|

市場調查報告書

商品編碼

2061753

歐洲IT設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Europe IT Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

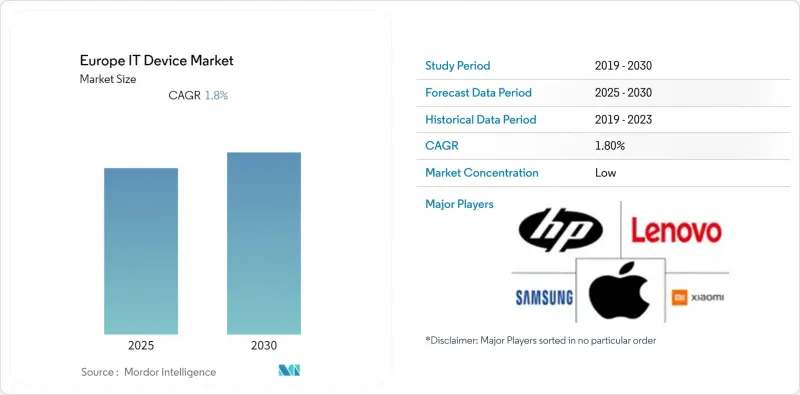

根據 Mordor Intelligence 預測,歐洲 IT 設備市場規模將從 2025 年的 2,100 億美元和 2026 年的 2,300 億美元成長到 2031 年的 3.32 兆美元,2026 年至 2031 年的年複合成長率(CAGR)為 7.5%。

本報告按裝置類型(智慧型手機、筆記型電腦、平板電腦、桌上型電腦和工作站、周邊設備)、最終用戶產業(一般消費者、企業、政府機構、教育機構)、通路(線上零售、實體零售等)、作業系統(Android、Windows等)和地區進行細分。市場預測以美元計價。

歐洲IT設備市場的趨勢與洞察

5G網路的擴展將加速智慧型手機的更換週期。

歐洲已部署79個獨立組網(SA)商用5G網路,支援倉庫自動化和基於擴增實境(AR)的現場服務等低延遲應用場景。德國通訊業者的目標是到2025年實現全國的SA覆蓋,從而幫助企業升級到支援網路切片的高效能5G終端。目前,5G終端的更新換代呈現出兩極分化的趨勢:富裕的都市區傾向選擇毫米波旗艦機型,而中等收入群體則在等待價格下降。 3GPP Release 18 RedCap規範將5G功能擴展到更換裝置和物聯網節點(ETSI.ORG)。因此,周邊設備製造商預計,能夠與這些網路同步的智慧型手錶和條碼掃描器的需求將會增加。

歐盟各國政府主導的數位化項目

「數位歐洲計畫」已累計13億歐元(約14.7億美元)用於2025年至2027年間的超級運算、人工智慧和網路安全領域的津貼。西班牙正利用其中37.5億歐元(約42.4億美元)的資金,透過其「西班牙數字2026」計畫改善當地電信基礎設施,並為中小企業提供設備補貼。波蘭、義大利和波羅的海國家也實施了類似的聯合資助計劃,指定採購在歐盟境內組裝的筆記型電腦和平板電腦,這為聯想波蘭工廠和戴爾愛爾蘭工廠創造了大量訂單的機會。這些要求正在鞏固多年的採購管道,並為歐洲IT設備市場創造可預測的需求前景。

在成熟市場,智慧型手機的更換週期正在延長。

隨著效能提升趨於平緩,且在許多市場設備價格超過 1000 歐元(1130 美元),設備更換週期已從 2019 年的 24-30 個月延長至 2025 年的 33-40 個月。 iOS 18 和 One UI 7 長達七年的軟體支援意味著安全漏洞不再是促使用戶購買新裝置的主要原因。歐盟對捆綁式行動電話和通訊套餐銷售利率的限制性規定減少了營運商的補貼,使得通訊業者的購買決策標準從每月現金流轉向終身成本。這些因素綜合起來將使歐洲 IT 設備市場的預期複合年成長率下降約 1 個百分點。

細分市場分析

預計平板電腦在2026年至2031年間將以8.58%的複合年成長率成長,成為所有外形規格中成長最快的,這主要得益於政府部門在課堂上推廣一對一平板電腦部署。智慧型手機在2025年仍將主導歐洲IT設備市場,佔46.43%的市場佔有率,但由於西歐市場飽和,年度更換有限,其銷售成長正在放緩。筆記型電腦將繼續在混合辦公室模式下發揮主導作用,受益於大容量電池和人工智慧最佳化晶片組。桌上型電腦和工作站則佔據電腦輔助設計(CAD)和量化金融等專業細分市場,在這些領域,散熱和多顯示器配置比便攜性更為重要。

