|

市場調查報告書

商品編碼

1939745

亞太地區合約物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Asia-Pacific Contract Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

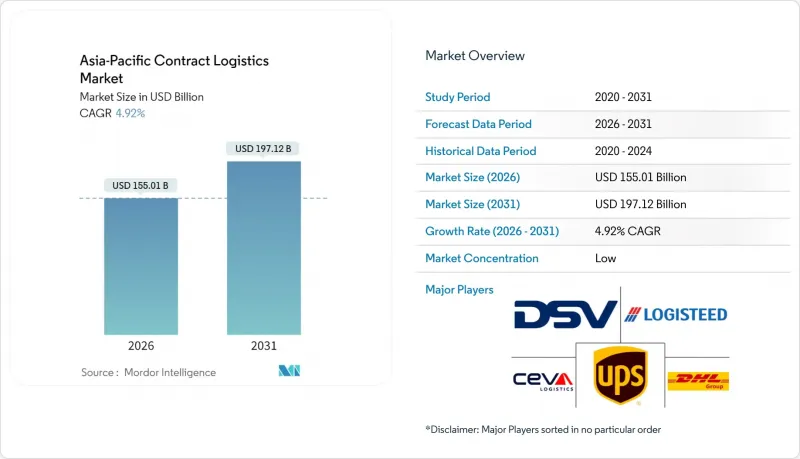

預計到 2026 年,亞太地區的合約物流市場規模將達到 1,550.1 億美元。

這意味著從 2025 年的 1,477.4 億美元成長到 2031 年的 1,971.2 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 4.92%。

亞太地區合約物流市場的當前規模反映了該地區作為全球外包價值鏈管理中心的地位,預計複合年成長率表明,隨著托運人履約網路進行現代化改造並拓展附加價值服務,市場將持續成長。電子商務的快速發展、大規模的近岸外包和回岸外包,以及政府對公路、鐵路、港口和數位基礎設施的大量投資,正在加速製造業、零售業和醫療保健行業對合約物流的採用。整合網路設計、自動化和數據平台的長期夥伴關係正在取代短期交易協議,使供應商即使在勞動力和房地產資源受限的環境下也能提供穩定的供給能力。南海航道擁擠導致海上保險費上漲,以及對溫度敏感的航線上持續存在的低溫運輸瓶頸,雖然增加了市場的複雜性,但也為能夠提供嚴格品管和跨境規服務的供應商創造了利潤豐厚的市場機會。

亞太地區合約物流市場趨勢與洞察

亞太地區電子商務爆炸性成長

數位商務的蓬勃發展正在重塑亞太地區合約物流市場的履約經濟格局。線上銷售的快速成長迫使品牌商採用全通路庫存分配、微型倉配點和專用逆向物流迴路,而這些是大多數企業內部物流網路無法實現的。印尼和越南的線上銷售額年增率遠超過實體店,迫使倉庫開發商增建夾層以實現自動化揀貨和包裝,並增設溫控單元用於存放高階食品雜貨。由於區域退貨率通常高達15%至30%,合約物流供應商現在正將再製造生產線、重新包裝站和即時視覺化儀錶板整合到其整合提案中。

供應鏈近岸外包/回流(中國+1策略)

跨國公司正將零件採購和最終組裝轉移到東南亞和印度,以分散地緣政治風險並降低總到岸成本。越南北部經濟區和印尼巴塘工業園區等新興生產中心需要原料預處理、為準時制生產線供料以及整合出口貨物——所有這些現有供應商都可以透過跨國控制中心提供。雙重採購策略要求對中國和海外工廠的營運進行跨工廠視覺化管理,因此,托運人擴大將運輸規劃、里程碑管理和供應商管理庫存外包給物流專家。印度的生產連結獎勵計畫計劃和印尼的綜合法案等政府舉措正在加速工廠搬遷,隨著新的物流走廊日趨成熟,亞太地區的合約物流市場預計將在中期內實現成長。

主要基地房地產和人事費用上漲

2024年,由於土地供應緊張以及資料中心營運商的競爭需求,新加坡、香港和東京的優質倉庫租金飆升。同時,澳洲和韓國的堆高機駕駛人和揀貨員的基本工資正以兩位數的速度成長,擠壓著大量營運的利潤空間。合約物流業者正透過機器人貨物搬運、自動堆垛機和節能空調系統來緩解這些壓力,但這些升級需要大量的資本支出和較長的投資回收期。這些經濟狀況促使以柔佛新山和千葉等低成本衛星城市為基地的樞紐輻射式網路興起,但大都會圈的「最後一公里」配送時效性仍然是一個挑戰,導致服務水準協議更加嚴格,短期價格上漲空間有限。

