|

市場調查報告書

商品編碼

2061755

北美IT設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)North America IT Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

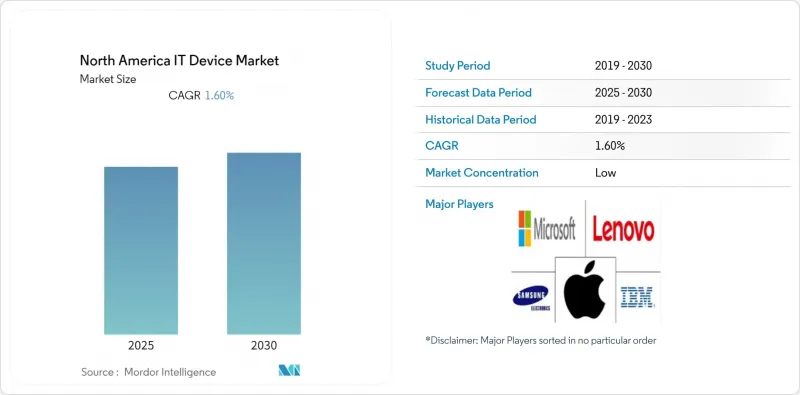

根據 Mordor Intelligence 預測,北美 IT 設備市場將從 2026 年的 8,018.5 億美元成長到 2031 年的 1.11417 兆美元,2026 年至 2031 年的複合年成長率為 6.8%。

本報告按設備類別(桌上型電腦、筆記型電腦、平板電腦等)、終端用戶產業(一般消費者、中小企業、大型企業、教育機構等)、連接方式(有線設備、無線設備)、分銷管道(線上零售、離線零售、B2B直銷等)和地區進行細分。市場預測以美元計價。

北美IT設備市場的趨勢與洞察

對混合辦公所需硬體的需求正在激增。

混合辦公模式已成常態,筆記型電腦、顯示器和網路攝影機的銷售在疫情期間激增之後仍持續成長。百思買在2026年第三季報告中指出,計算和行動產品佔國內銷售額的49%,同店銷售額較去年同期成長7.6%。戴爾科技和惠普都強調,由於企業將電腦更換週期從五年縮短至三年,導致累積訂單顯著增加。美國和加拿大的需求最為強勁,這兩個國家知識型員工遠距辦公的比例超過40%。而墨西哥則由於基礎設施限制而落後。因此,配備神經網路處理單元(NPU)的高階筆記型電腦銷售正在成長,以確保符合當地的人工智慧推理和資料主權法規。由此,北美IT設備市場商用產品的平均售價正在上漲,部分抵銷了入門級消費級電腦的下滑。

公司範圍內的裝置更新,此前Windows 10已停止支援。

微軟於2025年10月14日停止對Windows 10的支持,引發了自Windows 7停止支援以來最大的企業PC更新週期。惠普和戴爾的大量授權協議現在將Windows 11專業版與搭載高通驍龍X Elite或英特爾酷睿Ultra處理器的Copilot+ PC捆綁銷售,每款處理器都內建了各自的AI引擎。聯想ThinkPad X1 Carbon Gen 13正是這一趨勢的例證,它將英特爾晶片與在2025年國際消費電子展(CES 2025)上發布的設備內轉錄代理相結合。美國、加拿大各省和墨西哥子公司的公共部門採購正在釋放先前推遲的預算,以確保網路安全合規性,預計其影響將集中在2026-2027年。因此,北美IT設備市場的需求正在提前,這將提振短期收入,但可能會延長未來的週期。

半導體供應失衡的局面仍在持續。

儘管表面上的供應限制有所緩解,但高頻寬記憶體和先進邏輯節點的結構性短缺依然存在。三星宣布,由於人工智慧伺服器需求推動的供應緊張,將在2025年第一季將DDR5記憶體價格上調至多60%。美光也認為記憶體短缺將持續到2027年,導致原本用於消費性PC的產能被轉移。美國工業與安全局(BIS)分別於2024年12月和2025年1月發布的出口限制進一步限制了中國半導體工廠的生產設備供應,抑制了全球晶圓產能的擴張。由此導致的前置作業時間波動,使北美各地設備製造商的生產計畫變得複雜,並拖累了北美IT設備市場的預期成長率。

細分市場分析

儘管穿戴式裝置在2025年僅佔很小的市場佔有率,但預計到2031年將以較高的複合年成長率成長,成為所有IT設備領域中成長最快的類別。美國食品藥物管理局(FDA)於2026年初發布的最新指南放寬了低風險健康追蹤器的監管障礙,為加速其普及鋪平了道路。 Garmin的Fenix 8憑藉其心電圖(ECG)和血氧飽和度(SpO2)感測器等先進功能,可同時滿足運動員和急救人員的需求,填補了市場中一個雖小但至關重要的細分領域。此外,雅培、Medtronic和德康等公司的連續血糖監測儀正在整合智慧型手機連接功能,從而建立一個更緊密互聯的數據生態系統。這些由創新和監管支持推動的進步,凸顯了穿戴式裝置在更廣泛的IT設備市場中日益成長的重要性。