在教育類競標中,Android 和 iPadOS 平板電腦憑藉其強大的行動裝置管理功能競爭,而基於 ChromeOS 的可拆卸裝置則因其較低的授權成本,在預算有限的競標中更具優勢。在法國,根據「數位教育領域」(Territoires Numeriques Educatifs)計劃,2025 年共交付了 13 萬台學生平板電腦。同年,西班牙也購買了 50 萬台設備。其中大部分是售價低於 300 歐元(339 美元)的 Chromebook,並配備了可離線使用的課程軟體。這些設備的部署提高了周邊設備的普及率,顯示器和觸控筆製造商目前正在為歐洲 IT 設備市場客製化課堂套裝。

預計到2031年,教育產業的複合年成長率將達到8.38%,超過所有其他用戶群。受智慧型手機和遊戲筆記型電腦的更換週期推動,消費者市場在2025年仍將佔據歐洲IT設備市場54.19%的佔有率,但隨著北歐國家IT設備擁有率接近飽和,其成長速度正在放緩。企業需求依然強勁,這得益於Windows 11硬體需求、零信任專案以及需要更高運算能力的ESG資訊揭露軟體。政府機構正受惠於歐盟復甦基金,但由於漫長的競標流程,進展較為緩慢。

歐洲社會基金Plus已撥款993億歐元(約1120億美元),用於在2021年至2027年間提升數位技能,重點在於提高職業學校的數位素養並加速技術應用。這筆資金旨在支持採購筆記型電腦、平板電腦和其他必要的IT設備,確保學生和教師能夠使用最新的工具進行高效學習。此外,義大利的「Piano Scuola 4.0」計畫已獲得21億歐元(約23.8億美元)的撥款,用於將傳統教室改造為智慧教室環境。該舉措包括投資互動顯示器、先進的教學輔助設備和全面的教師培訓項目,以加速教育領域的技術應用。這些系統性的專案能夠創造對IT設備的穩定需求,即使在需求波動時期,也能為歐洲IT設備市場的需求前景提供可視性和穩定性。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 混合辦公模式的日益普及推動了對行動運算。

- 5G網路的擴展正在加速智慧型手機的更換週期。

- 歐盟各國政府主導的數位化項目

- 電子商務通路的成長和設備可訪問性的提高

- 歐盟關於「維修權」的立法旨在促進模組化設計

- 人工智慧驅動的邊緣設備在智慧製造領域的崛起

- 市場限制因素

- 在成熟市場,智慧型手機的更換週期正在延長。

- 半導體供應鏈的波動性

- 歐盟永續發展法規導致合規成本增加

- 翻新產品銷售的擴張正在蠶食新產品的銷售。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依設備類型

- 智慧型手機

- 筆記型電腦

- 藥片

- 桌上型電腦和工作站

- 周邊設備(顯示器、鍵盤、滑鼠、印表機)

- 按最終用戶行業分類

- 消費者

- 公司

- 政府

- 教育

- 透過分銷管道

- 線上零售

- 實體零售

- 增值轉售商

- 直銷(OEM網路商店)

- 作業系統

- 安德維爾

- Windows

- iOS/iPadOS

- ChromeOS

- Linux

- 按地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Lenovo Group Limited

- HP Inc.

- Dell Technologies Inc.

- ASUSTeK Computer Inc.

- Acer Inc.

- Xiaomi Corporation

- Huawei Technologies Co., Ltd.

- Microsoft Corporation

- ASUS Cloud Corporation

- Logitech International SA

- Koninklijke Philips NV

- Fujitsu Limited

- Huawei Device Co., Ltd.

- OPPO Guangdong Mobile Communications Co., Ltd.

- Realme Chongqing Mobile Telecommunications Corp., Ltd.

- Sony Group Corporation

- TCL Technology Group Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe iT device market size is projected to expand from USD 0.21 trillion in 2025 and USD 0.23 trillion in 2026 to USD 3.32 trillion by 2031, registering a 7.58% CAGR between 2026 and 2031.