細分市場分析

到2025年,運輸環節將佔亞太地區合約物流市場收入的62.55%,這主要得益於中國密集的道路運輸網路和印尼發達的國內海運網路。在地域分散的情況下,物流供應商正在協調長途公路運輸、鐵路聯運和短途海運支線,以平衡成本和速度。同時,受製造商對延遲出貨、套件組裝以及在區域配銷中心內簡化組裝能力的需求推動,附加價值服務預計將在2031年之前實現最高的複合年成長率(CAGR),達到4.03%。日益複雜的家電標籤法規促使合約物流供應商安裝本地印刷和貼標生產線。同時,時尚品牌正在利用倉庫內的縫紉單元來加快尺寸調整速度並提高銷售轉換率。這種轉變正在擴大利潤率並降低對波動較大的公路貨運價格的依賴。亞太地區合約物流市場規模在高附加價值領域正經歷結構性擴張。

倉儲和配送業務依然是核心業務,並隨著電子商務小包裹量和全通路庫存策略的推進而同步擴張。高密度穿梭運輸系統減少了城市中心偏遠地區的面積,而靠近海港的越庫作業佈局則縮短了對溫度敏感的農產品的停留時間。具有前瞻性的營運商正在將倉庫管理系統與即時運輸視覺化平台整合,以識別預計到達時間並提供異常警報,從而改善客戶體驗。空運貨量同樣在成長,而高價值小包裹和生技藥品的直接投遞模式需要從始發地到最終目的地的多模態管理,這支撐了亞太地區合約物流市場的整體成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 亞太地區電子商務滲透率爆炸性成長

- 供應鏈近岸外包/回流(中國+1策略)

- 政府對物流基礎建設進行大規模投資

- 製造業和零售業的外包重點

- 電動車電池超級工廠對廠內物流的需求

- 數位化海關平台加速跨境物流

- 市場限制

- 主要城市的房地產和人事費用不斷上漲

- 亞太地區國家標準和許可製度的碎片化

- 生物製藥低溫運輸能力瓶頸

- 南海航線海上保險費正在上漲

- 價值/供應鏈分析

- 監管環境

- 技術展望(自動化、人工智慧、物聯網、倉庫管理系統)

- 波特五力模型

- 新進入者的威脅

- 替代品的威脅

- 買方的議價能力

- 供應商的議價能力

- 競爭對手之間的競爭

- 政府措施和經濟特區現狀

- 交通走廊(海運、鐵路、公路)

- 電子商務洞察(國內和跨境)

- 逆向物流的考量

- 回顧新冠疫情和地緣政治事件的影響

第5章 市場規模與成長預測

- 按服務類型

- 運輸

- 路

- 鐵路

- 空運

- 海上運輸

- 倉儲/配送

- 附加價值服務(組裝、貼標、套件包裝)

- 運輸

- 按合約期限

- 1-3年

- 3年或以上

- 按最終用戶行業分類

- 製造業和汽車業

- 食品/飲料

- 零售與電子商務

- 醫療/製藥

- 化學品

- 其他行業

- 按國家/地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 印尼

- 泰國

- 亞太其他地區

第6章 競爭情勢

- 市場集中度分析

- 策略趨勢(併購、合資、自動化資本投資)

- 市佔率分析

- 公司簡介

- Deutsche Post DHL Group

- DSV

- CEVA Logistics

- UPS Supply Chain Solutions

- Logisteed Ltd

- CJ Logistics

- Nippon Express Co. Ltd

- Toll Group

- Yusen Logistics Co. Ltd

- Kuehne+Nagel

- Kerry Logistics Network Ltd

- Hellmann Worldwide Logistics

- Rhenus Logistics

- Geodis

- GAC

- Silk Contract Logistics

- Linc Group

- Rohlig Logistics

- Allcargo Logistics Ltd

- Broekman Logistics

第7章 市場機會與未來展望

第8章附錄

- 按行業和地區分類的GDP分佈

- 資金流分析

- 外貿統計

Asia-Pacific Contract Logistics Market size in 2026 is estimated at USD 155.01 billion, growing from 2025 value of USD 147.74 billion with 2031 projections showing USD 197.12 billion, growing at 4.92% CAGR over 2026-2031.

The current Asia-Pacific Contract Logistics market size reflects the region's role as the global center for outsourced supply-chain management, and the forecast CAGR points to sustained momentum as shippers modernize fulfillment networks and extend value-added services. Rapid e-commerce expansion, large-scale near- and re-shoring, and government mega-investments in road, rail, port, and digital infrastructure are accelerating contract-logistics adoption across manufacturing, retail, and healthcare sectors. Long-term partnerships that align network design, automation, and data platforms continue to replace short-term, transactional arrangements, allowing providers to deliver resilient capacity in tight labor and real-estate environments. Rising marine-insurance premiums on congested South-China-Sea routes and persistent cold-chain bottlenecks in temperature-sensitive corridors add complexity, but they also create high-margin niches that reward providers capable of rigorous quality control and cross-border compliance.