智慧型手機仍佔據北美IT設備市場最大的佔有率,但隨著市場滲透率趨於飽和,其成長速度正在放緩。相較之下,筆記型電腦和桌上型電腦則保持穩定成長,這得益於邊緣人工智慧技術的升級,這些升級增強了設備的功能和吸引力。伺服器和儲存設備的密度也不斷提高,以滿足人工智慧工作負載的需求,例如希捷推出的30TB高容量Exos M硬碟。周邊設備繼續受益於混合辦公環境的持續需求,而POS終端和工業手持設備仍然是「其他設備」類別中的關鍵組成部分。總而言之,這些變化反映了企業和消費者不斷變化的需求,凸顯了市場正在向支援持續分析服務的資料產生硬體進行更廣泛的轉變。

預計2026年至2031年間,醫療保健產業的複合年成長率將達到10.6%,超過目前仍佔最大市場佔有率的消費品產業。醫院正在加速採用堅固耐用的平板電腦用於床邊圖表製作,並採用穿戴式式監視器進行遠端患者監護,以確保在符合HIPAA(健康保險流通與責任法案)規定的前提下,與電子健康記錄無縫整合。美國和加拿大人口老化以及慢性病的盛行率上升,正在推動持續監測解決方案的需求。此外,中小企業傾向於選擇經濟實惠的筆記型電腦,而大型企業則正在標準化採用透過零信任安全主機管理的AI賦能型PC,以提高營運效率和資料安全性。

在教育領域,得益於加拿大各省提供的數位學習津貼,對Chromebook和iPad的需求依然強勁。美國政府機構正在利用多年期的GSA採購計劃,類似的協議也正在推動加拿大IT設備的現代化。銀行、金融和保險(BFSI)行業正在升級工作站,以支援即時詐欺分析,確保合規性和營運靈活性。同時,製造業和能源產業正在採用專為惡劣環境設計的加固型PC,以滿足特定的營運需求。這些趨勢共同表明,北美IT設備市場的需求正在轉變,而這種轉變是由特定產業需求和技術進步所驅動的。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對混合辦公所需硬體的需求正在激增。

- Windows 10 支援結束後,公司範圍內的裝置更新週期將結束。

- 5G部署的加速正在推動智慧型手機的更換。

- 墨西哥國內半導體組裝的稅收優惠

- XR穿戴裝置在訓練領域的廣泛應用。

- 將邊緣人工智慧整合到筆記型電腦和桌上型電腦中

- 市場限制因素

- 半導體供需長期失衡

- 通貨膨脹導致的消費者價格敏感性

- 加強中美兩國對先進半導體的出口限制

- 遵守電子廢棄物法規的成本不斷上升

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過裝置

- 桌上型電腦

- 筆記型電腦

- 藥片

- 智慧型手機

- 伺服器和儲存系統

- 穿戴式裝置

- 周邊設備(鍵盤、滑鼠)

- 其他設備類別

- 按最終用戶行業分類

- 消費者

- 小型企業

- 大公司

- 教育領域

- 政府/公共部門

- 醫療保健產業

- 零售與電子商務

- BFSI

- 其他終端用戶產業

- 連結性別

- 有線設備

- 無線裝置

- 透過分銷管道

- 線上零售

- 線下零售

- B2B直銷

- 增值轉售商

- 行動電信業者經營的商店

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Dell Technologies Inc.

- HP Inc.

- Lenovo Group Limited

- ASUSTeK Computer Inc.

- Acer Inc.

- Microsoft Corporation

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- LG Electronics Inc.

- Sony Group Corporation

- Panasonic Holdings Corporation

- Garmin Ltd.

- Zebra Technologies Corporation

- Fujitsu Limited

- Seagate Technology Holdings plc

- Western Digital Corporation

- Toshiba Electronic Devices and Storage Corporation

- Hisense Visual Technology Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america iT device market size is expected to increase from USD 801.85 billion in 2026 to reach USD 1,114.17 billion by 2031, growing at a CAGR of 6.8% over 2026-2031.