This report is Segmented by Device Type (Smartphones, Laptops and Notebooks, Tablets, Desktops and Workstations, and Peripherals), End-User Industry (Consumer, Enterprise, Government, and Education), Distribution Channel (Online Retail, Brick-And-Mortar Retail, and More), Operating System (Android, Windows, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe IT Device Market Trends and Insights

Expansion Of 5G Networks Accelerating Smartphone Refresh Cycles

Europe hosts 79 standalone 5G commercial networks, a footprint that enables low-latency use cases such as warehouse automation and augmented-reality field service. German operators finalized nationwide SA coverage in 2025, triggering enterprise upgrades to ruggedized 5G handsets capable of network slicing. Premium consumers in urban corridors adopt mmWave-ready flagships, while mid-tier users wait for prices to fall, creating a bifurcated refresh curve. The RedCap specifications in 3GPP Release 18 extend 5G capability to wearables and IoT nodes ETSI.ORG. Peripheral makers, therefore, see incremental demand for compatible smartwatches and barcode scanners that sync with those networks.

Government-Led Digitalization Programs Across The EU

The Digital Europe Program earmarked EUR 1.3 billion (USD 1.47 billion) for supercomputing, AI, and cybersecurity grants between 2025-2027. Spain channels EUR 3.75 billion (USD 4.24 billion) of that pool into rural connectivity and SME device subsidies under its Espana Digital 2026 plan. Poland, Italy, and the Baltic states run similar co-funded schemes that specify EU-assembled laptops and tablets, providing volume opportunities for Lenovo's Polish factory and Dell's Irish plant. These mandates anchor multi-year procurement pipelines and create predictable demand visibility for the Europe IT device market.

Lengthening Smartphone Replacement Cycles In A Maturing Market

Upgrade intervals widened to 33-40 months in 2025, up from 24-30 months in 2019, as performance gains flattened and devices crossed the EUR 1,000 (USD 1,130) threshold in many markets. Seven years of software support for iOS 18 and One UI 7 removes security obsolescence as a trigger to buy new models. EU rules that cap interest rates on bundled handset plans have weakened carrier subsidies, shifting decisions from monthly cashflow to lifetime cost. Collectively, these forces subtract nearly 1 percentage point from the projected CAGR of the Europe IT device market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption Of Hybrid Work Models Boosting Mobile Computing Demand

- Growth Of E-Commerce Channels Enhancing Device Accessibility

- Semiconductor Supply Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tablets are expected to post an 8.58% CAGR over 2026-2031, the quickest clip among form factors, as ministries enforce one-to-one ratios in classrooms. Smartphones, though still dominant with a 46.43% share of the Europe IT device market in 2025, are experiencing slower unit growth as saturation in Western Europe tempers annual upgrades. Laptops retain their role as the hybrid-work workhorse, benefiting from larger battery envelopes and AI-optimized chipsets. Desktops and workstations occupy specialized niches such as computer-aided design and quantitative finance, where thermal budgets and multi-monitor arrays matter more than portability.

In education tenders, Android and iPadOS tablets compete on depth of mobile device management, while ChromeOS-based detachables win budget-sensitive bids through lower licensing costs. France shipped 130,000 student tablets under its Territoires Numeriques Educatifs program in 2025. Spain procured 500,000 devices the same year, mostly sub-EUR 300 (USD 339) Chromebooks fitted with offline-capable curricula. These deployments lift peripheral attach rates, prompting monitor and stylus makers to tailor classroom bundles for the Europe IT device market.

The education vertical is forecast to record an 8.38% CAGR through 2031, outstripping all other user groups. The consumer segment retained 54.19% of the Europe IT device market in 2025, buoyed by smartphone cycles and gaming laptops, yet its growth rate is plateauing as ownership nears full penetration in Northern Europe. Enterprise demand remains resilient thanks to Windows 11 hardware prerequisites, zero-trust projects, and ESG disclosure software that requires higher compute headroom. Government agencies, although beneficiaries of EU recovery funds, advance at a steadier clip due to protracted tendering processes.

ESF Plus allocates EUR 99.3 billion (USD 112 billion) for digital skills from 2021-2027, focusing on enhancing digital literacy and fostering technological adoption across vocational schools. This funding supports the procurement of laptops, tablets, and other essential IT devices, ensuring that students and educators have access to modern tools for effective learning. Additionally, Italy's Piano Scuola 4.0 allocates EUR 2.1 billion (USD 2.38 billion) to transforming traditional classrooms into smart classroom environments. This initiative includes investments in interactive displays, advanced teaching aids, and comprehensive teacher training programs to facilitate the integration of technology into education. These structured programs provide a steady demand for IT devices, creating pipeline visibility and offering stability to the Europe IT device market, even during periods of fluctuating consumer demand.