Asia-Pacific Contract Logistics Market Trends and Insights

Explosive E-commerce Penetration Across Asia-Pacific

Digital commerce growth is redefining fulfillment economics across the Asia-Pacific Contract Logistics market. Online sales velocity is forcing brands to adopt omnichannel inventory allocation, micro-fulfillment nodes, and dedicated reverse-logistics loops that most in-house networks cannot match. Indonesia and Vietnam record annual online-sales expansion far above brick-and-mortar growth, pushing warehouse developers to add mezzanine floors for pick-and-pack automation and temperature-controlled cells for premium groceries. Regional return rates often reach 15-30%, demanding refurbishment lines, re-boxing stations, and real-time visibility dashboards that contract-logistics providers now bundle into integrated propositions.

Near-/Re-shoring of Supply Chains ("China+1")

Multinational corporations are reallocating component sourcing and final assembly to Southeast Asia and India to diversify geopolitical risk and lower total landed cost. New production clusters in Vietnam's Northern Economic Zone and Indonesia's Batang Industrial Park demand inbound raw-material staging, just-in-sequence line feeding, and export consolidation that established providers can deliver from multi-country control towers. Dual-sourcing strategies require visibility across Chinese and non-Chinese plants, prompting shippers to hand over transport planning, milestone monitoring, and supplier-managed inventory to logistics specialists. Government programs such as India's Production-Linked Incentive scheme and Indonesia's Omnibus Law further accelerate factory relocations, locking in mid-term growth for the Asia-Pacific Contract Logistics market as new corridors mature.

Soaring Real-estate & Labor Costs in Tier-1 Hubs

Prime-grade warehouse rents rose sharply across Singapore, Hong Kong, and Tokyo in 2024, driven by constrained land supply and competing demand from data-center operators. Simultaneously, base wages for forklift drivers and order-pickers climbed in double digits in Australia and South Korea, eroding profit margins for high-volume operations. Contract-logistics providers mitigate these pressures through goods-to-person robotics, automated palletizers, and energy-efficient HVAC systems, but such upgrades require heavy capital outlays and lengthier payback periods. The economics encourage hub-and-spoke networks anchored in lower-cost satellite cities such as Johor Bahru and Chiba, yet last-mile cut-off times in megacities remain challenging, tightening service-level agreements and limiting rate increases in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Government Mega-spend on Logistics Infrastructure

- Outsourcing Focus of Manufacturers & Retailers

- Fragmented Standards & Permits Across Asia-Pacific Nations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The transportation slice of the Asia-Pacific Contract Logistics market generated 62.55% of revenue in 2025, anchored by dense road fleets in China and sprawling domestic maritime lanes in Indonesia. Providers orchestrate synchronized long-haul trucking, rail shuttles, and short-sea feeder loops to balance cost and speed across fragmented geography. Meanwhile, value-added services are expected to post the strongest 4.03% CAGR to 2031 as manufacturers seek postponement, kitting, and light-assembly capabilities inside regional distribution centers. Growing label-compliance complexity in consumer electronics pushes contract operators to install on-site print-and-apply lines, while fashion brands use in-warehouse sewing cells for rapid size adjustments that elevate sell-through rates. The shift broadens margins and reduces reliance on volatile linehaul rates, reinforcing the structural expansion of the Asia-Pacific Contract Logistics market size within higher-value niches.

Warehouse-and-distribution operations remain central, scaling with e-commerce parcel volumes and omni-inventory strategies. High-density shuttle systems reduce footprint in urban infill sites, whereas cross-docking layouts near seaports cut dwell time for temperature-sensitive produce. Progressive operators couple warehouse-management systems with real-time transport-visibility platforms, unlocking predictive arrival windows and exception alerts that sharpen customer experience. Airfreight forwarding volumes climb in parallel as direct-injection models for high-value parcels and biologics require multi-modal control from origin to doorstep, buttressing growth across the Asia-Pacific Contract Logistics market.

The Asia-Pacific Contract Logistics Market Report is Segmented by Service Type (Transportation, Warehousing & Distribution, and Value-Added Services), Contract Duration (1-3 Years and Above 3 Years), End-User Industry (Manufacturing & Automotive, , Retail & E-Commerce, Healthcare & Pharmaceuticals, Chemicals, and More), Country (China, India, Japan, Australia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Deutsche Post DHL Group

- DSV

- CEVA Logistics

- UPS Supply Chain Solutions

- Logisteed Ltd

- CJ Logistics

- Nippon Express Co. Ltd

- Toll Group

- Yusen Logistics Co. Ltd

- Kuehne + Nagel

- Kerry Logistics Network Ltd

- Hellmann Worldwide Logistics

- Rhenus Logistics

- Geodis

- GAC

- Silk Contract Logistics

- Linc Group

- Rohlig Logistics

- Allcargo Logistics Ltd

- Broekman Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive e-commerce penetration across Asia-Pacific