This report is Segmented by Device Category (Desktop PCs, Laptop PCs, Tablets, and More), End User Industry (Consumer, Small and Medium Enterprises, Large Enterprises, Education Sector, and More), Connectivity (Wired Devices, and Wireless Devices), Distribution Channel (Online Retail, Offline Retail, Direct B2B Sales, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America IT Device Market Trends and Insights

Surging Demand for Hybrid Work Hardware

Hybrid work remains entrenched, propelling sustained purchases of laptops, monitors, and webcams beyond the pandemic spike. Best Buy disclosed that computing and mobile products generated 49% of domestic revenue in its third fiscal-quarter 2026 report, with comparable sales up 7.6% year-on-year. Dell Technologies and HP both emphasized growing commercial PC pipelines, underscoring condensed refresh cycles as enterprises step down from five-year to three-year replacement intervals. Demand is strongest in the United States and Canada, where remote work penetration tops 40% of knowledge workers, while Mexico lags because of infrastructure limits. The resulting uplift accelerates unit volumes across premium notebooks equipped with neural processing units, ensuring local AI inference and compliance with data-sovereignty mandates. Consequently, the North America IT device market benefits from higher average selling prices on commercial SKUs, partially offsetting softness in entry-level consumer PCs.

Enterprise-Wide Device Refresh Post-Windows 10 End-of-Life

Microsoft withdrew Windows 10 support on 14 October 2025, triggering the largest enterprise PC replacement cycle since the Windows 7 sunset. Volume-licensing agreements from HP and Dell now bundle Windows 11 Pro with Copilot+ PCs based on Qualcomm Snapdragon X Elite or Intel Core Ultra processors, each embedding dedicated AI engines. Lenovo's ThinkPad X1 Carbon Gen 13 exemplifies the trend, pairing Intel silicon with on-device transcription agents unveiled at CES 2025. Public-sector procurement in the United States, Canadian provinces, and Mexican subsidiaries is releasing deferred budgets to ensure cybersecurity compliance, concentrating the impact in 2026-2027. As a result, the North America IT device market is experiencing front-loaded demand that lifts near-term revenues but may elongate future cycles.

Persistent Semiconductor Supply Imbalances

Structural shortages persist in high-bandwidth memory and advanced logic nodes despite easing headline constraints. Samsung announced DDR5 price hikes of up to 60% for 1Q 2025, citing tight supply linked to AI server demand. Micron echoed that memory scarcity will extend through 2027, diverting capacity away from consumer PCs. Export-control rules issued by the U.S. Bureau of Industry and Security in December 2024 and January 2025 further limit equipment access for Chinese fabs, stalling global wafer additions. Resulting lead-time volatility complicates production planning for device makers across North America, trimming projected growth in the North America IT device market.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated 5G Roll-Outs Fueling Smartphone Upgrades

- Edge-AI Integration into Laptops and PCs

- Inflation-Driven Price Sensitivity Among Consumers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wearables contributed a modest share in 2025 yet are projected to expand at a strong compound annual growth rate through 2031, making it the fastest-growing category among all IT device segments. Recent FDA guidance issued in early 2026 has eased regulatory barriers for low-risk health trackers, paving the way for accelerated adoption. Garmin's Fenix 8, equipped with advanced features like ECG and SpO2 sensors, caters to both athletes and first responders, addressing niche yet critical market needs. Additionally, continuous glucose monitors from companies such as Abbott, Medtronic, and Dexcom are integrating smartphone connectivity, creating deeper and more interconnected data ecosystems. These advancements highlight the growing importance of wearables in the broader IT device market, driven by innovation and regulatory support.

Smartphones, while remaining the largest segment of the North America IT device market, are experiencing a slowdown in growth as market penetration reaches saturation. In contrast, laptops and desktops are seeing incremental growth fueled by edge-AI upgrades, which enhance their functionality and appeal. Servers and storage devices are scaling up in density to meet the demands of AI workloads, as demonstrated by Seagate's high-capacity 30-TB Exos M drives. Peripherals continue to benefit from sustained demand driven by hybrid work environments, while point-of-sale terminals and industrial handheld devices remain critical components of the "other devices" category. Collectively, these shifts underscore a broader market pivot toward data-generating hardware that supports recurring analytics services, reflecting the evolving needs of businesses and consumers alike.

Healthcare is forecast to post a 10.6% CAGR between 2026 and 2031, outstripping the consumer segment that nevertheless retains the largest share. Hospitals are increasingly deploying rugged tablets for bedside charting and wearable monitors for remote patient surveillance, ensuring seamless integration with electronic health records under HIPAA safeguards. The aging population and rising prevalence of chronic diseases in the United States and Canada are driving the demand for continuous monitoring solutions. Additionally, small and medium enterprises are opting for cost-effective laptops, while large enterprises are standardizing AI-ready PCs managed through zero-trust security consoles to enhance operational efficiency and data security.

