modernization Programs

- Near-Shoring of North American and EU Supply Chains

- Complex Cross-Border Customs and Tax Regimes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation services accounted for 62.87% of the South America contract logistics market share in 2025, underlining the scale of a continent where 60% of cargo still moves by truck. Value-added services are poised for a 6.18% growth trajectory, benefiting from postponement strategies that cut inventory costs by up to 25%, and from new labeling mandates tied to recycled-content disclosure.

Road haulage should benefit from Argentina's allowance of bitrenes, which lowers per-pallet costs by 12%. Rail remains limited at 15% of Brazil's freight share, though modernization of the Urquiza line could redirect up to two million tonnes from road to rail by 2028. Air freight centers on pharmaceuticals and perishables moving through Guarulhos, where shippers now pre-book apron-adjacent cold rooms. Sea freight growth aligns with DP World's plan to raise Santos capacity to 1.7 million TEU by 2026, reflecting strong containerized flows tied to the South America contract logistics market.

List of Companies Covered in this Report:

- DHL Supply Chain

- DSV Solutions

- Kuehne + Nagel

- CEVA Logistics (CMA CGM)

- Maersk Logistics & Services

- DP World

- JSL Logistica

- ID Logistics

- GEODIS

- UPS Supply Chain Solutions

- FedEx Logistics

- Andreani Logistica

- Penske Logistics

- Hellmann Worldwide Logistics

- Grupo TASA Logistica

- TPC Logistica

- Yusen Logistics

- R0hlig Logistics

- Expeditors

- Crane Worldwide Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce Boom & Same-/Next-Day Fulfilment Demand

- 4.2.2 Automotive Production & Export Growth

- 4.2.3 Infrastructure Modernization Programmes

- 4.2.4 Near-Shoring of North-American/EU Supply Chains

- 4.2.5 Cold-Chain Needs for Agrifood & Vaccines

- 4.2.6 Pay-As-You-Go 3PL Micro-Fulfilment in Secondary Cities

- 4.3 Market Restraints

- 4.3.1 Road & Port Infrastructure Bottlenecks

- 4.3.2 Complex Cross-Border Customs & Tax Regimes

- 4.3.3 FX-Volatility Risk to Long-Term 3PL Contracts

- 4.3.4 Skilled Warehouse-Labor Shortages

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Insights on E-commerce (Domestic and Cross-Border)

- 4.9 Insights on Reverse Logistics

- 4.10 Impact of Geo-Political Events

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Air

- 5.1.1.4 Sea

- 5.1.2 Warehousing & Distribution

- 5.1.3 Value-added Services (Assembly, Labelling, Kitting)

- 5.1.1 Transportation

- 5.2 By Contract Duration

- 5.2.1 1-3 Years

- 5.2.2 Above 3 years

- 5.3 By End-user Industry

- 5.3.1 Manufacturing and Automotive

- 5.3.2 Food and Beverage

- 5.3.3 Retail and E-commerce

- 5.3.4 Healthcare and Pharmaceuticals

- 5.3.5 Chemicals

- 5.3.6 Other Industries

- 5.4 By Country

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 DHL Supply Chain

- 6.4.2 DSV Solutions

- 6.4.3 Kuehne + Nagel

- 6.4.4 CEVA Logistics (CMA CGM)

- 6.4.5 Maersk Logistics & Services

- 6.4.6 DP World

- 6.4.7 JSL Logistica

- 6.4.8 ID Logistics

- 6.4.9 GEODIS

- 6.4.10 UPS Supply Chain Solutions

- 6.4.11 FedEx Logistics

- 6.4.12 Andreani Logistica

- 6.4.13 Penske Logistics

- 6.4.14 Hellmann Worldwide Logistics

- 6.4.15 Grupo TASA Logistica

- 6.4.16 TPC Logistica

- 6.4.17 Yusen Logistics

- 6.4.18 R0hlig Logistics

- 6.4.19 Expeditors

- 6.4.20 Crane Worldwide Logistics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

合約物流市場:按服務、類型、運輸方式、行業和地區分類

合約物流市場:按服務、類型、運輸方式、行業和地區分類 2026年全球合約物流市場報告

2026年全球合約物流市場報告 合約物流市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

合約物流市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 合約物流市場:2026-2032年全球市場預測(依服務類型、貨物類型、運輸方式、客戶規模及最終用途分類)

合約物流市場:2026-2032年全球市場預測(依服務類型、貨物類型、運輸方式、客戶規模及最終用途分類) 亞太地區合約物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲合約物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)北美合約物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

亞太地區合約物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲合約物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)北美合約物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 日本合約物流市場報告(按類型(內部物流、外部物流)、最終用戶(汽車、消費品和零售、能源、高科技和醫療保健、工業和航太、技術及其他)和地區分類,2026-2034 年)

日本合約物流市場報告(按類型(內部物流、外部物流)、最終用戶(汽車、消費品和零售、能源、高科技和醫療保健、工業和航太、技術及其他)和地區分類,2026-2034 年) 合約物流市場規模及預測 2021 - 2031、全球及地區佔有率、趨勢及成長機會分析報告涵蓋範圍:按類型、服務類型、最終用戶及地理分類

合約物流市場規模及預測 2021 - 2031、全球及地區佔有率、趨勢及成長機會分析報告涵蓋範圍:按類型、服務類型、最終用戶及地理分類 美國合約物流市場:依服務、類型、產業、運輸方式、地區、機會及預測,2018-2032

美國合約物流市場:依服務、類型、產業、運輸方式、地區、機會及預測,2018-2032