- 4.2.2 Near-/re-shoring of supply chains ("China+1")

- 4.2.3 Government mega-spend on logistics infrastructure

- 4.2.4 Outsourcing focus of manufacturers & retailers

- 4.2.5 EV battery gigafactories' in-plant logistics demand

- 4.2.6 Digital customs platforms speeding cross-border flows

- 4.3 Market Restraints

- 4.3.1 Soaring real-estate & labour costs in tier-1 hubs

- 4.3.2 Fragmented standards & permits across Asia-Pacific nations

- 4.3.3 Cold-chain capacity bottlenecks for biologics

- 4.3.4 Rising marine-insurance premiums in South-China-Sea lanes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (Automation, AI, IoT, WMS)

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Threat of Substitutes

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Government Initiatives & SEZ Landscape

- 4.9 Transport Corridors (Maritime, Rail, Road)

- 4.10 Insights on E-commerce (Domestic & Cross-Border)

- 4.11 Insights on Reverse Logistics

- 4.12 COVID-19 & Geo-Political Events Impact Review

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Air

- 5.1.1.4 Sea

- 5.1.2 Warehousing & Distribution

- 5.1.3 Value-added Services (Assembly, Labelling, Kitting)

- 5.1.1 Transportation

- 5.2 By Contract Duration

- 5.2.1 1 - 3 Years

- 5.2.2 Above 3 years

- 5.3 By End-user Industry

- 5.3.1 Manufacturing & Automotive

- 5.3.2 Food & Beverage

- 5.3.3 Retail & E-commerce

- 5.3.4 Healthcare & Pharmaceuticals

- 5.3.5 Chemicals

- 5.3.6 Other Industries

- 5.4 By Country

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Australia

- 5.4.6 Singapore

- 5.4.7 Malaysia

- 5.4.8 Indonesia

- 5.4.9 Thailand

- 5.4.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration Analysis

- 6.2 Strategic Moves (M&A, JVs, Automation Cap-ex)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Deutsche Post DHL Group

- 6.4.2 DSV

- 6.4.3 CEVA Logistics

- 6.4.4 UPS Supply Chain Solutions

- 6.4.5 Logisteed Ltd

- 6.4.6 CJ Logistics

- 6.4.7 Nippon Express Co. Ltd

- 6.4.8 Toll Group

- 6.4.9 Yusen Logistics Co. Ltd

- 6.4.10 Kuehne + Nagel

- 6.4.11 Kerry Logistics Network Ltd

- 6.4.12 Hellmann Worldwide Logistics

- 6.4.13 Rhenus Logistics

- 6.4.14 Geodis

- 6.4.15 GAC

- 6.4.16 Silk Contract Logistics

- 6.4.17 Linc Group

- 6.4.18 Rohlig Logistics

- 6.4.19 Allcargo Logistics Ltd

- 6.4.20 Broekman Logistics

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

8 Appendix

- 8.1 GDP Distribution by Activity & Region

- 8.2 Capital-Flow Insights

- 8.3 External Trade Statistics

合約物流市場:按服務、類型、運輸方式、行業和地區分類

合約物流市場:按服務、類型、運輸方式、行業和地區分類 2026年全球合約物流市場報告

2026年全球合約物流市場報告 合約物流市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

合約物流市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 合約物流市場:2026-2032年全球市場預測(依服務類型、貨物類型、運輸方式、客戶規模及最終用途分類)

合約物流市場:2026-2032年全球市場預測(依服務類型、貨物類型、運輸方式、客戶規模及最終用途分類) 歐洲合約物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)北美合約物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

歐洲合約物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)北美合約物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 日本合約物流市場報告(按類型(內部物流、外部物流)、最終用戶(汽車、消費品和零售、能源、高科技和醫療保健、工業和航太、技術及其他)和地區分類,2026-2034 年)

日本合約物流市場報告(按類型(內部物流、外部物流)、最終用戶(汽車、消費品和零售、能源、高科技和醫療保健、工業和航太、技術及其他)和地區分類,2026-2034 年) 合約物流市場規模及預測 2021 - 2031、全球及地區佔有率、趨勢及成長機會分析報告涵蓋範圍:按類型、服務類型、最終用戶及地理分類

合約物流市場規模及預測 2021 - 2031、全球及地區佔有率、趨勢及成長機會分析報告涵蓋範圍:按類型、服務類型、最終用戶及地理分類 美國合約物流市場:依服務、類型、產業、運輸方式、地區、機會及預測,2018-2032

美國合約物流市場:依服務、類型、產業、運輸方式、地區、機會及預測,2018-2032 合約物流的全球市場(2025年)

合約物流的全球市場(2025年)