Education continues to see steady demand for Chromebooks and iPads, supported by digital-learning grants from Canadian provinces. Government agencies in the United States leverage multi-year GSA schedules, while similar contracts in Canada are enabling the modernization of IT device fleets. The BFSI sector is refreshing workstations to support real-time fraud analytics, ensuring compliance and operational agility. Meanwhile, manufacturing and energy verticals are adopting ruggedized PCs designed for harsh environments, addressing specific operational needs. These trends collectively highlight the evolving demand dynamics within the North America IT device market, driven by sector-specific requirements and technological advancements.

List of Companies Covered in this Report:

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Dell Technologies Inc.

- HP Inc.

- Lenovo Group Limited

- ASUSTeK Computer Inc.

- Acer Inc.

- Microsoft Corporation

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- LG Electronics Inc.

- Sony Group Corporation

- Panasonic Holdings Corporation

- Garmin Ltd.

- Zebra Technologies Corporation

- Fujitsu Limited

- Seagate Technology Holdings plc

- Western Digital Corporation

- Toshiba Electronic Devices and Storage Corporation

- Hisense Visual Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Hybrid Work Hardware

- 4.2.2 Enterprise-wide Device Refresh Cycles Post-Windows 10 End-of-Life

- 4.2.3 Accelerated 5G Roll-outs Fueling Smartphone Upgrades

- 4.2.4 Tax Incentives on Domestic Semiconductor Assembly in Mexico

- 4.2.5 Growing Adoption of XR-Ready Wearables for Training

- 4.2.6 Edge-AI Integration into Laptops and PCs

- 4.3 Market Restraints

- 4.3.1 Persistent Semiconductor Supply Imbalances

- 4.3.2 Inflation-Driven Price Sensitivity Among Consumers

- 4.3.3 Tightened U.S.-China Export Controls on Advanced Chips

- 4.3.4 Escalating E-waste Regulatory Compliance Costs

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Category

- 5.1.1 Desktop PCs

- 5.1.2 Laptop PCs

- 5.1.3 Tablets

- 5.1.4 Smartphones

- 5.1.5 Servers and Storage Systems

- 5.1.6 Wearable Devices

- 5.1.7 Peripheral Devices (Keyboards, Mice)

- 5.1.8 Other Device Categories

- 5.2 By End User Industry

- 5.2.1 Consumer

- 5.2.2 Small and Medium Enterprises

- 5.2.3 Large Enterprises

- 5.2.4 Education Sector

- 5.2.5 Government and Public Sector

- 5.2.6 Healthcare Sector

- 5.2.7 Retail and E-Commerce

- 5.2.8 BFSI

- 5.2.9 Other End User Industries

- 5.3 By Connectivity

- 5.3.1 Wired Devices

- 5.3.2 Wireless Devices

- 5.4 By Distribution Channel

- 5.4.1 Online Retail

- 5.4.2 Offline Retail

- 5.4.3 Direct B2B Sales

- 5.4.4 Value-Added Resellers

- 5.4.5 Telecom Carrier Stores

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Apple Inc.

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Dell Technologies Inc.

- 6.4.4 HP Inc.

- 6.4.5 Lenovo Group Limited

- 6.4.6 ASUSTeK Computer Inc.

- 6.4.7 Acer Inc.

- 6.4.8 Microsoft Corporation

- 6.4.9 Huawei Technologies Co., Ltd.

- 6.4.10 Xiaomi Corporation

- 6.4.11 LG Electronics Inc.

- 6.4.12 Sony Group Corporation

- 6.4.13 Panasonic Holdings Corporation

- 6.4.14 Garmin Ltd.

- 6.4.15 Zebra Technologies Corporation

- 6.4.16 Fujitsu Limited

- 6.4.17 Seagate Technology Holdings plc

- 6.4.18 Western Digital Corporation

- 6.4.19 Toshiba Electronic Devices and Storage Corporation

- 6.4.20 Hisense Visual Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球資訊科技(IT)網路市場報告

2026年全球資訊科技(IT)網路市場報告 IT設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區IT設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲IT設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲IT設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

IT設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區IT設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲IT設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲IT設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) ITaaS(資訊科技即服務)市場報告:按類型、應用和地區分類(2026-2034 年)2026年全球混合資訊科技(IT)管理市場報告2026年全球資訊科技(IT)營運管理軟體市場報告2026年全球資訊科技(IT)資產管理軟體市場報告

ITaaS(資訊科技即服務)市場報告:按類型、應用和地區分類(2026-2034 年)2026年全球混合資訊科技(IT)管理市場報告2026年全球資訊科技(IT)營運管理軟體市場報告2026年全球資訊科技(IT)資產管理軟體市場報告 超個人化技術市場規模、佔有率和趨勢分析報告:按組件、技術、應用、最終用途、地區和細分市場預測(2026-2033 年)

超個人化技術市場規模、佔有率和趨勢分析報告:按組件、技術、應用、最終用途、地區和細分市場預測(2026-2033 年)