List of Companies Covered in this Report:

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Lenovo Group Limited

- HP Inc.

- Dell Technologies Inc.

- ASUSTeK Computer Inc.

- Acer Inc.

- Xiaomi Corporation

- Huawei Technologies Co., Ltd.

- Microsoft Corporation

- ASUS Cloud Corporation

- Logitech International S.A.

- Koninklijke Philips N.V.

- Fujitsu Limited

- Huawei Device Co., Ltd.

- OPPO Guangdong Mobile Communications Co., Ltd.

- Realme Chongqing Mobile Telecommunications Corp., Ltd.

- Sony Group Corporation

- TCL Technology Group Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Hybrid Work Models Boosting Mobile Computing Demand

- 4.2.2 Expansion of 5G Networks Accelerating Smartphone Refresh Cycles

- 4.2.3 Government-Led Digitalisation Programmes Across the EU

- 4.2.4 Growth of E-Commerce Channels Enhancing Device Accessibility

- 4.2.5 EU Right-to-Repair Legislation Encouraging Modular Design

- 4.2.6 Emergence of AI-Enabled Edge Devices in Smart Manufacturing

- 4.3 Market Restraints

- 4.3.1 Lengthening Smartphone Replacement Cycles in a Maturing Market

- 4.3.2 Semiconductor Supply Chain Volatility

- 4.3.3 Heightened Compliance Costs Under EU Sustainability Rules

- 4.3.4 Growth of Refurbished Device Sales Cannibalising New Units

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type

- 5.1.1 Smartphones

- 5.1.2 Laptops and Notebooks

- 5.1.3 Tablets

- 5.1.4 Desktops and Workstations

- 5.1.5 Peripherals (Monitors, Keyboards, Mice, Printers)

- 5.2 By End-user Industry

- 5.2.1 Consumer

- 5.2.2 Enterprise

- 5.2.3 Government

- 5.2.4 Education

- 5.3 By Distribution Channel

- 5.3.1 Online Retail

- 5.3.2 Brick-and-Mortar Retail

- 5.3.3 Value-Added Resellers

- 5.3.4 Direct Sales (OEM Web-stores)

- 5.4 By Operating Systems

- 5.4.1 Android

- 5.4.2 Windows

- 5.4.3 iOS / iPadOS

- 5.4.4 ChromeOS

- 5.4.5 Linux

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Apple Inc.

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Lenovo Group Limited

- 6.4.4 HP Inc.

- 6.4.5 Dell Technologies Inc.

- 6.4.6 ASUSTeK Computer Inc.

- 6.4.7 Acer Inc.

- 6.4.8 Xiaomi Corporation

- 6.4.9 Huawei Technologies Co., Ltd.

- 6.4.10 Microsoft Corporation

- 6.4.11 ASUS Cloud Corporation

- 6.4.12 Logitech International S.A.

- 6.4.13 Koninklijke Philips N.V.

- 6.4.14 Fujitsu Limited

- 6.4.15 Huawei Device Co., Ltd.

- 6.4.16 OPPO Guangdong Mobile Communications Co., Ltd.

- 6.4.17 Realme Chongqing Mobile Telecommunications Corp., Ltd.

- 6.4.18 Sony Group Corporation

- 6.4.19 TCL Technology Group Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球資訊科技(IT)網路市場報告

2026年全球資訊科技(IT)網路市場報告 IT設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區IT設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美IT設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲IT設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

IT設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區IT設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美IT設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲IT設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) ITaaS(資訊科技即服務)市場報告:按類型、應用和地區分類(2026-2034 年)2026年全球混合資訊科技(IT)管理市場報告2026年全球資訊科技(IT)營運管理軟體市場報告2026年全球資訊科技(IT)資產管理軟體市場報告

ITaaS(資訊科技即服務)市場報告:按類型、應用和地區分類(2026-2034 年)2026年全球混合資訊科技(IT)管理市場報告2026年全球資訊科技(IT)營運管理軟體市場報告2026年全球資訊科技(IT)資產管理軟體市場報告 超個人化技術市場規模、佔有率和趨勢分析報告:按組件、技術、應用、最終用途、地區和細分市場預測(2026-2033 年)

超個人化技術市場規模、佔有率和趨勢分析報告:按組件、技術、應用、最終用途、地區和細分市場預測(2026-2033 年)